Market Overview: Refillable Packaging Market Set for Robust Growth Driven by Sustainability and Cost-Efficiency

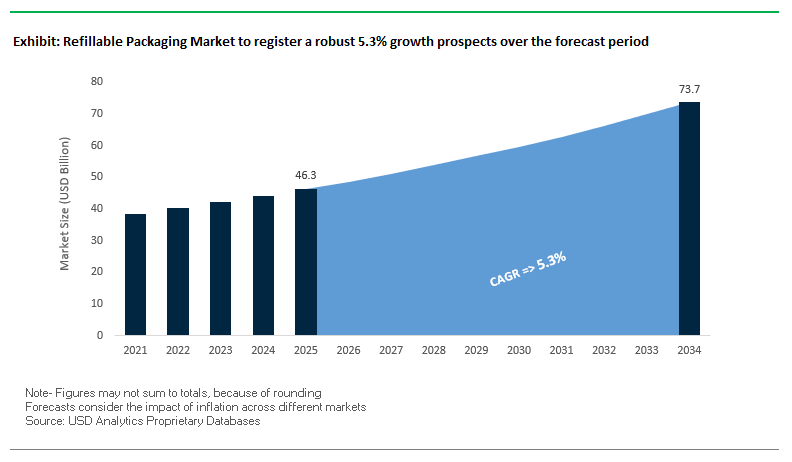

The global refillable packaging market is projected to grow from $46.3 billion in 2025 to $73.7 billion by 2034, at a CAGR of 5.3%. The market is gaining traction due to increasing environmental awareness, regulatory pressures, and corporate sustainability initiatives. Refillable packaging is recognized for its ability to reduce solid waste, lower carbon footprints, and improve supply chain efficiency, making it a strategic choice for companies aiming to implement circular economy models.

Key Insights for industry professionals and buyers:

- Significant Waste Reduction: Reusable transport packaging systems, like RPCs, generate up to 86% less solid waste than single-use alternatives.

- Lower Carbon Footprint: Refillable models can reduce CO2 emissions by up to 60% compared to single-use packaging.

- Enhanced Supply Chain Efficiency: Standardized reusable containers minimize product damage by up to 98% and are compatible with automated warehouse systems.

- Cost Savings Over Time: Companies can reduce recurring packaging costs by up to 50% through durable, reusable solutions.

- Integration with Sustainability Goals: Increasing adoption aligns with brand ESG strategies and regulatory compliance.

- Innovation Opportunities: Refillable packaging encourages design improvements in durability, barrier performance, and user convenience.

These factors highlight the strategic and operational benefits of refillable packaging, providing industry players with opportunities to optimize costs while promoting sustainability.

Market Analysis: Strategic Partnerships and Technological Innovations Are Shaping Refillable Packaging Adoption

The refillable packaging market is evolving rapidly due to partnerships between leading brands and packaging innovators, along with technological advancements. In August 2025, Mars collaborated with Berry Global to transition pantry jars for M&M'S® and other brands to 100% recycled packaging, with a clear focus on future refillable models. In the same month, the UK-based Flexible Plastic Fund (FPF), alongside SUEZ Recycling and Recovery UK, released the FlexCollect report, providing a blueprint for integrating flexible plastic packaging into household recycling systems—a key enabler for refillable pouches and flexible refill solutions.

Innovations in materials and sustainable design are further driving market growth. In June 2025, DS Smith launched a fiber-based e-commerce bag for Matas Group, a Danish beauty retailer, supporting a refill-at-home model. Earlier, in April 2025, Amcor partnered with Nfinite Nanotechnology to improve oxygen barrier performance in recyclable and compostable packaging, critical for maintaining product quality in refillable systems. In March 2025, Cascades Inc. introduced produce baskets made from 100% recycled fibers, designed for durability and repeated use in supply chains.

Leading brands are also piloting consumer-facing refillable initiatives. In December 2024, Nestlé launched reusable stainless-steel containers for KitKat and Lion products in France, while Hermès unveiled refillable glass bottles for its Le Bain collection. Strategic mergers, such as Smurfit Kappa and WestRock in September 2024, provide scale and expertise for B2B refillable solutions. Earlier, in July 2023, Coca-Cola announced a target to achieve 25% refillable packaging globally by 2030, signaling long-term industry commitment.

