Market Overview: FMCG Packaging Market to Reach $1.43 Trillion by 2034 at 5.9% CAGR

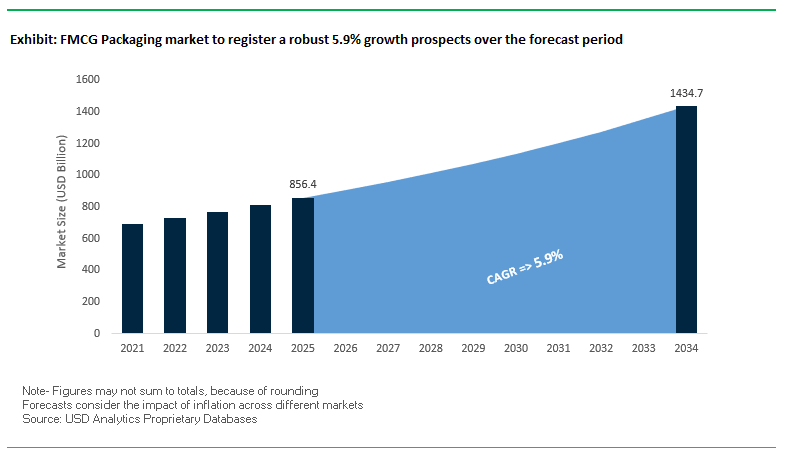

The global FMCG packaging market is set to expand from $856.4 billion in 2025 to $1,434.6 billion by 2034, registering a strong CAGR of 5.9%. This growth is being propelled by sustainability-driven consumer preferences, rapid e-commerce adoption, and digital packaging innovations. FMCG packaging is no longer just a protective medium; it has evolved into a strategic tool for consumer engagement, logistics optimization, and brand differentiation. For industry professionals and buyers, the central questions are: How can packaging improve sustainability compliance, what role will digital technologies like QR and NFC play in strengthening consumer-brand relationships, and how are companies tackling the e-commerce durability challenge?

Key Insights for Industry Stakeholders:

- Sustainability Premium: Over 60% of global consumers indicate a willingness to pay more for eco-friendly packaging, fueling demand for recyclable, compostable, and bio-based materials.

- Rise of Smart Packaging: QR codes, NFC tags, and AR-enabled packaging are redefining consumer engagement in FMCG retail.

- Monomaterial Innovation: Companies are accelerating the adoption of mono-PE and mono-PP flexible packaging for simplified recycling and reduced waste.

- E-commerce Durability: Growth in direct-to-consumer shipping is driving packaging designs optimized for impact resistance, lightweighting, and easy unboxing.

Market Analysis: Recent Developments in the Global FMCG Packaging Industry

The FMCG packaging industry is undergoing rapid transformation, with strategic mergers, sustainable product launches, and material science breakthroughs dominating recent developments.

In August 2025, Amcor reported strong Q4 results, confirming continued growth momentum after its major acquisitions and setting the tone for fiscal 2026. In July 2025, two major consolidation events reshaped the market: Smurfit Kappa completed its merger with WestRock, creating Smurfit WestRock, one of the largest sustainable packaging leaders globally, while International Paper finalized its $9.9 billion acquisition of DS Smith, strengthening its European presence in fiber packaging.

Sustainability-focused innovations are also accelerating. In June 2025, Mondi collaborated with Saga Nutrition to introduce a recyclable, paper-based pet food packaging solution, expanding paper into new FMCG categories. Earlier, in April 2025, Amcor closed its all-stock acquisition of Berry Global, forming a packaging powerhouse in consumer and healthcare packaging solutions. That same month, Billerud launched a new formable fiber-based material, designed to replace plastics in select applications, showcasing a breakthrough in material science for circular packaging.

In March 2025, DS Smith opened a new R&D and innovation center in the UK, underscoring its leadership in sustainable packaging design, while Mondi won 10 WorldStar Awards in January 2025, highlighting the recognition of its innovation pipeline. Collectively, these developments confirm a market increasingly shaped by scale-driven consolidation, consumer-centric design, and ESG-aligned innovations.

Trends and Opportunities Reshaping the FMCG Packaging Market

Regulatory Mandates Driving Mono-Material and Recyclable Packaging Design

The FMCG packaging market is undergoing a profound transformation as global regulatory frameworks force brands to re-engineer their packaging portfolios. The European Union’s Packaging and Packaging Waste Regulation (PPWR), effective from early 2025, sets legally binding requirements mandating all packaging to be recyclable by 2030, alongside ambitious recycled content quotas such as 30% for PET-based food-contact packaging and 35% for other plastics. Non-compliance is not optional manufacturers face increased Extended Producer Responsibility (EPR) fees, making mono-material and recyclable designs a financial as well as regulatory imperative.

