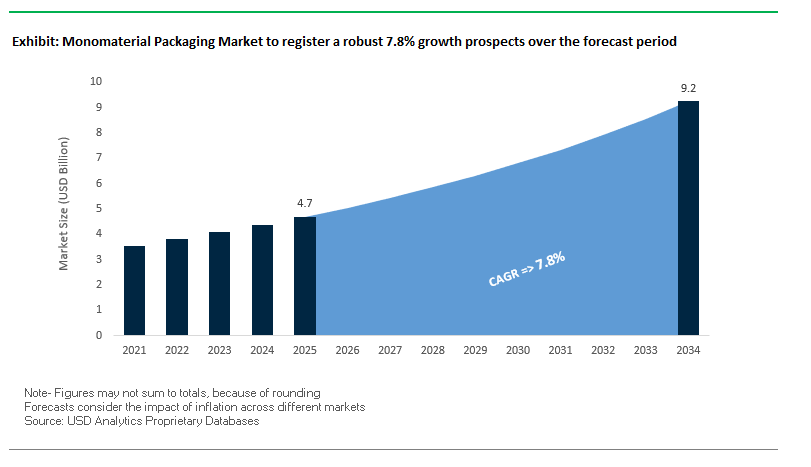

Monomaterial Packaging Market to Reach $9.2 Billion by 2034 at 7.8% CAGR

The global monomaterial packaging market is expected to grow from $4.7 billion in 2025 to $9.2 billion by 2034, registering a CAGR of 7.8%. This expansion is fueled by rising adoption of single-polymer packaging solutions, regulatory pressures for recyclability, and advances in high-barrier monomaterial films. Monomaterial packaging, typically made from polyethylene (PE) or polypropylene (PP), simplifies recycling streams, improves environmental sustainability, and enables brands to meet circular economy targets.

Key Insights for Industry Stakeholders

- Recyclability and simplification: Monomaterial designs eliminate multilayer separation, enhancing sorting efficiency and cleaner recycling streams.

- Circular economy alignment: Transition from multi-layer laminates supports sustainability pledges and company goals for recyclable or reusable packaging by 2025.

- High-performance material innovation: Modern PE and PP films provide barrier properties equivalent or superior to traditional laminates, protecting against oxygen, moisture, and light.

- Recycled polymer integration: Post-consumer recycled (PCR) content in monomaterial films creates closed-loop systems, reducing reliance on virgin plastics.

- Cross-industry applicability: Widely used across food, beverage, pharmaceuticals, and e-commerce packaging, offering versatility in high-volume and premium applications.

Recent Developments Driving Monomaterial Packaging Innovation

The monomaterial packaging industry is witnessing significant innovation, partnerships, and mergers that reflect its sustainability and performance-driven growth. In September 2025, Mondi launched a patented PE-based mono-material pouch with removable panels for liquid detergents and soaps, certified 100% recyclable, positioning it as the most recyclable spouted pouch in the market. In August 2025, ProAmpac acquired PAC Worldwide, expanding its global footprint and accelerating monomaterial innovations across e-commerce, consumer packaged goods, and industrial markets. The same month, Graphic Packaging International introduced the PaperSeal® Pressed MAP Tray, reducing plastic usage by up to 85%, emphasizing sustainable alternatives in food packaging.

Strategic mergers also shaped the market structure. In July 2025, WestRock and Smurfit Kappa debuted as Smurfit WestRock on the New York and London Stock Exchanges, consolidating capabilities to better serve the monomaterial packaging sector. Innovations in product design continued with Amcor and Cofigeo in June 2025, introducing a PP-based ready meal tray adhering to Design for Recycling (DfR) principles, featuring near-infrared (NIR) detectable masterbatch for efficient sorting. The same month, Mondi and Saga Nutrition launched sustainable monomaterial pet food solutions, further reinforcing eco-friendly packaging adoption.

Earlier, in May 2025, Mondi commissioned a €400 million paper machine at its Štětí mill, strengthening production capacity for sustainable solutions, while in January 2025, Cirkla introduced molded fiber MAP trays, reducing plastic usage by 85%, demonstrating a strong market shift toward high-performance, recyclable packaging alternatives.

Trends and Opportunities Reshaping the Monomaterial Packaging Market

Legislative Mandates Driving Forced Adoption Across Consumer Goods

The monomaterial packaging market is entering a compliance-driven era where regulatory mandates are replacing voluntary sustainability initiatives. Governments worldwide are using Extended Producer Responsibility (EPR) laws and plastic taxes to create hard deadlines for packaging redesign. The European Union’s Packaging and Packaging Waste Regulation (PPWR), which came into force in February 2025, is a central catalyst. It mandates that by 2030, all plastic packaging must contain minimum levels of post-consumer recycled (PCR) content—30% for beverage bottles and 35% for other plastics excluding contact-sensitive PET.

