Bag-in-Box Container Market Overview: Lightweighting, Sustainability, and Liquid Packaging Drive Growth

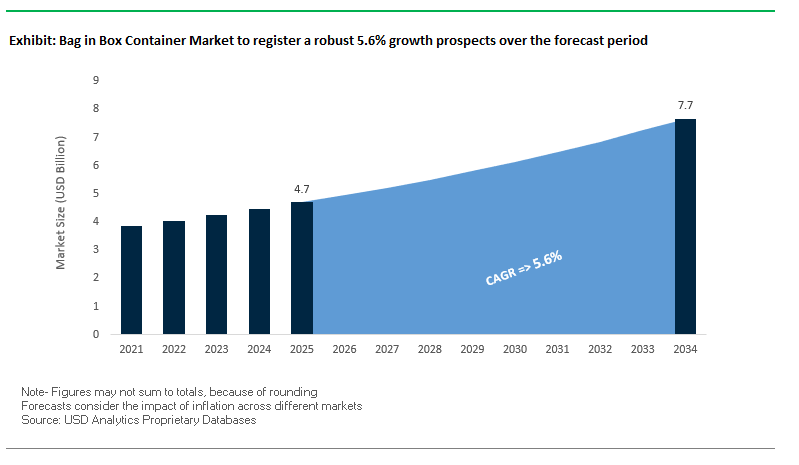

The Global Bag-in-Box (BIB) Container Market is projected to expand from $4.7 billion in 2025 to $7.7 billion by 2034, growing at a CAGR of 5.6%. This growth reflects the format’s unmatched advantages in sustainability, logistics efficiency, and product shelf life extension, making it a preferred choice for wine, juice, dairy, edible oils, and industrial liquids. Industry professionals and buyers must track innovations in recyclable films, dispensing taps, and paper-based secondary packaging, as brands intensify efforts to align with consumer expectations and global sustainability mandates.

Key Insights shaping market priorities:

- Lightweight sustainability: A 10-liter BIB weighs ~90% less than glass equivalents, cutting both costs and CO₂ emissions.

- Shelf-life advantage: Airtight bags and taps extend opened product life to 8 weeks, reducing food waste significantly.

- Logistics efficiency: Flat-packed containers enable 7.4x more empty units per truck compared to glass, lowering freight costs.

- Liquid segment dominance: Food and beverages remain the largest share, led by wine and juice, but growth opportunities are expanding in water, dairy, and edible oils.

Market Analysis: Strategic Investments, Mergers, and Sustainable Innovations

The BIB packaging sector has seen major investments, acquisitions, and innovations over the past two years as companies align with stricter regulations and sustainability goals. In February 2025, Smurfit Kappa invested €54 million in Alicante, Spain, to double plant capacity and enhance energy efficiency, reinforcing its leadership in European BIB systems. In January 2025, the Smurfit Kappa–WestRock merger created Smurfit WestRock, a global paper-based packaging giant now scaling its BIB capabilities. This was followed in August 2025 by the launch of a fully recyclable all-paper stretch wrap for pallets, extending the company’s circular packaging portfolio.

Meanwhile, suppliers are focusing on material substitution to eliminate non-recyclables. In November 2024, Smurfit Kappa developed a recyclable polyethylene film to replace nylon in U.S. BIB products, while Amcor (October 2024) launched a recyclable connector for Walmart’s BIB lines, showcasing the move toward end-to-end recyclability. On the M&A front, Sealed Air’s February 2024 acquisition of Liquibox significantly expanded its footprint in liquid packaging, giving it access to advanced BIB dispensing technology and pouches. Similarly, DS Smith’s integration with International Paper (January 2025) has created a global fiber-packaging leader with a substantial BIB portfolio.

Key Trends and High-Impact Opportunities Driving the Bag-in-Box Container Market

Expansion Beyond Wine into Commercial and Industrial Liquid Packaging

The bag-in-box container market is rapidly expanding beyond its traditional association with wine, driven by increasing adoption in commercial, industrial, and foodservice applications. Efficiency and cost savings are key drivers: U.S. FDA case studies highlight that dispensing syrups for soft drink fountains via bag-in-box technology reduces both transportation and handling costs compared to traditional bottles. The lightweight, stackable design allows for optimized pallet space and lower shipping weight, while maintaining product integrity. Foodservice adoption is accelerating, with major brands like PepsiCo and Coca-Cola using bag-in-box for fountain beverages, sauces, concentrated juices, and liquid eggs, ensuring freshness and minimizing waste. Industrial applications are also gaining traction, with the format being used for lubricants, chemical reagents, and other bulk liquids. UN certification for transporting dangerous goods further supports the shift, making bag-in-box containers an increasingly versatile solution across industries.

