Extended Shelf Life, Sustainability, and Cost Efficiency Push Bag-in-Box Packaging Market to USD 6.7 Billion by 2034

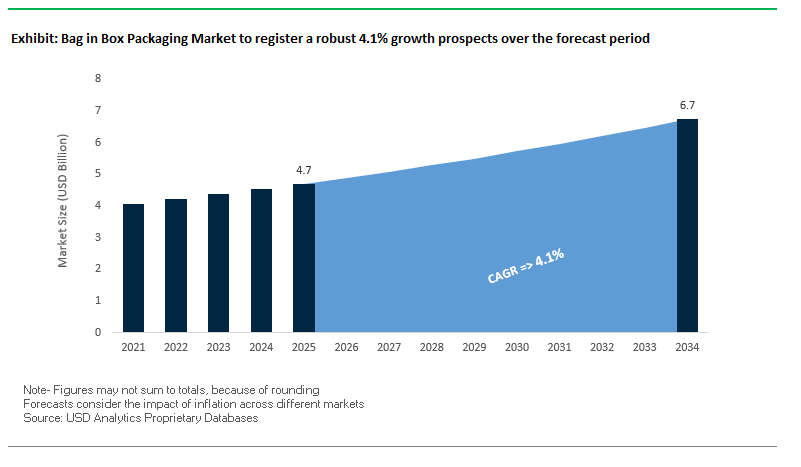

The global bag-in-box (BIB) packaging market is valued at USD 4.7 billion in 2025 and is projected to reach USD 6.7 billion by 2034, expanding at a steady CAGR of 4.1%. Bag-in-box packaging is increasingly preferred across food, beverage, and household industries for its ability to preserve freshness while meeting sustainability requirements. Its superior oxygen and light barrier properties ensure extended shelf life for liquid and semi-liquid products, while the collapsible inner bag prevents air re-entry, maintaining quality even after opening.

The market is also witnessing strong momentum due to its reduced environmental impact compared with rigid packaging. By using less plastic and incorporating a recyclable paperboard outer layer, BIB solutions align with global consumer and regulatory demand for eco-friendly packaging formats. In addition, the flat shipping and lightweight design of bag-in-box systems lowers transportation costs and carbon emissions, making it attractive for manufacturers seeking efficiency in global supply chains. Finally, the format’s dispensing convenience through built-in taps and fitments has strengthened adoption in wine, juice, cooking oil, and foodservice applications, where controlled dispensing is critical.

Key Insights for Industry Professionals

- Barrier protection against oxygen and light extends shelf life post-opening.

- Paperboard outer boxes reduce plastic dependency and support recyclability goals.

- Transportation efficiency lowers logistics costs and carbon emissions.

- Dispensing taps and fitments improve consumer convenience and product safety.

Recycling Milestones, Mergers, and Smart Packaging Innovations Shape Bag-in-Box Packaging Market

The bag-in-box packaging industry is evolving through strategic mergers, recycling certifications, and smart material innovations. In August 2025, SIG received APR recognition for its recycle-ready wine BIB package featuring a new laminate and tap, underscoring its leadership in sustainable packaging. That same month, Smurfit WestRock officially debuted post-merger, consolidating its position as a paper-based packaging leader with deep capabilities in BIB outer box solutions.

In July 2025, DS Smith Hellas partnered with Minerva A.E. to launch DS Smith Tape Back, a smart packaging solution simplifying e-commerce returns a signal of how functionality is expanding beyond protection. Earlier in June 2025, Mondi introduced its re/cycle PaperPlus Bag Advanced, a paper-based solution that reduces plastic content while offering strong protection for moisture-sensitive products, aligning with the industry’s pivot toward hybrid paper–plastic solutions.

Other developments demonstrate capacity expansion and acquisitions. In May 2025, Pregis invested in EVOH barrier film production, enhancing high-performance films for inner BIB bags. In October 2024, SIG launched its Terra RecShield D BIB for post-mix concentrates, achieving recyclability recognition. And in November 2023, Smurfit Kappa acquired Bulgarian BIB manufacturer Artemis Ltd., strengthening its footprint in Eastern Europe.

