Market Overview: Food Packaging Market to Surpass $745.1 Billion by 2034

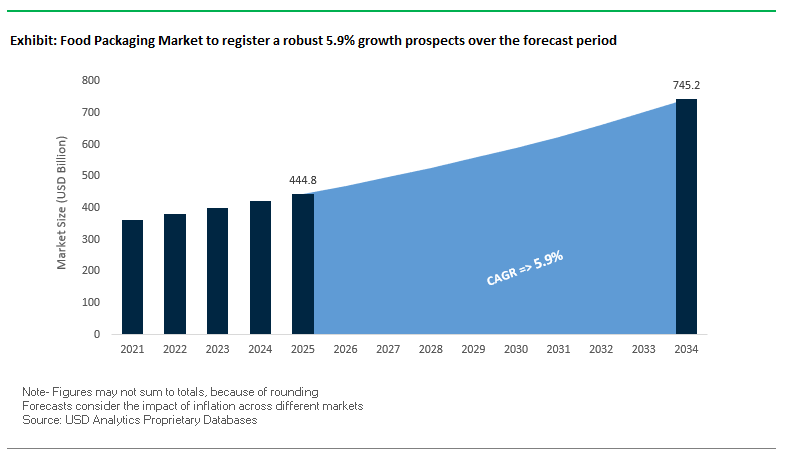

The global food packaging market is valued at $444.8 billion in 2025 and is projected to reach $745.1 billion by 2034, growing at a CAGR of 5.9%. This expansion reflects the rising consumer demand for safe, sustainable, and technology-enabled packaging solutions that meet the evolving requirements of both global brands and regulatory frameworks. For industry professionals and buyers, food packaging is not only about preservation but also about ensuring circularity, supply chain efficiency, and brand differentiation.

The industry is witnessing a sharp transition from linear to circular packaging models, with recyclability and lightweighting emerging as core design priorities. Flexible packaging formats are gaining significant traction for their efficiency in transportation and extended shelf-life capabilities. At the same time, the integration of smart and connected technologies into packaging formats is helping brands build stronger consumer engagement through traceability and transparency.

Key Insights for Industry Professionals:

- Shift Toward Circular Models: Aluminum and glass dominate due to their recyclability; U.S. aluminum cans average 71% recycled content.

- Flexible Packaging Expansion: Lightweight pouches and films are extending shelf life while reducing emissions.

- Smart Packaging Adoption: QR codes, NFC chips, and sensors enhance traceability and consumer trust.

- Lightweighting Strategies: Steel food cans are now 40% lighter than 30 years ago, reducing resource use and shipping costs.

Market Analysis: Recent Strategic Developments in Food Packaging

The food packaging sector is experiencing rapid transformation, driven by consolidation, innovation, and a strong pivot toward sustainability.

In August 2025, Amcor reported strong fiscal Q4 results, reflecting the successful execution of its sustainability-driven strategies following the April 2025 closure of its merger with Berry Global. This deal created a global leader in consumer and healthcare packaging solutions with a significantly expanded portfolio. At the same time, the July 2025 International Paper acquisition of DS Smith for $9.9 billion marked a significant consolidation in fiber-based packaging, while the Smurfit Kappa–WestRock merger completed in July 2025 created Smurfit WestRock, a powerhouse in paper and corrugated packaging.

On the innovation front, Huhtamaki introduced recyclable and compostable ice cream packaging in May 2025, demonstrating the industry’s continued investment in fiber-based solutions. Similarly, Ball Corporation divested its aerospace business in March 2025 for $5.6 billion, sharpening its focus on aluminum packaging. Meanwhile, WestRock’s February 2025 partnership with Recipe Unlimited is expected to prevent 31 million plastic containers from entering Canadian landfills annually, highlighting sustainability-driven collaborations.

Earlier moves also shaped the market Amcor and Berry Global’s November 2024 merger announcement was a pivotal moment, setting the stage for one of the largest consolidations in packaging history. These strategic developments underscore how the industry is being redefined by M&A activity, sustainability mandates, and material innovation.

Trends and Opportunities Driving Innovation in the Food Packaging Market

Strategic Reshoring and Supply Chain Diversification Driving Regionalized Investment

The food packaging market is undergoing a structural shift as food and beverage manufacturers accelerate reshoring strategies and supply chain diversification. Disruptions caused by the pandemic, geopolitical tensions, and rising logistics costs have exposed vulnerabilities in globalized supply chains, pushing companies to invest in regionalized manufacturing facilities closer to their end markets. This transition directly fuels demand for advanced packaging machinery, automation systems, and packaging materials in North America and Europe.

