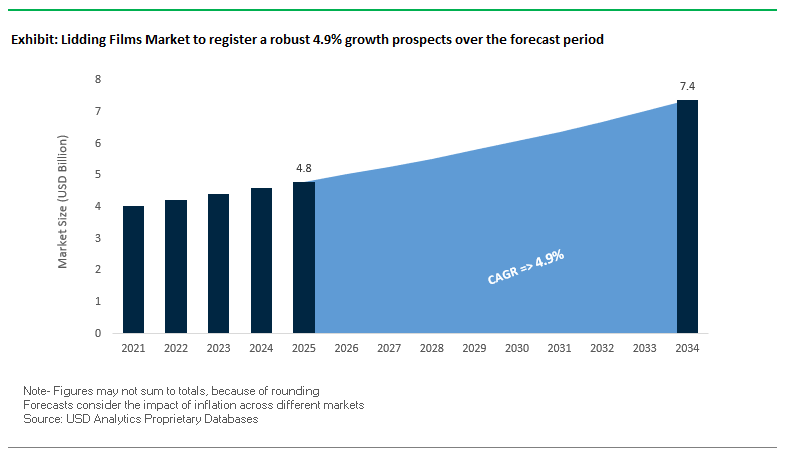

Lidding Films Market Overview: Shelf-Life, Sustainability, and Speed Define Growth (MV: USD 4.8 Bn in 2025 → USD 7.4 Bn by 2034, CAGR 4.9%)

The global lidding films market is scaling steadily as brand owners and retailers prioritize extended shelf life, food safety, and recyclability across ready meals, dairy, meat, fresh produce, and healthcare trays. High-barrier PE/PP/PET lidding structures—with oxygen/moisture barriers, anti-fog, easy-peel/reseal, and tamper evidence—are now core to retail merchandising and cold-chain integrity. Procurement teams are shifting specs toward mono-material lidding films (PP- or PE-based) to meet design-for-recycling targets without sacrificing seal integrity, hot-fill/retort resistance, machinability, or high-speed tray-sealing throughput.

Key insights

- Shelf-life first: High-barrier MAP-ready lidding films materially cut waste in meat, dairy, and ready meals.

- Convenience upsell: Single-serve and ready-to-eat formats are accelerating peelable and resealable lidding adoption.

- Sustainable structures: Mono-material PP/PE lidding enables tray-to-tray recycling, supporting retailer ESG scorecards.

- Merchandising optics: High-clarity, anti-fog lidding safeguards visibility in chilled cabinets—vital for conversion.

Market Analysis: Recent Developments Signal Barrier, Mono-Material, and PCR Momentum

Industry moves in 2025 concentrate on barrier innovation, recyclability, and scale. In August 2025, Constantia Flexibles completed the acquisition of FFP Packaging Solutions, materially strengthening its UK presence and its sustainable lidding films portfolio. Also in August 2025, Amcor unveiled a new high-barrier, easy-peel lidding film designed to extend fresh-produce life and curb food waste—an unmistakable push toward MAP-optimized breathable and barrier solutions. Sealed Air followed in July 2025 with an anti-fog lidding film tailored for refrigerated/frozen channels, addressing condensation and branding clarity in cold-chain retail.

Circularity is moving from pilot to production. In May 2025, Klöckner Pentaplast (kp) launched lidding films with ≥30% PCR content, bringing recycled material into contact-sensitive applications under robust compliance frameworks. Coveris committed new extrusion capacity in February 2025 to scale sustainable, high-performance lidding, while Jindal Films showcased recyclable PP mono-material barrier lidding in April 2025, proving mono-PP can meet high-speed packaging demands. Mondi introduced compostable lidding in March 2025 for organic brands prioritizing bio-based end-of-life options, and UPM Raflatac’s June 2025 rebrand to UPM Adhesive Materials underscores broader adhesive/tapes synergies that influence lidding seal-layer strategies.

