Recyclable Packaging Materials Market Size, Overview, and Growth Outlook (2025–2034)

Global Recyclable Packaging Materials Market Projected to Reach $8.6 Billion by 2034 Amid Rising Sustainability Priorities

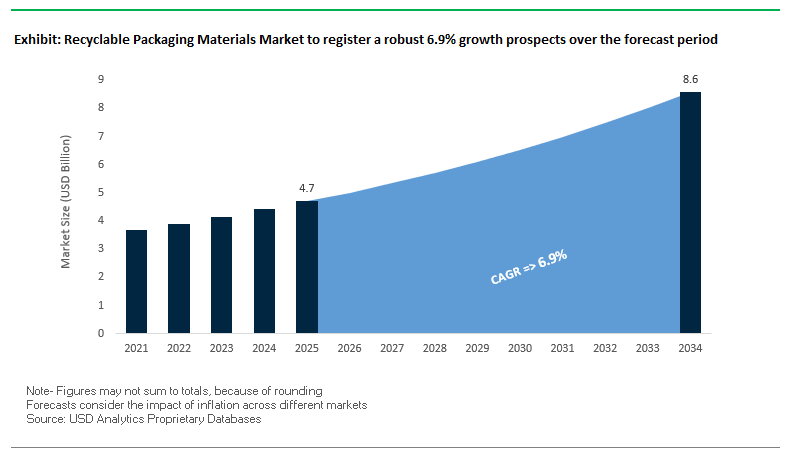

The global recyclable packaging materials market is anticipated to grow from $4.7 billion in 2025 to $8.6 billion by 2034, achieving a CAGR of 6.9%. Increasing regulatory mandates and consumer demand for sustainable products are driving adoption across industries, including food and beverages, retail, and e-commerce. Paper-based materials remain dominant due to their established collection infrastructure and high recyclability rates, while the inclusion of post-consumer recycled (PCR) content is central to achieving circular economy goals.

Key Insights for industry professionals and buyers:

- Paper and Paperboard Lead the Market: Corrugated cardboard and folding cartons are widely recycled and form the backbone of sustainable packaging initiatives.

- Post-Consumer Recycled Content Gains Strategic Importance: Manufacturers are increasing PCR use to reduce reliance on virgin materials.

- Mono-Material Packaging Simplifies Recycling: Using a single material type enhances sorting efficiency and increases material recovery value.

- Cost Advantage Encourages Adoption: Recycling technologies and efficient collection systems are making recycled materials increasingly cost-competitive.

- Technological Advancements Enhance Sustainability: Automation, digital printing, and barrier innovations are improving both recyclability and operational efficiency.

Market Analysis: Strategic Collaborations and Technological Innovations Accelerate Adoption of Recyclable Packaging Materials

The recyclable packaging materials market is experiencing significant growth due to technological innovation, strategic corporate moves, and a strong focus on sustainability. In August 2025, International Paper sold its Global Cellulose Fibers business for $1.5 billion and simultaneously invested $250 million to convert its Riverdale mill for containerboard production, signaling a renewed focus on core sustainable packaging solutions. Novolex appointed a new Chief Procurement Officer the same month, emphasizing supply chain optimization and sustainable material sourcing.

Major global brands are also transitioning to recycled materials. In July 2025, Mars partnered with Berry Global to convert pantry jars for M&M'S® and other brands to 100% recycled plastic, eliminating over 1,300 metric tons of virgin plastic annually. In April 2025, Amcor collaborated with Canadian startup Nfinite Nanotechnology to test nanocoating technologies that improve oxygen barrier performance in recyclable and compostable packaging. Meanwhile, Cascades Inc. introduced produce baskets in March 2025 made from up to 100% recycled fibers, offering growers sustainable alternatives to hard-to-recycle packaging.

