Cold Chain Packaging Market Overview: Growth Trajectory to $102.1 Billion by 2034

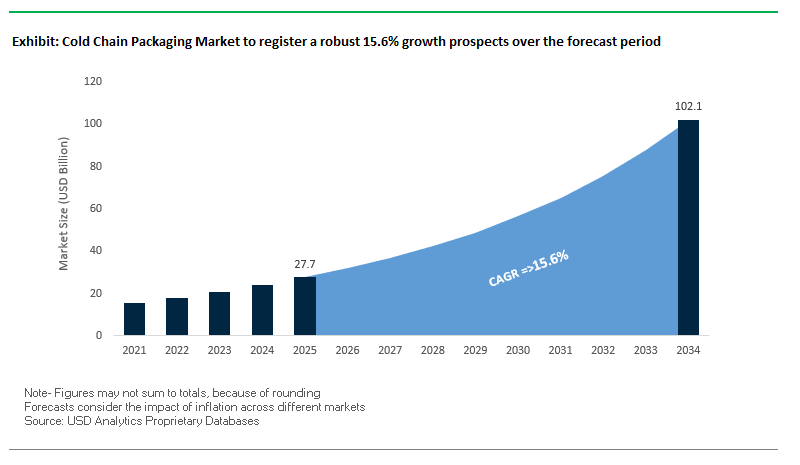

The global cold chain packaging market is projected to reach $27.7 billion in 2025 and expand to $102.1 billion by 2034, growing at a robust CAGR of 15.6%. This rapid growth underscores the market’s essential role in ensuring the safe and efficient movement of temperature-sensitive goods across pharmaceutical, food, and biotech supply chains. For industry professionals, the sector answers critical questions: How will biologics, vaccines, and high-value perishable foods be safeguarded? What sustainability models will dominate future packaging designs? And how will digitalization reshape cold chain monitoring and traceability?

Key Insights include:

- Pharmaceutical Sector Demand: The global pharmaceutical cold chain, valued at nearly $65 billion in 2025, is set to double over the next decade, driven by biologics and advanced therapies requiring stringent temperature controls.

- IoT and Real-Time Monitoring: IoT-enabled tracking with 1–5 minute interval monitoring is becoming standard, enhancing shipment integrity and risk management.

- Sustainability Imperative: The industry is shifting toward natural refrigerants, reusable systems, and high recycled content to meet ESG targets and regulatory mandates.

- Food Safety and Traceability: Regulations such as the U.S. FSMA Rule 204 require 24-hour traceability for high-risk foods, pushing adoption of traceability-ready packaging solutions.

Market Analysis: Key Developments Shaping Cold Chain Packaging in 2025

The cold chain packaging market is undergoing transformative change, powered by sustainability goals, mergers, and digital innovations. The industry is witnessing intensified competition as companies expand geographically and adopt new materials and monitoring technologies.

In September 2025, Cold Chain Technologies expanded operations in the Asia Pacific, opening hubs in Tokyo and Mumbai to meet surging pharmaceutical and biotech demand. Earlier, in August 2025, an industry report underscored the rise of AI and predictive analytics in cold chain logistics, highlighting applications such as predictive maintenance, optimized delivery routes, and demand forecasting, all aimed at lowering costs and improving reliability.

A landmark event occurred in July 2025, when Smurfit Kappa merged with WestRock to form Smurfit WestRock, creating a packaging giant with significant implications for cold chain services, particularly in corrugated and paper-based thermal solutions. The same month, reports revealed growing demand for single-use cold chain packaging for small-volume biologics shipments, reflecting cost-effectiveness and practicality.

Earlier in June 2025, Sonoco finalized its merger with Eviosys, strengthening its metal packaging capabilities, while industry sources also noted increasing adoption of passive thermal packaging for e-commerce-driven last-mile delivery. In May 2025, the focus turned to cold storage modernization, with global summits emphasizing energy-efficient refrigeration, insulation upgrades, and renewable energy integration. Meanwhile, in April 2025, a pharmaceutical partnership piloted reusable clinical trial containers, marking a critical step toward scalable, sustainable cold chain packaging.

Trends and Opportunities Shaping the Future of the Cold Chain Packaging Market

Strategic Shift from Single-Use EPS to Sustainable and Reusable Systems

The cold chain packaging market is witnessing a paradigm shift from expanded polystyrene (EPS) single-use formats toward reusable, recyclable, and circular models, spurred by regulatory mandates and corporate ESG commitments. Traditional EPS packaging, long criticized for its poor recyclability and landfill accumulation, is being rapidly replaced with curbside-recyclable insulation systems and durable reusable solutions.