Refillable Packaging Market: Trends and Opportunities Accelerating Circular Systems

Scalable Refill-at-Home Systems from Major CPG Brands

One of the most transformative trends in the refillable packaging market is the rapid scaling of refill-at-home systems by consumer packaged goods (CPG) leaders. Unilever has been at the forefront, piloting refill solutions in emerging markets such as Indonesia. As of July 2024, the company reported that it is serving approximately 6,000 customers across 1,000 refill stations, achieving a reduction of nearly 6 metric tons of plastic annually. These trials underline two critical adoption factors: affordability and convenience. By lowering refill costs and ensuring accessibility, Unilever is building consumer trust and engagement with circular packaging models. Similarly, Procter & Gamble (P&G) has made refill models central to its sustainability roadmap. In August 2025, the company announced that brands like Olay and Head & Shoulders are adopting refill pouches that use up to 60% less plastic compared to bottles. Consumers purchase durable starter containers once and subsequently refill them, thereby cutting plastic consumption at scale. Together, these initiatives are proving that refillable packaging can work across both developed and emerging markets, creating scalable pathways for waste reduction in the personal care and household sectors.

Standardization of Returnable/Reusable Transport Packaging (RTP) in Retail Supply Chains

Another major trend in the refillable packaging market is the shift towards mandatory returnable transport packaging (RTP) for retail supply chains. Initially promoted as voluntary initiatives, RTP adoption is now being driven by retailer requirements that suppliers transition to reusable crates, pallets, and containers. Companies like Schoeller Allibert highlight that their RTP systems can last up to 15 years, creating a sustainable and cost-effective alternative to single-use packaging formats such as corrugated cartons and wooden pallets. Efficiency is another strong driver of this trend. Solutions like Nilkamal BubbleGUARD collapsible pallets can be quickly assembled and disassembled, and when empty, they nest compactly—reducing return-transport volume by up to 80%. This efficiency cuts both labor costs and fuel consumption, directly lowering emissions across the supply chain. The integration of RTP into large-scale retail operations reflects a strategic move from one-time use packaging towards circular logistics systems, enabling cost savings while reducing packaging waste streams at an industrial level.

Development of Interoperable and Standardized Refill Ecosystems

A major opportunity in the refillable packaging market lies in the development of shared, interoperable refill platforms. A critical barrier to scaling has been the fragmented approach, with brands developing proprietary systems that are difficult to expand beyond single companies. Companies like Reposit are tackling this by offering “packaging-as-a-service” models, where brands and retailers share a pool of standardized reusable containers. This approach lowers entry barriers for smaller brands while creating economies of scale for logistics providers. The importance of consumer participation is equally evident. Lush Cosmetics’ “Bring It Back” program demonstrates how financial incentives can drive closed-loop packaging recovery. Customers are offered $1 off per returned pot, or a free face mask for five returned pots, leading to significant return rates for its black pot containers, which are recycled into new ones. This model highlights how behavioral economics and shared infrastructure can work in tandem to accelerate the adoption of refillable packaging.

Integration of Smart Technology for Deposit, Return, and Traceability

Another transformative opportunity comes from integrating smart technologies into refillable packaging systems. The deployment of QR codes, RFID, and IoT-enabled tags is enabling automated deposit return mechanisms and real-time tracking of reusable assets. According to a 2025 Roambee report, IoT-enabled returnable pallets and containers now provide data on location, fill level, and reuse cycles, allowing companies to optimize asset utilization, reduce losses, and cut down on reverse logistics inefficiencies. Beyond tracking, digital identifiers are paving the way for digital product passports (DPPs), which will soon become mandatory in the EU. By embedding lifecycle data into packaging, brands can ensure regulatory compliance while also communicating sustainability credentials to consumers. These passports not only boost transparency but also strengthen consumer trust, positioning refillable packaging as a cornerstone of traceable and compliant supply chains. As regulatory frameworks tighten and data-driven supply chains become the norm, smart-enabled refillable packaging will become a high-growth segment of the global circular economy.

Competitive Landscape: Leading Packaging Companies Are Driving Refillable Solutions Through Innovation and Circular Economy Integration

The competitive landscape of refillable packaging is defined by companies that combine product innovation, closed-loop systems, and sustainability strategies to meet market demand. Industry leaders are leveraging partnerships, R&D, and acquisitions to scale reusable and refillable solutions.

DS Smith Plc: Innovating Fiber-Based Refillable Packaging for E-Commerce and B2B Logistics

DS Smith provides sustainable, recyclable paper-based packaging solutions, including retail-ready packaging, transit cases, and e-commerce formats. In June 2025, DS Smith launched a fiber-based e-commerce bag supporting refill-at-home models, and in January 2025, introduced TapeBack, eliminating single-use plastic tear strips. Its circular design principles and closed-loop recycling model allow brands to optimize recyclability and performance metrics, providing a competitive edge in refillable packaging solutions.