The U.S. food manufacturing industry is at the forefront of this shift. In 2024, the sector recorded 90 new capital projects, up from 64 in 2023, representing a combined investment of $15.3 billion. These investments are increasingly directed toward vertically integrated facilities capable of both production and in-house packaging. Recent examples include a $160 million bakery facility in Texas and a $110 million dairy product expansion in New York, both highlighting how manufacturers are aligning CapEx with consumer demand and packaging innovation. Analysts point to a “pent-up CapEx demand” in North America, where investment has lagged behind revenue growth. This imbalance is now being corrected, unlocking a new cycle of growth in packaging system upgrades, automation adoption, and demand for regionally optimized packaging designs.

Integration of AI and Machine Vision for Predictive Quality Control (PQC)

Another defining trend is the rapid adoption of AI-powered machine vision systems for predictive quality control (PQC). Unlike traditional systems that only reject defective packaging, new-generation AI solutions proactively analyze production data to detect anomalies, predict failures, and optimize processes. This advancement supports the food packaging industry’s shift toward zero-defect manufacturing, reduced waste, and improved operational efficiency.

Real-world case studies underscore this transformation. A major bakery group implementing AI-enabled vision cut rejection rates by 72% in just six months, saving 15 metric tons of bread annually that would otherwise have been discarded. In the UK, a meat processor deployed 3D imaging with AI and achieved a 99.9% detection rate for bone fragments as small as 2mm, eliminating a key safety hazard and avoiding potential recalls. Beyond defect detection, PQC systems are being used on high-speed bottling lines, monitoring fill levels, cap alignment, and seal integrity with real-time corrective feedback. By detecting subtle signals of equipment wear, these systems also facilitate predictive maintenance, ensuring higher uptime and lower production costs. The shift to AI-driven predictive control represents a fundamental leap in packaging efficiency and compliance with food safety standards.

Development of Agile and Modular “Skinnable” Machinery Platforms

The dynamic nature of FMCG and food markets with frequent product launches, limited editions, and smaller batch production is creating strong demand for agile and modular packaging machinery platforms. These so-called “skinnable systems” allow manufacturers to quickly reconfigure packaging lines without costly downtime, enabling seamless adaptation to new products and packaging formats.

Machinery suppliers are investing in quick-changeover technology, with some companies introducing tool-less part replacement systems that reduce downtime from hours to minutes. Modular automation platforms are also gaining traction, enabling multiple packaging formats such as cartons, trays, and flexible pouches to be run on a single line. Robotics plays a critical role in this transition, with programmable robotic arms now capable of handling different product sizes, package formats, and palletizing patterns with minimal reprogramming. This modularity supports high-mix, low-volume production environments, particularly in categories like snacks, bakery, and specialty beverages, where agility is a competitive differentiator.

Robotics-as-a-Service (RaaS) for Palletizing and End-of-Line Operations

The chronic labor shortage in food manufacturing, especially in physically demanding and repetitive areas like palletizing, is fueling demand for Robotics-as-a-Service (RaaS). This model eliminates the need for high upfront capital expenditure, enabling manufacturers to access advanced automation through a predictable operational expense structure.

Under RaaS, equipment providers retain ownership of the robots and handle maintenance, upgrades, and technical support, freeing food manufacturers to focus on production. This lowers financial and technical barriers, making automation viable for small and medium-sized enterprises (SMEs) in addition to large-scale manufacturers. A RaaS provider reported that its fleet surpassed 100,000 production hours and successfully packed and stacked over 1.2 billion products, demonstrating scalability and reliability. Service-level agreements (SLAs) ensure guaranteed uptime and performance, giving manufacturers confidence in operational continuity.

RaaS is emerging as a cornerstone of end-of-line packaging automation, supporting efficiency gains, reducing dependence on manual labor, and aligning with the industry’s shift toward flexible, technology-enabled packaging operations.

Competitive Landscape: Global Leaders Driving Innovation and Sustainability

The global food packaging market is dominated by multinational corporations with broad portfolios and global footprints. Competition is characterized by large-scale mergers, heavy investment in sustainable materials, and R&D efforts focused on recyclability and circularity.

Amcor: Expanding Portfolio Through Berry Global Merger

Amcor remains at the forefront of global packaging with its extensive portfolio of flexible and rigid solutions. The 2025 merger with Berry Global created one of the largest consumer and healthcare packaging companies worldwide. Amcor continues to drive innovation with AmFiber™ high-barrier paper-based packaging and AmPrima™ recycle-ready flexible solutions, alongside expanding its footprint with new facilities in Asia.

