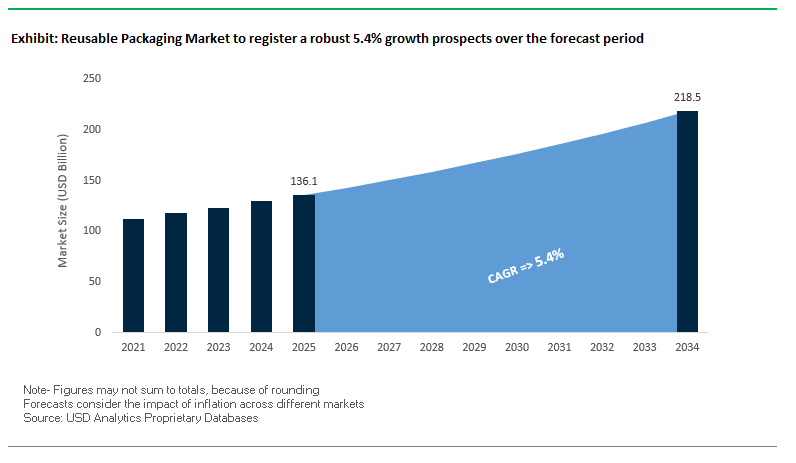

Reusable Packaging Market Overview: Cost-Efficiency and Sustainability Drive Growth (MV: USD 136.1 Bn in 2025 → USD 218.5 Bn by 2034, CAGR 5.4%)

The global reusable packaging market is expanding rapidly as industries transition from single-use to circular packaging models. The sector is underpinned by measurable benefits in total cost of ownership (TCO), waste reduction, and supply chain efficiency. Businesses are increasingly willing to absorb higher upfront investment, knowing reusable systems generate ROI within 12–18 months and reduce product damage and waste by double-digit percentages.

The market spans plastic crates, pallets, foldable containers, bulk bins, and modular systems, applied across food & beverage, automotive, healthcare, retail, and logistics. As global EPR laws and the EU’s Packaging and Packaging Waste Regulation (PPWR) tighten definitions of “reusable,” companies are responding with durable, trackable, and recyclable systems that deliver both compliance and operational efficiency.

Key insights for industry professionals:

- ROI advantage: Lifecycle economics show up to 60% cost savings compared to single-use over time.

- Damage prevention: RPCs can cut supply chain damage by 98%, ensuring product integrity.

- Carbon footprint: Life-cycle analysis demonstrates up to 60% CO₂ reduction compared to disposables.

- Waste minimization: A single RPC replaces hundreds of corrugated cartons, easing landfill pressure.

Market Analysis: Strategic Shifts and Regulatory Reinforcement

The last two years highlight how automation partnerships, strategic acquisitions, and regulatory updates are accelerating adoption of reusable packaging. In August 2025, Rehrig Pacific partnered with AutoStore, positioning itself as the U.S. bin manufacturing partner for robotic warehouses, showing the fusion of automation and reusable logistics assets. The same month, Nefab Group acquired FARUSA Emballage, enhancing its heavy-duty corrugated reusable portfolio and signaling regional consolidation in Northern Europe.

Also in June 2025, Schoeller Allibert deepened its European presence by naming Transoplast a platinum distribution partner in the Netherlands, while March 2025 saw its SBTi-validated carbon reduction targets, cementing sustainability as a growth differentiator. May 2025 brought the EU’s updated PPWR, codifying reuse criteria, pushing converters and OEMs to redesign packaging systems for compliance.

Automation is also reshaping demand: April 2025, SSI SCHAEFER completed a semi-automated warehouse for Rossmann in Hungary, embedding reusable packaging into intralogistics flows. Meanwhile, new reusable packaging product launches highlight innovation: November 2024 saw GWP Correx’s Rapitainer debut, designed to replace corrugated boxes with durable crates, and October 2024 brought Tri-Wall Circular’s YOYOBin Adjustable for automotive supply chains.

