Market Overview: Insulated Shippers Market to Reach $19.7 Billion by 2034 on Pharma Cold Chain Demand and Advanced Insulation

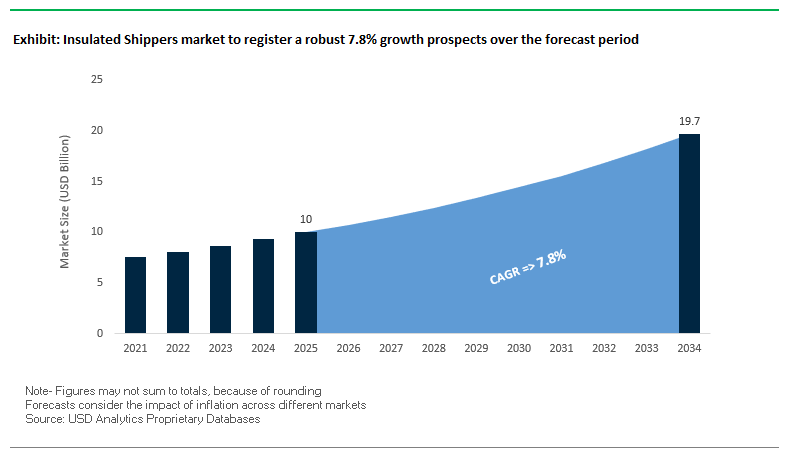

The global insulated shippers market is valued at $10 billion in 2025 and is projected to reach $19.7 billion by 2034, growing at a robust CAGR of 7.8%. The sector is a cornerstone of the global cold chain industry, ensuring safe transport of temperature-sensitive pharmaceuticals, biologics, food, and specialty chemicals. For buyers and industry professionals, the market answers pressing questions: Which technologies offer the longest protection? Should buyers invest in reusable or single-use formats? And how are digital tools reshaping shipment integrity?

Key Insights for Industry Stakeholders

- Pharmaceuticals as the core driver: Demand is surging for both active (powered) and passive (non-powered) shippers in biologics, vaccines, and cell & gene therapy logistics.

- Reusable vs. single-use dynamics: Reusable containers offer lifecycle cost savings and sustainability benefits, while single-use shippers dominate last-mile and small-lot shipments.

- Shift to high-performance insulation: Vacuum insulated panels (VIPs) and phase change materials (PCMs) are replacing EPS foam, providing lighter yet superior thermal performance.

- Smart, connected cold chain: IoT sensors and real-time monitoring are standardizing compliance, ensuring visibility of temperature, humidity, and location data across logistics.

Market Analysis: Strategic Acquisitions and Sustainability Goals Redefine Insulated Shippers (2024–2025)

The insulated shippers market is undergoing rapid transformation as pharma cold chain stakeholders demand higher performance and sustainability. In August 2025, CSafe Global released a whitepaper on vacuum insulation panels (VIPs), underscoring their growing role in transporting high-value biologics and extending long-duration temperature stability. The same month, Amcor reported a 43% YoY revenue increase in Q4 2025, reflecting the integration of Berry Global’s cold chain expertise into its portfolio.

Sustainability credentials are increasingly used as competitive differentiators. In July 2025, Peli BioThermal earned an EcoVadis Silver rating, placing it in the top 15% of companies assessed globally, while International Paper completed its acquisition of DS Smith, creating a sustainable packaging leader with implications for insulated paper-based solutions. Earlier in August 2024, Softbox Systems was recognized with a major sustainability award for its advancements in reusable insulated packaging a sign that environmental impact is now a boardroom-level priority in the cold chain sector.

Innovation pipelines remain robust. Peli BioThermal (February 2025) expanded its dry ice shipper portfolio capable of keeping payloads at ultra-low temperatures for 144+ hours. Similarly, CSafe (October 2024) launched its CGT Ultra D Dewar, engineered for cell and gene therapy shipments at -70°C for over 37 days a breakthrough for highly sensitive materials. These launches illustrate the trend toward specialized insulated containers that meet the evolving needs of biologics and advanced therapies.

Trends and Opportunities Transforming the Insulated Shippers Market

Accelerated Adoption of Curbside-Recyclable Insulated Materials

The insulated shippers market is witnessing a fundamental material transformation as regulatory bans and brand sustainability pledges converge to phase out expanded polystyrene (EPS). Across the U.S., as of June 2024, 11 states and over 250 cities and counties have either banned or restricted EPS, pushing manufacturers toward curbside-recyclable alternatives. Companies like ProAmpac are leading the transition with innovations such as FiberCool, a curbside recyclable insulated bag introduced in mid-2024. Designed from a single-piece paper structure, FiberCool eliminates assembly steps, reduces material use, and lowers costs, while maintaining insulation efficiency for e-commerce and cold chain applications.

