Vaccine Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Vaccine Packaging Market to Reach $5.9 Billion by 2034 Driven by Cold Chain Innovation and Patient Safety Solutions

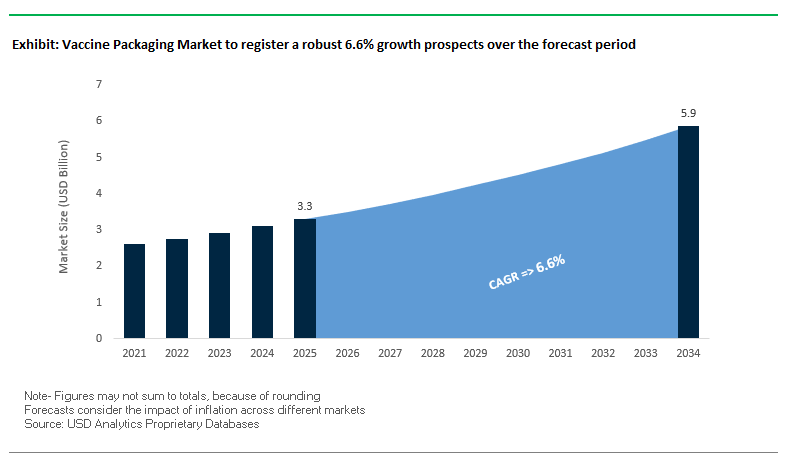

The global vaccine packaging market is projected to grow from $3.3 billion in 2025 to $5.9 billion by 2034, at a steady CAGR of 6.6%. This specialized market is central to public health, ensuring that life-saving vaccines are delivered safely and efficiently. Packaging formats including vials, pre-filled syringes, and ampoules provide sterile, tamper-evident containers, maintaining efficacy from manufacturing to administration.

Key Insights for industry professionals and buyers:

- Cold chain integrity and ultra-cold storage innovations are essential for mRNA vaccines and other temperature-sensitive immunizations.

- Advanced traceability and anti-counterfeiting features, such as QR codes, holograms, and serialized barcodes, safeguard vaccine authenticity.

- Sustainable packaging trends include mono-material solutions, bio-based plastics, and plant-sourced materials to reduce environmental impact.

- Pre-filled syringes and auto-disable devices improve patient safety, minimize needle-stick injuries, and enhance workflow efficiency.

- Market growth is supported by global vaccination campaigns, regulatory compliance, and rising demand in developing countries.

Market Analysis: Industry Dynamics Highlight Technological Innovation, Sustainability, and Strategic Investments

The vaccine packaging industry is evolving rapidly, driven by technological advancements, sustainability, and global health initiatives. In August 2025, Amcor upgraded its UK recycling facility, supporting post-consumer recycled content in its flexible packaging portfolio. That same month, a study introduced a composite antimicrobial film from carrageenan and polyoxometalate, demonstrating strong bactericidal activity and rapid biodegradability, highlighting eco-conscious innovation.

In July 2025, Alvotech expanded its assembly and packaging capacity through the acquisition of Ivers-Lee in Switzerland, enhancing its capabilities in biotech vaccine packaging. UNICEF also delivered its first vaccine shipment by sea, transporting over 500,000 doses of pneumococcal vaccines, reducing greenhouse gas emissions and freight costs. Johnson & Johnson Innovation launched the Pitching Respiratory Innovation QuickFire Challenge to encourage novel packaging solutions for respiratory illnesses, emphasizing safety and convenience.

Earlier developments include PCI Pharma Services acquiring Ajinomoto Althea in April 2025, giving the company its first North American sterile fill-finish facility for pre-filled syringes. In October 2024, Nipro PharmaPackaging launched D2F glass vials with Stevanato Group’s EZ-fill technology, while SCHOTT Pharma introduced EVERIC freeze vials in January 2024, designed for ultra-cold storage of mRNA vaccines.

Trends and Opportunities Shaping the Vaccine Packaging Market

Strategic Shift Towards Ready-to-Use (RTU) Vials and Pre-Fillable Syringes

The vaccine packaging market is undergoing a major transition with the adoption of ready-to-use (RTU) vials and pre-fillable syringes. These solutions reduce the need for washing, sterilization, and preparation steps, ensuring safer handling and faster administration in clinical and commercial settings. According to Apotek Produktion & Laboratorier (APL), pre-filled syringes significantly lower the risk of piercing injuries and accidental toxic exposure, while also ensuring accurate dosing that minimizes medication errors.

Another critical driver is cost and waste reduction. Traditional vials require a 20–30% overfill to account for preparation waste, whereas pre-filled syringes eliminate this requirement, reducing losses in high-value biological vaccines. This is particularly important for mRNA-based vaccines and other biologics where the active ingredients are costly to manufacture.