Corporate leaders are responding with measurable, public redesign commitments. PepsiCo’s 2024 ESG report confirms that 93% of its global packaging portfolio is already designed to be reusable, recyclable, or compostable, driven by a transition from multi-layer laminates to recyclable mono-materials. Coca-Cola has accelerated its sustainable packaging pledge by converting all U.S. 20-ounce bottles to 100% rPET, underscoring how multinationals are leveraging recycled plastics to meet circular economy benchmarks. Beyond brand initiatives, $2.1 billion in global private equity investment in 2024 flowed into PET and PE recycling startups, illustrating how regulatory pressure is stimulating capital inflows for infrastructure to close the loop on packaging waste.

Digital Integration Through Smart Packaging at Scale

Digitalization is another defining trend as FMCG brands scale smart packaging technologies from experimental pilots to mass-market adoption. The HolyGrail 2.0 project, involving more than 130 companies, validated the industrial feasibility of digital watermarking, achieving an impressive 95% detection and sorting rate for flexible packaging. This level of granularity allows recyclers to separate food-grade from non-food-grade plastics, improving recycled resin quality and enabling closed-loop systems.

From a consumer engagement perspective, brands are leveraging QR codes and watermarks to connect directly with buyers. A simple scan can provide ingredient transparency, recycling instructions, loyalty program access, or interactive brand storytelling, transforming packaging into a powerful digital channel. At the same time, these technologies help companies comply with emerging digital labeling regulations, which allow digital links to carry multilingual, legally required product information, replacing cluttered physical labels. This dual functionality consumer interaction and regulatory compliance positions smart packaging as a mainstream feature of FMCG supply chains.

Development of Advanced Chemical Recycling-Compatible Packaging

While mechanical recycling remains limited by contamination and material degradation, chemical recycling compatibility offers a high-growth innovation frontier. FMCG brands are increasingly partnering with chemical companies to design packaging optimized for depolymerization processes. For example, Unilever’s multi-year partnership with Neste and Recycling Technologies converts waste plastic into recycled oil, which is then refined into virgin-equivalent feedstock for new packaging.

The key lies in designing for disassembly, where films and polymer blends are engineered to efficiently break down into pure monomers during chemical recycling. This approach is particularly transformative for flexible multi-layer films, one of the FMCG sector’s most problematic waste streams. By enabling these difficult-to-recycle formats to be chemically processed, companies can reduce dependence on virgin fossil-based plastics while meeting circular economy targets. This opportunity positions chemical recycling not only as a compliance solution but as a strategic value chain innovation for flexible packaging.

Packaging-as-a-Service (PaaS) and Reusable Delivery Systems

The rapid growth of e-commerce in FMCG has spotlighted inefficiencies in single-use packaging, opening the door to packaging-as-a-service (PaaS) models. Here, durable containers are owned, cleaned, and redistributed by third parties, shifting packaging from a disposable cost to a reusable asset. TerraCycle’s Loop initiative, backed by major brands like Nestlé, Unilever, and Procter & Gamble, exemplifies this shift by enabling consumers to return containers for professional cleaning and reuse, much like the traditional milkman system.

The economic and environmental advantages are compelling. A lifecycle study found that reusable containers can outperform single-use packaging after just a few rotations, cutting both greenhouse gas emissions and waste. Financially, brands can amortize durable container costs over multiple trips, unlocking long-term savings. However, scalability depends on building reverse logistics and industrial cleaning infrastructure at scale. With increasing retailer and logistics investment, reusable delivery systems represent a transformative growth opportunity in FMCG packaging, particularly for high-frequency e-commerce categories such as beverages, personal care, and household essentials.

Competitive Landscape: Global Leaders Driving FMCG Packaging Innovation

The global FMCG packaging market is defined by multinational giants and specialized innovators, each shaping the industry through strategic acquisitions, R&D-driven sustainability initiatives, and expansion into high-value applications.

Amcor PLC Expanding Global Leadership Through Strategic Acquisitions

Amcor remains a front-runner in sustainable packaging, with strong portfolios in both flexible and rigid packaging. Its AmPrima™ recycle-ready portfolio and AmFiber™ high-barrier paper packaging showcase leadership in eco-innovation. In April 2025, Amcor completed its acquisition of Berry Global, creating a new global leader in consumer and healthcare packaging. By expanding its healthcare network in Costa Rica and upgrading its UK recycling plant, Amcor is aligning growth with circular economy goals.