These mandates directly incentivize the shift to monomaterial structures because they generate higher-quality recyclates that can reliably meet PCR content targets. Additionally, the design-for-recycling requirement, which compels all packaging to achieve a recyclability score of at least 70%, makes complex multi-material laminates non-compliant. The financial pressure is reinforced by eco-modulated EPR fees, where producers face higher costs for difficult-to-recycle packaging. For instance, a U.K. policy statement confirms that producers pay lower fees for recyclable formats and higher fees for problematic designs, ensuring that economics favor monomaterial packaging adoption.

This regulatory momentum is echoed beyond Europe. Countries across North America and Asia are introducing plastic taxes and EPR schemes that make non-recyclable formats financially unviable. As a result, brand owners across food, beverage, personal care, and household goods are accelerating transitions to monomaterials to ensure both compliance and cost competitiveness.

Breakthroughs in High-Barrier Monomaterial Polymer Development

While regulatory push is clear, the technological pull is equally strong. Historically, one of the biggest barriers to monomaterial adoption has been achieving the oxygen, moisture, and aroma resistance demanded by food and beverage applications. Recent breakthroughs in polymer science and coating technology are solving this challenge, creating new growth opportunities.

Innovations in polyethylene (PE) and polypropylene (PP) films have enhanced their barrier performance by as much as 30% compared to legacy multi-material structures, making them viable for applications like cheese, baked goods, and fresh produce. These new polymer grades also improve mechanical strength and clarity, reducing the need for multiple layers. Complementing polymer advancements, functional coatings—often water-based or solvent-free—are being developed to deliver barrier protection without compromising recyclability. Unlike traditional EVOH or PVDC layers, these coatings ensure that the entire structure remains compatible with existing recycling streams.

Together, these innovations are enabling the packaging industry to balance regulatory compliance, product protection, and consumer appeal in a monomaterial format, bridging the gap between sustainability and functionality.

Development of Bio-Based and Marine-Degradable Monomaterials for Flexible Applications

The global packaging industry is also seeing an opportunity beyond recyclability—bio-based and marine-degradable monomaterials for low-recycling-rate applications. A large proportion of flexible packaging, such as snack bar wraps and condiment sachets, escapes formal recycling systems and often ends up in the environment. Developing materials from polylactic acid (PLA) and polyhydroxyalkanoates (PHA) offers a sustainable end-of-life pathway by ensuring biodegradability in marine environments.

Studies highlight that PHA-based films degrade naturally in seawater, providing a viable solution for leakage-prone packaging categories. This innovation directly addresses public and regulatory concerns about ocean plastic pollution. With growing demand from FMCG brands seeking plastic-free and compostable solutions, suppliers of marine-degradable monomaterials stand to benefit from strong market traction. This segment also aligns with consumer expectations for environmentally safe packaging that supports zero-waste and plastic-neutral commitments.

Integration of Digital Watermarking for Precision Sorting at Scale

Another transformative opportunity lies in digital watermarking technology, pioneered by initiatives like HolyGrail 2.0. This system embeds invisible codes into monomaterial packaging, which can be detected by high-resolution cameras during sorting. When combined with near-infrared (NIR) technology, these codes enable sorting accuracies of up to 99% and ejection efficiencies of 95%, as proven in large-scale industrial trials conducted across Europe between 2023 and 2024.

Digital watermarking goes beyond sorting by allowing packaging to carry detailed metadata, such as polymer type, brand, and food vs. non-food use, enabling the creation of high-purity PCR feedstock. This is particularly critical for food-grade plastics, where safety regulations demand extremely high purity levels. Beyond recycling efficiency, digital watermarks open the door for consumer engagement—packaging could double as a scannable interface for sustainability information, authenticity checks, or brand storytelling.

Competitive Landscape of Global Monomaterial Packaging Market

The monomaterial packaging industry is competitive, with top players leveraging innovation, sustainability, and high-barrier performance to differentiate themselves. Leading companies focus on PE and PP-based packaging, advanced recycling-friendly solutions, and partnerships that enhance global reach and technological capabilities.

Amcor plc: Global Leader in Sustainable Monomaterial Packaging

Amcor specializes in flexible and rigid monomaterial packaging, including high-performance films, trays, and pouches made from single polymers such as PE and PP. In June 2025, Amcor partnered with Cofigeo to develop a PP-based ready meal tray, aligning with its 2025 goal of fully recyclable or reusable packaging. Through its Catalyst™ program, Amcor collaborates with brands like Nestlé to create tailored sustainable solutions, providing a competitive advantage over paper-based alternatives. Key offerings include all-PP pouches and trays that deliver superior barrier protection while remaining fully recyclable.