Key Trends and Strategic Opportunities in the Lidding Films Market

Accelerated Shift to Mono-Material, Polyolefin-Based Structures for Enhanced Recyclability

The lidding films market is witnessing a significant move toward mono-material polyolefin structures, driven by stringent Extended Producer Responsibility (EPR) regulations and brand sustainability initiatives. Multi-layer laminates, such as PET/PE and NY/PE, are increasingly being replaced by single-polymer designs like PP/PP and PE/PE, which align with existing polyolefin recycling streams. Corporations like Hartmann have adopted polypropylene (PP) films for products like Bacillol® Zero Tissues, improving recyclability and contributing to circular packaging solutions. Industry-wide initiatives, such as Profol’s CPPeel® lidding film, demonstrate a 4x better CO2 balance compared to aluminum lids, highlighting both environmental and operational advantages. Strategic product development by KM Packaging and technological advancements from barrier film producers like TOPPAN showcase how essential barrier properties can be maintained while transitioning to fully recyclable mono-material films. This trend reflects the convergence of sustainability regulations, corporate ESG goals, and technological innovation in high-performance lidding solutions.

Integration of Advanced Sealants and Active Coatings for Extended Fresh Food Shelf-Life

To address food waste and evolving consumer expectations, lidding film manufacturers are increasingly incorporating active and functional coatings into packaging. Anti-fog coatings improve product visibility, while integrated oxygen or ethylene absorbers significantly extend the freshness of perishable goods. Studies by ReFED indicate that efficient food packaging could divert an estimated 72,000 tons of U.S. food waste annually, emphasizing the direct environmental impact of these innovations. Active packaging reduces oxidation-related spoilage, which accounts for approximately 25% of post-harvest losses, and supports “clean label” initiatives by minimizing the need for chemical preservatives. Additionally, improved consumer experience, such as anti-fog visibility for refrigerated products, strengthens brand perception and drives adoption among food manufacturers seeking sustainable and functional packaging solutions.

Development of High-Barrier, Retortable Lidding Films for Pet Food and Human Nutrition

The growing markets for premium wet pet food and ready-to-eat human meals are driving demand for lidding films that can withstand retort sterilization at high temperatures (

121°C). Retortable mono-material films offer a lightweight and sustainable alternative to traditional metal lids while providing enhanced functionality, such as easy peelability and superior branding surfaces. Mondi’s innovative retortable pouches demonstrate the potential to replace aluminum lids while maintaining high barrier properties essential for extending shelf life up to two years. These films also reduce the need for refrigeration during transport and storage, providing both cost and environmental benefits. This opportunity allows packaging manufacturers to capture value by offering lightweight, convenient, and sustainable solutions tailored to premium food and pet product segments.

On-Demand Digital Printing Compatibility for Short-Run and Personalized Packaging

The rise of e-commerce, personalized nutrition, and niche brands is creating demand for short-run, customized packaging solutions. Lidding films with pre-treated surfaces compatible with high-speed digital printing (e.g., UV-curable inkjet) allow for flexible customization, versioning, and regionalization without the high costs of traditional flexographic plates. Digital printing eliminates tooling expenses, reduces time-to-market, and enables rapid response to consumer trends. Brands like Coca-Cola have leveraged digitally printed packaging to execute hyper-localized campaigns efficiently. Moreover, hybrid printing strategies—combining digital and traditional flexographic methods—allow companies to optimize production efficiency while offering targeted customization for seasonal or regional product variants. This opportunity positions digital-compatible lidding films as a key enabler of agile and consumer-focused packaging strategies.

Competitive Landscape: High-Barrier Specialists and Mono-Material Leaders Set the Pace

The global lidding films industry is led by converters and materials innovators scaling high-barrier, anti-fog, easy-peel, and mono-material platforms. Vendors differentiate on sealability across substrates (PET/rPET, PP, PE, HIPS), PCR/compostable content, regulatory compliance, and machinability at scale.