Corporate investments are accelerating this transition. Cold Chain Technologies, through its acquisition of Packaging Technology Group (PTG), expanded its portfolio to include sustainable, recyclable packaging tailored for pharmaceuticals. This reflects a broader strategy to align packaging innovation with life sciences’ sustainability needs. Similarly, Peli BioThermal’s Crēdo Go line has demonstrated how rental and pooling systems deliver not only environmental benefits but also operational efficiency, cutting waste while optimizing total cost of ownership.

The regulatory landscape is amplifying this momentum. The EU Packaging and Packaging Waste Regulation (PPWR) mandates significant increases in recyclable and reusable content, pushing pharmaceutical and food logistics stakeholders to redesign cold chain systems. For companies facing compliance costs under Extended Producer Responsibility (EPR) frameworks, shifting to circular packaging is now as much a financial necessity as it is an environmental strategy.

Integration of IoT and Real-Time Condition Monitoring as a Standard Service

Cold chain packaging has evolved into a smart, data-driven solution that ensures integrity and compliance across the supply chain. IoT sensors are now being embedded into containers and insulation systems to provide continuous monitoring of critical parameters such as temperature, humidity, and shock exposure. This represents a shift from passive packaging insulation to active, verifiable condition monitoring as a standard offering.

The relevance of real-time monitoring was highlighted during Pfizer’s COVID-19 vaccine distribution, where IoT-powered sensors and cloud-based data systems ensured ultra-cold temperature compliance from production to delivery. Beyond compliance, predictive analytics derived from sensor data now enable companies to identify high-risk shipping routes, predict excursions, and optimize logistics proactively, reducing spoilage and losses in high-value pharmaceutical shipments.

Development of High-Performance, Sustainable Insulation Materials

One of the most pressing opportunities lies in the R&D of insulation materials that deliver high thermal performance while eliminating reliance on environmentally harmful plastics. Research on bio-based foams and aerogels is paving the way for sustainable solutions that rival EPS in insulation but decompose naturally or integrate seamlessly into recycling streams. For instance, Fiberwood, a Finnish startup, has secured funding to scale wood fiber–based insulation for both building and cold chain packaging markets, highlighting cross-industry potential.

Another promising area is vacuum-insulated panels (VIPs), which offer superior thermal efficiency, thinner walls, and increased payload capacity. While higher in cost, VIPs provide long-term savings by reducing transportation volumes, emissions, and product losses. With cost curves expected to decline as adoption scales, sustainable insulation materials are positioned to become the defining innovation in premium cold chain applications such as biologics, gene therapies, and high-value perishable goods.

Standardization and Interoperability for a Scalable Reusable Ecosystem

The fragmented nature of reusable cold chain packaging currently limits scalability. Developing standardized container sizes, material specifications, and interoperability protocols presents a transformative opportunity to create multi-party pooling networks. Standardization would allow participants across pharmaceuticals, food, and logistics to use a shared reverse logistics infrastructure, significantly improving asset utilization and reducing operational costs.

A public-private partnership (PPP) model could catalyze this effort by aligning government oversight with private sector innovation. This approach would provide regulatory clarity, encourage industry-wide adoption, and reduce barriers for smaller players. Furthermore, shared logistics networks for collection, cleaning, and redistribution would address one of the most significant challenges in reusable packaging: the complexity and cost of reverse logistics.

Competitive Landscape: Leading Companies in Cold Chain Packaging

The cold chain packaging market is characterized by a mix of global leaders and niche specialists, each innovating to strengthen sustainability, digitalization, and service networks.

Sonoco Products Company (Sonoco ThermoSafe)

Sonoco ThermoSafe leverages its parent company’s global reach to deliver a diverse range of temperature-controlled packaging solutions. With strengths in single-use and reusable containers, the company has built a reputation in pharmaceuticals and biotech. The acquisition of Eviosys in June 2025 has broadened its packaging capabilities and geographic footprint. Its PharmaTherm series offers precise control for biologics, while its reuse program supports circular economy goals by refurbishing and redeploying containers.

Peli BioThermal

Peli BioThermal specializes in high-performance, reusable thermal packaging for life sciences and healthcare. Its Crēdo Cube Dry Ice shippers demonstrate innovation in ultra-low temperature protection, maintaining conditions for over 144 hours. The company’s global refurbishing network underscores its focus on reusability and sustainability, ensuring reduced waste and extended asset life. Peli remains a trusted partner for clinical trials and cell and gene therapy logistics.