Reusable Packaging Market: Trends and Opportunities Driving Circular Supply Chains

Mandated Adoption Driven by Stringent Extended Producer Responsibility (EPR) Regulations

A defining trend in the reusable packaging market is the regulatory push from Extended Producer Responsibility (EPR) frameworks, with the European Union’s Packaging and Packaging Waste Regulation (PPWR) serving as a global blueprint. Enforced in February 2025, the PPWR establishes binding reuse and refill targets, reshaping how companies design, distribute, and manage packaging. One of its most significant provisions requires that 10% of beverages sold in the EU by 2030 must be delivered through reusable packaging within a reuse system. This regulatory mandate creates both compliance pressure and a market expansion opportunity for reusable packaging formats such as glass bottles, crates, and rigid containers. Beyond beverages, the regulation extends to e-commerce packaging, setting a maximum 50% empty space ratio for grouped parcels from January 2030. This measure not only discourages inefficient single-use packaging but also promotes compact, reusable logistics solutions. With governments outside the EU watching closely, these EPR-driven mandates are expected to ripple into North America and Asia-Pacific, reinforcing reusable packaging as a regulatory and market necessity.

Strategic Corporate Investment in Washing and Logistics Infrastructure

Another trend reshaping the reusable packaging market is the strategic scaling of washing, sanitizing, and reverse logistics infrastructure. Major consumer packaged goods (CPG) companies and global retailers are transitioning from small-scale pilot projects to dedicated, high-capacity washing hubs capable of processing reusable packaging for multiple brands. A report by Upstream Solutions emphasizes that this centralized approach reduces costs while ensuring hygiene and regulatory compliance across industries like food, beverages, cosmetics, and household goods. To further improve efficiency, companies are creating regionalized hubs for collection, cleaning, and redistribution. By reducing transport distances and consolidating operations, these hubs achieve economies of scale, cut emissions, and lower the capital intensity of reuse adoption. This collaborative infrastructure strategy prevents fragmentation and allows brands to avoid building costly proprietary systems, accelerating the mainstream adoption of reusable packaging across global retail supply chains.

B2B Pooling Systems for Non-Food Retail and Manufacturing

The evolution of B2B pooling systems presents one of the most immediate opportunities for the reusable packaging market. While pooling is already mature in sectors like food logistics, particularly fresh produce, it is rapidly expanding into non-food retail and manufacturing. In the automotive sector, manufacturers have long used standardized reusable crates and pallets in closed-loop pooling systems, achieving significant reductions in packaging waste and operational inefficiencies. A logistics case study highlighted how these returnable plastic containers ensure consistent material flow from suppliers to assembly plants while lowering costs. Building on this success, similar models are being applied to general retail. A European electronics retailer partnered with a returnable packaging provider to deploy standardized, reusable delivery containers for store replenishment. This eliminated vast amounts of single-use cardboard waste while improving stocking efficiency. These examples highlight how pooling can standardize material flow across multiple industries, offering scalability and sustainability while meeting both cost and compliance objectives.

Technology-Enabled Reuse-As-A-Service (RaaS) Platforms

Another high-potential opportunity is the development of Reuse-as-a-Service (RaaS) platforms that combine physical packaging with digital services. These platforms integrate IoT and RFID technologies to provide real-time asset visibility, capturing data on location, condition, and reuse cycles. A technical review on smart packaging notes that such data-driven insights help companies minimize asset loss, ensure higher utilization rates, and provide auditable proof for sustainability reporting. RaaS providers go beyond packaging rental by offering end-to-end services, including cleaning, logistics, and performance analytics. This creates a subscription-like model where businesses can track ROI by measuring cost savings, cycle counts, and asset efficiency. Furthermore, the monetization of data allows brands to analyze reuse performance at SKU level, providing actionable intelligence to optimize supply chain operations. With global brands under pressure to prove compliance with ESG commitments, RaaS platforms are emerging as critical enablers of scalable, measurable, and profitable reusable packaging systems.

Competitive Landscape: Leading Innovators in Reusable Packaging Solutions

The competitive field is dominated by companies excelling in durability, automation readiness, circularity, and regional expansion. Each is pursuing sustainability-linked strategies, building capacity, and leveraging acquisitions to consolidate share.

Schoeller Allibert — Driving sustainability through recycled content integration

Schoeller Allibert leads Europe’s RPC sector with crates, foldable large containers (FLCs), pallets, and dollies. In June 2025, it expanded Dutch reach via a Transoplast platinum partnership, while its March 2025 SBTi target validation reinforced ESG commitments. With EcoVadis gold ratings and exceeding its 35% recycled content goal (achieved 48% in 2022), the company demonstrates circular design leadership, including innovative projects like Tetra Pak-sourced transport crates.

