Mirror Coatings Market Size, Copper-Free Technologies, and High-Reflectivity Glass Applications Outlook

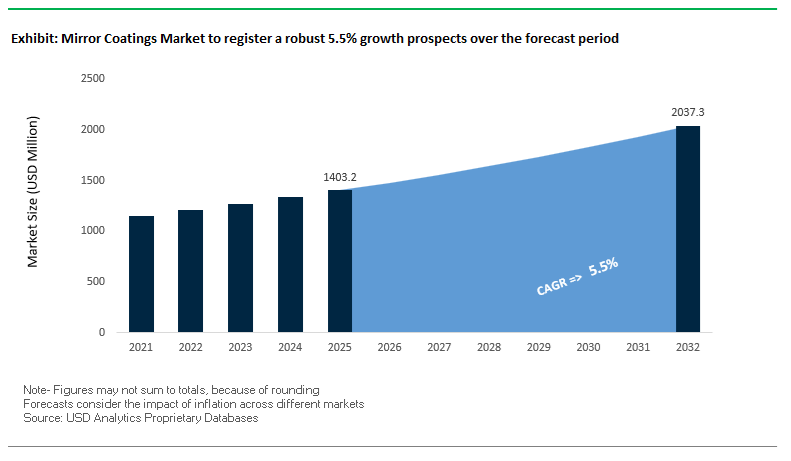

The global mirror coatings market was valued at $1,403.2 million in 2025 and is projected to reach $2,041.2 million by 2032, expanding at a CAGR of 5.5%. Market growth is driven by rising demand for high-reflectivity mirror coatings, silver-based coatings, aluminum mirror coatings, copper-free mirror systems, and protective mirror-backing coatings across architectural, automotive, solar, and decorative applications. As industries increasingly prioritize durability, environmental compliance, and optical performance, mirror coatings are evolving beyond aesthetics to deliver corrosion resistance, enhanced reflectivity, and long-term stability.

A key growth driver is the shift toward copper-free and lead-free mirror coatings, which eliminate toxic byproducts associated with traditional mirror manufacturing processes. These advanced systems are increasingly adopted in green building projects, commercial interiors, and high-humidity environments, where durability and environmental safety are critical. Additionally, growing demand for premium interior design, smart mirrors, and solar reflective technologies is expanding the application scope of mirror coatings in both residential and commercial sectors.

The market is also benefiting from advancements in vacuum deposition technologies, nano-coatings, and high-performance backing systems, which improve adhesion, moisture resistance, and longevity. Innovations in low-VOC formulations and water-based coatings are aligning with global sustainability standards, while the use of reduced-iron glass substrates is enhancing color clarity and optical precision in premium mirror applications. Regionally, Asia-Pacific leads due to strong construction activity, while Europe and North America drive sustainability-focused innovation and advanced coating technologies.

Market Analysis: Copper-Free Innovation, Sustainability Certifications, and Advanced Backing Systems Driving Market Evolution

The mirror coatings industry is undergoing significant transformation driven by environmental regulations, product innovation, and strategic expansion in high-performance coating systems. In January 2026, Guardian Glass achieved full-scale production capacity for its UltraMirror® product line, focusing on copper-free mirror coatings that eliminate toxic runoff during the silvering process. This advancement reflects the growing industry shift toward environmentally safe and high-reflectivity coating technologies.

Sustainability and transparency are becoming key differentiators. Guardian Glass further strengthened its position by achieving third-party verified Health Product Declarations (HPDs) in January 2025, providing full ingredient transparency for its mirror coatings—an essential requirement for green building certifications. Additionally, its August 2024 Environmental Product Declarations (EPDs) highlight measurable reductions in carbon footprint and VOC emissions, reinforcing the importance of sustainability in coating selection.

Product innovation is advancing both performance and application versatility. Fenzi Group’s March 2026 strategic roadmap introduces its Next Generation Reactive mirror-backing series (Duralux), available in high-durability epoxy and water-based formulations, targeting improved corrosion resistance and long-term protection. Similarly, Saint-Gobain’s May 2024 showcase of eco-friendly Mirasafe and SGG Mira mirrors emphasizes lead-free and low-solvent coatings, aligning with stringent Indian Green Building Council (IGBC) standards.