Key Trends Reshaping the Bag-in-Box Packaging Market

Rapid Expansion Beyond Wine into Commercial and Liquid Food Service Applications

While wine packaging continues to dominate demand, the bag-in-box packaging market is rapidly expanding into new high-volume commercial and food service applications. Restaurants, QSR chains, and institutional buyers are adopting this format for liquid eggs, dairy alternatives, fruit juices, condiments, and edible oils due to its unmatched efficiency, portion control, and food waste reduction. For example, its ability to dispense cleanly and consistently makes it ideal for liquid eggs and dairy alternatives in large-scale kitchens, where spoilage and inconsistency can lead to significant losses. The food service industry has long relied on bag-in-box for post-mix syrups and sauces, but the format’s vacuum-sealed dispensing system is now being applied to newer categories where hygiene and extended shelf life are critical. This is particularly impactful because the self-collapsing inner bag prevents oxygen entry, keeping products fresh for longer and reducing daily waste accumulation. Industry leaders like Scholle IPN have broadened their portfolios to include solutions for condiments, industrial syrups, and alternative beverages, demonstrating that bag-in-box is evolving into a core food service packaging format beyond wine.

Integration of Advanced Barrier Films and Lightweighting for Enhanced Sustainability

A second major trend shaping the bag-in-box industry is the innovation in high-performance barrier films and lightweight designs that enhance product protection while lowering environmental impact. Compared to rigid containers, bag-in-box offers a dramatically lower transportation footprint: a 10-liter bag-in-box weighs only 359 grams, versus 2.5 kg for a 10-liter metallic jerrican, according to a Smurfit Kappa study. This weight reduction translates directly into reduced carbon emissions in logistics. Packaging leaders like Mondi Group are developing multi-layer EVOH barrier films that protect against oxygen and light while still being recyclable, striking a balance between performance and sustainability. Circularity is also accelerating, with Scholle IPN launching a 100% recyclable all-polyethylene bag-in-box for water, certified by the Association of Plastic Recyclers (APR). Beyond materials, Smurfit Kappa’s shelf-life–extending film technologies prevent oxygen exposure during dispensing, keeping products like wine fresh for weeks after opening. By reducing product spoilage a leading contributor to carbon footprint these innovations reinforce the bag-in-box as a low-impact, next-generation packaging solution.

Emerging Opportunities Driving Growth in Bag-in-Box Packaging

Development of Integrated Smart Dispensing and Inventory Management Systems

A high-potential opportunity in the bag-in-box packaging market lies in integrating smart technology such as IoT-enabled taps, RFID tags, and connected dispensing systems to transform traditional bag-in-box into a smart asset. In commercial food service environments, smart bag-in-box solutions can connect directly with inventory management systems, automatically alerting staff when products are running low and triggering re-orders. This eliminates manual stock checks, reduces the risk of stockouts, and ensures uninterrupted operations. By providing granular data on product usage, connected bag-in-box packaging allows restaurants and caterers to forecast demand, minimize over-ordering, and reduce waste. Early prototypes from technology providers demonstrate the potential of real-time monitoring, with some systems even offering predictive analytics to optimize supply chains. As the food service sector increasingly demands operational transparency and efficiency, connected bag-in-box systems could deliver a clear ROI by merging packaging with digital supply chain intelligence.

Capitalizing on Regulatory Push Against Single-Use Plastics in Hospitality

Regulatory restrictions on single-use plastics are accelerating the adoption of bag-in-box as a sustainable packaging alternative in the hospitality sector. The European Union’s Single-Use Plastics Directive and similar laws worldwide are forcing HoReCa operators to shift away from small PET bottles and disposable containers. Bag-in-box offers an attractive solution, particularly in hotels, cafes, and restaurants, where a single large-format package of juice, water, or milk can replace dozens of single-serve bottles, cutting both waste and handling costs. In India, the Plastic Waste Management Amendment Rules, 2021 further ban high-litter, low-utility plastics, reinforcing demand for bulk liquid packaging formats. Environmentally, bag-in-box performs strongly: Smurfit Kappa reports that 75% of a 3-liter bag-in-box is made from recyclable corrugated cardboard, while the flexible inner liner can be easily separated for recycling. For businesses under regulatory and consumer pressure to demonstrate sustainability, bag-in-box provides a scalable, cost-effective, and eco-friendly packaging model that aligns perfectly with circular economy goals.