Mondi plc Driving Circular Packaging with MAP2030 Sustainability Strategy

Mondi has positioned itself as a pioneer in sustainable-by-design FMCG packaging, guided by its MAP2030 sustainability roadmap. Its portfolio spans kraft papers, functional barrier papers, and specialty films. Mondi recently introduced Ad/Vantage Smooth Brown Semi Extensible paper and scaled production of FunctionalBarrier Paper Ultimate, a recyclable high-barrier packaging for food and consumer goods. Its forest-to-finished product integration provides strong supply chain control and quality assurance.

Smurfit Kappa Group Merger with WestRock Creates Smurfit WestRock

Smurfit Kappa is a global leader in paper-based FMCG packaging, with strong expertise in corrugated, containerboard, and retail-ready solutions. In July 2025, the company completed its merger with WestRock, forming Smurfit WestRock, a new global giant in sustainable packaging. Known for smart packaging design and its network of Experience Centres, Smurfit Kappa provides end-to-end packaging innovation tailored to e-commerce and retail channels.

International Paper Strengthening European Reach with DS Smith Acquisition

International Paper continues to be a dominant force in corrugated and paperboard packaging. In July 2025, it finalized its $9.9 billion acquisition of DS Smith, expanding its European manufacturing footprint and reinforcing its leadership in fiber-based FMCG packaging. A $250 million investment in its Riverdale mill to produce containerboard further strengthens its role in e-commerce packaging. Its strategy of divesting non-core assets, including the Global Cellulose Fibers business, reflects a sharpened focus on higher-margin packaging solutions.

Constantia Flexibles Expanding Sustainable Portfolio with Aluflexpack Acquisition

Constantia Flexibles is a leading flexible packaging producer with a strong presence in films, foils, and laminates. In July 2025, it acquired a majority stake in Aluflexpack AG, expanding its reach in high-value pharmaceutical and consumer packaging markets. With over €100 million invested in production upgrades, including a €50 million expansion of aluminum foil capacity and a new MDO line at Constantia Pirk, the company is scaling its Ecolutions portfolio of mono-material, recyclable solutions. Constantia also continues to innovate with products like ComforLid and EcoPeelCover, designed for resource efficiency and recyclability.

FMCG Packaging market Share Insights

Flexible Packaging Leads Market Share by Packaging Type in FMCG Packaging

In 2025, flexible packaging commands 55% of the FMCG packaging market, underscoring its dominance as the go-to solution for food, beverage, and personal care brands seeking cost efficiency, lightweighting, and sustainability. Formats such as pouches, bags, and multilayer films enable brand owners to reduce material consumption, cut shipping costs, and deliver strong shelf appeal with high-quality print surfaces. The rise of single-serve products and e-commerce logistics has further fueled adoption, making flexible packaging indispensable for meeting fast turnaround and diverse SKU demands. By contrast, rigid packaging retains a resilient 45% share, supported by categories where structure, durability, and premium perception remain critical. Bottles, jars, and cartons continue to dominate in beverages, cosmetics, and premium foods, where reusability, tamper resistance, and consumer familiarity ensure sustained demand. This segmentation highlights how flexible packaging accelerates through convenience and sustainability goals, while rigid packaging maintains relevance in high-value and structurally dependent categories.

Food and Beverages Dominate Market Share by End-Use in FMCG Packaging

By end-use, food products lead the FMCG packaging market with 35% share in 2025, reinforcing their role as the volume and innovation engine. From barrier pouches for snacks and frozen meals to rigid trays for produce, food applications sit at the intersection of sustainability mandates and shelf-appeal battles. Beverages follow closely at 30%, driven by PET bottles, aluminum cans, and glass containers, with Deposit Return Schemes (DRS) and recycled PET (rPET) regulations shaping material choices. Personal care and cosmetics continue to expand with premium rigid jars and refill pouches, positioning packaging as a direct extension of brand identity. Household care products increasingly adopt flexible refill systems to cut costs and reduce plastic footprints, while pharmaceuticals and healthcare remain a regulated niche where compliance and protection are non-negotiable. End-use segmentation demonstrates that food and beverage sectors anchor FMCG packaging volumes, while premiumization, refills, and compliance-driven niches sustain demand diversification.

United States: Sustainability and Smart Packaging Transforming FMCG Packaging

The U.S. FMCG packaging market is increasingly shaped by the rise of sustainable and recyclable packaging, driven by both consumer expectations and corporate ESG commitments. Major brands like PepsiCo and L’Oréal are investing in post-consumer recycled (PCR) content and designing packaging that is easily recyclable to strengthen their sustainability profiles.