Technological advancements in substrates and coating systems are enhancing optical performance. Guardian Glass’s April 2024 launch of CrystalClear™ reduced-iron glass improves color rendering and clarity, supporting premium applications in retail and hospitality environments. Furthermore, strategic collaborations, such as the September 2024 agreement between Guardian Glass and Privacy Glass Solutions, are expanding the use of opaque mirror-like coatings for privacy glass applications in healthcare and commercial sectors.

Training and application expertise are also gaining importance in ensuring coating durability. Guardian Glass’s November 2024 “Stewardship Training Series” focuses on educating industrial applicators on vacuum-coated and mirror-backing technologies, particularly for high-humidity environments, where improper application can lead to premature coating failure.

Regional expansion and project-based growth continue to support market development. Fenzi Group’s March 2024 supply contract for architectural projects in Brazil highlights strong demand for decorative and functional mirror coatings in emerging markets.

Aesthetic trends are also influencing innovation. Sherwin-Williams’ 2024 color strategy, including the “Upward” trend, is being integrated into mirror coating R&D, supporting evolving design preferences in interior architecture and decorative glass applications.

Market Trend: Magnetron Sputtered Silver Coatings Enabling High-Performance Architectural Mirrors

The mirror coatings industry is undergoing a fundamental transition in architectural applications, driven by the rapid adoption of magnetron sputtering technology for silver deposition. This Physical Vapor Deposition (PVD) approach is replacing traditional wet chemical silvering processes, particularly in high-end construction projects that demand superior durability, precision, and compatibility with thermal processing.

Magnetron sputtering enables atomic-scale control over coating thickness, typically in the range of 50 to 100 nanometers, delivering a significant improvement in coating uniformity across large-format glass panels. For jumbo architectural glass sizes up to 3.2 by 6.0 meters, this results in approximately 30% higher thickness consistency compared to conventional spray-based wet processes. This level of precision is critical for maintaining consistent reflectivity and optical performance across large façade installations and interior mirror applications.

Thermal stability is a key differentiator driving adoption. Sputtered mirror coatings can withstand tempering temperatures exceeding 600°C, enabling the production of safety-rated, toughened mirrors suitable for high-traffic environments such as elevators, commercial lobbies, and fitness facilities. In contrast, traditional wet-silvered mirrors are prone to delamination under such conditions, limiting their use in safety-critical applications.

Operational efficiency and environmental performance further strengthen the case for sputtering technologies. Manufacturing audits conducted in 2025 indicate that sputtering lines reduce energy consumption per square meter by approximately 15% while eliminating the need for water-intensive chemical processing and heavy metal waste treatment. This aligns with sustainability objectives and regulatory pressures, positioning magnetron sputtering as the preferred technology for next-generation architectural mirror production.

Market Trend: Copper-Free and Low-VOC Mirror Backing Systems Advancing Automotive Sustainability and Durability

The automotive mirror segment is experiencing a parallel shift toward copper-free and environmentally compliant coating systems, driven by the need to improve corrosion resistance while reducing environmental impact. Traditional mirror constructions rely on a copper interlayer to protect the reflective silver coating; however, issues related to electrochemical corrosion and toxicity have accelerated the adoption of advanced organic and polyurethane-based backing systems.

Modern copper-free mirror coatings are achieving high levels of corrosion resistance, exceeding 480 hours in Copper-Accelerated Salt Spray testing with minimal edge degradation. These performance levels match or surpass those of legacy copper-based systems, ensuring long-term durability in harsh environmental conditions, including exposure to road salts and moisture.

Environmental compliance is another critical driver. The transition to waterborne and high-solids backing coatings has enabled a 60% to 80% reduction in VOC emissions within automotive mirror production lines. This ensures alignment with stringent regulatory frameworks such as REACH in Europe and emissions standards in North America, which are increasingly influencing supplier qualification for automotive OEMs.