Smurfit Kappa Group (Smurfit WestRock): Leveraging Scale and Expertise to Expand Durable Refillable Packaging

Smurfit Kappa offers corrugated, folding carton, and bag-in-box solutions optimized for repeated use in supply chains. The September 2024 merger with WestRock created Smurfit WestRock, enhancing its global footprint and expertise. The company operates a closed-loop recycling model, ensuring recovered fiber is reused efficiently. Products like corrugated crates and trays are engineered for durability and stackability, making them ideal for B2B refillable logistics.

Amcor plc: Advancing Refillable Packaging Through Nanotechnology and Sustainable Materials

Amcor provides rigid and flexible packaging solutions with a strong focus on recyclable and reusable features. In April 2025, the company partnered with Nfinite Nanotechnology to improve oxygen barrier performance, crucial for refillable packaging. Its EcoGuard™ brand highlights products with sustainable features, and participation in initiatives like the Ellen MacArthur Foundation’s New Plastics Economy demonstrates a strategic commitment to circular economy practices.

Nestlé S.A.: Pioneering Consumer-Facing Refillable Packaging with Stainless-Steel and Returnable Systems

Nestlé is actively developing refillable packaging solutions, including a pilot program in France (Dec 2024) for KitKat and Lion products in reusable stainless-steel containers. Investments include $30 million in the US to increase the use of food-grade recycled plastics. Nestlé explores multiple models such as in-store refill stations, return-from-home systems, and reusable B2B transport packaging, aiming to make all packaging recyclable or reusable by 2025.

The Coca-Cola Company: Setting Global Refillable Packaging Targets to Reduce Single-Use Plastic Dependence

Coca-Cola is driving the refillable packaging market with its “World Without Waste” initiative. In July 2023, the company set a goal for 25% of global product volume to be refillable by 2030. Coca-Cola is reintroducing refillable glass bottles and aluminum cans in various markets, collaborating with retailers and local governments to optimize collection and return systems, ensuring the scalability and success of its refillable initiatives.

Refillable Packaging Market Share Insights, 2025-2034

Homecare Leads Market Share by Application in the Refillable Packaging Industry

Homecare applications command the largest share of the refillable packaging industry at 35%, underscoring their role as the logical first movers in reusable systems. Detergents, soaps, and cleaning agents lend themselves naturally to refill models due to their high consumption frequency, long shelf life, and low contamination risk, which minimizes regulatory and safety hurdles. The industry is shifting toward ultra-concentrated refills that cut both transport emissions and packaging material use, aligning with corporate zero-waste targets and Extended Producer Responsibility (EPR) frameworks. Personal care and cosmetics follow at 30%, leveraging refillable formats to create premium consumer experiences, particularly in skincare, perfumes, and cosmetics where brands integrate durable, branded primary containers to enhance loyalty and prestige. Food and beverages at 20% remain more constrained by hygiene and logistics but show growth in structured niches like bulk dispensing and deposit-return glass systems. Industrial goods at 10% continue to benefit from well-established reusable IBCs, drums, and pallets where economic efficiency outweighs marketing considerations. Pharmaceuticals, though holding only 5%, demonstrate highly cautious adoption due to stringent sterility rules, with limited scope in secondary logistics packaging. The distribution of market share illustrates how refillable packaging thrives first in low-risk, high-volume consumer categories before scaling to more regulated or complex applications.

Retail Dominates Market Share by End-Use in the Refillable Packaging Industry

Retail channels hold the largest share at 50%, highlighting their position as the central hub for refillable packaging systems. Supermarkets, hypermarkets, and specialty retailers are increasingly deploying in-store refill stations for liquids and dry goods, alongside take-back schemes where branded durable containers are collected, sanitized, and refilled. This dominance is reinforced by retailers’ ability to control infrastructure, consumer education, and reverse logistics, making them the natural leaders in scaling circular economy models. E-commerce follows at 25%, gaining traction through subscription-based closed-loop systems where durable delivery totes and refill packs are returned with the next shipment. However, the economics of reverse logistics limit penetration largely to dense urban environments and recurring-use categories. Industrial users account for 15%, leveraging refillables in long-established B2B supply chains for pooled assets such as pallets, cages, and IBCs, driven purely by operational savings and asset reusability. Food service contributes 7%, with glass bottle deposit systems and reusable cup initiatives expanding under municipal single-use reduction mandates. Healthcare remains niche at 3%, confined to durable secondary packaging and sterilizable logistics containers where compliance and sterility are paramount. The leadership of retail demonstrates how consumer-facing infrastructure integration is shaping the refillable packaging ecosystem, while e-commerce and B2B supply chains represent the next frontiers of expansion.