Mondi Group: Innovating High-Barrier Monomaterial Films

Mondi is a global packaging and paper leader, with a strong focus on monomaterial barrier films designed for recyclability. In September 2025, the company launched a patented mono-material pouch for liquid detergents with removable panels, certified 100% recyclable. Mondi emphasizes value-accretive growth with sustainability, offering products like BarrierPack Recyclable (95% recyclable) and re/cycle WalletPack (93% recyclable) that cater to food, pharmaceuticals, and consumer goods while supporting circular economy principles.

Sealed Air Corporation: High-Barrier Recyclable Solutions for Food Safety

Sealed Air provides protective and food packaging solutions, including high-barrier films and trays designed to extend shelf life while being fully recyclable. Its expertise in materials science enables innovative monomaterial packaging that supports circular economy goals. The CRYOVAC® brand includes recyclable-ready bags and films used in fresh red meat, pet food, and processed meat applications, balancing food safety and sustainability.

Berry Global Inc.: Sustainable Rigid and Flexible Monomaterials

Berry Global manufactures innovative monomaterial packaging, including rigid containers, films, and trays. In October 2023, the company launched a refillable deodorant stick constructed entirely from monomaterial, demonstrating sustainability and recycled plastic integration. Berry focuses on CleanStream® PCR polypropylene for FDA-approved food-contact applications, underlining its commitment to eco-friendly, high-performance packaging.

ProAmpac: Flexible Monomaterial Solutions for E-commerce and CPG

ProAmpac specializes in flexible monomaterial packaging, including its ProActive Recyclable film series, designed to replace hard-to-recycle laminated structures. In August 2025, ProAmpac acquired PAC Worldwide, enhancing its global reach and innovation capabilities. The company’s ProActive Sustainability® program focuses on delivering recyclable films and fiber-based solutions for food, healthcare, and retail markets, aligning performance with circular economy goals.

Monomaterial Packaging Market Share Insights

Pouches Lead Market Share by Packaging Type in the Monomaterial Packaging Industry

Pouches command the largest share at 30% in 2025, establishing themselves as the dominant packaging format in the global monomaterial packaging market. Their rapid adoption stems from the food and beverage industry’s urgent need to replace multi-layer, non-recyclable flexible structures with recyclable mono-PE and mono-PP stand-up pouches. These pouches offer lightweighting advantages, extended shelf-life with high-barrier coatings, and compatibility with high-speed filling lines. Films follow with 25% share, largely because of their role as shrink films, lidding films, and stretch wraps that are directly targeted by EPR regulations and single-use plastic bans. Bottles secure 20% share, a stable segment underpinned by the well-established recyclability of PET and HDPE beverage containers, with innovation focused on rPET and rHDPE integration. Trays and containers, with 15% share, are growing steadily in ready-meal and dairy packaging, while bags (8%) remain entrenched in retail and household use despite competition from paper alternatives. Specialized formats like tubes make up the remaining 2%, reflecting the more complex shift in technical applications where barrier requirements remain high.

Food & Beverage Dominates Market Share by End-Use Industry in the Monomaterial Packaging Industry

The food and beverage sector accounts for 60% of global monomaterial packaging demand, underscoring its role as the epicenter of this industry shift. Regulatory and consumer pressure to eliminate multi-material laminates in snack pouches, frozen food bags, and beverage bottles has pushed F&B brands to accelerate adoption of recyclable mono-PE, mono-PP, and PET solutions. This dominance is reinforced by the retail sector’s push for sustainable private-label packaging and the rise of e-commerce grocery delivery, both of which require reliable yet recyclable protective packaging. Homecare and household products hold 18% share, leveraging mono-PE bottles and refill pouches as brands like Unilever and P&G position sustainability as a key marketing tool. Personal care and cosmetics secure 12% share, reflecting their transition to mono-material bottles, jars, and tubes, though progress is tempered by the need for aesthetics, pigments, and oxygen barriers. Pharmaceuticals and healthcare contribute 8%, focused on recyclable blister and bottle formats, while industrial and niche applications make up the remaining 2%, where performance remains a higher priority than recyclability.