Integration of Advanced Barrier Films and Aseptic Technology for Premium Products

The integration of advanced barrier films and aseptic filling technology is transforming bag-in-box packaging for oxygen-sensitive and high-value liquids. Aseptic filling allows for sterile packaging, extending shelf life without preservatives and enabling storage at room temperature for up to a year, ideal for products such as fruit juice concentrates, purees, plant-based milk, and liquid eggs. Advanced films, like Mondi Group’s EVOH-based barrier films, provide exceptional protection against oxygen, gas, and light, preserving product quality. This combination of technology and high-barrier materials is driving market expansion into premium segments, including high-end wines and craft beverages, allowing bag-in-box packaging to compete effectively with glass and other rigid formats while offering superior convenience, sustainability, and safety.

Development of Monomaterial or Easily Recyclable Film Structures

A critical opportunity in the bag-in-box market lies in developing recyclable, monomaterial film structures that maintain high barrier performance. Traditional multi-material laminates present recycling challenges, making sustainable monomaterial solutions a priority. Companies like Mondi and LD PACK are pioneering all-polyethylene bag-in-box films that comply with CEFLEX circular economy guidelines. Technical innovations in bio-based and advanced polymer coatings allow single-polymer films to achieve barrier properties comparable to multi-layer laminates, protecting oxygen-sensitive liquids. Growing consumer demand and brand commitments to recyclable packaging further reinforce this opportunity, positioning manufacturers to gain a competitive edge while aligning with evolving sustainability regulations.

Proliferation of Integrated Smart Dispensing and Inventory Management Systems

The convergence of bag-in-box technology with IoT-enabled smart dispensing systems represents a transformative opportunity for commercial and industrial users. Integrated sensors track real-time product volume, flow rates, and consumption patterns, enabling automated reordering and inventory management. IoT-enabled systems reduce manual inventory checks, minimize human error, and streamline supply chain operations, freeing resources for strategic activities. Beyond inventory control, predictive analytics from smart dispensers provide insights into usage trends, optimize product mix, manage peak demand, and forecast future requirements accurately. This technology-driven approach enhances operational efficiency, reduces waste, and adds value to the bag-in-box format as a high-tech, data-enabled packaging solution.

Competitive Landscape: Strategic Directions of Global Bag-in-Box Leaders

The global BIB container market is shaped by five key players whose strategies span sustainability, integration, and product innovation.

Smurfit WestRock scaling fiber-based innovation for bag-in-box

Smurfit WestRock leverages its integrated supply chain from forestry to converting to dominate the BIB segment in wine, juice, and dairy. Its Lx recyclable polyethylene film (November 2024) replaces nylon in U.S. formats, while a €54 million investment (February 2025) in Spain doubled capacity for sustainable BIB production. With vertical integration and global scale, the company is positioned as a sustainability leader driving recyclable, lightweight packaging formats across food and beverage markets.

International Paper + DS Smith building a fiber-based packaging giant

The January 2025 merger of International Paper and DS Smith created one of the largest global suppliers of circular packaging. DS Smith’s bag-in-box systems (with dispensing taps and corrugated outer boxes) are core to its European leadership. With Europe’s largest paper recycling network, the combined company’s competitive edge lies in its closed-loop design, ensuring materials are recovered, reused, and reintroduced into the supply chain.

Sealed Air Corporation strengthened by Liquibox acquisition

Following its February 2024 acquisition of Liquibox, Sealed Air expanded into BIB containers, spouted pouches, and dispensing systems. The acquisition enhanced its offering to beverage, foodservice, and industrial fluid customers. Sealed Air now integrates smart dispensing technologies with its protective packaging expertise, positioning itself as a player that improves both supply chain efficiency and waste reduction in the liquid packaging space.

Scholle IPN (part of SIG) expertise in aseptic filling and shelf-life solutions

Acquired by SIG in 2022, Scholle IPN remains a leading innovator in bag-in-box and spouted pouch systems. Its core strength lies in aseptic filling technology, which extends shelf life without refrigeration critical for global wine, juice, and dairy shipments. The company’s integrated dispensing solutions are designed to reduce oxygen exposure and product loss, enabling both sustainability and extended product usability.

