Vacuum Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Vacuum Packaging Market Expected to Reach $14.6 Billion by 2034 Amid Rising Demand for Shelf Life Extension and Food Safety

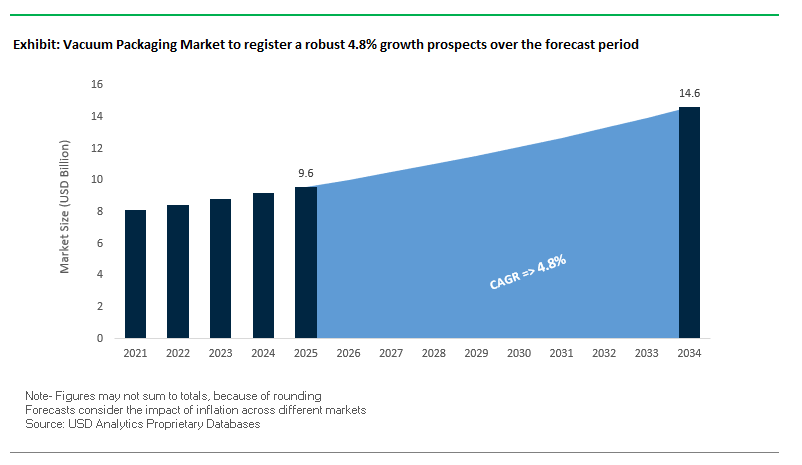

The global vacuum packaging market is projected to grow from $9.6 billion in 2025 to $14.6 billion by 2034, at a CAGR of 4.8%. Vacuum packaging, which removes air from a package before sealing, is critical for preserving perishable products, preventing microbial growth, and maintaining product integrity. While widely used in food and beverages, this technology also serves pharmaceuticals, electronics, and industrial goods, where protection against spoilage and contamination is essential.

Key Insights for industry professionals and buyers:

- High-performance barrier materials such as Nylon/EVOH liners enhance oxygen and moisture resistance, extending shelf life.

- Sustainable packaging trends are gaining momentum, including mono-material films, recyclable, and compostable solutions.

- Automation and smart packaging technologies, integrating AI and IoT, enable predictive maintenance, real-time monitoring, and multi-functional production lines.

- Customization and versatility are increasingly important, with innovations such as resealable pouches, easy-open features, and on-demand printing enhancing consumer experience.

- Growing regulatory and consumer emphasis on sustainability drives adoption of eco-friendly solutions in food, medical, and industrial sectors.

Market Analysis: Recent Developments Showcase Sustainability, Smart Packaging, and Material Innovation Driving Industry Growth

The vacuum packaging industry is witnessing rapid advancements in technology, sustainability, and operational efficiency. In August 2025, Klöckner Pentaplast received a German Packaging Award for its kp 100% Tray2Tray® innovation, reinforcing its focus on sustainable packaging. That same month, Coveris completed an $11 million upgrade to its German facility, adding a cast film extrusion line and next-generation printing press to meet advanced customer demands.

In July 2025, Klöckner Pentaplast introduced kp Elite® Nova, the lightest modified atmosphere packaging tray in its class, while a study on carrageenan-polyoxometalate antimicrobial films highlighted strong bactericidal properties and excellent biodegradability.

Earlier strategic moves include Amcor’s Moda Bag system showcased in September 2024, enabling on-demand vacuum bag making for meat and cheese, significantly reducing material and labor costs. Condor Expedite launched a reusable cold chain division in May 2024, allowing pallets to be refrigerated for up to nine days without dry ice. October 2024 collaborations by Newwen and Parrdekopper introduced reusable transport packaging with integrated RFID/QR tracking, emphasizing traceability, efficiency, and sustainability.

Trends and Opportunities Defining the Future of the Vacuum Packaging Market

Strategic Shift Towards Ready-to-Use (RTU) Vials and Pre-Fillable Syringes

The vacuum packaging market is undergoing a structural shift driven by the healthcare sector’s adoption of ready-to-use (RTU) vials and pre-fillable syringes. These formats address one of the most pressing issues in pharmaceutical and clinical operations—medication preparation errors. According to FDA insights on pre-filled syringes, pre-measured unit doses “eliminate the human error involved in manual dose preparation” at the point of care, significantly reducing risks for high-value and high-risk drugs.