Mergers and sustainability certifications are reshaping the industry landscape. The September 2024 merger between Smurfit Kappa and WestRock created a global leader in sustainable packaging, enhancing geographic coverage and product diversity. In June 2024, WestRock received the USDA Certified Biobased Product Label for its FENIX™ Bio Locking Tag, highlighting innovation in renewable materials.

Recyclable Packaging Materials Market: Trends and Opportunities Driving the Next Phase of Circular Packaging

Strategic Integration of Post-Consumer Recycled (PCR) Content in Rigid Packaging

The integration of post-consumer recycled (PCR) content into rigid packaging is a defining trend in the recyclable packaging materials market, driven by both regulatory mandates and corporate sustainability goals. India has emerged as a critical case study, with its Extended Producer Responsibility (EPR) framework requiring a minimum of 30% recycled content in Category I rigid plastic packaging beginning April 1, 2025. This regulation sets a benchmark for emerging markets and positions India alongside global leaders in pushing mandatory PCR adoption. Global corporations are aligning with these regulatory shifts. Nestlé reported in 2024 that it achieved 14.7% recycled content across its global plastic packaging portfolio, signaling measurable progress toward its 2025 sustainability targets. PepsiCo, in parallel, introduced 100% rPET beverage bottles in Taiwan and rolled out India’s first energy drink in an rPET container, showcasing regional execution of global circular economy strategies. Similarly, Mars Inc. has incorporated more than 14,000 metric tons of PCR into candy brands like Skittles and M&M’s, while also debuting 60% PCR pouches for pet food. These developments demonstrate that PCR integration has moved beyond pilot projects into commercial-scale adoption across multiple product categories.

Rapid Standardization of Mono-Material Flexible Packaging Designs

Mono-material packaging designs are gaining rapid momentum as the flexible packaging industry seeks to overcome the recycling challenges associated with multi-layer laminates. Companies like Huhtamaki have introduced their blueloop™ mono-material portfolio, offering recycle-ready solutions based on PE, PP, and PET. These formats simplify recycling processes while enabling brand owners to meet their public commitments for 100% recyclable packaging by 2025. At an industry-wide level, collaboration initiatives are ensuring that design innovation aligns with practical recycling capabilities. The Circular Economy for Flexible Packaging (CEFLEX), a European consortium, is developing standardized design guidelines for recyclable flexible packaging. Their efforts focus on mono-material structures compatible with current mechanical recycling infrastructure, while also anticipating integration with future chemical recycling technologies. This standardization effort is key to unlocking higher collection rates, improved sorting efficiency, and better-quality recyclates for reuse in high-demand markets such as food and beverage, personal care, and household products.

Development of Advanced Chemical Recycling for Complex and Contaminated Feedstocks

The rise of advanced chemical recycling technologies presents one of the most promising opportunities for recyclable packaging materials. Unlike mechanical recycling, which is often limited by contamination and material degradation, chemical recycling can handle complex and contaminated feedstocks, converting them back into virgin-quality polymers. A major milestone was ExxonMobil’s November 2024 announcement of a $200 million expansion of its advanced recycling operations in Texas, with the ambition of reaching 1 billion pounds of annual recycling capacity by 2027. This scale-up underscores the industry’s commitment to chemical recycling as a mainstream solution for circularity. Organizations such as Plastics Europe highlight that chemical recycling not only enables closed-loop systems for hard-to-recycle plastics but also ensures that the recycled output is suitable for sensitive, high-value applications like food packaging. For brand owners, this represents a strategic pathway to meet recycled content mandates while ensuring product safety and performance.