Ball Corporation: Reinforcing Aluminum Packaging Leadership

Ball Corporation is recognized globally for its lightweight, infinitely recyclable aluminum packaging. Following the sale of its aerospace division in March 2025, Ball sharpened its focus exclusively on packaging. Recent divestments, including a 41% stake sale in its Saudi Arabia joint venture, streamlined operations while retaining market presence in the Middle East. Its leadership in lightweighting technology and sustainability messaging positions Ball as a top choice for beverage and food companies.

Crown Holdings: Innovating Metal Food Containers with BPA-NI Coatings

Crown Holdings remains a global leader in metal packaging for food and beverages. The company reported $3.15 billion in Q2 2025 revenue, exceeding expectations, and continues to focus on expanding beverage can capacity worldwide. Its innovations in lightweighting and BPA-NI coatings ensure food safety while aligning with sustainability mandates, making Crown a critical partner for multinational brands.

Berry Global: Advancing Recycled and Circular Packaging Solutions

Berry Global has repositioned itself following the spin-off of its health and hygiene business into Magnera. The company focuses on recycling innovation and circular plastics, collaborating with brands like Mars and Mondelez to deliver 100% recycled packaging. By investing in AI-powered sorting technologies, Berry is improving recyclate quality while maintaining a strong position in rigid and flexible plastic packaging for foodservice and consumer applications.

International Paper: Strengthening Fiber-Based Packaging with DS Smith Acquisition

International Paper has expanded significantly through its $9.9 billion acquisition of DS Smith in July 2025, strengthening its leadership in corrugated and paperboard solutions. The company is also investing $250 million to convert its Riverdale mill for containerboard production, aligning with rising e-commerce and sustainable packaging demand. Its divestment of cellulose fibers ensures sharper focus on high-margin, fiber-based food packaging solutions.

Food Packaging Market Share Insights

Flexible Packaging Dominates Market Share by Packaging Type in Food Packaging

In 2025, flexible packaging secures 55% of the global food packaging market, establishing itself as the undisputed growth leader. Its dominance is rooted in the convergence of sustainability, cost reduction, and convenience three of the most powerful forces shaping the packaging industry. Pouches, films, and bags reduce material usage by up to 70% compared to rigid formats, significantly lowering transportation costs and carbon footprints while offering excellent barrier protection to extend shelf life. Flexible formats are also central to portion control and e-commerce logistics, where lightweighting directly improves operational efficiency. The large printable surface enables brands to achieve high-impact shelf presence and consumer engagement, making flexible packaging both a sustainability solution and a marketing vehicle. Rigid packaging, while holding a smaller share, remains irreplaceable in categories where structure, reusability, or product perception matters most such as glass bottles for dairy, metal cans for shelf-stable proteins, and rigid trays for fresh produce. This balance shows that flexible packaging dominates on efficiency and sustainability, while rigid packaging sustains relevance in premium and high-protection applications.

Ready Meals & Convenience Foods Lead Market Share by Application in Food Packaging

By application, ready meals and convenience foods represent 30% of the food packaging market in 2025, making this the largest and fastest-expanding end-use category. Rising urbanization, dual-income households, and on-the-go lifestyles drive consumer reliance on microwave-ready trays, dual-ovenable containers, and portion-controlled pouches. This segment is also a proving ground for new sustainable materials, with brands experimenting in compostable trays, recyclable mono-material pouches, and plant-based coatings to align with regulatory and consumer sustainability demands. Fruits and vegetables follow closely with 25%, where retailers are rapidly transitioning from plastic clamshells and trays to molded fiber punnets and paper-based bags to appeal to eco-conscious shoppers. Meat, poultry, and seafood remain safety-critical applications, where high-barrier films and modified atmosphere packaging (MAP) solutions are non-negotiable to ensure hygiene and shelf life. Bakery, confectionery, and dairy segments round out demand, leveraging packaging for freshness, branding, and functionality. Collectively, this landscape demonstrates how convenience foods anchor growth, fresh produce drives plastic-free innovation, and proteins sustain the demand for high-performance protective packaging.

United States: PFAS-Free Packaging and E-Commerce Innovation Driving Market Growth

The U.S. food packaging market is increasingly shaped by sustainability and corporate responsibility initiatives. Following Maine’s August 2025 “Fix It” bill aligning Extended Producer Responsibility (EPR) laws across states, companies are prioritizing recyclable and eco-friendly packaging solutions to meet regulatory and consumer expectations. PFAS-free packaging initiatives are gaining momentum, with manufacturers adopting alternative barrier coatings that provide grease and moisture resistance without harmful fluorochemicals. The rapid growth of e-commerce has further accelerated demand for durable, lightweight, and cost-effective packaging solutions, encouraging innovation in flexible and minimalist designs. In parallel, automation and robotics integration in packaging lines is improving operational efficiency and reducing waste, while smart and interactive packaging solutions leveraging QR codes, RFID, and NFC enhance consumer engagement by providing product origin, sustainability credentials, and interactive experiences.