The transition also improves clinical workflow efficiency. Amneal Pharmaceuticals’ FDA approval in July 2024 for an RTU intravenous infusion bag demonstrated how such products reduce compounding steps, cutting down preparation time and minimizing contamination risks. For hospitals under pressure to increase throughput, RTU packaging eliminates redundant preparation processes, allowing staff to focus more on patient care.

The relevance of RTU packaging was further emphasized during the COVID-19 mass vaccination campaigns, where pre-fillable syringes accelerated administration by removing the need for on-site dose preparation. By reducing wastage and ensuring faster delivery, this trend has permanently reshaped how vaccines and biologics are packaged and distributed under vacuum-sealed sterile environments.

Enhanced Focus on Ultra-Low Temperature (ULT) Packaging and Monitoring

Another defining trend in the vacuum packaging market is the development of solutions designed to meet ultra-low temperature (ULT) requirements. mRNA vaccines and advanced biologics demand storage at temperatures as low as -80°C, requiring packaging with enhanced thermal insulation and mechanical resilience. Studies confirm that even minor temperature variations can compromise vaccine efficacy, underscoring the importance of robust vacuum-sealed ULT packaging systems.

To maintain product stability, manufacturers are integrating IoT-enabled monitoring devices and data loggers directly into shipping containers and primary packaging. The European Journal of Medical Research highlights how these solutions enable continuous temperature tracking, improving accountability across supply chains and ensuring regulatory compliance.

Global distribution challenges, particularly in emerging markets, are also pushing innovation in dry ice–based insulated containers. By extending dry ice retention from hours to several days, these systems enable last-mile delivery in resource-limited settings, ensuring reliable access to life-saving vaccines in remote regions.

Development of Sustainable and Low-Carbon Footprint Primary Packaging

Sustainability is an emerging opportunity for the vacuum packaging market, especially in vaccine packaging applications where billions of single-use containers are consumed globally. Traditional formats such as glass vials and plastic syringes contribute heavily to landfill waste and carbon emissions. Researchers are actively exploring alternatives like bioplastics and recyclable paper-based materials that reduce environmental impact without compromising sterility.

A pharmaceutical pilot project in the U.S. demonstrated the potential of circular economy initiatives, where 60% of vaccine packaging was collected and returned for recycling through specialized partnerships. This model shows how closed-loop programs can help mitigate waste and support ESG-driven corporate strategies.

Sustainability innovation also extends to the manufacturing process. Technologies such as effervescent vaccine tablets, which replace freeze-dried pellets in glass vials, have shown a 70% reduction in water footprint and an 80% reduction in climate change impact. Such breakthroughs highlight how rethinking both materials and processes can deliver lower-carbon packaging solutions for the pharmaceutical sector.

Integration of Digital End-to-End Traceability and Anti-Counterfeiting

The rise in global counterfeit vaccines and pharmaceuticals has accelerated demand for digital traceability solutions integrated into vacuum packaging. Regulations such as the U.S. Drug Supply Chain Security Act (DSCSA) and the EU Falsified Medicines Directive (FMD) require serialization, 2D barcodes, and tamper-evident features to secure supply chains.

Counterfeit risk remains a global challenge, with the Pharmaceutical Security Institute (PSI) recording over 6,400 incidents of counterfeit drugs in 2024. To combat this, manufacturers are embedding serialized RFID tags and QR codes within vacuum packaging. These features enable pharmacists and patients to verify authenticity in real-time, significantly reducing illicit trade.

Competitive Landscape: Leading Vacuum Packaging Companies Are Driving Innovation Through Sustainability and Smart Solutions

The vacuum packaging market is shaped by companies leveraging advanced materials, automation, and sustainable design to deliver high-performance solutions for food, medical, and industrial applications.