Technological advancements are also redefining the market, with automation and robotics enhancing packaging line efficiency and minimizing waste. Strategic collaborations, such as Amcor and Moda Systems, focus on improving vacuum packaging efficiency, particularly in the food and beverage sector. Additionally, the e-commerce boom has fueled demand for durable, lightweight, and cost-effective packaging solutions. The integration of smart and interactive packaging technologies, including QR codes, RFID, and NFC, enables brands to offer product traceability, consumer engagement, and sustainability credentials, marking a new era of intelligent FMCG packaging.

Germany: Circular Economy and Paper-Based Innovation Driving FMCG Packaging

Germany’s FMCG packaging industry operates under the stringent German Packaging Act (VerpackG), establishing one of the strictest regulatory frameworks globally. Companies, including foreign sellers, must register packaging and participate in recycling systems, positioning Germany as a leader in recycling and waste reduction.

The market emphasizes innovation in paper-based solutions, with companies like Mondi and Veetee developing recyclable paper-based packaging for products such as dry rice. This trend is reinforced by Germany’s commitment to the circular economy, incorporating high percentages of recycled content and designing packaging for recyclability. The upcoming EU Packaging and Packaging Waste Regulation (PPWR) will further push standards, ensuring FMCG packaging continues to meet ambitious sustainability and environmental compliance goals.

China: Regulatory Push and Rising Domestic Demand Fuel FMCG Packaging Growth

China’s FMCG packaging market is undergoing significant transformation due to new regulations on packaging and labeling, aimed at controlling excessive packaging and improving food safety standards. National standards, including those for moist toilet tissue, encourage standardization and adoption of degradable materials.

Government initiatives promoting sustainability, including plastic bans and waste management regulations, are driving companies to innovate with recyclable and eco-friendly materials. For example, the adoption of Dow’s BOPE-based INNATE TF 220 resin by a Chinese detergent brand highlights material innovation supporting sustainability objectives. The market is also fueled by rising domestic demand, driven by e-commerce expansion, urbanization, and a growing middle class, creating strong opportunities for convenient, safe, and attractively packaged FMCG products.

India: Make in India Initiative and Sustainability Regulations Shaping FMCG Packaging

India’s FMCG packaging industry is benefiting from the Make in India initiative and flexible regulatory frameworks, attracting foreign direct investment and boosting local manufacturing capabilities. Rapid urbanization and the expansion of modern retail and e-commerce platforms are driving demand for lightweight, durable, and protective packaging, particularly in flexible and paper-based formats.

Government mandates, including plastic waste management rules and Extended Producer Responsibility (EPR) requirements, are further encouraging sustainable packaging adoption. The upcoming mandate for minimum 10% PCR content in flexible plastic packaging from 2025 reinforces the shift toward circular economy practices, positioning India as a growing hub for sustainable FMCG packaging innovation.

Brazil: Bioplastics and E-commerce Driving Modern FMCG Packaging

Brazil’s FMCG packaging market is at the forefront of bioplastics innovation, with companies like Braskem producing green polyethylene from sugarcane ethanol, reducing reliance on fossil fuels and supporting sustainable packaging development.

The booming e-commerce sector is a significant market driver, creating demand for lightweight, flexible, and protective packaging that minimizes shipping costs and material usage. There is also a growing focus on sustainability and recycling, with companies investing in R&D to develop recyclable packaging compatible with Brazil’s developing recycling infrastructure, reflecting an increasing commitment to environmentally responsible FMCG packaging solutions.

Japan: High-Quality and Barrier Technology Advancing Sustainable FMCG Packaging

Japan’s FMCG packaging industry is defined by its focus on high-quality, aesthetically appealing, and functional packaging to meet consumer expectations for premium products. Traditional motifs, advanced printing techniques, and innovative designs are widely employed to enhance product appeal.

Innovation in barrier technology is a key trend, with companies like Nippon Paper Industries developing products such as SHIELDPLUS, a paper with barrier properties comparable to plastics, to extend food shelf life and replace traditional plastic films. Additionally, the industry emphasizes reducing plastic waste through mono-material packaging and the use of bio-based and compostable materials, aligning with government initiatives to promote recycling and a circular economy.