European Union: PPWR and National Reuse Obligations Accelerating Refillable Packaging Growth

The European Union is taking a leadership role in shaping the refillable packaging market through its Packaging and Packaging Waste Regulation (PPWR), which came into effect in February 2025. This regulation compels companies to offer a fixed percentage of products in refillable or reusable packaging, with particular emphasis on takeaway food and beverage formats. By 2030, all packaging must achieve at least 70% recyclability (Grade C), advancing to 95% (Grade A) by 2038, ensuring compatibility with the EU’s circular economy goals. In addition, the ban on single-use plastic packaging for fresh fruits and vegetables under 1.5 kg by 2030 underscores the bloc’s commitment to drastically reducing disposable plastics.

Germany has been an early mover, introducing its “reusable packaging obligation” in January 2023, requiring catering outlets to offer reusable alternatives to disposable takeaway containers at the same price point. Alongside this, the EU is pushing for Deposit Return Systems (DRS) to improve collection and reduce littering, with pilot initiatives like “Mehrweg Modell Stadt” establishing city-wide reusable take-back systems. Furthermore, the Ecodesign for Sustainable Products Regulation (ESPR) launched in 2024 introduces a Digital Product Passport, which will mandate transparency on product origin and compliance, creating traceable accountability in refillable systems. These combined regulatory and industry-led measures are transforming the EU into one of the fastest-growing refillable packaging markets globally.

United States: State-Level EPR and Federal Investments Reshaping Refillable Packaging

In the United States, the refillable packaging market is expanding under the dual influence of federal environmental initiatives and state-level Extended Producer Responsibility (EPR) laws. The U.S. Environmental Protection Agency (EPA) and the U.S. Plastics Pact are at the forefront of steering packaging systems toward a circular economy. Seven states, including Maryland, have enacted EPR laws, with Maryland’s framework mandating that Producer Responsibility Organizations (PROs) fund at least 90% of packaging waste management costs by 2030. This legislative momentum is encouraging brand owners to explore refillable and reusable solutions as a compliance mechanism while reducing their reliance on virgin plastic.

The U.S. market is also being propelled by innovations in mono-material packaging and lightweight paper-based alternatives that simplify recycling and align with refill models. Federal support through the Infrastructure Investment and Jobs Act is fueling the construction of advanced recycling and local packaging facilities, creating a strong backbone for refill and reuse. A growing trend in the U.S. is the shift toward innovative refill formats for groceries, beverages, and personal care, with companies partnering under the U.S. Plastics Pact to meet national sustainability targets. Collectively, these initiatives position the U.S. as a major growth hub for refillable packaging, particularly across fresh produce, household goods, and e-commerce-driven retail.

China: Regulatory Push and Logistics Sector Driving Reusable Systems

China is rapidly scaling its refillable packaging market, with new regulations that came into effect on June 1, 2025, mandating eco-friendly, reduced, and reusable packaging for express delivery companies. This policy is significant given the country’s booming e-commerce and logistics sectors, where companies like JDL Express and SF Express are now deploying reusable circulation boxes to replace single-use cardboard, cutting waste in high-volume operations.

Governmental bodies such as the National Development and Reform Commission (NDRC) and the Ministry of Ecology and Environment (MEE) are reinforcing these initiatives through the 14th Five-Year Plan, which prioritizes plastic pollution reduction and resource efficiency. On-the-ground innovation includes community-led reuse models, such as Zhejiang University’s packaging reuse program, where students leave boxes at collection stations for redistribution. Local manufacturers are also leveraging automation and scalable production to supply reusable packaging materials for retail and logistics. These efforts, coupled with China’s industrial upgrading agenda, are positioning the country as a dominant player in scalable refillable packaging solutions.

India: EPR Compliance and Bioplastic Innovation Supporting Refillable Packaging

In India, the Plastic Waste Management (Amendment) Rules, 2024 serve as the cornerstone of the refillable packaging market, with an emphasis on Extended Producer Responsibility (EPR). While MSMEs are exempt from EPR obligations, the burden falls on manufacturers and importers, pushing them to integrate reusable and refillable models. Starting in July 2025, all plastic packaging must be traceable via QR codes, barcodes, or unique identifiers, improving accountability in waste management.

The market is witnessing strong innovation in bioplastic packaging derived from agricultural and dairy waste, with patents for biodegradable materials such as ghee residue-based bioplastic. This complements the rising use of refill stations and reusable formats in food, beverages, and household products. The country’s growing processed food sector and organized retail formats are particularly driving adoption. By coupling regulatory enforcement with innovation-led refillable alternatives, India is emerging as a key growth market for refillable packaging in Asia.