Germany: Circular Economy Leadership and Advanced Paper-Based Packaging Solutions

Germany’s food packaging market is governed by one of the strictest regulatory frameworks globally, including the German Packaging Act (VerpackG), which mandates registration and recycling system participation for all packaging. The market leads Europe in recycling and waste reduction, driven by policies that encourage high recycled content and reusable solutions. Industry initiatives like the EU-funded CIRCULAR FoodPack project, involving the Fraunhofer Institute, are pioneering sustainable paper-based alternatives and tracer-based sorting technologies to separate food and non-food packaging waste efficiently. Germany’s commitment to the circular economy, combined with advanced sorting technologies and innovation in sustainable materials, positions the country as a model for eco-conscious packaging design and functionality.

China: Regulatory Reforms and Sustainable Solutions Shaping Market Dynamics

China’s food packaging market is experiencing significant transformations driven by regulatory reforms and sustainability mandates. New measures, including the revised Food Label Supervision and Administration Measures and the National Food Safety Standard General Rules for Prepackaged Food Labels (GB 7718-2025), will come into effect in 2027, strengthening food safety and compliance. Government bans on disposable plastics for e-commerce and takeaway food are encouraging the adoption of reusable and eco-friendly packaging solutions. Companies are also addressing environmental impacts from online delivery, with initiatives like Meituan’s “opt-out for disposable cutlery,” used by over 70% of Shanghai orders, reducing single-use plastic waste. Rising domestic demand from the growing e-commerce and food and beverage sectors, fueled by urbanization and a rising middle class, is further driving innovation and investment in sustainable and convenient packaging options.

India: Make in India and Technological Advancements Catalyzing Market Growth

India’s food packaging market is expanding rapidly due to government initiatives like “Make in India” and liberal FDI policies, positioning the country as a potential global hub for food and packaging materials. The adoption of AI-driven automation and smart packaging technologies is transforming operations, enhancing efficiency, and enabling innovative packaging solutions. Regulatory efforts by the Food Safety and Standards Authority of India (FSSAI) promote eco-friendly materials and the use of recycled PET in food-contact applications, supporting the circular economy. Additionally, the growth of the organic food sector is driving demand for packaging solutions that align with consumer preferences for sustainability and premium quality, reinforcing India’s emerging prominence in the global food packaging landscape.

Brazil: Bioplastics Innovation and Circular Economy Initiatives Driving Sustainable Packaging

Brazil’s food packaging industry is at the forefront of bioplastics development, with companies like Braskem producing green polyethylene from sugarcane ethanol to reduce reliance on fossil fuels. The Brazilian Health Regulatory Agency (Anvisa) has implemented clear regulatory frameworks for food contact materials, ensuring consumer safety and compliance. Initiatives supporting the circular economy, including upcoming legislative measures and the “eureciclo” program issuing Packaging Recycling Certificates, encourage companies to recycle a significant portion of their packaging and adopt environmentally responsible practices. Rapid growth in e-commerce is also creating demand for lightweight and durable packaging solutions, enabling cost-efficient shipping while supporting sustainability and waste reduction efforts.

Japan: High-Barrier Technology and Premium Sustainable Packaging Enhancing Market Competitiveness

Japan’s food packaging market emphasizes high-quality, aesthetic, and functional designs, driving demand for premium materials and decorative printing techniques. The industry is leading in high-barrier technology, developing transparent films with properties comparable to aluminum foil to extend shelf life while reducing material use and enhancing recyclability. Technological advancements, including innovative paper-plastic composite bags by companies like the Ajinomoto Group, ensure durability and moisture resistance while supporting sustainability objectives. The government and companies are actively promoting waste reduction and recycling, facilitating the transition to mono-material solutions and paper-based packaging, which aligns with the country’s circular economy goals.