Global Packaging Leaders Compete with Sustainable Designs, Barrier Films, and Integrated BIB Systems

The bag-in-box packaging market’s competitive landscape is defined by leading global packaging groups that are diversifying through eco-friendly innovations, barrier film technologies, and vertically integrated solutions.

Smurfit WestRock: Expanding with EasySplit Bag-in-Box for Improved Recycling

Following its July 2025 merger, Smurfit WestRock launched the EasySplit BIB design, enabling easier separation of inner bags and outer cartons for recycling. With facilities in over 42 countries, the company is positioned as a global leader in sustainable paper-based outer boxes. Its strategy focuses on circular economy principles, delivering high-performance corrugated solutions for BIB systems.

SIG Combibloc: Integrating Scholle IPN for Full Value Chain Control

Through its acquisition of Scholle IPN, SIG has become a vertically integrated player in the BIB sector. In August 2025, it introduced a recycle-ready wine BIB package recognized by APR. With expertise spanning films, fitments, pouches, and filling equipment, SIG is uniquely positioned to deliver end-to-end bag-in-box packaging systems. Its sustainability-driven innovations, such as SIG Terra RecShield D, reflect its leadership in recyclable packaging technologies.

Mondi Group: Developing High-barrier Paper and Film Solutions for BIB Applications

Mondi has strengthened its portfolio with the launch of re/cycle PaperPlus Bag Advanced (June 2025), a paper-based alternative for humidity-sensitive products. Its EVOH barrier films provide oxygen, scent, and gas protection, enhancing the shelf life of liquid food products in BIB formats. Mondi’s material-neutral strategy and vertically integrated operations from forestry to conversion enable it to deliver high-quality, sustainable BIB components.

DS Smith plc: Scaling Bag-in-Box Solutions Through International Paper Acquisition

DS Smith, acquired by International Paper in July 2025, is expanding its global footprint in corrugated BIB outer boxes. With its circular business model and integrated paper-to-packaging value chain, DS Smith is investing in innovative solutions that combine strength, branding features, and recyclability. The company’s outer box solutions play a critical role in supporting liquid food and beverage brands worldwide.

Bag in Box Packaging Market Share Insights

Bags Dominate Market Share by Component in Bag-in-Box Packaging

Bags hold the largest share at 50% of the bag-in-box packaging market, underscoring their role as the core functional barrier in the system. These multi-layer, co-extruded pouches often incorporating EVOH or nylon are engineered to deliver superior oxygen and moisture resistance, ensuring extended shelf-life for sensitive products ranging from wines and dairy alternatives to industrial chemicals. Unlike the outer carton or fitments, the inner bag directly determines product stability and quality, making it the highest-value component in the value chain. As consumer demand for sustainable packaging grows, the development of recyclable and bio-based film structures is expected to reinforce the centrality of the bag component in driving innovation and market differentiation.

Beverages Continue to Drive Market Share by Application in Bag-in-Box Packaging

The beverage sector leads with 40% share, firmly establishing itself as the largest and most dynamic application for bag-in-box systems. Wine remains the flagship product, leveraging the format’s ability to minimize oxygen ingress after opening extending usability from days to weeks. Beyond wine, liquid dairy alternatives, fruit juices, and cold-brew coffee are increasingly adopting bag-in-box formats to reduce logistics costs compared to glass bottles while maintaining product freshness. The segment’s strong position reflects the convergence of consumer demand for convenience, sustainability, and cost efficiency, making beverages the anchor that supports further adoption in food, household, and industrial applications.

United States: FDA Regulations and Sustainability Shape Bag-in-Box Packaging Growth

The U.S. bag-in-box packaging market is guided by strict U.S. Food and Drug Administration (FDA) regulations, ensuring all materials used in food-contact packaging are safe and compliant. This regulatory stability has provided manufacturers a foundation to invest in new innovations, particularly in advanced films and dispensing systems. Companies like Liqui-Box are pioneering barrier films that minimize oxygen ingress and extend product shelf life, making bag-in-box packaging increasingly reliable for sensitive liquid products.