Rehrig Pacific Company — Expanding into automation and smart logistics

Rehrig Pacific blends pallets, crates, and roll-out carts with data-enabled supply chain services. In August 2025, it became AutoStore’s U.S. bin manufacturing partner, showing its push into robotic warehouse ecosystems. Earlier in October 2024, it opened a major Arizona manufacturing facility, doubling potential capacity. Its GMA Rackable Plastic Pallet integrates IoT monitoring (temperature, shock, vibration), exemplifying its smart, sustainable, and recyclable solutions portfolio.

DS Smith Plc — Scaling fiber-based reusable and recyclable systems

DS Smith dominates fiber-based reusable packaging, leveraging its closed-loop recycling model. It has already replaced 1+ billion problem plastics, 16 months ahead of its 2025 target, and launched designs like TapeBack tear-strip eliminator. With a 46% GHG reduction target by 2030, DS Smith integrates Circular Design Principles into its innovation pipeline, making it a go-to partner for sustainability-driven FMCG and e-commerce clients.

Myers Industries, Inc. — Industrial durability through rotational molding

Myers Industries’ Buckhorn brand is synonymous with rugged reusable transport packaging. The company is undergoing a Focused Transformation, streamlining operations and targeting USD 20 million cost savings by end-2025. Its rotational molding expertise allows production of highly durable bulk containers and pallets for industrial, automotive, and agri-food applications. It reclaims 99% of plastic scrap, reinforcing its zero-waste manufacturing philosophy.

SSI SCHAEFER — Embedding reusable packaging into intralogistics

SSI SCHAEFER integrates automation and reusable packaging via vertical lift modules, ASRS, and AGVs. Its April 2025 Rossmann semi-automated warehouse demonstrates synergy between logistics automation and reusable packaging flows. With its 2024 sustainability report, the company committed to greener intralogistics, positioning its technologies as enablers of circular, efficient supply chains in food, retail, and healthcare.

Reusable Packaging Market Share Insights, 2025-2034

Pallets & Crates dominate Market Share by Product Type in the Reusable Packaging Industry

In the broader reusable packaging market, pallets and crates lead with 45%, underscoring their irreplaceable role as the foundation of global supply chains. Their adoption is propelled by the shift from single-use wooden pallets to reusable plastic and metal formats, which deliver durability, hygiene, and total cost savings over hundreds of cycles. Intermediate Bulk Containers (IBCs) secure a significant share by enabling the safe and efficient movement of liquids, powders, and granules, becoming essential in chemical, pharmaceutical, and food ingredient supply chains. Bottles and containers are emerging as the consumer-facing growth engine, spurred by brand commitments to refill and reuse systems across beverages, cosmetics, and homecare, where sustainability directly intersects with branding. Drums and barrels, while traditional workhorses, are seeing share erosion as IBCs displace them for bulk liquid handling, though they remain entrenched in certified chemical and hazardous material applications. Collapsible bins, despite holding a niche share, are recognized as logistics efficiency enablers, reducing reverse logistics costs by collapsing up to 80% in volume, particularly in automotive and retail closed-loop systems. This segmentation highlights the duality of the market: industrial efficiency on one side and consumer-driven sustainability innovation on the other.

Food & Beverages lead Market Share by End-Use Industry in the Reusable Packaging Industry

The food & beverages sector commands 35%, reflecting its unmatched demand for hygienic, durable, and cost-efficient reusable packaging across pallets, crates, and IBCs. This dominance is reinforced by the sector’s focus on reducing spoilage, maintaining cold chain integrity, and enabling high-speed sanitization cycles. The chemicals industry follows as a compliance-driven stronghold, relying heavily on reusable IBCs and drums where secure containment of hazardous or sensitive materials is legally mandated, ensuring safety and regulatory adherence. E-commerce and retail are the fastest-growing segments, leveraging totes, bins, and collapsible containers to streamline fulfillment and reverse logistics while reducing single-use packaging waste. Automotive continues as a precision-focused user, deploying custom-designed reusable systems to protect high-value, sensitive components in JIT manufacturing, where downtime costs far outweigh packaging expenses. Healthcare and pharmaceuticals, though smaller in volume, hold one of the highest-value niches, requiring validated sterilization, tamper-evidence, and compliance with clean-room standards. Personal care and cosmetics close the distribution by using reusable bottles and jars as both a branding differentiator and sustainability strategy, driving innovation in consumer-facing packaging formats. Together, these industries demonstrate how volume-intensive F&B and compliance-heavy chemicals anchor the market, while e-commerce and consumer brands inject growth momentum.