Material optimization is also contributing to lightweighting initiatives. By eliminating the metallic copper layer and optimizing polymer-based backing systems, manufacturers have achieved approximately 5% reduction in total mirror weight. While modest at the component level, this contributes to cumulative vehicle weight reduction, supporting energy efficiency and range extension objectives in electric vehicles. These advancements are positioning copper-free mirror coatings as a standard specification in modern automotive manufacturing.

Market Opportunity: DOE Solar Energy Programs Driving Innovation in High-Durability CSP Mirror Coatings

The expansion of concentrating solar-thermal power (CSP) technologies is creating a significant opportunity for advanced mirror coatings, supported by funding initiatives from the U.S. Department of Energy’s Solar Energy Technologies Office. These programs are focused on improving the durability and performance of heliostat mirrors, which are critical components in CSP systems.

A primary objective of these initiatives is to reduce the levelized cost of solar-thermal electricity to $0.05 per kilowatt-hour by 2030. Achieving this target requires mirror coatings capable of maintaining specular reflectance above 95% over extended operational lifetimes. This is driving demand for coatings with enhanced resistance to environmental degradation, including UV exposure, dust accumulation, and mechanical abrasion.

Funding availability is a key enabler of innovation. In the 2025 to 2026 cycle, over $25 million has been allocated specifically for research and development projects targeting improvements in soiling resistance and abrasion resistance of mirror coatings. These investments are fostering collaboration between coating manufacturers, research institutions, and energy developers, accelerating the commercialization of next-generation reflective materials.

The increasing scale of CSP deployment, combined with performance-driven funding mechanisms, is positioning high-durability mirror coatings as a critical component in the renewable energy value chain, creating long-term growth opportunities for advanced coating technologies.

Market Opportunity: China’s 30-Year CSP Durability Mandates Creating Demand for Ultra-Stable Reflective Coating Systems

China’s aggressive expansion of solar-thermal power capacity is creating a large-scale opportunity for advanced mirror coatings, driven by stringent performance requirements established under national energy policies and long-term infrastructure planning. The latest mandates specify a minimum service life of 30 years for CSP mirrors, significantly exceeding the historical industry benchmark of 20 years.

To meet these requirements, mirror coatings must demonstrate extremely low degradation rates, typically below 0.1% per year, even under harsh desert conditions characterized by intense ultraviolet radiation and abrasive sand exposure. This has led to increased adoption of advanced dielectric overcoats, such as alumina-silica multilayer systems, which provide enhanced protection for the underlying silver reflective layer.

The scale of deployment further amplifies the opportunity. As of early 2026, China has approximately 30 CSP projects under construction, representing a combined capacity of over 3.1 million kilowatts. Each gigawatt of CSP capacity requires millions of square meters of high-performance mirror surfaces, translating into substantial demand for durable, high-reflectivity coating systems.

These developments are positioning China as a key global driver for innovation in mirror coating technologies, with significant implications for material science advancements, manufacturing scale, and competitive dynamics in the renewable energy coatings market.

Mirror Coatings Market Share and Segmentation Insights

Silver-Based Mirror Coatings Capture 55.6% Share Driven by High Reflectance and Premium Applications

The mirror coatings market by substrate material is led by silver-based mirror coatings, accounting for 55.6% of the global market share in 2025, due to their unmatched optical performance and widespread use in high-end applications. Silver delivers 95–99% reflectivity across the visible spectrum, significantly outperforming aluminum (90–92%) and chrome (55–65%), making it the preferred material for architectural mirrors, automotive mirrors, solar reflectors, and optical instruments such as telescopes. However, pure silver is highly prone to tarnishing, necessitating advanced multi-layer coating systems that include copper underlayers and dielectric overcoats (e.g., silicon dioxide, titanium dioxide) for enhanced durability and corrosion resistance. This added complexity increases the value proposition of silver coatings, reinforcing their dominance in the high-performance mirror coatings market.