Amcor: Scaling easy-peel, high-barrier, recycle-ready lidding

Amcor’s portfolio spans high-barrier, easy-peel, and anti-fog lidding for produce, ready meals, dairy, and healthcare. Innovations like P-Plus™ flexible lidding tune permeability for produce respiration, extending freshness vs. clamshells while adding billboard graphics. The company’s strategy centers on recyclable/reusable/compostable formats by 2025, with mono-PE/PP lidding engineered for PET, PP, PE trays and aseptic/retort/hot-fill conditions. Integrated design-to-manufacture support helps reduce time-to-line and validation risk.

Sealed Air (CRYOVAC): Anti-fog optics with cold-chain reliability

Under CRYOVAC®, Sealed Air provides anti-fog + oxygen-barrier lidding optimized for protein and chilled prepared foods. Its recycle-ready lidding for mono-PET/rPET trays and Multi-Seal FlexLOK reseal feature lift consumer convenience and reduce food waste. Global R&D focuses on consistent peel forces, broad sealing windows, and puncture resistance to sustain 72-hour+ cold-chain performance and high-speed throughput in e-commerce and retail channels.

Klöckner Pentaplast (kp): PCR-enabled barrier top webs

kp FlexiLid barrier lidding—produced via advanced blown extrusion—targets thin-gauge, strong-seal performance to extend shelf life without compromising machinability. New ranges with ≥30% PCR support brand circularity KPIs while maintaining clarity, anti-fog, and peelability. Options include die-cut, lock-seal, peelable, and burst-peelable formats compatible with common tray materials and lidding equipment.

Constantia Flexibles: Ecolutions-driven mono-PE barrier leadership

Constantia invests heavily (incl. MDO lines) to scale EcoLam mono-PE structures such as EcoLamHighPlus for recycle-ready lidding and laminates. The FFP Packaging Solutions acquisition (August 2025) boosts UK capacity and know-how in sustainable lidding for dairy and ready meals. The portfolio spans aluminum-based, easy-peel, and high-barrier options for retort/dry applications with strong weight reduction and LCA gains.

Coveris: Capacity expansion and closed-loop “No Waste” strategy

Coveris builds customized lidding films for food, dairy, and medical, emphasizing EVOH-barrier shelf-life extension and automation compatibility. Its ReCover platform closes the loop—collecting, recycling, and reintegrating post-consumer materials—while February 2025 extrusion investments expand sustainable, high-performance lidding supply. Engineering priorities include sealing latitude, optical clarity, and line efficiency on fast tray-seal systems.

Jindal Films: Mono-PP lidding for high-speed lines

Jindal leverages BOPP/BOPE expertise to deliver recyclable PP mono-material lidding with high thermal stability, excellent machinability, and tuned barrier/peel layers. The April 2025 showcase confirmed mono-PP viability on high-speed flexible packaging lines, aligning with retailer recycling guidelines. Ongoing R&D targets higher PCR integration, optimized COF, and anti-fog clarity for chilled cabinets.

Lidding Films Market Share Insights

Ready-to-Eat Meals Lead Market Share by Application in the Lidding Films Industry

Ready-to-eat meals account for the largest application share, representing 25% of the lidding films market in 2025, as convenience-driven consumption reshapes global food habits. These films must provide strong seals, high-barrier performance, and easy-peel functionality to maintain freshness, prevent leakage, and deliver consumer convenience. Meat, poultry, and seafood packaging also commands a substantial share, driven by the need for modified atmosphere packaging (MAP) to extend shelf life and preserve visual appeal. Dairy products such as yogurt and desserts represent another high-volume category, where delamination and hermetic sealing are critical. Fruits and vegetables utilize lidding films with anti-fog properties to enhance product visibility on shelves, while pharmaceuticals and medical packaging leverage sterile, tamper-evident lidding for safety and compliance. The application mix demonstrates how ready-to-eat meals spearhead demand, supported by protein, dairy, and pharmaceutical segments that demand technical performance.