This regulatory shift is also driving adoption of bio-based foams and fiber insulation. For instance, Nature-Pack’s Fibrease® cellulose wood foam, launched in late 2024, provides insulation performance comparable to EPS but is made from FSC-certified cellulose fiber, giving brands an environmentally friendly alternative that satisfies both consumers and regulators. The trend toward recyclable and biodegradable insulation is now viewed as a non-negotiable standard, ensuring that insulated shipper manufacturers align with circular economy goals while meeting stringent packaging waste directives.

Integration of Phase Change Materials (PCMs) for Precision Temperature Control

As the cold chain becomes increasingly complex, insulated shippers are incorporating bio-based, non-toxic Phase Change Materials (PCMs) to meet the rigorous demands of pharmaceuticals, diagnostics, and premium food delivery. The World Health Organization (WHO) has repeatedly emphasized that over 50% of vaccines globally are wasted due to cold chain failures, making precision-controlled packaging an industry priority. PCMs outperform traditional ice packs or dry ice by maintaining specific ranges (e.g., 2°C to 8°C) for extended durations, ensuring compliance with healthcare standards.

Beyond vaccines, advanced PCMs have been engineered to maintain ultra-low temperatures (−78°C to −65°C), catering to biologics and specialty medicines. Their versatility also extends to hot food logistics, with some PCMs maintaining stable temperatures of 55°C for last-mile meal delivery. This adaptability underscores PCMs’ role as a disruptive enabler in both healthcare and food sectors, redefining insulated shippers as precision thermal management systems rather than simple passive containers.

Development of IoT-Enabled “Smart Shipper” Platforms for Real-Time Monitoring

A major opportunity lies in transitioning from passive packaging to IoT-enabled insulated shippers that provide real-time visibility, compliance, and proactive risk management. Wireless sensors, RFID tags, and GPS modules are now being embedded in insulated packaging, creating connected “smart shippers” capable of continuously monitoring temperature, location, and handling conditions. These devices feed data to cloud platforms, giving logistics managers an auditable digital trail essential for regulatory compliance under FDA and WHO guidelines.

The advantages extend beyond compliance proactive alerts allow intervention before damage occurs. For example, a shipment of biologics can trigger an automated notification if temperatures rise above the 8°C threshold, enabling immediate corrective action. In clinical trial logistics, where data integrity and product safety are paramount, smart shippers offer verifiable proof of condition at every stage of transit. This transforms insulated packaging from a cost center into a compliance and risk-management tool, creating significant growth potential for suppliers who integrate IoT seamlessly into their solutions.

Expansion of Reusable and Returnable Pooling Systems for Urban Delivery Networks

Reusable insulated shippers are gaining momentum as dense urban delivery ecosystems particularly meal kits, grocery services, and courier-based cold chains demand sustainable, cost-effective solutions. Unlike single-use EPS or film-based coolers, reusable pooling systems are engineered for durability and integrated with reverse logistics models, ensuring they can be collected, sanitized, and redeployed multiple times.

For example, Sonoco ThermoSafe has introduced reusable shipping containers equipped with UV sanitization systems, ensuring regulatory compliance for healthcare shipments while cutting down on packaging waste. Meal kit providers are also adopting modular, passive shippers that optimize space within urban delivery vehicles while eliminating the need for active refrigeration. This model significantly reduces energy use, operational costs, and landfill burden, while enhancing the brand’s ESG profile.

Reusable pooling also eliminates consumer end-of-life responsibility, simplifying recycling complexities and reinforcing circular supply chains. With high-frequency, predictable delivery routes becoming the norm in urban centers, reusable insulated shippers are emerging as a cornerstone of last-mile cold chain sustainability.

Competitive Landscape: Pharma Cold Chain Leaders Drive Innovation, Sustainability, and Digital Integration

The insulated shippers market is dominated by a consolidated group of specialized players that balance thermal performance, regulatory compliance, and sustainability. Competition is driven by R&D in insulation technology, reusable vs. single-use designs, and digital monitoring integration.