United States: Extended Producer Responsibility Laws Drive Monomaterial Packaging Innovation

The U.S. monomaterial packaging market is being reshaped by the rapid expansion of Extended Producer Responsibility (EPR) legislation across states. California’s SB 54 and Maryland’s new EPR bill set ambitious recycling and source reduction targets, forcing packaging manufacturers to pivot toward nationwide recyclable monomaterial solutions. This regulatory complexity is fueling innovation in polyethylene (PE) and polypropylene (PP) monomaterial films, which now rival multi-layer laminates in terms of oxygen and moisture protection. A growing trend is the use of digital printing directly on monomaterial substrates, enabling brand customization without compromising recyclability.

Corporate investments are further strengthening this market shift. Berry Global Inc., for instance, launched a bio-based polyethylene monomaterial tray in February 2025, targeting food applications. Adoption is particularly strong in food and beverages, personal care, and pharmaceuticals, where monomaterial formats extend shelf life while meeting sustainability mandates. Healthcare companies are increasingly adopting sterile monomaterial packaging to meet recyclability targets. The U.S. market also benefits from the surge in e-commerce-ready packaging solutions, positioning monomaterials as a cornerstone of future-ready sustainable packaging.

Germany: EU Packaging Regulation Accelerates Adoption of High-Barrier Monomaterials

Germany’s monomaterial packaging industry is thriving under the stringent European Union Packaging and Packaging Waste Regulation (PPWR), which requires all packaging to be recyclable by 2030. This regulation, coupled with Germany’s strong circular economy infrastructure, places monomaterials at the center of sustainable packaging strategies. Technological leadership is evident in the development of ultra-thin, resource-efficient recyclable films, such as the mono-oriented MDO-PE films unveiled by SML in 2024, which offer strength and recyclability at just 15 microns.

The German market is also benefiting from significant corporate investments. Borealis is channeling over €100 million into a new polypropylene foam line in Burghausen, tripling production capacity to support lightweight and recyclable packaging formats. Applications extend across consumer goods, automotive, and construction, but the strongest growth lies in food and beverage packaging, where high-barrier monomaterials enable efficient recycling. Germany’s leadership in Industry 4.0 ensures digitalized and automated manufacturing processes that enhance efficiency, supporting its position as a global hub for advanced monomaterial packaging solutions.

China: Dual-Carbon Goals Propel Monomaterial Packaging Transformation

China’s monomaterial packaging market is being shaped by the government’s dual-carbon targets—carbon peaking by 2030 and neutrality by 2060—which have accelerated the push toward eco-friendly and recyclable materials. Policies encouraging circular economy principles are spurring the adoption of bio-based, recycled, and lightweight monomaterials. The government has also implemented stricter plastic waste laws, reinforcing demand for innovative, single-material solutions that can be easily recycled within growing domestic systems.

Chinese manufacturers are heavily investing in automation, AI, and “5G plus industrial internet” technologies to improve production efficiency, particularly for food packaging and e-commerce. Key applications include flexible pouches, shrink films, and high-volume packaging for consumer goods and electronics. A strong emphasis on domestic substitution ensures local companies are scaling up capacity to meet national demand while reducing reliance on imported packaging technologies. With China leading globally in textile and electronics production, its demand for recyclable monomaterial packaging is expected to accelerate significantly.

India: Policy-Backed Circular Economy Strengthens Monomaterial Packaging Growth

India’s monomaterial packaging industry is gaining momentum under government initiatives such as “Make in India” and the Production Linked Incentive (PLI) scheme, which promote domestic manufacturing and sustainability. Regulatory signals like the mandate for 30% recycled PET content in beverage bottles from 2025 reflect the broader national push toward circular economy practices. These policies create fertile ground for monomaterial adoption across packaging sectors.

Technological advancements are also reshaping India’s packaging market. Innovations like Koehler’s monomaterial paper with grease and oxygen barrier properties are enabling curbside recycling while meeting performance standards. Companies such as Uflex are pioneering sustainable film and laminate production, with heavy investments in R&D to support monomaterial adoption. Food and beverage remains the leading application segment, driven by supermarket and online retail expansion, while pharmaceutical and personal care packaging are emerging as high-growth areas. With India’s growing role as an export hub, demand for recyclable and eco-friendly monomaterial packaging is expected to surge internationally.

Japan: Nanotechnology and Premium Packaging Fuel Monomaterial Market Expansion

Japan’s monomaterial packaging market is strongly supported by sustainability-focused corporate strategies and government policies. The Plastic Resource Circulation Act provides clear regulatory guidance, while Industry-Government-Academia partnerships foster the development of recycled plastics and recyclable single-material solutions. Companies like TOPPAN are actively advancing monomaterial designs as part of their growth strategies, recognizing the ease of recycling compared to multi-material formats.