Innovation in Bio-Based and Compostable Barrier Materials

Another transformative opportunity lies in the innovation of bio-based and compostable materials that can replace conventional petroleum-based plastics without sacrificing functionality. Recent research highlighted on ResearchGate in August 2025 showcased the potential of seaweed-derived bio-films and other natural polymers with strong mechanical strength, moisture resistance, and biodegradability. These bio-based films are scalable for large food packaging applications, positioning them as credible alternatives in categories such as single-serve snacks and ready-to-eat meals. In addition, paper-based alternatives with bio-coatings are pushing the performance envelope. A July 2025 study in the International Journal of Engineering Research & Technology emphasized the use of cellulose and chitosan as coatings that improve paper’s moisture and oxygen barrier properties. These advancements allow paper-based packaging to compete with plastics in applications like snack food packaging, while still remaining compatible with standard paper recycling streams. Together, bio-based and compostable innovations open new pathways for brands to reduce plastic dependency, achieve sustainability targets, and appeal to environmentally conscious consumers.

Competitive Landscape: Leading Recyclable Packaging Companies Are Driving Growth Through Circular Economy and Innovation

The competitive landscape of recyclable packaging materials is defined by companies prioritizing sustainability, circular economy practices, and technological innovation. Leading players focus on expanding recycling capabilities, investing in R&D, and optimizing operations to meet growing demand for eco-friendly packaging.

International Paper Company: Streamlining Operations to Strengthen Leadership in Sustainable Fiber-Based Packaging

International Paper specializes in recyclable fiber-based packaging, pulp, and paper products. In August 2025, the company sold its Global Cellulose Fibers business for $1.5 billion and invested $250 million in Riverdale mill containerboard production. Its key strengths include forest stewardship, recycling, and water conservation, making it a trusted partner for agriculture and e-commerce packaging solutions.

Smurfit Kappa Group: Expanding Global Presence Through Strategic Merger and R&D Investments

Smurfit Kappa provides recyclable paper-based solutions, including corrugated, folding cartons, and bag-in-box products. The September 2024 merger with WestRock established a global sustainable packaging leader. With multi-million-pound R&D investments, the company optimizes fiber strength, resilience, and recyclability, while its closed-loop recycling model improves efficiency and reduces waste.

Amcor plc: Advancing Recycling Infrastructure and Barrier Technology for Sustainable Packaging

Amcor develops rigid and flexible recyclable packaging, including films, bags, and trays. In August 2025, Amcor expanded its UK recycling capabilities to support circular economy objectives. Its EcoGuard™ brand highlights recyclable features, and its April 2025 collaboration with Nfinite Nanotechnology focuses on enhancing barrier performance for recyclable and compostable packaging.

DS Smith Plc: Driving Circular Economy Adoption Through Closed-Loop Paper and Corrugated Recycling

DS Smith offers retail, shelf-ready, and transit packaging solutions. Its closed-loop recycling collects, processes, and reuses paper and corrugated materials, reducing waste. The company invests in fully recyclable translucent packaging for applications like sandwich and ready meal packs and is expanding its North American presence with new headquarters in Atlanta, Georgia.

WestRock Company: Leveraging Automation and Smart Packaging to Lead Sustainable Fiber-Based Solutions

WestRock delivers a wide range of recyclable containers and folding cartons. The September 2024 merger with Smurfit Kappa created Smurfit WestRock, a global sustainable packaging leader. Its focus on automation and smart packaging solutions, including RFID integration, positions the company as a future-ready partner for recyclable materials.

Novolex: Integrating Diverse Materials and PCR Content to Foster Circular Economy Innovation

Novolex manufactures paper, plastic, and sustainable packaging for food, retail, and industrial markets. Its Eco-Products brand won a national award in April 2025 for reusable containers. Novolex offers molded fiber bases, plant-based films, and products with at least 10% post-consumer recycled (PCR) content, supported by two world-class plastic film recycling facilities to ensure a circular packaging model.