Amcor plc: Pioneering Circular Economy Solutions with Recyclable Vacuum Packaging

Amcor offers flexible and rigid packaging, including AmPrima® recycle-ready pouches and the Moda Bag system. In August 2025, the company upgraded its UK recycling facility to enhance post-consumer content use. Amcor’s vertically integrated network and R&D in PVC-free, aluminum-free solutions underline its commitment to sustainability and operational efficiency.

Sealed Air Corporation: Enhancing Freshness and E-Commerce Efficiency with CRYOVAC® Solutions

Sealed Air provides CRYOVAC® vacuum packaging for food safety and recyclability. Its solutions include the Jiffy® Embossed Mailer, a curbside-recyclable packaging optimized for e-commerce. The company focuses on reducing waste, optimizing supply chains, and providing innovative protective solutions across global markets.

Coveris Holdings S.A.: Driving Sustainability with Mono-Material Vacuum Films

Coveris delivers sustainable vacuum packaging films, including mono-material and recyclable solutions. In August 2025, the company completed an $11 million upgrade of its German facility, enhancing production capabilities. Its No Waste strategy emphasizes innovative, eco-friendly packaging for food, consumer goods, and medical applications.

Klöckner Pentaplast Group: Leading Lightweight and Modified Atmosphere Packaging Innovations

Klöckner Pentaplast specializes in rigid and flexible films for vacuum and specialty packaging. Awarded the German Packaging Award in August 2025 for kp 100% Tray2Tray®, the company continues to expand globally, focusing on sustainable, high-performance solutions across food and pharmaceuticals.

Wipak Group: Advancing Flexible Vacuum Packaging Towards a Zero-Carbon Future

Wipak provides FlexPod™ vacuum packaging for food and medical sectors. In September 2024, the company made multi-million-euro investments to achieve a zero-carbon organization by 2025. Wipak emphasizes sustainability, material innovation, and high-quality, compliant solutions across its global operations.

Vacuum Packaging Market Share Insights, 2025-2034

Bags & Pouches Dominate Market Share by Product Type in the Vacuum Packaging Industry

Bags and pouches account for around 55% of the vacuum packaging market, cementing their role as the most versatile and widely used product format. Their dominance stems from their adaptability to an extensive range of products, from fresh meat, cheese, and processed foods to industrial and consumer goods. These formats are typically made from multi-layer laminates with nylon and EVOH, which deliver strong oxygen and moisture barriers, critical for extending shelf life and preventing spoilage. In addition, vacuum pouches offer efficient material utilization, lightweight logistics advantages, and compatibility with automated packaging machinery, making them cost-efficient for high-volume production. Sustainability efforts are further reinforcing this segment’s leadership, with manufacturers developing recyclable and bio-based barrier films to meet regulatory pressures and corporate sustainability targets.

Food & Beverages Hold the Overwhelming Share by Application in the Vacuum Packaging Industry

The food and beverages sector commands nearly 75% of the vacuum packaging market, underscoring the alignment between vacuum sealing technology and global food preservation needs. By removing oxygen and preventing microbial growth, vacuum packaging significantly extends the shelf life of perishable goods while maintaining taste, texture, and freshness—benefits essential for meat, dairy, seafood, coffee, dried foods, and ready-to-eat meals. The rising consumer demand for convenience foods, combined with global efforts to reduce food waste and optimize cold chain logistics, reinforces this segment’s dominance. Regulatory compliance with food safety standards and the shift toward sustainable, recyclable packaging materials also amplify the importance of vacuum packaging in this sector, ensuring it remains the largest and most resilient application.

European Union: PPWR Regulations and EPR Mandates Shaping Vacuum Packaging

The European Union vacuum packaging market is undergoing a rapid transformation due to the Packaging and Packaging Waste Regulation (PPWR), which became effective in February 2025. This regulation mandates that packaging producers prioritize recyclability and reusability, pushing companies to redesign vacuum films and trays using recyclable mono-materials and compostable alternatives. The EU’s Horizon Europe funding is channeling significant resources toward the R&D of bio-based vacuum packaging films, including starch blends and cellulose-based structures. These efforts align with the bloc’s wider goal of achieving a circular economy by 2030.