Peelable Lidding Films Dominate Market Share by Technology in the Lidding Films Industry

Peelable lidding films hold the largest technology share at 50% in 2025, as they embody the core of convenience-oriented packaging. These films balance secure sealing with easy opening, making them essential for dairy cups, ready-to-eat trays, medical device packs, and single-serve formats. The global shift toward consumer convenience and on-the-go lifestyles has cemented peelable films as the market leader. High-barrier lidding films also maintain a critical share due to their ability to extend the shelf life of oxygen-sensitive products like meats, seafood, and premium ready meals, where protection against gas exchange is vital. Heat-sealable and anti-fog films provide functional support, with the former enhancing durability in permanent seals and the latter ensuring product visibility in chilled environments. This segmentation reflects how peelable films dominate through convenience and safety, while high-barrier solutions address the preservation needs of perishable and high-value products.

United States Lidding Films Market Grows on Regulatory Compliance and High-Barrier Innovations

The U.S. lidding films market is heavily shaped by a fragmented regulatory landscape, including FDA regulations ensuring product safety and integrity in food, beverage, and pharmaceutical packaging. The Drug Supply Chain Security Act (DSCSA) drives demand for track-and-trace high-performance lidding films, especially for pharmaceuticals and biologics. Technological advancements, such as the adoption of metallized PET (MET PET) films and dual-ovenable PP films, are transforming the ready-to-eat meals sector by offering superior durability, stiffness, and oxygen barrier properties.

Corporate investments are focused on sustainability, with initiatives like single-stream curbside recycling pilots for flexible plastics, demonstrating the technical feasibility of recyclable lidding films. Key applications are concentrated in e-commerce, healthcare, and ready-to-eat meals, driven by consumer demand for fresh, high-quality products—the so-called “Amazon Effect.” The industry is increasingly prioritizing mono-material recyclable lidding films made from PE and PP to meet brand sustainability targets and comply with evolving environmental regulations.

Germany Lidding Films Market Advances Through Circular Economy and Barrier Innovations

Germany’s lidding films market operates under a stringent regulatory framework, including the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, mandating fully recyclable or reusable packaging by 2030. This has accelerated adoption of sustainable, mono-material lidding films designed for recyclability.

Technological innovation is a hallmark of the German market. Companies are developing high-barrier, anti-fog, and easy-peel films to meet the diverse demands of the food industry. The Packaging Act (VerpackG) incentivizes design for recycling, strengthening demand for environmentally friendly lidding solutions. Corporate investments by domestic and international players are expanding sustainable and high-performance film portfolios, positioning Germany as a leader in eco-friendly lidding technologies.

China Lidding Films Market Expands with Green Policies and Smart Manufacturing

China’s lidding films industry is undergoing transformation under the government’s dual carbon policy, promoting sustainable materials and recycling. The Action Plan for Promoting Large-Scale Equipment Updates encourages eco-friendly production, while revised standards like GB/T 31268 regulate excessive packaging, directly affecting e-commerce and FMCG packaging sectors.

Technological adoption is accelerating, with automation, AI, and RFID-enabled tracking systems optimizing production and logistics. Domestic manufacturers are expanding capacity to meet growing demand for high-quality, circular lidding films. The booming e-commerce, electronics, and food sectors are driving innovation in specialized lidding films with enhanced barrier properties, durability, and sustainability.

India Lidding Films Market Strengthens Through Circular Economy Policies and Industrial Growth

India’s lidding films market is benefiting from government initiatives promoting a circular economy, including the ban on single-use plastics introduced in 2022. These measures are catalyzing adoption of sustainable flexible packaging solutions across industries.

The market is seeing technological advancements with a focus on high-barrier lidding films for the food processing and cold chain sectors. Corporate investments are increasing, supported by expansions in food and beverage, pharmaceutical, and e-commerce industries. Rising exports of industrial and pharmaceutical products are creating demand for modern, high-performance lidding films that comply with international safety and regulatory standards.

Japan Lidding Films Market Drives Innovation Through Advanced Materials and High-Performance Products

Japan’s lidding films industry leverages precision manufacturing to produce next-generation packaging solutions. Regulatory guidance through the Plastic Resource Circulation Act and revised food contact regulations supports sustainable design and reduced single-use plastics.