Japan: Circular Economy Targets and Cosmetics Industry Leadership in Refillable Packaging

Japan’s Plastic Resource Circulation Strategy is a pivotal driver of the refillable packaging market, requiring that by 2025 all plastic packaging be reusable or recyclable. Furthermore, the strategy mandates that renewable material use must double by 2030, supported by strict waste sorting regulations to ensure collection efficiency.

The country’s cosmetics and personal care industry is leading innovation, with companies like Shiseido and Tokiwa Cosmetics rolling out refillable formats for skincare and beauty products such as creams, serums, and foundations. This sector is complemented by breakthroughs in paper-based barrier packaging from firms like Nippon Paper Industries, which developed SHIELDPLUS, a recyclable paper resistant to oxygen and odors. Japan is also advancing the use of bio-polypropylene (bio-PP), with companies like LyondellBasell and Shiseido integrating bio-based solutions into refill packaging. These combined efforts are reinforcing Japan’s position as a global leader in refillable and reusable packaging innovations, particularly in premium consumer markets.

Brazil: Reverse Logistics and Policy Enforcement Strengthening Refillable Packaging Adoption

In Brazil, the National Solid Waste Policy (PNRS) is the backbone of the refillable packaging market, mandating strong accountability for waste disposal, recycling, and reuse. The country’s reverse logistics system requires producers to handle post-consumer collection and recycling, encouraging packaging companies to invest in refill-ready designs and infrastructure.

Law enforcement and government initiatives are aiming to curb solid waste generation, with policies pushing both reuse and recycling practices. The food and retail industries in Brazil are increasingly adopting refillable formats and multi-use trays, often designed with Modified Atmosphere Packaging (MAP) or vacuum sealing to extend freshness. These sustainable approaches are gaining traction not only in domestic retail but also in export-sensitive sectors, where global trade partners are demanding adherence to stricter sustainability standards. By combining policy-driven accountability with industry-led innovations, Brazil is strengthening its role as a major market for refillable packaging in Latin America.

Refillable Packaging Market Report Scope

Refillable Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$46.3 Billion

|

|

Market Size (2034)

|

$73.7 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Material (Plastic, Glass, Metal, Paper & Paperboard), By Application (Food & Beverages, Personal Care & Cosmetics, Homecare, Pharmaceuticals, Industrial Goods), By End-Use Industry (E-commerce, Retail, Food Service, Industrial, Healthcare)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, DS Smith Plc, Smurfit Kappa Group Plc, Graphic Packaging Holding Company, Sonoco Products Company, Huhtamaki Oyj, International Paper Co., WestRock Company, ProAmpac, Berry Global, Inc., Greif, Inc., Silgan Holdings Inc., Pactiv Evergreen Inc., PAPACKS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Refillable Packaging Market Segmentation

By Material

- Plastic

- Glass

- Metal

- Paper & Paperboard

By Application

- Food & Beverages

- Personal Care & Cosmetics

- Homecare

- Pharmaceuticals

- Industrial Goods

By End-Use Industry

- E-commerce

- Retail

- Food Service

- Industrial

- Healthcare

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Refillable Packaging Market

- Amcor plc

- Mondi Group

- DS Smith Plc

- Smurfit Kappa Group Plc

- Graphic Packaging Holding Company

- Sonoco Products Company

- Huhtamaki Oyj

- International Paper Co.

- WestRock Company

- ProAmpac

- Berry Global, Inc.

- Greif, Inc.

- Silgan Holdings Inc.

- Pactiv Evergreen Inc.

- PAPACKS

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and multi-faceted research methodology to develop its market insights on the global refillable packaging industry. Our approach combines quantitative and qualitative analyses, incorporating historical data, industry trends, regulatory frameworks, and technological advancements to forecast market growth accurately from 2025 to 2034. We leverage primary research through interviews with key stakeholders, including packaging manufacturers, CPG brands, and logistics providers, complemented by secondary research from company reports, government publications, and credible industry databases. Advanced data modeling techniques, including CAGR projections, supply-demand gap analysis, and segmentation by material, application, and end-use industry, allow us to identify market opportunities and competitive dynamics. USDAnalytics also evaluates regional regulatory impacts, such as EPR mandates, deposit-return systems, and EU PPWR compliance, as well as technological enablers like smart IoT-enabled containers and interoperable refill platforms. This robust methodology ensures that our market intelligence delivers actionable insights for industry professionals, investors, and corporate strategists aiming to capitalize on sustainability-driven growth in refillable packaging.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.