Backside Coatings Hold 68.4% Share Due to Mass Manufacturing and Surface Protection Advantages

In the mirror coatings market by application area, backside coatings dominate with a 68.4% market share in 2025, driven by their widespread adoption in consumer, automotive, and construction applications. This method involves applying the reflective coating to the rear side of a glass substrate, followed by protective paint layers, ensuring scratch resistance and long-term durability. Backside coatings are the standard for bathroom mirrors, furniture mirrors, and automotive rearview mirrors, where cost efficiency and ease of manufacturing are critical. High-speed production lines, operating at up to 10 meters per minute, enable the large-scale output of millions of square meters annually, supporting global demand across multiple industries. This combination of scalability, durability, and cost-effectiveness firmly establishes backside coatings as the leading segment in the global mirror coatings market.

Competitive Landscape in the Mirror Coatings Market

Fenzi leads mirror backing coatings with water-based and integrated glass chemistry solutions

Fenzi Group remains the global leader in mirror coatings, particularly in the backing segment, leveraging its comprehensive portfolio of glass processing chemicals. Its Duralux range dominates both silver and aluminum mirror applications, with the 2026 introduction of water-based formulations significantly reducing VOC emissions while maintaining high corrosion resistance. The company is actively promoting next-generation reactive technologies through global exhibitions such as GlassBuild America and Glasstec 2026. With 12 manufacturing facilities across key regions, Fenzi ensures localized supply of Luxver silvering chemicals, particularly supporting demand in Asia-Pacific construction markets. Its vertical integration across sealants, enamels, and coatings provides a strong competitive edge in end-to-end mirror production solutions.

Sherwin-Williams strengthens industrial mirror coatings with protective durability and supply chain reach

The Sherwin-Williams Company leverages its industrial coatings expertise to deliver high-performance mirror backing systems for commercial and automotive applications. In Q1 2026, the company reported a 6.8% increase in net sales to $5.67 billion, with strong profitability in its Performance Coatings Group. Sherwin-Williams is implementing pricing strategies and cost optimization measures to manage raw material volatility in the coatings supply chain. Its extensive network of over 4,400 stores enables localized technical support for large-scale architectural projects, including high-reflectivity solar mirrors. The company’s strength in protective and marine coatings translates into durable mirror backing systems designed for harsh environmental conditions.

Arkema advances bio-based polymer solutions for lightweight and smart mirror applications

Arkema is driving innovation in mirror coatings through its advanced polymer technologies and bio-based material solutions. At Chinaplas 2026, the company showcased Rilsan® Clear transparent polyamides, offering lightweight, BPA-free alternatives for consumer electronics and AR/VR mirror applications. Its new production unit in Singapore strengthens its position as a leading supplier of transparent polyamides in Asia. Arkema’s Luperox® organic peroxides play a critical role in curing high-performance mirror coatings for automotive and solar energy applications. Through its Tippox™ bio-based additives, the company is enabling manufacturers to reduce VOC emissions and production defects, aligning with global sustainability and decarbonization goals in the coatings industry.

Vibrantz drives functional mirror coatings with copper-free and solar-grade technologies

Vibrantz Technologies, formed through the merger of Prince, Ferro, and Chromaflo, is a major player in functional mirror coatings and glass solutions. The company specializes in high-durability silvering paints and copper-free mirror technologies that comply with stringent REACH regulations while preventing corrosion issues such as black edge formation. Vibrantz plays a key role in the concentrated solar power (CSP) sector, providing coatings that enhance reflectivity and durability of solar mirrors. Its integration of legacy Ferro assets has strengthened its unified glass coatings portfolio, targeting growth in emerging markets such as India and China. The company’s expertise in pigments and dispersion technologies ensures consistent color stability and UV resistance in decorative mirrors.

Saint-Gobain integrates smart coatings and Low-E technologies for energy-efficient mirrors

Saint-Gobain is a technological leader in advanced mirror coatings through its integration of glass manufacturing and coating technologies. With a reported turnover of €46.5 billion in 2025, the company is focusing on high-performance building solutions under its “Lead & Grow” strategy. Its Verifi digital monitoring system ensures precise coating thickness and uniformity during float glass production, enhancing product quality and consistency. Saint-Gobain’s expertise in low-emissivity (Low-E) coatings enables mirrors to reduce infrared heat transfer, improving energy efficiency in buildings. The company’s strategic focus on sustainable construction solutions positions it as a key player in smart and energy-efficient mirror coating technologies.