Peli BioThermal Expanding dry ice shippers with long-duration payload protection

Peli BioThermal is a global leader in passive insulated packaging, with a strong portfolio of reusable Crēdo® shippers and dry ice solutions. In 2025, it launched the Credo Cube Dry Ice series, leveraging VIP technology to extend frozen protection beyond 144 hours. The company’s EcoVadis Silver award confirms its sustainability credentials. With its global rental program and lifecycle cost advantages, Peli is positioned as a leading partner for pharmaceutical cold chain logistics.

CSafe Global Pioneering active and passive solutions for biologics and therapies

CSafe provides a full suite of active and passive cold chain systems, including air cargo containers and Dewar solutions. Its CGT Ultra D Dewar (October 2024) sets a benchmark for cell and gene therapy logistics with 37-day -70°C performance. In May 2025, CSafe appointed a Chief Product Officer to drive innovation, signaling its commitment to next-gen pharma packaging. With integrated IoT monitoring via CSafe Connect, it delivers real-time shipment visibility, strengthening regulatory compliance and patient safety.

Softbox Systems Sustainability leader in reusable and recyclable insulated packaging

Softbox specializes in high-performance passive shippers for pharma and biotech industries. Recognized in August 2024 with a sustainability award, Softbox has pioneered paper-based solutions (ClimaCell®) and reusable formats aligned with circular economy goals. Its strength lies in balancing thermal compliance with environmental stewardship, appealing to brands under pressure to decarbonize supply chains.

Sonoco Products Company Scaling ThermoSafe brand with diversified cold chain solutions

Sonoco delivers insulated packaging under its ThermoSafe® brand, covering both single-use and reusable systems. Following its acquisition of Eviosys (December 2024), Sonoco expanded its material expertise into metal packaging, complementing its cold chain product line. With offerings like EnviroTainer® and Orion®, Sonoco focuses on durability, compliance, and cost-effectiveness, serving pharmaceutical and food segments alike.

Sealed Air Corporation Combining cushioning and insulation for versatile cold chain protection

Sealed Air, known for its protective packaging innovation, integrates insulation into bubble cushioning and foam-in-place systems that reflect up to 97% radiant energy. Its solutions serve both food and pharma cold chains, reducing spoilage and extending shelf life. The company’s strategic vision centers on designing recyclable packaging with higher recycled content, while its global brand equity gives it strong leverage across industries adopting insulated shipping.

Insulated Shippers Market Share Insights

Single-Use Insulated Shippers Dominate Market Share by Product Type

In the insulated shippers industry, single-use insulated shippers hold a commanding 65% share in 2025, making them the backbone of temperature-controlled logistics. Their leadership is due to simplicity, reliability, and cost-efficiency: they remove the complexities of reverse logistics, guarantee sterility and integrity for each shipment, and are adaptable with phase-change materials for temperature ranges from frozen (-18°C) to chilled (2–8°C). Active temperature-control containers represent a smaller but rapidly growing share, especially for high-value biopharmaceuticals and cell therapies requiring ultra-cold conditions such as -70°C or cryogenic environments. Although cost-intensive, they are indispensable for long-haul international shipping and ultra-sensitive payloads. Multiple-use shippers remain the smallest category, viable only within closed-loop supply chains where return and revalidation are economically feasible. This segmentation illustrates how single-use dominates for scale, active systems expand through precision and long-haul reliability, and reusables remain confined to specialized networks.

Pharmaceuticals & Biologics Anchor Insulated Shippers Market Share by Application

Pharmaceuticals and biologics account for 55% of the insulated shippers market in 2025, making them the undisputed anchor application. Global vaccine distribution, biologic drugs, and temperature-sensitive treatments drive massive demand for reliable cold chain packaging under strict FDA and EMA regulations. Clinical trials and cell/gene therapies represent the fastest-growing segment, commanding premium value as these shipments require deep cryogenic storage (-150°C to -196°C) and meticulous chain-of-custody protocols. Food and beverages, though less stringent in requirements, contribute significant volume by relying on EPS boxes and gel packs for seafood, meat, and gourmet products. Meanwhile, chemicals and other applications serve niche industrial needs, such as transporting reagents and diagnostic materials, though they remain comparatively fragmented. This application breakdown underscores how life sciences dominate insulated shipper demand, food provides steady volume, and advanced therapies drive the frontier of innovation and profitability.