European Union: PPWR and Reusable Packaging Obligations Reshaping Industry

The European Union reusable packaging market is undergoing transformative change with the enforcement of the Packaging and Packaging Waste Regulation (PPWR) in February 2025. This regulation establishes sector-specific reuse targets and mandates a reduction in packaging waste per capita by 5% by 2030, 10% by 2035, and 15% by 2040, compared to 2018 levels. The directive directly accelerates the transition from single-use packaging toward reusable formats across retail, foodservice, and logistics.

Germany plays a leading role, having introduced its “reusable packaging obligation” in January 2023, requiring foodservice outlets to provide reusable takeaway packaging alternatives at no extra cost. Alongside this, the Deposit Return Systems (DRS) initiative is expanding across the bloc to ensure higher collection rates of bottles and containers. The Ecodesign for Sustainable Products Regulation (ESPR) complements these shifts by introducing Digital Product Passports to ensure compliance transparency, while restrictions on substances like PFAS in food contact packaging (effective August 2026) are driving innovation in material science. Together, these measures make the EU a frontrunner in creating a circular economy for reusable packaging.

United States: EPR Laws and Corporate Sustainability Targets Accelerating Adoption

The United States reusable packaging market is increasingly shaped by Extended Producer Responsibility (EPR) laws, now enacted in seven states, including Maryland, which requires Producer Responsibility Organizations (PROs) to cover at least 90% of packaging waste management costs by 2030. These policies are reshaping supply chains and encouraging businesses to adopt reusable packaging models. The U.S. Plastics Pact is another critical driver, aligning stakeholders toward national goals for a circular economy.

Private sector initiatives are also fueling market expansion. PepsiCo has set a target to ensure 97% or more of its primary and secondary packaging in key markets will be reusable, recyclable, or compostable by 2030, while Unilever is piloting concentrated detergent formats that reduce overall packaging needs and transport emissions. Investments in advanced recycling facilities supported by the Infrastructure Investment and Jobs Act are building the infrastructure necessary for scaled adoption. Alongside these efforts, the growing emphasis on mono-material packaging and lightweight designs highlights the U.S.’s dual focus on sustainability and cost efficiency in reusable packaging adoption.

China: Government Mandates and Logistics Giants Leading Reuse Transformation

The China reusable packaging market is expanding rapidly under regulatory mandates and logistics-driven innovation. From June 1, 2025, express delivery companies are legally required to prioritize reusable and eco-friendly packaging, a policy that aligns with the 14th Five-Year Plan and its goals to reduce plastic pollution. The National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are reinforcing this agenda by tightening restrictions on wasteful packaging.

Leading logistics companies such as JDL Express and SF Express are implementing reusable circulation boxes for inter-station transport, directly replacing disposable cardboard. Furthermore, Shanghai’s plastic restriction policy (September 2025) bans “greenwashing” packaging products and prohibits foam bowls and plastic straws, reinforcing stricter compliance. The government is also incentivizing the remanufacturing industry and offering tax benefits for companies investing in green technologies, making China one of the fastest-growing markets for reusable packaging in e-commerce and logistics.

India: EPR Mandates and Traceability Rules Driving Reusable Packaging Growth

The India reusable packaging market is strongly influenced by the Plastic Waste Management (Amendment) Rules, 2024, which highlight Extended Producer Responsibility (EPR) for producers, importers, and brand owners. While MSMEs are exempt, larger entities must comply with strict guidelines. Effective July 1, 2025, all plastic packaging must be traceable through barcodes or QR codes, improving accountability. Additionally, from April 1, 2025, PIBOs are obligated to include a minimum of 30% recycled content in rigid plastic packaging.