A landmark policy shift is set for October 1, 2025, when Denmark introduces Extended Producer Responsibility (EPR) for packaging. This requires manufacturers to prove recyclability and support post-consumer waste recovery systems. The European Food Safety Authority (EFSA) is also pivotal in shaping this market by rigorously evaluating materials used in vacuum packaging for food safety compliance. Industry activity remains strong—Proseal, a JBT Corporation company, reached a milestone in January 2025 with the installation of its 8000th tray sealing machine at Bakkavor Group, highlighting the scale of automation in prepared food packaging across the EU.

United States: IoT-Integrated Machinery and Mono-Material Packaging Demand

The U.S. vacuum packaging market is driven by regulatory oversight and technological innovation. The Environmental Protection Agency (EPA) continues to promote recycling initiatives, spurring companies to adopt sustainable and recyclable packaging solutions. A major growth driver comes from e-commerce and meal kit delivery services, where vacuum-sealed trays and pouches are essential for maintaining freshness and preventing contamination during last-mile delivery.

Manufacturers are increasingly investing in IoT-enabled vacuum packaging machinery that offers real-time monitoring of temperature and seal integrity—a critical need in pharmaceutical, meat, and ready-to-eat food sectors. Simultaneously, companies are developing mono-material vacuum films that provide high oxygen and moisture barriers while improving recyclability. Advocacy groups like the American Institute for Packaging and the Environment (AMERIPEN) are accelerating the adoption of such technologies, ensuring sustainability standards remain at the forefront of packaging innovation.

China: Stricter Food Contact Standards and Smart Packaging Expansion

The China vacuum packaging market is being reshaped by the government’s 14th Five-Year Plan, which prioritizes eco-friendly, reduced, and reusable packaging to address plastic pollution. Effective June 1, 2025, new regulations mandate express delivery companies to adopt sustainable packaging, creating ripple effects across the e-commerce-driven vacuum packaging sector. Furthermore, tax incentives for green technologies are encouraging domestic manufacturers to scale innovation in sustainable vacuum films and machinery.

The State Administration for Market Regulation (SAMR) has introduced new GB 4806.1 standards for food contact materials, raising the bar for compliance by requiring complete barrier properties and improved safety. Domestic machinery players are focusing on compact, versatile vacuum sealers capable of processing diverse substrates, meeting the needs of both food and pharmaceutical sectors. With a growing demand for advanced barrier properties and anti-counterfeit features, China is emerging as a key hub for technologically advanced vacuum packaging solutions.

India: EPR, FSSAI Guidelines, and BIS Certification Boosting Standards

The India vacuum packaging market is advancing under the Plastic Waste Management (Amendment) Rules, 2024, which came into effect in April 2025. These rules impose Extended Producer Responsibility (EPR) obligations on producers, importers, and brand owners, requiring robust recycling and waste recovery systems. From July 1, 2025, all plastic packaging—including vacuum packs—must carry barcodes or QR codes to enhance traceability and accountability.

The Food Safety and Standards Authority of India (FSSAI) introduced the Packaging First Amendment Regulations, 2025, approving the use of recycled PET (rPET) in food packaging, aligning domestic practices with global benchmarks. Additionally, the Bureau of Indian Standards (BIS) made it mandatory for commercial vacuum packaging appliances to meet IS 302 Part 1:2024 certification, ensuring product safety and reliability. These regulations, coupled with India’s booming retail and e-commerce sector, are creating strong demand for eco-friendly, traceable, and high-performance vacuum packaging solutions.

Japan: Circular Economy Policies and Industry 4.0 Integration

The Japan vacuum packaging market is driven by the government’s Plastic Resource Circulation Strategy, which requires all packaging to be reusable or recyclable by 2025. The Plastic Resource Circulation Promotion Law, effective the same year, mandates the reduction and redesign of 12 single-use plastic categories, accelerating the adoption of compostable and paper-based alternatives. The Ministry of Health, Labor and Welfare (MHLW) further reinforces safety by implementing a positive list for synthetic food contact materials effective June 2025.