Recyclable Packaging Materials Market Share Insights, 2025-2034

Boxes & Cartons lead Market Share by Packaging Type in Recyclable Packaging Materials

Fiber-based substrates anchor the recyclable packaging materials mix at 38% because paperboard and corrugated enable true mono-material design and high real-world recovery, now amplified by recyclable barrier systems (water-based dispersions, PVOH, PLA, silica) that displace PE lamination without sacrificing grease/moisture resistance. Bottles & jars (28%) follow on the back of rPET, rHDPE and rPP scale, with material innovation focused on mono-polymer builds (full-PET labels/closures, oxygen scavengers) to preserve a high-value recyclate stream. Bags & pouches (16%) are the materials frontier: converters are re-platforming to mono-PE and mono-PP (mPE, BOPE/BOPP) to hit store-drop or curbside compatibility while holding aroma/oxygen barrier. Films & wraps (9%) remain infrastructure-constrained; growth in this materials segment is tethered to chemical recycling that can return contaminated flexibles to virgin-quality feedstock. Tubes & vials (9%) are mid-transition, with HDPE/PP mono-material tubes and aluminum gaining share; resin rheology is being tuned to keep tube squeezability while meeting bale-level recyclability. Net-net, material science is migrating from “recyclable in principle” to “recycled in practice,” with mono-material design + compatible barriers as the decisive market share flywheel.

Food & Beverages dominate Market Share by End-Use in Recyclable Packaging Materials

Food & beverages (42%) set the pace for recyclable materials because barrier performance equates directly to shelf-life and food-waste prevention; this drives investment into coated paperboard, BOPE/BOPP, and high-barrier mono-PE solutions validated on real lines at commercial speeds. Consumer goods (24%) provide durable, predictable demand signals for rPET/rHDPE/rPP, prioritizing PCR availability, cost, and impact resistance over ultra-high barrier—thereby underwriting new reprocessing capacity. E-commerce (14%) “right-weights” corrugated and paper cushioning with stronger fibers and starch glues to cut freight emissions while remaining curbside-recyclable. Personal care & cosmetics (13%) requires premium aesthetics with recyclability: color-stable rPET, clear rPP, glass, and aluminum are favored to maintain brand equity without contaminating streams. Healthcare & pharma (7%) move cautiously—material validation for mono-material blister replacements (PP, PET) must survive sterilization and extractables/leachables testing—so progress is deliberate but durable once approved. The center of gravity remains F&B, where combining recyclability + barrier is the key material gate.

European Union: PPWR and Circular Economy Targets Reshaping Packaging Design

The European Union has become a global leader in driving change in the recyclable packaging materials market through the Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025. This regulation is the single most transformative policy in the region, covering the entire life cycle of packaging. Its primary aim is to create a circular economy that reduces waste while promoting recyclability and reusability. A landmark requirement of the PPWR is the ban on single-use plastic packaging for fresh fruits and vegetables below 1.5 kg by 2030, which is reshaping the use of plastic trays, wraps, and films. Additionally, the grading system for recyclability mandates all packaging to reach 70% recyclability (Grade C) by 2030 and 95% (Grade A) by 2038, setting a strict compliance path for industry stakeholders.

The EU is also restricting PFAS in food-contact packaging materials starting August 2026, compelling manufacturers to adopt PFAS-free coatings and adhesives. By 2028, all packaging must carry a harmonized recycling label, ensuring standardization and consumer clarity across member states. Another pivotal development is the 50% empty space rule for e-commerce and transport packaging by 2030, which is pushing companies to redesign boxes and cartons for greater efficiency. Together, these regulations are accelerating investment in mono-material packaging, fiber-based alternatives, and reusable systems, making the EU a benchmark region for sustainable packaging innovation.

United States: EPA Regulations and Infrastructure Funding Driving Recycling Innovation

The United States recyclable packaging materials market is being shaped by regulatory initiatives from the U.S. Environmental Protection Agency (EPA) and cross-industry collaborations like the U.S. Plastics Pact. These initiatives aim to build a circular economy for plastics by improving recycling streams and cutting landfill waste. A strong emphasis is being placed on advanced recycling technologies, particularly chemical recycling, and the development of mono-material films that simplify sorting and reprocessing. Growing demand for mono-material polyethylene (PE) and polypropylene (PP) packaging reflects this shift, as these formats can be more easily integrated into existing recycling systems.