Cold Chain Technologies (CCT)

CCT offers end-to-end thermal packaging integrated with digital monitoring platforms. Its acquisition of Tower Cold Chain in 2024 expanded its reusable solutions, while its 2025 expansion in Asia Pacific highlights its global ambitions. Through its CCT Smart Solutions platform, the company provides real-time visibility of shipments, reinforcing reliability and compliance for pharmaceutical clients worldwide.

Sealed Air Corporation

Sealed Air has a diversified packaging portfolio with strong positions in food and healthcare. Its Cryovac brand offers shrink films and bags that extend the shelf life of perishables, addressing food safety and efficiency. Sealed Air is heavily investing in curbside recyclable packaging and automation solutions, aligning with both sustainability and e-commerce growth trends.

va-Q-tec AG

va-Q-tec is known for its vacuum insulation panel (VIP) technology and innovations in phase-change materials that enable shipment at -70°C without dry ice. Widely used in pharma and life sciences, its va-Q-tainer and va-Q-box solutions are valued for long-duration performance and reusability. With its global rental network, the company advances circular economy practices while ensuring cost-efficient cold chain logistics.

Cold Chain Packaging Market Share Insights

Insulated Containers Dominate Market Share by Product Type

Insulated containers (shippers) hold the largest share of the global cold chain packaging market at 40% in 2025, reflecting their indispensable role in parcel-level distribution of temperature-sensitive goods. These containers both reusable and single-use are the backbone of pharmaceutical logistics, especially in transporting biologics, vaccines, and clinical trial materials. Their widespread use is driven by the need for precise thermal regulation and secure delivery via parcel carriers like FedEx, DHL, and UPS. Temperature-controlled pallet shippers, accounting for 25% of the market, serve as the bulk logistics anchor, facilitating wholesale movements of vaccines, APIs, and perishable foods in large volumes while maximizing cost efficiency per unit shipped. Refrigerants such as gel packs and advanced Phase Change Materials (PCMs) form the active core of all cold chain systems, ensuring exact thermal ranges from 2–8°C or as low as -20°C are consistently maintained. Their growing adoption is fueled by their superior performance over traditional ice packs. Monitoring devices, though representing a smaller revenue share, are growing the fastest, as real-time data logging and GPS-enabled tracking have become non-negotiable for compliance, liability reduction, and supply chain transparency. Protective liners and thermal blankets occupy a niche but crucial role, offering cost-effective solutions for less sensitive products or as supplemental thermal protection in multimodal logistics. Together, these product categories highlight how functionality, compliance, and innovation converge to define market share dynamics.

Pharmaceuticals Continue to Command the Largest Market Share by Application

Pharmaceuticals and healthcare lead the cold chain packaging market with a 55% share in 2025, underscoring their high-value, high-stakes role in global logistics. This segment is propelled by the rising demand for mRNA vaccines, oncology therapies, cell and gene treatments, and biologics, where even minor temperature deviations can cause product loss worth millions. Regulatory compliance requirements by FDA, EMA, and WHO further reinforce the dominance of pharmaceutical-driven cold chain innovation. Food and beverages represent 35% of the market, acting as the largest volume consumer of cold chain packaging. Applications include fresh produce, seafood, dairy, and frozen meals, where shelf-life extension and food safety are paramount. Cost sensitivity in this segment pushes manufacturers toward efficiency-driven packaging designs that balance performance with affordability. Chemicals remain a specialized but critical niche, with applications in temperature-sensitive reagents, enzymes, and industrial chemicals that require corrosion-resistant or explosion-proof packaging systems. Although smaller in share, their high-value shipments demand precision-engineered protective solutions. Other applications, including cosmetics, horticulture, and select electronics, are emerging as growth frontiers, reflecting how more industries are recognizing the value of thermal-controlled logistics for product quality assurance. This shift indicates that cold chain packaging demand will continue to diversify beyond its traditional pharmaceutical and food strongholds.

United States: Biopharma Leadership and Smart Cold Chain Packaging Transforming the Market

The United States cold chain packaging market is strongly driven by its global leadership in biopharmaceuticals, life sciences, and advanced healthcare. The transportation of sensitive products such as vaccines, biologics, and cell and gene therapies requires strict temperature-controlled packaging solutions, making the U.S. one of the most critical markets worldwide. Innovation is evident in the adoption of sustainable cold chain materials, including phase change materials (PCMs) and vacuum insulated panels (VIPs), which offer enhanced thermal efficiency. At the same time, the commercialization of curbside recyclable and biodegradable parcel shippers is aligning with corporate ESG commitments and consumer demand for eco-friendly solutions.