The RTU format also enhances production agility. By relying on pre-sterilized components, manufacturers can simplify their fill-finish operations, eliminating the need for dedicated sterilization lines and accelerating time-to-market. This trend is especially beneficial for clinical trials, where speed and flexibility are essential.

Enhanced Focus on Ultra-Low Temperature (ULT) Packaging and Monitoring

The emergence of mRNA vaccines has reshaped cold chain requirements, demanding storage and transport at -60°C to -80°C. Companies like Cryoport have developed advanced ULT shipping systems that combine dry ice with vacuum insulation technology, ensuring reliable protection of biologics under extreme conditions.

At the same time, real-time monitoring technologies are being embedded into vaccine packaging. RFID tags, IoT sensors, and temperature loggers provide continuous visibility of cold chain conditions, alerting supply chain managers when shipments approach temperature thresholds. A white paper on RFID solutions notes that these systems enhance regulatory compliance and enable immediate interventions to prevent product spoilage.

The WHO and UNICEF have endorsed the use of integrated monitoring devices to safeguard vaccine integrity globally. Beyond pandemic-related supply chains, these smart packaging solutions are being adopted for other biologics, building a resilient infrastructure for future pandemics and high-value therapies.

Development of Sustainable and Low-Carbon Footprint Primary Packaging

With sustainability becoming a key corporate and regulatory priority, the vaccine packaging industry is exploring innovations in eco-friendly materials. According to Pfizer’s sustainability report, the company is actively working with suppliers to integrate recycled content into its packaging and optimize packaging designs for lower carbon emissions.

Traditional formats like glass vials and PVC-based blister packs contribute heavily to environmental impact. Research into mono-material polyethylene (PE) and polypropylene (PP) solutions offers an alternative, simplifying recyclability without compromising protection. Additionally, bio-based plastics derived from corn and sugarcane are being tested as potential biodegradable options for pharmaceutical applications.

This shift aligns with the EU Circular Economy Action Plan and global carbon neutrality targets, creating a strong opportunity for suppliers who can develop validated, recyclable, and bio-based primary packaging tailored to the stringent requirements of biologics.

Integration of Digital End-to-End Traceability and Anti-Counterfeiting

The global counterfeit medicines market, estimated at over $30 billion annually, underscores the importance of secure vaccine packaging. Regulatory frameworks such as the U.S. DSCSA and international GS1 standards mandate serialization and unique identifiers on unit-level packaging. UNICEF’s pilot systems in Rwanda and Nigeria demonstrate how GS1 barcodes enable healthcare workers to verify vaccine authenticity using simple mobile apps.

Beyond barcoding, companies are experimenting with blockchain-based traceability systems. Blockchain provides an immutable digital ledger of a vaccine’s journey from production to administration, offering full transparency for regulators, distributors, and patients.

At the operational level, serialization and RFID integration are enhancing inventory management and recall efficiency. With serialized codes, recalls can be targeted to specific batches, reducing disruption and costs. These technologies also improve supply chain security, helping manufacturers detect diversion and ensuring that vaccines reach their intended destinations without tampering.

Competitive Landscape: Leading Players Drive Innovation and Sustainability Across the Global Vaccine Packaging Industry

The vaccine packaging market is shaped by companies leveraging expertise in glass, plastics, and drug delivery systems to provide high-performance, compliant, and sustainable solutions for vaccines and biotech applications.

Gerresheimer AG: Expanding Global Capabilities in High-Precision Pharmaceutical Packaging

Gerresheimer produces glass vials, ampoules, and prefillable syringes with a focus on pharmaceutical and biotech applications. Under its Ambition 2028 strategic plan, the company invests in innovative materials and technologies, ensuring compliance and global reach. Its vertically integrated manufacturing network allows efficient supply of high-quality, sterile vaccine packaging solutions.

SCHOTT Pharma: Pioneering Ultra-Cold Glass Vials for mRNA and Gene Therapies

SCHOTT Pharma offers vials, cartridges, and syringes made from high-quality pharmaceutical glass. In January 2024, it launched EVERIC freeze vials for deep-cold storage of mRNA vaccines and gene therapies. The company is expanding its North Carolina facility to meet rising demand while maintaining sustainability and compliance standards.

Becton, Dickinson and Company (BD): Delivering Pre-Filled Syringe Systems with Circular Economy Focus

BD manufactures pre-filled syringes, vial systems, and drug delivery devices. Its BD Way strategic plan emphasizes environmental footprint reduction, innovation, and sustainability. BD leverages a vertically integrated model to meet global pharmaceutical market demands efficiently.