Sustainability is a defining force in the U.S. market, as industry leaders like Scholle IPN introduce SIOC (Ships-In-Own-Container)-approved bag-in-box solutions that cut carbon footprints by up to 67%. The Association of Plastic Recyclers (APR) has validated many designs for recyclability, accelerating the adoption of eco-friendly solutions. Demand is strongest in the beverage and foodservice sectors, with applications ranging from wine and juices to post-mix syrups. Reinforced by government initiatives promoting supply chain resilience and sustainable practices, the U.S. continues to position bag-in-box as a cost-efficient, eco-conscious, and scalable solution for liquid packaging.

Germany: EU Circular Economy Mandates Fuel Bag-in-Box Packaging Innovation

Germany is at the forefront of the circular economy, with its bag-in-box packaging industry shaped by the EU Packaging and Packaging Waste Regulation (PPWR) and the Packaging Act (VerpackG). Both frameworks hold producers accountable for the full life cycle of packaging, requiring all solutions to be recyclable or reusable by 2030. This is spurring widespread innovation in sustainable outer box materials, such as grass paper and recycled fibers, combined with advanced barrier films for the inner bag.

The German market has strong demand in the wine, juice, and industrial liquids sectors, where bag-in-box offers both shelf stability and high-volume efficiency. Companies are investing heavily in reusable cartons and refillable solutions to meet PPWR targets, while corporate expansions like Aran Group’s acquisition of IBA Germany reinforce global confidence in the European market. Germany’s robust R&D ecosystem ensures its bag-in-box packaging solutions remain technologically advanced, sustainable, and fully aligned with EU waste reduction mandates.

China: Dual Carbon Goals and AI-Driven Efficiency Advance Bag-in-Box Market

China’s bag-in-box packaging market is advancing rapidly under the government’s “dual carbon” policy, which restricts non-degradable plastics and drives demand for sustainable, paper-based, and recyclable alternatives. The nation’s massive food and beverage industry, coupled with booming e-commerce and packaged food demand, has positioned bag-in-box packaging as a critical enabler of safe, cost-effective, and long-lasting liquid packaging.

Chinese manufacturers are also leading in automation, AI, and “5G plus industrial internet” integration, which is optimizing efficiency and enabling highly flexible production capacity. Local companies are expanding domestic manufacturing to reduce reliance on imports, in line with national industrial policies. Corporate investments, such as Ingka Group’s stake in plastic recycler Re-mall, are expanding recycled material availability, strengthening sustainability in packaging. Meanwhile, SIG’s ISO 13485-certified Suzhou plant demonstrates how China’s bag-in-box industry is aligning with high international quality and safety standards, even extending applications into medical and industrial liquids.

India: Make in India and Food Safety Regulations Drive Bag-in-Box Packaging Demand

India’s bag-in-box packaging market is accelerating under government initiatives such as “Make in India”, which promotes domestic innovation and production, and the Food Safety and Standards Authority of India (FSSAI) Packaging Regulations, 2018, which mandate strict compliance for food-contact packaging. These frameworks have established India as a strong player in both domestic food processing and global exports, driving demand for oxygen- and moisture-resistant barrier films that extend product shelf life.

Sustainability is a parallel growth driver, with increasing investment in biodegradable and compostable outer box materials. The recent joint venture between Brazil’s Packem SA and India’s Umasree Texplast to establish a 100% rPET packaging plant reflects the country’s commitment to circular economy principles. Bag-in-box packaging is particularly popular in edible oils and fruit-based beverages, as well as bulk supplies for institutional use. As the country’s food processing sector expands and automated packaging systems gain ground, India is emerging as a hub for affordable, high-quality, and sustainable bag-in-box packaging solutions.

Brazil: ANVISA Regulations and Food Sector Growth Strengthen Bag-in-Box Packaging

Brazil’s bag-in-box packaging market is being shaped by ANVISA’s updated regulatory framework (September 2024), which modernizes food packaging oversight with risk-based assessments. This regulatory clarity has provided momentum for companies to scale production while ensuring compliance with international standards. The packaging industry is also investing in AI and robotics to boost efficiency, reduce defects, and deliver consistent product quality.