United States: Regulatory Push and Technological Innovations Driving High-Performance Insulated Shippers

The U.S. insulated shippers market is experiencing strong growth due to regulatory pressures from the FDA aimed at ensuring cold chain integrity, particularly for pharmaceuticals, biologics, and decentralized clinical trials. These regulations have heightened the need for high-performance insulated shippers that maintain temperature and preserve product efficacy during last-mile delivery. Sustainability is another key driver, with manufacturers developing shippers from post-consumer recycled (PCR) plastics and paper-based alternatives. Legislative measures, including bans on expanded polystyrene (EPS) in states like New York and California, are accelerating this transition. The rise of e-commerce, particularly in perishable foods and meal kits, is further increasing demand for lightweight, efficient, and safe insulated shippers. Companies are also integrating IoT sensors and GPS tracking to enable real-time monitoring of temperature and location, ensuring end-to-end visibility. Investments in automated cold chain infrastructure, including micro-fulfillment hubs, are creating new opportunities for shippers compatible with automated handling systems.

Germany: Circular Economy Leadership and Advanced Insulation Materials Strengthen Market Position

Germany’s insulated shippers industry is heavily influenced by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR). These regulations foster strong demand for eco-friendly and recyclable packaging materials, pushing manufacturers to innovate in sustainable insulated shipping solutions. Germany’s leadership in the circular economy encourages collaboration between manufacturers and end-users to develop shippers with high recycled content and full recyclability. Technological advancements are focused on high-performance insulation materials capable of maintaining precise temperatures even under extreme conditions, making German products reliable for pharmaceutical and biotech cold chain applications.

China: Cold Chain Expansion and Automation Driving Demand for Smart Insulated Shippers

China’s insulated shippers market is growing rapidly due to government-backed expansion of the cold chain logistics sector, fueled by initiatives to boost domestic consumption. The China Federation of Logistics and Purchasing (CFLP) reported significant growth in food-related cold chain logistics in early 2025, highlighting the importance of temperature-controlled packaging. China’s “dual carbon” objectives are driving the development of eco-friendly and energy-efficient shippers to reduce emissions. Technological advancements, including automation and AI-driven packaging systems, are enhancing operational efficiency, particularly for inland logistics. Intelligent packaging with real-time temperature monitoring and GPS sensors is increasingly adopted to ensure product integrity throughout the supply chain.

India: Government Support and E-commerce Growth Accelerate Adoption of Insulated Shippers

The Indian market is witnessing robust growth, supported by government initiatives such as the Integrated Cold Chain and Value Addition Infrastructure program, which provides comprehensive cold chain facilities connecting farms to consumers. The rapid expansion of e-commerce, particularly in online grocery and food delivery, is driving demand for insulated shippers that can maintain temperature during last-mile deliveries. Technological advancements, including innovative materials and design solutions, are improving product safety and convenience, ensuring that shipments meet regulatory standards and consumer expectations. The adoption of cost-effective and sustainable insulated shippers is a key trend in the Indian market.

Brazil: Ultra-Low Temperature Storage and Smart Shippers Driving Market Development

Brazil’s insulated shippers market is strongly influenced by governmental investments in ultra-low temperature storage, particularly for vaccine distribution. Facilities such as Instituto Butantan now maintain consistent -60 °C to -80 °C transport lanes, which require high-performance insulated shippers. The country’s commitment to a circular economy under the National Solid Waste Policy encourages the use of reusable packaging solutions. Technological innovations, including IoT-enabled coolers and remote-controlled systems, are allowing companies to monitor shipments in real time, with insurers offering premium reductions for validated data trails. This reinforces the adoption of smart insulated shippers across pharmaceutical and perishable goods sectors.

Japan: Technological Advancements and Green Transportation Propel Market Growth

Japan’s insulated shippers market is characterized by technological innovation in insulation, with products like Tiger Corporation’s Stainless Steel Vacuum Insulation Panels, which are highly insulating and nonflammable. The government’s focus on green transportation, including ammonia-fueled engines by J-ENG, aligns with the demand for eco-friendly shipping solutions. Strict regulatory requirements for quality and safety ensure that shippers maintain hygienic conditions, protecting pharmaceuticals, biologics, and perishable products. The combination of advanced insulation technology and environmentally sustainable transport solutions is positioning Japan as a leader in high-performance insulated shippers.