FMCG Packaging Market Report Scope

FMCG Packaging market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$856.4 Billion

|

|

Market Size (2034)

|

$1434.6 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Material Type (Paper and Paperboard, Plastics, Metal, Glass, Bio-Based and Compostable Materials), By Packaging Type (Flexible Packaging, Rigid Packaging), By End-Use Industry (Food, Beverages, Personal Care and Cosmetics, Household Care Products, Pharmaceuticals and Healthcare, Other End-use Industries), By Distribution Channel (Direct Sales, Indirect Sales)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, International Paper Company, WestRock Company, Smurfit Kappa Group plc, Mondi Group, DS Smith Plc, Huhtamaki Oyj, Graphic Packaging Holding Company, Sonoco Products Company, Crown Holdings Inc., Ardagh Group S.A., Tetra Pak International S.A., Ball Corporation, BillerudKorsnäs AB, TC Transcontinental Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

FMCG Packaging Market Segmentation

By Material Type

- Paper and Paperboard

- Plastics

- Metal

- Glass

- Bio-Based and Compostable Materials

By Packaging Type

- Flexible Packaging

- Rigid Packaging

By End-Use Industry

- Food

- Beverages

- Personal Care and Cosmetics

- Household Care Products

- Pharmaceuticals and Healthcare

- Other End-use Industries

By Distribution Channel

- Direct Sales

- Indirect Sales

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in FMCG Packaging Market

- Amcor plc

- International Paper Company

- WestRock Company

- Smurfit Kappa Group plc

- Mondi Group

- DS Smith Plc

- Huhtamaki Oyj

- Graphic Packaging Holding Company

- Sonoco Products Company

- Crown Holdings Inc.

- Ardagh Group S.A.

- Tetra Pak International S.A.

- Ball Corporation

- BillerudKorsnäs AB

- TC Transcontinental Inc.

*List not Exhaustive

Research Coverage

This USDAnalytics report investigates the global FMCG packaging market, examining breakthroughs in sustainable materials, smart packaging technologies, and e-commerce-optimized designs. The analysis reviews recent mergers, innovations in mono-material and chemical recycling-compatible solutions, and the integration of digital features like QR codes, NFC tags, and AR-enabled packaging to enhance consumer engagement and regulatory compliance. The report highlights market developments such as strategic acquisitions by Amcor, Smurfit Kappa, and International Paper, alongside innovations in fiber-based, recyclable, and bio-based packaging materials. This report is an essential resource for industry professionals, brand managers, packaging engineers, and supply chain stakeholders seeking actionable insights into growth drivers, competitive positioning, and emerging opportunities. By combining historical data from 2021 to 2024 with forecasts through 2034, USDAnalytics delivers a comprehensive view of market trends, end-use dynamics, and regional growth prospects, enabling informed strategic decisions in a rapidly evolving FMCG packaging landscape.

Scope Highlights:

- Segmentation: By Material Type (Paper and Paperboard, Plastics, Metal, Glass, Bio-Based and Compostable Materials), By Packaging Type (Flexible Packaging, Rigid Packaging), By End-Use Industry (Food, Beverages, Personal Care and Cosmetics, Household Care Products, Pharmaceuticals and Healthcare, Other End-use Industries), By Distribution Channel (Direct Sales, Indirect Sales)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa

- Timeframe: Historical data from 2021 to 2024; forecast data from 2025 to 2034

- Companies: Profiles and analysis of 15+ key manufacturers including Amcor, International Paper, Smurfit Kappa, Mondi, DS Smith, Huhtamaki, Graphic Packaging Holding, Sonoco, Crown Holdings, Ardagh Group, Tetra Pak, Ball Corporation, BillerudKorsnäs, and TC Transcontinental

Methodology

This study applies a robust research methodology combining primary interviews, expert consultations, and secondary data analysis to ensure precise market insights. USDAnalytics conducted discussions with packaging professionals, brand managers, regulatory bodies, and material scientists to understand sustainability initiatives, digital integration, and e-commerce packaging challenges. Secondary sources, including corporate filings, trade publications, regulatory databases, and prior market reports, were examined to capture historical trends and forecast future developments. Top-down and bottom-up approaches were utilized to quantify market size across material types, packaging formats, end-use industries, and distribution channels. Additionally, competitive benchmarking, market trend validation, and scenario modeling were employed to assess the impact of regulatory mandates, technological innovations, and consumer preferences on market dynamics. The methodology ensures data accuracy, relevance, and actionable insights for FMCG brand strategists, packaging engineers, and supply chain decision-makers.

Deliverables:

• Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

• Country-Specific Forecasts & Analysis.

• Segment-Wise Revenue Forecasts (2025–2034).

• Competitive Analysis, Benchmarking, and SWOT Profiles.

• Recent Developments & Innovation Tracker.

• Executive Summary & Analyst Commentary.

• Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.