With the food and beverage industry expanding rapidly, bag-in-box packaging has become a preferred solution for wine, juices, and soy-based drinks, offering both sterility and cost efficiency. Sustainability is increasingly central, with new government policies supporting domestic recycling and circular economy principles, such as the 2025 law allowing solid waste imports for recycling. This policy indirectly boosts the bag-in-box sector by improving recycled material supply. Combined with strategic corporate investments, Brazil is cementing its role as a regional leader in sustainable liquid packaging solutions.

Japan: Smart Packaging and Lightweight Materials Redefine Bag-in-Box Solutions

Japan’s bag-in-box packaging industry is driven by its precision manufacturing ecosystem, where companies like DNP Group and Toyo Seikan Group are investing in smart packaging technologies and recyclable lightweight designs. The Ministry of Health, Labour and Welfare’s (MHLW) 2025 Food Sanitation Act revision introduced stricter standards for food-contact packaging, reinforcing trust in Japanese packaging quality.

The market is also transitioning toward digital-enabled packaging with integrated sensors to monitor safety and shelf life, expanding bag-in-box into premium and high-performance applications. Academic research plays a vital role, with universities developing biopolymers and natural agents for sustainable barrier films. Corporate innovation, particularly in lightweighting and dimensional stability, ensures bag-in-box solutions meet both environmental and functional requirements. With automation at the core of Japanese logistics and manufacturing, the country is setting global benchmarks for intelligent, high-performance, and eco-friendly bag-in-box packaging solutions.

Bag in Box Packaging Market Report Scope

Bag in Box Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.7 Billion

|

|

Market Size (2034)

|

$6.7 Billion

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Component (Bag, Box, Fitments), By Material Type (Liner Material, Outer Box Material), By Volume (Up to 5 Liters, 5 to 10 Liters, 10 to 20 Liters, Above 20 Liters), By Application (Beverages, Food Products, Industrial Liquids, Household Products, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Smurfit Kappa Group, Mondi Group, DS Smith Plc, WestRock Company, International Paper Company, Nefab AB, Sonoco Products Company, Pregis LLC, Sealed Air Corporation, Huhtamäki Oyj, Menasha Corporation, Amcor plc, Greif, Inc., Scholle IPN, Liqui-Box

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bag in Box Packaging Market Segmentation

By Component

By Material Type

- Liner Material

- Outer Box Material

By Volume

- Up to 5 Liters

- 5 to 10 Liters

- 10 to 20 Liters

- Above 20 Liters

By Application

- Beverages

- Food Products

- Industrial Liquids

- Household Products

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bag in Box Packaging Market

- Smurfit Kappa Group

- Mondi Group

- DS Smith Plc

- WestRock Company

- International Paper Company

- Nefab AB

- Sonoco Products Company

- Pregis LLC

- Sealed Air Corporation

- Huhtamäki Oyj

- Menasha Corporation

- Amcor plc

- Greif, Inc.

- Scholle IPN

- Liqui-Box

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous and industry-centric research methodology to provide accurate insights into the global bag-in-box (BIB) packaging market. Our approach combines primary research through interviews with packaging manufacturers, food and beverage companies, and industry experts, alongside secondary research from verified corporate reports, trade publications, regulatory filings, and news sources. Market sizing and growth projections are developed using proprietary quantitative models that incorporate factors such as sustainability adoption, barrier film innovations, e-commerce expansion, and operational efficiency improvements in commercial and foodservice applications. Competitive intelligence examines strategic mergers, acquisitions, and technology-driven innovations by leaders like Smurfit WestRock, SIG Combibloc, Mondi, and DS Smith, highlighting their impact on material development, smart dispensing systems, and recyclable packaging. Regional analyses cover key markets including the U.S., Germany, China, India, Brazil, and Japan, considering regulatory frameworks, environmental mandates, and evolving consumer demands. By triangulating multiple reliable data sources and validating trends with industry stakeholders, USDAnalytics ensures actionable, high-quality, and decision-oriented insights for packaging professionals, investors, and supply chain strategists.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.