Smart cold chain packaging is another defining trend in the U.S. Companies are rapidly adopting IoT-enabled sensors, RFID tags, and data loggers to ensure real-time visibility of temperature, humidity, and product location across the supply chain. These technologies mitigate risks, prevent spoilage, and build trust in pharmaceutical distribution. Strategic collaborations are also shaping the landscape, such as Cold Chain Technologies’ partnership with VPL Rx, which integrates advanced thermal packaging into pharmacy logistics. This combination of innovation, sustainability, and technology integration positions the U.S. as a global frontrunner in cold chain packaging solutions.

Germany: EU Regulations and Passive Cold Chain Packaging Driving Market Evolution

Germany’s cold chain packaging industry is heavily influenced by strict European Union guidelines, particularly the Good Distribution Practice (GDP) standards mandated by the European Medicines Agency. These regulations emphasize validated containers, continuous temperature monitoring, and full compliance during distribution, pushing companies to adopt high-performance cold chain solutions. Passive packaging systems, which do not rely on active refrigeration, are particularly in demand due to their reliability and cost-effectiveness across multiple temperature ranges—from chilled to cryogenic.

In addition, Germany’s world-class logistics infrastructure is being enhanced by automation and robotics tailored for temperature-sensitive goods. Automated warehouse management and advanced sorting systems improve handling precision while reducing errors in pharmaceutical and food shipments. With regulatory rigor, cutting-edge logistics, and industry-wide innovation, Germany has positioned itself as a model market for advanced cold chain packaging in Europe.

China: Expanding Food and Pharma Sectors Driving Cold Chain Packaging Innovation

China’s cold chain packaging market is expanding rapidly due to growth in the pharmaceutical, food, and beverage sectors. Rising consumer demand for online groceries, ready-to-eat meals, and fresh produce requires robust packaging that ensures product integrity across long distances. Simultaneously, the pharmaceutical sector is investing heavily in cold chain logistics to support the distribution of biologics and vaccines, further boosting demand for reliable cold chain packaging solutions.

Government initiatives focused on food safety have become a key catalyst. By tightening regulations and enforcing strict compliance, China is driving investments into modern cold chain logistics infrastructure. At the same time, technological adoption is reshaping the market, with RFID-enabled packaging and IoT-based traceability tools allowing for real-time monitoring and better quality assurance. This combination of regulatory support, consumer demand, and digital adoption makes China a high-growth market for cold chain packaging worldwide.

India: Government Programs and Pharma Exports Fueling Cold Chain Packaging Demand

India’s cold chain packaging market is accelerating under strong government initiatives and the rapid expansion of its pharmaceutical and agricultural sectors. The Integrated Cold Chain and Value Addition Infrastructure scheme, part of the Pradhan Mantri Kisan Sampada Yojana (PMKSY), provides funding support for storage facilities, reefer trucks, and packaging solutions. This has significantly boosted demand for cold chain packaging across perishable food, fruit, vegetable, and pharma supply chains.

India’s dual role as a global pharmaceutical powerhouse and a leading exporter of fresh produce requires a mix of passive and active temperature-controlled packaging to maintain product safety during domestic and international shipments. Major companies, including Cold Chain Technologies, are making strategic investments, such as setting up new facilities in Mumbai, to meet the growing demand. This alignment of government support, industry growth, and private investment makes India one of the fastest-growing cold chain packaging markets globally.

Brazil: Agriculture Exports and Food Safety Regulations Strengthening Cold Chain Packaging

Brazil’s cold chain packaging market is primarily shaped by its position as one of the world’s largest agricultural producers and exporters. Meat, poultry, seafood, and fresh vegetables require temperature-controlled packaging solutions to preserve quality during long-haul transport, both domestically and internationally. As global demand for Brazilian agri-food exports grows, cold chain packaging has become a vital enabler of the country’s trade competitiveness.

The Brazilian government is actively funding food safety and cold chain infrastructure projects to modernize the industry. This push is complemented by rising adoption of IoT-enabled monitoring tools and fleet management systems, which enhance operational efficiency and ensure regulatory compliance. By integrating advanced technologies into logistics and packaging, Brazil is strengthening its ability to deliver high-quality products to global markets, making it a critical player in the Latin American cold chain packaging landscape.

Japan: Pharmaceutical Regulations and Precision Packaging Driving Market Growth

Japan’s cold chain packaging industry is defined by its stringent pharmaceutical regulations and emphasis on quality. The Pharmaceuticals and Medical Devices Agency (PMDA) and the Ministry of Health, Labour and Welfare (MHLW) impose strict guidelines on pharmaceutical cold chain distribution, ensuring safety and efficacy. As the country expands into advanced biologics, cell therapies, and precision medicines, demand for highly reliable and validated cold chain packaging has grown exponentially.