China Mirror Coatings Market: Solar Energy Expansion and High-Reflectivity Innovations Driving Dominance

China leads the global mirror coatings market, fueled by aggressive investments in renewable energy infrastructure and large-scale urban modernization projects. Under the “2026–2030 Renewable Energy Expansion Plan,” the country is deploying massive Concentrated Solar Power (CSP) plants, particularly in the Gobi Desert, creating strong demand for high-reflectivity, sand-abrasion-resistant mirror coatings. Technological advancements such as ultra-white glass coatings with solar reflectivity index (SRI) exceeding 94% are setting new performance benchmarks for solar thermal applications.

Industrial expansion is further strengthening China’s leadership, with the establishment of automated production lines for BPA-free and lead-free mirror backing paints to meet global export standards. Regulatory enforcement of GB/T 38597-2026 is pushing manufacturers toward low-VOC coating technologies, while investments in magnetron sputtering (PVD) are replacing traditional wet-silvering processes for high-end applications. The market is also expanding into smart infrastructure, with one-way mirror coatings used in surveillance systems and smart buildings, reinforcing China’s dominance across both energy and construction sectors.

Germany Mirror Coatings Market: Precision Optics and Smart Glass Integration for Advanced Applications

Germany represents a technology-driven hub for mirror coatings, driven by expertise in optical thin films, smart glass technologies, and automotive innovation. The commercialization of visible-light photocatalytic mirror coatings is enhancing performance in sectors such as healthcare and hospitality by enabling self-cleaning surfaces that decompose organic contaminants under ambient light.

The integration of dielectric mirror coatings in EV heads-up displays (HUDs) is transforming automotive applications, allowing high transparency for sensor data while maintaining reflective properties. Strong regulatory alignment with EU REACH directives is accelerating the transition toward 100% water-based coating systems, eliminating solvent-based primers. Investments in vacuum insulating glass (VIG) technologies are further boosting demand for mirror coatings that enhance energy efficiency in buildings. Germany’s leadership in laser-grade mirror coatings for semiconductor and medical applications underscores its role as a global innovator in precision coating technologies.

United States Mirror Coatings Market: Smart Surfaces and Defense Applications Driving Innovation

The United States mirror coatings market is characterized by advanced smart surface technologies, nanotechnology integration, and defense-driven innovation. Product developments such as self-healing mirror coatings are enabling surfaces to repair micro-scratches under UV exposure, significantly improving durability and lifecycle performance.

Technological advancements in AI-optimized PVD coating processes are reducing silver consumption while enhancing reflectivity and coating longevity. The market is also benefiting from regulatory frameworks such as ESG disclosure rules, which are driving the adoption of sustainable, cradle-to-cradle coating materials. Key applications include anti-glare (AG) and anti-reflective (AR) coatings for military optical systems and drone sensors, where precision and reliability are critical. Infrastructure investments under federal programs are further boosting demand for energy-efficient mirror coatings in smart buildings, reinforcing the U.S. position as a leader in high-value coating technologies.

India Mirror Coatings Market: Urban Infrastructure Growth and Sustainable Housing Driving Demand

India is emerging as a high-growth market for mirror coatings, driven by rapid urbanization and large-scale infrastructure projects under initiatives such as the Gati Shakti Master Plan. The development of modern airports, railway stations, and smart cities is increasing demand for high-durability architectural mirror coatings.

The transition toward copper-free and lead-free mirror coatings in residential and commercial applications is gaining momentum, supported by government programs like Pradhan Mantri Awas Yojana and GreenPro certification. Technological advancements, including the shift to automated curtain coating systems, are improving production efficiency and reducing waste in the SME sector. Investments in projects such as GIFT City are further driving demand for heat-reflective mirror façades, while stricter BIS standards are ensuring long-term durability and performance in automotive mirror applications.

Japan Mirror Coatings Market: Functional Aesthetics and Nano-Coating Innovation Leadership

Japan’s mirror coatings market is defined by advanced material science, nano-coating innovations, and functional aesthetics, particularly in electronics and transportation sectors. The development of anti-fog nano-composite mirror coatings is addressing condensation challenges in high-speed rail systems and residential applications.