The country’s rising consumption of processed and packaged foods is another significant driver, fueling demand for durable, reusable formats that can withstand India’s diverse climate and logistics challenges. Reusable packaging is gaining traction not only in food distribution but also in pharmaceuticals and FMCG sectors. With its regulatory push and growing consumer awareness, India is positioning itself as an emerging hub for reusable and recycled packaging innovation.

Japan: Circular Economy Strategy and Refillable Packaging Innovations

The Japan reusable packaging market is strongly guided by the Plastic Resource Circulation Strategy, which mandates that all plastic packaging and goods must be reusable or recyclable by 2025. This regulation is complemented by the Plastic Resource Circulation Promotion Law (2025), which requires redesign or reduction of 12 single-use plastic categories, pushing industries toward reusable or compostable alternatives. The government’s goal of doubling renewable material usage by 2030 further reinforces this shift.

Japanese companies are at the forefront of innovation. Shiseido and Tokiwa Cosmetics are leading in refillable packaging for beauty and personal care, offering products such as refillable creams, serums, and foundations. Simultaneously, collaborations with global firms like LyondellBasell are integrating bio-polypropylene (bio-PP) into cosmetics and consumer goods packaging. The combination of regulatory enforcement, consumer demand for premium sustainability, and strong industrial innovation makes Japan a key market setting global benchmarks in reusable packaging technologies.

Reusable Packaging Market Report Scope

Reusable Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$136.1 Billion

|

|

Market Size (2034)

|

$218.5 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material (Plastics, Glass, Metal, Paper & Paperboard, Wood), By Product Type (Bottles & Containers, Pallets & Crates, Drums & Barrels, IBCs, Collapsible Bins), By End-Use Industry (Food & Beverages, E-commerce & Retail, Healthcare & Pharmaceuticals, Personal Care & Cosmetics, Automotive, Chemicals), By Circulation Model (Closed-Loop Systems, Open-Loop Systems, Pooling Services)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, DS Smith Plc, Smurfit Kappa Group Plc, Graphic Packaging Holding Company, Sonoco Products Company, Huhtamaki Oyj, International Paper Co., WestRock Company, ProAmpac, Berry Global, Inc., Greif, Inc., Silgan Holdings Inc., Pactiv Evergreen Inc., PAPACKS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Reusable Packaging Market Segmentation

By Material

- Plastics

- Glass

- Metal

- Paper & Paperboard

- Wood

By Product Type

- Bottles & Containers

- Pallets & Crates

- Drums & Barrels

- IBCs

- Collapsible Bins

By End-Use Industry

- Food & Beverages

- E-commerce & Retail

- Healthcare & Pharmaceuticals

- Personal Care & Cosmetics

- Automotive

- Chemicals

By Circulation Model

- Closed-Loop Systems

- Open-Loop Systems

- Pooling Services

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Reusable Packaging Market

- Amcor plc

- Mondi Group

- DS Smith Plc

- Smurfit Kappa Group Plc

- Graphic Packaging Holding Company

- Sonoco Products Company

- Huhtamaki Oyj

- International Paper Co.

- WestRock Company

- ProAmpac

- Berry Global, Inc.

- Greif, Inc.

- Silgan Holdings Inc.

- Pactiv Evergreen Inc.

- PAPACKS

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive research methodology to provide precise, actionable insights into the global reusable packaging market. Our approach combines extensive secondary research—including corporate filings, sustainability and ESG reports, regulatory frameworks, and industry publications—with primary interviews of manufacturers, logistics providers, retailers, and end-users across food & beverage, automotive, healthcare, e-commerce, and chemicals sectors. We analyze key metrics such as total cost of ownership (TCO), lifecycle CO₂ reduction, waste minimization, product protection, and operational efficiency. Quantitative modeling incorporates market adoption trends, regulatory influences (EPR laws, EU PPWR, Plastic Resource Circulation strategies), automation integration, and technology-enabled platforms such as Reuse-as-a-Service (RaaS). USDAnalytics also assesses mergers, acquisitions, partnerships, and innovation pipelines to map competitive dynamics and growth potential. This methodology ensures a high-resolution view of market value, CAGR, regional adoption, and end-use segmentation, enabling industry professionals to make informed decisions on scalable, compliant, and sustainable reusable packaging solutions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.