Technological innovations in Japan emphasize premium quality and functionality. Advances in coatings and finishes are enhancing the durability, shelf life, and visual appeal of monomaterial packaging without compromising recyclability. The country’s strong presence in food and beverage and electronics markets drives demand for high-quality, aesthetically refined packaging that supports brand identity. With corporate and academic collaborations accelerating progress in recyclable paperboard and plastics, Japan is setting benchmarks for functional and design-driven monomaterial packaging.

Brazil: Legal Reforms and Molded Pulp Innovation Redefine Sustainable Packaging

Brazil’s monomaterial packaging industry is being reshaped by legal reforms to its National Solid Waste Policy, including Law No. 15,088 (2025), which bans the import of most plastic waste while allowing only strategic, non-hazardous imports. These reforms strengthen local recycling systems and support the adoption of domestic sustainable packaging solutions. Decree No. 12,451 further reinforces life cycle responsibility across the supply chain, compelling stakeholders to adopt recyclable and compostable packaging formats.

Technological innovation is centered on molded pulp, which is gaining traction as a durable, printable, and compostable alternative to molded plastics. Adoption is rising in foodservice and consumer goods packaging, where renewable and protective solutions are in high demand. The pulp and paper industry, a traditional strength in Brazil, is at the forefront of this transition, driving the integration of monomaterial formats into mainstream packaging. With both government support and corporate investments aligning, Brazil is positioning itself as a Latin American leader in compostable monomaterial packaging solutions.

Monomaterial Packaging Market Report Scope

Monomaterial Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.7 Billion

|

|

Market Size (2034)

|

$9.2 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Material (PE, PP, PET, PLA, Paper & Paperboard, Others), By Packaging Type (Films, Pouches, Bags, Trays & Containers, Bottles, Others), By End-Use Industry (Food & Beverage, Pharmaceuticals & Healthcare, Personal Care & Cosmetics, Homecare & Household, Others), By Application (Dairy Products, Meat, Poultry & Seafood, Fresh Fruits & Vegetables, Bakery & Confectionery, Pet Food, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Berry Global Group, Inc., Huhtamaki Oyj, DS Smith Plc, Sealed Air Corporation, Constantia Flexibles, Uflex Limited, Rengo Co., Ltd., International Paper Company, WestRock Company, Sonoco Products Company, Graphic Packaging Holding Company, Sappi Limited, Greiner Packaging International GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Monomaterial Packaging Market Segmentation

By Material

- PE

- PP

- PET

- PLA

- Paper & Paperboard

- Others

By Packaging Type

- Films

- Pouches

- Bags

- Trays & Containers

- Bottles

- Others

By End-Use Industry

- Food & Beverage

- Pharmaceuticals & Healthcare

- Personal Care & Cosmetics

- Homecare & Household

- Others

By Application

- Dairy Products

- Meat

- Poultry & Seafood

- Fresh Fruits & Vegetables

- Bakery & Confectionery

- Pet Food

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Monomaterial Packaging Market

- Amcor plc

- Mondi Group

- Berry Global Group, Inc.

- Huhtamaki Oyj

- DS Smith Plc

- Sealed Air Corporation

- Constantia Flexibles

- Uflex Limited

- Rengo Co., Ltd.

- International Paper Company

- WestRock Company

- Sonoco Products Company

- Graphic Packaging Holding Company

- Sappi Limited

- Greiner Packaging International GmbH

* List Not Exhaustive

Methodology

USDAnalytics utilizes a rigorous and integrated research methodology to deliver comprehensive insights into the global Monomaterial Packaging market. Our approach combines primary research, including detailed interviews with packaging engineers, sustainability managers, supply chain executives, and R&D specialists, with secondary research sourced from regulatory filings, corporate reports, industry publications, and trade associations. Market sizing and forecasting leverage historical trends, CAGR projections, material adoption rates (PE, PP, PET, PLA, and paperboard), and end-use industry dynamics across food & beverage, pharmaceuticals, personal care, and e-commerce packaging. We evaluate technological innovations such as high-barrier monomaterial films, bio-based and marine-degradable polymers, digital watermarking for recycling, and advanced coatings, alongside regulatory influences like Extended Producer Responsibility (EPR), PPWR, and plastic taxes. Competitive intelligence assesses mergers, acquisitions, sustainability initiatives, and global capacity expansions by leading players including Amcor, Mondi, Berry Global, Sealed Air, and ProAmpac, emphasizing their role in driving recyclable, high-performance, and premium monomaterial packaging solutions. This methodology ensures USDAnalytics delivers actionable, reliable, and data-driven insights that enable industry professionals to optimize packaging design, achieve regulatory compliance, and capitalize on emerging market opportunities.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.