The country is also leading in premium chrome-effect mirror coatings, widely used in robotics and consumer electronics to deliver both aesthetic appeal and functional performance. Government initiatives under Society 5.0 are promoting the integration of smart mirror technologies with touch-screen capabilities, expanding application scope. Investments in low-carbon glass production using renewable hydrogen energy are further strengthening Japan’s position in sustainable coating technologies. Additionally, ongoing infrastructure renewal projects are driving demand for coatings that can be applied to existing mirrors without substrate replacement, enhancing cost efficiency and sustainability.

Mexico Mirror Coatings Market: Automotive Export Growth and Near-Shoring Opportunities

Mexico is emerging as a strategic hub in the mirror coatings market, primarily driven by its role in the North American automotive supply chain under USMCA. Expansion by companies such as PPG Industries is strengthening production capabilities for high-reflectivity automotive mirror coatings, particularly for the growing electric vehicle market.

Technological advancements include the adoption of electrostatic coating systems, improving efficiency and reducing material waste in automotive mirror production. The market is witnessing strong demand for electrochromic (EC) mirror coatings, which enable automatic dimming in response to light intensity, a standard feature in modern vehicles. Investments in closed-loop silver recovery systems are enhancing sustainability, while regulatory alignment with USMCA is encouraging local sourcing of raw materials. Additionally, innovations in bio-based protective coatings for coastal applications are supporting the hospitality and infrastructure sectors in regions such as the Riviera Maya.

Mirror Coatings Market Report Scope

Mirror Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1403.2 Million

|

|

Market Size (2032)

|

$2041.2 Million

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Resin Type (Polyurethane, Epoxy, Acrylic, Specialty Resins), By Technology (Water-borne Coatings, Solvent-borne Coatings, Nanotechnology-based Coatings, Radiation-Cured), By Substrate Material (Silver-based Mirror Coatings, Aluminum-based Mirror Coatings, Chrome and Specialty Metal Coatings), By End-Use Industry (Architectural and Construction, Automotive and Transportation, Solar Power, Decorative and Furniture, Healthcare and Electronics), By Application Area (Backside, Front-surface Coatings, Internal), By Functional Property (Corrosion Resistance, Abrasion and Scratch Resistance, UV Protection, Anti-Fog, Self-Cleaning)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, FENZI S.p.A., Guardian Glass LLC, Saint-Gobain S.A., AGC Inc., PPG Industries, Inc., Arkema S.A., Nippon Sheet Glass Co., Ltd., Vitro, S.A.B. de C.V., Jenoptik AG, Edmund Optics Inc., Diamon-Fusion International, Inc., AccuCoat Inc., General Optics, Pearl Nano

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Mirror Coatings Market Segmentation

By Resin Type

- Polyurethane

- Epoxy

- Acrylic

- Specialty Resins

By Technology

- Water-borne Coatings

- Solvent-borne Coatings

- Nanotechnology-based Coatings

- Radiation-Cured

By Substrate Material

- Silver-based Mirror Coatings

- Aluminum-based Mirror Coatings

- Chrome and Specialty Metal Coatings

By End-Use Industry

- Architectural and Construction

- Automotive and Transportation

- Solar Power

- Decorative and Furniture

- Healthcare and Electronics

By Application Area

- Backside

- Front-surface Coatings

- Internal

By Functional Property

- Corrosion Resistance

- Abrasion and Scratch Resistance

- UV Protection

- Anti-Fog

- Self-Cleaning

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Mirror Coatings Industry

- The Sherwin-Williams Company

- FENZI S.p.A.

- Guardian Glass LLC

- Saint-Gobain S.A.

- AGC Inc.

- PPG Industries, Inc.

- Arkema S.A.

- Nippon Sheet Glass Co., Ltd.

- Vitro, S.A.B. de C.V.

- Jenoptik AG

- Edmund Optics Inc.

- Diamon-Fusion International, Inc.

- AccuCoat Inc.

- General Optics

- Pearl Nano

*- List not Exhaustive