Sonoco Products Company cold chain and diversified packaging strength

Sonoco continues to diversify, with capabilities across rigid paper containers, flexibles, and temperature-assured packaging. While not a pure-play BIB specialist, Sonoco integrates engineered design, testing, and validation services through its ISC Labs®, supporting customized solutions for customers. Its expertise in cold chain logistics and safe liquid transport ensures a niche but strategic role in the global BIB market.

Bag in Box Container Market Share Insights

Bags Command Market Share by Product Type in Bag-in-Box Container Industry

Within the bag-in-box (BiB) container industry, the bag component represents 50% of total market share, reflecting its role as the technological and functional core of the system. Engineered from co-extruded, multi-layer barrier films often incorporating EVOH or metallized layers the bag ensures oxygen and moisture protection, directly determining product shelf life and safety. This is particularly critical for sensitive applications such as dairy, edible oils, and liquid eggs, where product spoilage risks are high. Innovation in bag design, such as recyclable mono-material barriers and improved puncture resistance, is accelerating adoption in both foodservice and consumer-facing markets. While outer cartons and fitments provide structural and dispensing functions, it is the barrier-engineered bag that anchors the industry’s value proposition and explains its dominant share.

Liquid Food Retains the Largest Market Share by Application in Bag-in-Box Container Industry

The liquid food sector, representing 35% of bag-in-box packaging demand, is the industry’s volume driver, fueled by the efficiency needs of foodservice and bulk supply chains. BiB formats have replaced metal cans and rigid pails in applications such as sauces, dairy, syrups, and liquid eggs, offering superior sanitary handling, reduced spoilage, and lower storage costs. Their ability to minimize oxygen exposure during dispensing not only extends product usability but also aligns with sustainability goals by cutting down on food waste. The format’s lightweight profile and compatibility with hygienic dispensing systems make it indispensable in institutional kitchens, catering services, and industrial food preparation environments. As global foodservice demand scales, BiB remains the most efficient packaging solution for liquid food distribution, reinforcing its market leadership.

United States: Regulatory Pressures and Sustainable Innovations Driving Bag-in-Box Container Adoption

The U.S. bag-in-box container market is being shaped by a combination of stringent regulations, sustainability trends, and technological advancements. States like California are enforcing regulations such as the Plastic Pollution Prevention and Packaging Producer Responsibility Act (SB 54), driving manufacturers to adopt recyclable and reusable bag-in-box solutions. Sustainability remains a central focus, with companies like Smurfit Kappa developing recyclable nylon-like films for bag-in-box products, particularly in the food and beverage sectors.

Technological innovations, including advanced barrier films and multilayer laminations, are enhancing protection against oxygen and light, extending the shelf life of sensitive products like wine and liquid foods. Corporate initiatives, such as LIQUI MOLY’s adoption of bag-in-box packaging for motor oils, highlight benefits like reduced plastic content and improved storage efficiency. The U.S. market is also seeing a preference for bulk packaging in foodservice and institutional sectors, and infrastructure investments, such as WestRock’s new corrugated box plant in Pleasant Prairie, Wisconsin, are expanding production capacity to meet growing regional demand.

Germany: Circular Economy and Regulatory Compliance Driving Eco-Friendly Bag-in-Box Packaging

Germany’s bag-in-box container market is strongly influenced by a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025. This legislation promotes eco-friendly and highly recyclable packaging, creating robust demand for paperboard-based bag-in-box solutions. Germany’s leadership in the circular economy ensures that producers are accountable for the entire packaging lifecycle, which drives innovation in recyclable materials and fiber-based alternatives.

Technological advancements focus on meeting minimum recycled content targets and improving material efficiency. Regulatory updates favoring paper-based packaging over plastics have accelerated adoption in the bag-in-box sector. The market is also witnessing consolidation, exemplified by Aran Group’s acquisition of a majority stake in IBA Germany in February 2024, strengthening its presence and showcasing strategic growth within the German bag-in-box market.

China: Green Transformation and E-Commerce Expansion Accelerate Bag-in-Box Market

China’s bag-in-box container industry is benefiting from government initiatives under the “dual carbon” goal, promoting the use of eco-friendly and reusable packaging materials. Policies restricting non-degradable plastics by the end of 2025 are driving demand for paperboard components in bag-in-box containers. The integration of automation, AI, and 5G-enabled industrial internet technologies is enhancing production efficiency and flexibility for manufacturers.