Infrastructure support through the Infrastructure Investment and Jobs Act is enabling the construction of state-of-the-art recycling facilities across the country, boosting regional recycling capacity. At the same time, the market is witnessing the rapid rise of paper-based packaging, molded fiber trays, and compostable solutions, driven by consumer preference for sustainable alternatives. A notable trend is the premiumization of recyclable materials, particularly in high-value industries such as automotive wraps and architectural graphics, where manufacturers are investing in high-margin cast films that combine durability with recyclability. This dual focus on sustainability and product performance highlights the strategic direction of the U.S. market.

China: Policy Reforms and E-Commerce Expansion Fueling Recyclable Packaging Demand

China’s recyclable packaging materials market is advancing under government policies that support the “14th Five-Year Plan” for sustainable growth. The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are jointly enforcing stricter controls on plastic pollution, pushing manufacturers toward recyclable and eco-friendly packaging formats. New national standards on edible agricultural products regulate packaging by limiting the interspace ratio, number of layers, and overall packaging costs, addressing long-standing concerns about over-packaging in retail and e-commerce.

Aligned with the country’s Dual Circulation strategy, which prioritizes domestic consumption, e-commerce has become a major driver of recyclable packaging demand. Companies are also benefiting from tax incentives for green technology adoption and government-backed efforts to develop the remanufacturing industry, strengthening recycling infrastructure. By focusing on lightweight packaging, mono-material structures, and recyclable laminates, China is positioning itself as both a production hub and consumer market for recyclable packaging. These advancements make it one of the fastest-growing global markets in the sustainable packaging sector.

India: EPR-Driven Compliance and Bioplastic Innovation Boosting Growth

In India, the recyclable packaging materials market is undergoing rapid evolution, shaped by the Plastic Waste Management (Amendment) Rules, 2024. These rules place strong emphasis on Extended Producer Responsibility (EPR), requiring producers, importers, and brand owners to take responsibility for the post-consumer recycling of packaging. While micro, small, and medium enterprises (MSMEs) are exempt, raw material manufacturers and large producers remain accountable, pushing the market toward better waste management practices. Moreover, all recycled plastic packaging must include a label specifying the percentage of recycled plastic and conform to the Indian Standard IS 14534:2023, driving transparency and standardization across the sector.

India is also emerging as a hub for bioplastic innovations, with patents being awarded for biodegradable packaging derived from agricultural and dairy waste, such as ghee residue. These eco-friendly alternatives align with both consumer demand and global sustainability commitments. Rising consumption of processed foods, dairy, and ready-to-eat meals is further strengthening the role of recyclable films and containers in the food sector. Coupled with initiatives like the India Plastics Pact, which aims to make 100% of plastic packaging reusable or recyclable by 2030, India is building a framework for long-term growth in sustainable packaging adoption.

Japan: Bio-PP Adoption and Paper-Based Innovation Strengthening Circular Economy

Japan is establishing itself as a leader in sustainable packaging innovation, particularly with its strong push toward bio-polypropylene (bio-PP). Supported by government plans to introduce 2 million tons of bio-PP annually by 2030, companies like LyondellBasell and Shiseido are actively integrating bio-based solutions into cosmetic and food packaging applications. In parallel, Japanese firms are advancing paper-based barrier technologies, with innovations such as Nippon Paper Industries’ SHIELDPLUS, a recyclable paper that resists oxygen and odor transmission, setting new benchmarks for eco-friendly alternatives.

The market is also being shaped by the government’s commitment to a circular economy, encouraging materials that can be recycled or composted efficiently. Oversight by the Japan Vinyl Industry Association (JVIA) ensures quality and safety in plastic and vinyl packaging, balancing regulatory compliance with innovation. By combining premium aesthetics, high performance, and sustainability, Japan is delivering recyclable packaging materials that not only meet domestic regulatory expectations but also set international standards for eco-conscious design and innovation.