Food Packaging Market Report Scope

Food Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$444.8 Billion

|

|

Market Size (2034)

|

$745.1 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Material Type (Plastics, Paper and Paperboard, Metal, Glass, Bioplastics), By Packaging Type (Flexible Packaging, Rigid Packaging), By Application (Fruits & Vegetables, Meat, Poultry & Seafood, Dairy & Dairy Products, Bakery & Confectionery, Ready Meals & Convenience Foods, Other Applications), By End-Use (Food Manufacturers, Food Service Providers, Retailers, Households)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, International Paper Company, WestRock Company, Smurfit Kappa Group plc, Mondi Group, DS Smith Plc, Huhtamaki Oyj, Graphic Packaging Holding Company, Sonoco Products Company, Crown Holdings Inc., Ardagh Group S.A., Tetra Pak International S.A., Ball Corporation, Berry Global Group, Inc., Silgan Holdings Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Food Packaging Market Segmentation

By Material Type

- Plastics

- Paper and Paperboard

- Metal

- Glass

- Bioplastics

By Packaging Type

- Flexible Packaging

- Rigid Packaging

By Application

- Fruits & Vegetables

- Meat

- Poultry & Seafood

- Dairy & Dairy Products

- Bakery & Confectionery

- Ready Meals & Convenience Foods

- Other Applications

By End-Use

- Food Manufacturers

- Food Service Providers

- Retailers

- Households

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Food Packaging Market

- Amcor plc

- International Paper Company

- WestRock Company

- Smurfit Kappa Group plc

- Mondi Group

- DS Smith Plc

- Huhtamaki Oyj

- Graphic Packaging Holding Company

- Sonoco Products Company

- Crown Holdings Inc.

- Ardagh Group S.A.

- Tetra Pak International S.A.

- Ball Corporation

- Berry Global Group, Inc.

- Silgan Holdings Inc.

*List not Exhaustive

Research Coverage

This report investigates the dynamic and evolving landscape of the global food packaging market, providing a comprehensive overview of breakthroughs, strategic developments, and market trends that are shaping the industry. USDAnalytics’ analysis reviews the latest innovations in sustainable, smart, and functional packaging solutions, highlighting key factors driving adoption, including regulatory compliance, circular economy initiatives, and technology-enabled consumer engagement. The report highlights significant M&A activity, product launches, and regional developments while examining the influence of emerging materials like bioplastics, paper-based solutions, and high-recycled-content plastics. It also emphasizes the convergence of flexible and rigid packaging formats, AI-driven predictive quality control, and robotics-based automation as pivotal forces redefining operational efficiency. This report is an essential resource for investors, packaging manufacturers, food service providers, and industry stakeholders seeking a forward-looking perspective on market growth, competitive positioning, and regulatory adaptation from 2025 to 2034, supported by historical insights from 2021 to 2024. In addition, the study profiles leading global players to provide actionable intelligence on strategic priorities, technological advancements, and sustainability-driven practices.

Scope Highlights:

- Segmentation: By Material Type (Plastics, Paper & Paperboard, Metal, Glass, Bioplastics), By Packaging Type (Flexible Packaging, Rigid Packaging), By Application (Fruits & Vegetables, Meat, Poultry & Seafood, Dairy & Dairy Products, Bakery & Confectionery, Ready Meals & Convenience Foods, Other Applications), By End-Use (Food Manufacturers, Food Service Providers, Retailers, Households)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Historic and Forecast Data: Historic data from 2021 to 2024; forecast data from 2025 to 2034

- Companies: Analysis and profiles of 15+ leading companies, including Amcor plc, International Paper Company, WestRock Company, Smurfit Kappa Group plc, Mondi Group, DS Smith Plc, Huhtamaki Oyj, Graphic Packaging Holding Company, Sonoco Products Company, Crown Holdings Inc., Ardagh Group S.A., Tetra Pak International S.A., Ball Corporation, Berry Global Group, Inc., Silgan Holdings Inc.

Methodology

The research methodology employed by USDAnalytics combines rigorous primary and secondary research techniques to deliver an accurate and actionable assessment of the global food packaging market. Primary research includes interviews with industry executives, R&D heads, and key stakeholders to obtain firsthand insights on market trends, technology adoption, and strategic initiatives. Secondary research involves comprehensive analysis of company reports, investor presentations, regulatory documents, trade journals, and sustainability studies to validate market drivers, competitive dynamics, and regional variations. Quantitative modeling techniques, including CAGR projections, market sizing, and segmentation analysis, were applied to ensure precise forecasts from 2025 to 2034. Additionally, USDAnalytics leverages comparative benchmarking and scenario-based modeling to evaluate the impact of emerging technologies such as AI-driven predictive quality control, robotics automation, and smart packaging solutions. The methodology also incorporates evaluation of historical trends from 2021 to 2024 to provide a robust understanding of market evolution, competitive positioning, and adoption patterns across geographies, applications, and material types.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.