The expansion of domestic e-commerce platforms is a critical growth driver, increasing demand for secure, lightweight, and tamper-proof bag-in-box packaging. Industry innovations, supported by regulatory reforms under China’s “Made in China 2025” initiative, are fostering the development of high-tech manufacturing capabilities, aiming to raise the domestic content of core materials to 70% and strengthen the sustainability and competitiveness of China’s bag-in-box market.

India: Government Initiatives and Beverage Industry Demand Boost Bag-in-Box Adoption

India’s bag-in-box container market is gaining momentum through government programs such as “Make in India” and “Zero Effect Zero Defect”, which support high-quality domestic production. The Production Linked Incentive (PLI) Scheme, with an outlay of INR 10,900 crore, promotes standardized and high-quality packaging solutions, benefiting the food and beverage sectors.

Regulatory policies, including the Plastic Waste Management (Amendment) Rules, are accelerating the adoption of eco-friendly alternatives, while rising disposable income and urbanization are shifting consumer preferences toward convenient, single-serve, and ready-to-use packaging. The market is particularly driven by beverage and dairy industries, which require efficient, cost-effective, and shelf-stable bag-in-box solutions. These trends, coupled with increasing infrastructure investments, are creating a robust growth environment for India’s bag-in-box container market.

Bag in Box Container Market Report Scope

Bag in Box Container Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.7 Billion

|

|

Market Size (2034)

|

$7.7 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Material Type (Liner, Outer Box), By Product Type (Bags, Fitments, Outer Boxes), By Capacity (Less than 5 Liters, 5–10 Liters, 10–20 Liters, More than 20 Liters), By End-Use Industry (Food & Beverages, Household & Industrial, Chemicals, Other End-Use Industries), By Application (Liquid Food, Alcoholic Beverages, Non-Alcoholic Beverages, Liquid Detergents, Industrial Chemicals)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Smurfit Kappa Group plc, Amcor plc, DS Smith plc, Mondi Group, Liquibox Corporation, Scholle IPN, CDF Corporation Inc., WestRock Company, Rapak, Aran Group, Great Northern Packaging, Encore Container, LLC, Vine Valley Group, TPS Rental Systems, Greif, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bag in Box Container Market Segmentation

By Material Type

By Product Type

- Bags

- Fitments

- Outer Boxes

By Capacity

- Less than 5 Liters

- 5–10 Liters

- 10–20 Liters

- More than 20 Liters

By End-Use Industry

- Food & Beverages

- Household & Industrial

- Chemicals

- Other End-Use Industries

By Application

- Liquid Food

- Alcoholic Beverages

- Non-Alcoholic Beverages

- Liquid Detergents

- Industrial Chemicals

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Bag in Box Container Market

- Smurfit Kappa Group plc

- Amcor plc

- DS Smith plc

- Mondi Group

- Liquibox Corporation

- Scholle IPN

- CDF Corporation Inc.

- WestRock Company

- Rapak

- Aran Group

- Great Northern Packaging

- Encore Container, LLC

- Vine Valley Group

- TPS Rental Systems

- Greif, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employed a rigorous, multi-faceted research methodology to deliver a comprehensive analysis of the global Bag-in-Box (BIB) Container Market. The study combined primary research, including interviews with packaging manufacturers, brand owners, foodservice operators, and industry experts, with secondary research from corporate reports, regulatory publications, and market announcements. Market sizing and growth forecasts were determined using historical trends, technological innovations, sustainability initiatives, regulatory frameworks, and evolving consumer preferences. Segmentation was analyzed by material type, product type, capacity, end-use industry, and application, while regional insights focused on major markets such as the U.S., Germany, China, and India. Competitive intelligence evaluated strategies, mergers, acquisitions, and innovations of leading players including Smurfit Kappa, Amcor, DS Smith, Mondi Group, and Liquibox, highlighting advancements in recyclable films, aseptic filling, lightweight packaging, and smart dispensing systems. By integrating insights on circular economy initiatives, logistics efficiency, high-barrier packaging, and automation-driven adoption, USDAnalytics provides industry professionals with actionable intelligence to guide investment, operational, and sustainability decisions in the BIB container market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.