Brazil: Reverse Logistics and Solid Waste Policy Accelerating Recycling Adoption

Brazil’s recyclable packaging materials market is anchored by the National Solid Waste Policy (PNRS), which outlines a comprehensive framework for waste reduction, recycling, and reuse. A critical component of this policy is the reverse logistics system, which requires producers and distributors to manage the post-consumer collection and recycling of packaging. This regulatory approach has created significant pressure on companies to design packaging with recyclability in mind, boosting demand for sustainable plastics, recyclable trays, and eco-films.

The PNRS is complemented by government investments in waste management infrastructure and initiatives aimed at reducing overall solid waste generation. In the food packaging sector, Modified Atmosphere Packaging (MAP) and recyclable vacuum films are being widely adopted to extend shelf life while maintaining recyclability. With its strong export-oriented produce industry and rising domestic sustainability awareness, Brazil is strategically aligning its packaging sector with global environmental standards. This positions the country as a growing hub for innovative, recyclable packaging solutions across both domestic and international markets.

Recyclable Packaging Materials Market Report Scope

Recyclable Packaging Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.7 Billion

|

|

Market Size (2034)

|

$8.6 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Material (Plastics, Paper & Paperboard, Glass, Metal, Bioplastics), By Packaging Type (Bottles & Jars, Boxes & Cartons, Bags & Pouches, Films & Wraps, Tubes & Vials), By End-Use Industry (Food & Beverages, Consumer Goods, Healthcare & Pharmaceuticals, E-commerce, Personal Care & Cosmetics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, DS Smith Plc, Smurfit Kappa Group Plc, Graphic Packaging Holding Company, Sonoco Products Company, Huhtamaki Oyj, International Paper Co., WestRock Company, ProAmpac, Berry Global, Inc., Greif, Inc., Silgan Holdings Inc., Pactiv Evergreen Inc., PAPACKS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Recyclable Packaging Materials Market Segmentation

By Material

- Plastics

- Paper & Paperboard

- Glass

- Metal

- Bioplastics

By Packaging Type

- Bottles & Jars

- Boxes & Cartons

- Bags & Pouches

- Films & Wraps

- Tubes & Vials

By End-Use Industry

- Food & Beverages

- Consumer Goods

- Healthcare & Pharmaceuticals

- E-commerce

- Personal Care & Cosmetics

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Recyclable Packaging Materials Market

- Amcor plc

- Mondi Group

- DS Smith Plc

- Smurfit Kappa Group Plc

- Graphic Packaging Holding Company

- Sonoco Products Company

- Huhtamaki Oyj

- International Paper Co.

- WestRock Company

- ProAmpac

- Berry Global, Inc.

- Greif, Inc.

- Silgan Holdings Inc.

- Pactiv Evergreen Inc.

- PAPACKS

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive, multi-layered research methodology to deliver precise insights into the Recyclable Packaging Materials Market. Our approach combines primary data collection through interviews with key industry stakeholders, including packaging manufacturers, brand owners, and regulatory authorities, with secondary research drawing from corporate filings, sustainability reports, government regulations, and industry publications. We analyze global market dynamics, regional regulatory frameworks, and technological innovations, including developments in post-consumer recycled (PCR) content, mono-material designs, and bio-based barrier materials. Quantitative modeling techniques are applied to forecast market growth, segment adoption, and material trends, incorporating factors such as consumer preferences for eco-friendly packaging, corporate sustainability commitments, and infrastructure advancements across regions like the EU, U.S., China, India, Japan, and Brazil. Our methodology also emphasizes cross-validation with industry consortium data, trade associations, and patent filings to ensure accuracy and reliability. By integrating strategic corporate initiatives, technological advancements, regulatory impacts, and competitive landscape analyses, USDAnalytics provides a 360-degree perspective of the recyclable packaging materials ecosystem, empowering industry professionals to make data-driven decisions for sustainable growth and investment opportunities.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.