Japan’s machinery market is at the forefront of Industry 4.0 adoption, with robotics, AI, and smart sensors being integrated into vacuum packaging lines. This ensures improved efficiency, reduced labor costs, and consistent quality, particularly in the country’s robust processed food and pharmaceutical industries. The combination of circular economy mandates and technological innovation positions Japan as a leader in sustainable and intelligent vacuum packaging systems.

Brazil: PNRS Regulations and Reverse Logistics Driving Sustainability

The Brazil vacuum packaging market is shaped by the National Solid Waste Policy (PNRS), which mandates reuse, recycling, and responsible waste disposal. This policy is compelling packaging producers to adopt eco-friendly vacuum packaging materials and support recycling infrastructure. Furthermore, the government is actively investing in reverse logistics systems, holding producers accountable for post-consumer recycling and disposal.

With growing consumer awareness and stricter regulatory oversight, Brazilian companies are prioritizing sustainable, recyclable vacuum packaging films. The country’s strong agricultural and food export industry further drives the need for durable, compliant vacuum packaging that ensures both freshness and environmental responsibility. These initiatives are positioning Brazil as a key Latin American market advancing toward a circular economy in vacuum packaging.

Vacuum Packaging Market Report Scope

Vacuum Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.6 Billion

|

|

Market Size (2034)

|

$14.6 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Product Type (Films, Bags & Pouches, Trays, Other Product Types), By Technology (Skin, Shrink, Gas Flush, MAP), By Material (Plastics, Paper & Paperboard, Aluminum Foil, Glass, Other Materials), By Application (Food & Beverages, Healthcare & Pharmaceuticals, Electronics, Industrial Goods, Consumer Goods), By Packaging Type (Flexible, Semi-Rigid, Rigid)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Sealed Air Corporation, MULTIVAC Sepp Haggenmüller SE & Co. KG, Coveris Holdings S.A., Winpak Ltd., Klöckner Pentaplast, ProAmpac, JBT Corporation (Proseal), ULMA Packaging, S. Coop., Henkelman, Italian Pack S.r.l., V.S. Engineering Ltd. (Vebomatic), Ossid, LLC, Sealed Air Corporation, Berry Global, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Vacuum Packaging Market Segmentation

By Product Type

- Films

- Bags & Pouches

- Trays

- Other Product Types

By Technology

- Skin

- Shrink

- Gas Flush

- MAP

By Material

- Plastics

- Paper & Paperboard

- Aluminum Foil

- Glass

- Other Materials

By Application

- Food & Beverages

- Healthcare & Pharmaceuticals

- Electronics

- Industrial Goods

- Consumer Goods

By Packaging Type

- Flexible

- Semi-Rigid

- Rigid

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Vacuum Packaging Market

- Amcor plc

- Sealed Air Corporation

- MULTIVAC Sepp Haggenmüller SE & Co. KG

- Coveris Holdings S.A.

- Winpak Ltd.

- Klöckner Pentaplast

- ProAmpac

- JBT Corporation (Proseal)

- ULMA Packaging, S. Coop.

- Henkelman

- Italian Pack S.r.l.

- V.S. Engineering Ltd. (Vebomatic)

- Ossid, LLC

- Sealed Air Corporation

- Berry Global, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a rigorous, multi-dimensional research methodology to assess the global vacuum packaging market, integrating primary insights from manufacturers, suppliers, technology providers, and regulatory authorities with secondary data from corporate filings, industry reports, and scientific publications. Our analysis focuses on market drivers such as shelf-life extension, food safety, cold chain requirements, and sustainable packaging trends, including mono-material films, recyclable pouches, and compostable solutions. We examine technological advancements, including IoT-enabled machinery, automation, smart packaging, and ultra-low temperature (ULT) solutions, alongside innovations in barrier materials like Nylon/EVOH liners. Regional coverage spans North America, Europe, Asia-Pacific, China, India, Japan, and Latin America, providing in-depth insights on regulatory compliance, EPR mandates, and local market dynamics. USDAnalytics also provides granular segmentation by product type, technology, material, application, and packaging format, highlighting growth opportunities for stakeholders across food, pharmaceutical, electronics, and industrial sectors, while analyzing strategic investments, sustainability initiatives, and competitive developments shaping the future of vacuum packaging globally.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.