Japanese companies prioritize high-quality packaging materials and designs that guarantee consistent temperature control and prevent even minimal deviations that could compromise product safety. Strategic investments in advanced logistics infrastructure, including temperature-controlled warehouses and distribution systems, further support this precision-driven market. With its blend of strict regulations, high consumer expectations, and a commitment to innovation, Japan continues to set benchmarks for cold chain packaging excellence in Asia.

Cold Chain Packaging Market Report Scope

Cold Chain Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.7 Billion

|

|

Market Size (2034)

|

$102.1 Billion

|

|

Market Growth Rate

|

15.6%

|

|

Segments

|

By Product (Insulated Containers, Refrigerants, Temperature-Controlled Pallet Shippers, Protective Liners & Thermal Blankets, Monitoring Devices), By Application (Pharmaceuticals & Healthcare, Food & Beverages, Chemicals, Other Applications), By Temperature Range (Chilled, Frozen, Ambient, Deep Frozen), By Usability (Reusable, Single-use)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sealed Air Corporation, Cold Chain Technologies, Pelican BioThermal, Softbox Systems, DS Smith plc, Sonoco Products Company, Envirotainer, Schaefer Systems International, Inc., Cryopak Industries Inc., Sofrigam SA, B Medical Systems, ACH Foam Technologies, Inc., Placon, Cold Chain Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cold Chain Packaging Market Segmentation

By Product

- Insulated Containers

- Refrigerants

- Temperature-Controlled Pallet Shippers

- Protective Liners & Thermal Blankets

- Monitoring Devices

By Application

- Pharmaceuticals & Healthcare

- Food & Beverages

- Chemicals

- Other Applications

By Temperature Range

- Chilled

- Frozen

- Ambient

- Deep Frozen

By Usability

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Cold Chain Packaging Market

- Sealed Air Corporation

- Cold Chain Technologies

- Pelican BioThermal

- Softbox Systems

- DS Smith plc

- Sonoco Products Company

- Envirotainer

- Schaefer Systems International, Inc.

- Cryopak Industries Inc.

- Sofrigam SA

- B Medical Systems

- ACH Foam Technologies, Inc.

- Placon

- Cold Chain Group

* List Not Exhaustive

Research Coverage

This report investigates the global cold chain packaging market, providing an in-depth review of innovations, sustainability breakthroughs, and strategic developments shaping the sector. USDAnalytics’ analysis reviews both historical trends from 2021 to 2024 and forecast data from 2025 to 2034, highlighting opportunities in reusable solutions, IoT-enabled real-time monitoring, and advanced insulation materials. The report also evaluates regulatory impacts, cross-industry adoption, and competitive dynamics, making it an essential resource for industry professionals, packaging engineers, supply chain managers, and decision-makers seeking insights into market growth drivers, strategic partnerships, and technology-led transformations. Through a combination of quantitative analysis, company profiling, and market trend evaluation, this report identifies emerging areas of growth such as sustainable insulation, smart packaging, and standardization for scalable reusable ecosystems.

Scope Highlights:

- Segmentation: By Product (Insulated Containers, Refrigerants, Temperature-Controlled Pallet Shippers, Protective Liners & Thermal Blankets, Monitoring Devices); By Application (Pharmaceuticals & Healthcare, Food & Beverages, Chemicals, Other Applications); By Temperature Range (Chilled, Frozen, Ambient, Deep Frozen); By Usability (Reusable, Single-use)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data from 2021 to 2024; forecast data from 2025 to 2034.

- Companies: In-depth analysis and profiles of 15+ key players, including Sealed Air Corporation, Cold Chain Technologies, Pelican BioThermal, Softbox Systems, DS Smith plc, Sonoco Products Company, Envirotainer, Schaefer Systems International, Cryopak Industries Inc., Sofrigam SA, B Medical Systems, ACH Foam Technologies, Inc., Placon, and Cold Chain Group.

Methodology

This report employs a multi-faceted research methodology combining primary and secondary data sources to provide a holistic analysis of the cold chain packaging market. Primary research involved interviews with senior executives, packaging engineers, and supply chain managers from leading companies to validate industry trends, technology adoption, and regulatory impacts. Secondary research sources included industry publications, trade journals, government regulations, corporate annual reports, and proprietary databases. Quantitative models were applied to project historical and forecast market sizes, CAGR, and segment growth, while qualitative analysis reviewed sustainability initiatives, IoT integration, and reusable packaging strategies. Competitive landscape assessment includes mergers, acquisitions, and strategic partnerships, enabling professionals to understand both current market positioning and future opportunities. All insights are synthesized to offer actionable intelligence for decision-makers in pharmaceuticals, food, and high-value logistics.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.