Insulated Shippers Market Report Scope

Insulated Shippers market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10 Billion

|

|

Market Size (2034)

|

$19.7 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Product Type (Single-Use Insulated Shippers, Multiple-Use Insulated Shippers, Active Temperature-Control Containers), By Material Type (Expanded Polystyrene, Polyurethane, Vacuum Insulated Panels, Phase-Change-Material Composites, Other Materials), By Application (Pharmaceuticals & Biologics, Clinical Trials & Cell/Gene Therapies, Food & Beverages, Chemicals, Other Applications)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sonoco ThermoSafe, Cold Chain Technologies, Pelican BioThermal, Va-Q-Tec AG, Cryopak Industries, Softbox Systems, CSafe Global, Insulated Products Corp., Tempur-Pak, Sofrigam SA, Peli BioThermal, Nordic Cold Chain Solutions, Plasti-Fab Ltd., TemperPack, E3 Sustainable Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Insulated Shippers Market Segmentation

By Product Type

- Single-Use Insulated Shippers

- Multiple-Use Insulated Shippers

- Active Temperature-Control Containers

By Material Type

- Expanded Polystyrene

- Polyurethane

- Vacuum Insulated Panels

- Phase-Change-Material Composites

- Other Materials

By Application

- Pharmaceuticals & Biologics

- Clinical Trials & Cell/Gene Therapies

- Food & Beverages

- Chemicals

- Other Applications

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Insulated Shippers Market

- Sonoco ThermoSafe

- Cold Chain Technologies

- Pelican BioThermal

- Va-Q-Tec AG

- Cryopak Industries

- Softbox Systems

- CSafe Global

- Insulated Products Corp.

- Tempur-Pak

- Sofrigam SA

- Peli BioThermal

- Nordic Cold Chain Solutions

- Plasti-Fab Ltd.

- TemperPack

- E3 Sustainable Solutions

*List not Exhaustive

Research Coverage

This report investigates the global insulated shippers market, highlighting breakthroughs in advanced insulation technologies, reusable versus single-use solutions, and smart, connected cold chain platforms. USDAnalytics’ analysis reviews market trends from 2021 to 2024, forecasts growth trajectories to 2034, and evaluates strategic innovations that redefine pharmaceutical, food, and specialty chemical logistics. The report emphasizes high-value developments such as phase-change material integration, IoT-enabled shipment monitoring, and curbside-recyclable insulated materials that address both regulatory and sustainability imperatives. It highlights key competitive dynamics, adoption of advanced reusable systems, and expansion into urban last-mile delivery networks, while assessing market drivers, growth opportunities, and risk factors. This report is an essential resource for supply chain managers, cold chain operators, and packaging innovators seeking to benchmark performance, optimize procurement strategies, and gain insights into lifecycle cost benefits, compliance requirements, and next-generation insulated shipper solutions. USDAnalytics further provides detailed company profiles, operational strategies, and technological advancements to guide decision-making across the global cold chain landscape.

Scope Highlights:

- Segmentation: By Product Type (Single-Use Insulated Shippers, Multiple-Use Insulated Shippers, Active Temperature-Control Containers), Material Type (Expanded Polystyrene, Polyurethane, Vacuum Insulated Panels, Phase-Change-Material Composites, Other Materials), Application (Pharmaceuticals & Biologics, Clinical Trials & Cell/Gene Therapies, Food & Beverages, Chemicals, Other Applications)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic Data: 2021–2024; Forecast Data: 2025–2034

- Companies Covered: Sonoco ThermoSafe, Cold Chain Technologies, Pelican BioThermal, Va-Q-Tec AG, Cryopak Industries, Softbox Systems, CSafe Global, Insulated Products Corp., Tempur-Pak, Sofrigam SA, Peli BioThermal, Nordic Cold Chain Solutions, Plasti-Fab Ltd., TemperPack, E3 Sustainable Solutions

Methodology

The study employs a comprehensive, multi-step methodology combining quantitative and qualitative research to deliver actionable insights into the insulated shippers market. USDAnalytics collected primary data from manufacturers, distributors, and end-users through interviews, surveys, and field observations, while secondary research included company reports, regulatory filings, patent databases, and industry publications. Market sizing and forecasting leverage bottom-up and top-down approaches, factoring historical shipment volumes, adoption rates of single-use versus reusable shippers, and regional cold chain expansion trends. Advanced statistical modeling, CAGR analysis, and scenario planning are applied to project growth from 2025 to 2034. Competitive intelligence and innovation benchmarking focus on technology adoption, IoT integration, insulation breakthroughs, and sustainable material deployment. The methodology ensures accurate, reliable, and actionable insights for supply chain professionals, packaging innovators, and investment decision-makers operating in global cold chain logistics.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.