Japanese manufacturers, including Toray Industries, are leading innovation in peelable, bio-based, and high-barrier lidding films. Market focus is on specialty and value-added applications, with innovations such as anti-fog and self-sealing films to meet specific industrial needs. The emphasis on high-performance, environmentally responsible lidding films ensures Japan remains a key hub for advanced packaging technologies.

Brazil Lidding Films Market Grows Through Sustainable Waste Management and Strategic Investments

Brazil’s lidding films market is evolving under the National Solid Waste Policy, which modernizes waste management and drives sustainable packaging adoption. Trade regulations like provisional antidumping duties on PE imports are promoting domestic production and circular solutions.

Technological advancements focus on biodegradable, recyclable, and compostable films to reduce environmental impact. The market is strong in food and beverage, agricultural, and ready-to-eat sectors, supported by corporate investments from companies like Amcor, which achieved ISCC Plus certification for sustainable production. These initiatives position Brazil as a growing leader in eco-friendly lidding film manufacturing in Latin America.

Lidding Films Market Report Scope

Lidding Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.8 Billion

|

|

Market Size (2034)

|

$7.4 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Material (PE, PP, PET, Aluminum, Others), By Application (Meat, Poultry & Seafood, Dairy Products, Ready-to-Eat Meals, Fruits & Vegetables, Bakery & Confectionery, Pharmaceuticals & Medical, Other Applications), By Technology (Peelable Lidding Films, Heat-Sealable Lidding Films, High-Barrier Lidding Films, Anti-Fog Lidding Films)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Sealed Air Corporation, DS Smith Plc, Uflex Ltd., Tekni-Plex, Inc., Toray Plastics (America), Inc., Wipak Group, Sonoco Products Company, KM Packaging, Winpak Ltd., Berry Global, Inc., Placon Corporation, TCL Packaging Ltd., Schur Flexibles Holding GesmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Lidding Films Market Segmentation

By Material

- PE

- PP

- PET

- Aluminum

- Others

By Application

- Meat

- Poultry & Seafood

- Dairy Products

- Ready-to-Eat Meals

- Fruits & Vegetables

- Bakery & Confectionery

- Pharmaceuticals & Medical

- Other Applications

By Technology

- Peelable Lidding Films

- Heat-Sealable Lidding Films

- High-Barrier Lidding Films

- Anti-Fog Lidding Films

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Lidding Films Market

- Amcor plc

- Mondi Group

- Sealed Air Corporation

- DS Smith Plc

- Uflex Ltd.

- Tekni-Plex, Inc.

- Toray Plastics (America), Inc.

- Wipak Group

- Sonoco Products Company

- KM Packaging

- Winpak Ltd.

- Berry Global, Inc.

- Placon Corporation

- TCL Packaging Ltd.

- Schur Flexibles Holding GesmbH

* List Not Exhaustive

Methodology

USDAnalytics applies a rigorous multi-layered research methodology to deliver fact-based insights into the Lidding Films Market. Primary research included structured interviews with packaging engineers, R&D specialists, procurement heads, sustainability officers, and supply chain managers across major geographies, providing firsthand perspectives on barrier innovations, recyclability initiatives, and evolving regulatory compliance. Secondary research involved analyzing annual reports, sustainability disclosures, trade statistics, government regulations (such as FDA, EU PPWR, and India’s plastic ban), patent databases, and peer-reviewed journals to validate industry developments. Data triangulation was used to integrate macroeconomic indicators, raw material pricing (PE, PP, PET, and aluminum), and adoption rates of mono-material and PCR-based lidding films. Market sizing and forecasts were built using both top-down and bottom-up approaches, combining production capacities, regional trade flows, and consumption trends across applications like ready meals, dairy, protein, fresh produce, and pharmaceuticals. Forecast models were stress-tested against scenarios such as accelerated adoption of EPR-compliant recyclable packaging, growth in digital printing, and consumer-driven sustainability goals, ensuring accuracy and practical relevance. This methodology enables USDAnalytics to provide reliable, actionable intelligence for business leaders, R&D teams, and investors navigating the global lidding films industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.