West Pharmaceutical Services, Inc.: Advancing Injectable Components with Sustainability and Safety

West specializes in stoppers, seals, and drug delivery components for vials and syringes. Through its West Way strategic plan, the company invests in new materials and sustainable technologies, expanding its global manufacturing presence while ensuring high-quality, compliant, and safe vaccine packaging solutions.

Stevanato Group: Innovating Direct-to-Fill Glass Vials for Scalable Vaccine Delivery

Stevanato Group provides glass vials, cartridges, and syringes for pharmaceutical and biotech industries. In October 2024, Nipro PharmaPackaging launched D2F glass vials using EZ-fill technology. The company focuses on sustainability, advanced manufacturing, and vertically integrated solutions, supporting scalable and compliant vaccine packaging globally.

Vaccine Packaging Market Share Insights, 2025-2034

Vials Dominate Market Share by Product Type in the Vaccine Packaging Industry

Vials account for approximately 50% of the vaccine packaging industry, establishing themselves as the unchallenged workhorse of global immunization supply chains. Manufactured primarily from borosilicate glass or advanced polymers like cyclic olefin copolymer (COC), vials provide unmatched barrier properties, chemical resistance, and compatibility with ultra-cold chain storage—a non-negotiable requirement for mRNA and other temperature-sensitive vaccines. Their dominance is reinforced by established filling and sealing infrastructure, scalability for billions of doses, and proven reliability in maintaining sterility. With ongoing global immunization programs and emerging pandemic preparedness strategies, vials remain the backbone of vaccine packaging, balancing performance, cost-effectiveness, and compliance with WHO and GMP standards.

Pharmaceuticals & Biotechnology Control the Majority Market Share by End-Use in the Vaccine Packaging Industry

Pharmaceuticals and biotechnology companies hold nearly 70% of the vaccine packaging market, reflecting their pivotal role as the developers, manufacturers, and fillers of vaccine doses worldwide. Their dominance is tied to the sheer scale of production, stringent technical requirements for sterility and stability, and the critical need for packaging formats that support high-throughput filling lines while ensuring global cold chain compliance. Beyond traditional glass vials, these companies are also driving adoption of pre-filled syringes, cyclic olefin containers, and advanced barrier technologies to support next-generation vaccines. Their commanding market share is reinforced by sustained investments in R&D, strategic partnerships with packaging suppliers, and their central role in meeting both commercial demand and government-backed immunization initiatives.

United States: FDA Regulations and Innovation in Vaccine Packaging

The United States vaccine packaging market is heavily influenced by FDA regulations, which mandate tamper-evident, traceable, and secure pharmaceutical packaging to ensure patient safety. The Drug Supply Chain Security Act (DSCSA) and FDA guidelines have accelerated the use of unit dose formats, RFID-enabled systems, and 2D barcodes in vaccine packaging. Hospitals and long-term care facilities are increasingly adopting these solutions to minimize medication errors, a trend also supported by the American Society of Health-System Pharmacists (ASHP).

Technological investments are driving significant change, particularly in pre-filled syringes and blister packs that support personalized medicine. In March 2024, SCHOTT Pharma announced a $371 million investment in Wilson, North Carolina, to establish a facility dedicated to producing prefillable polymer and glass syringes, including those for mRNA vaccines. The rise of e-pharmacy networks is also boosting demand for secure, portable unit dose packaging that protects integrity during distribution. Additionally, smart labels with QR codes are gaining traction, enabling dose verification, patient education, and improved adherence—making the U.S. a hub for high-tech vaccine packaging innovation.

European Union: PPWR, EMA Guidelines, and Advanced Cold Chain Packaging

The European Union vaccine packaging market is undergoing transformation due to the Packaging and Packaging Waste Regulation (PPWR), which took effect in February 2025. This regulation enforces a circular economy model, requiring recyclable and reusable materials for pharmaceutical packaging, including vaccine formats. The European Medicines Agency (EMA) has made serialization and anti-counterfeiting features mandatory, particularly for biologics and vaccines, while the GDP guidelines demand a validated cold chain to prevent temperature excursions.

In March 2025, the EMA published a draft guideline specifically addressing mRNA vaccine packaging requirements, which is expected to reshape container and labeling practices. Companies are already innovating to meet these needs: in October 2024, Nipro PharmaPackaging introduced D2F (Direct-to-Fill) glass vials, designed to enhance efficiency and safety in biologics packaging. Combined with demographic pressures such as an aging population and growing chronic disease prevalence, the EU market is experiencing rising demand for single-dose and multi-dose vaccine packs that balance safety, sustainability, and usability.

China: Stringent NMPA Oversight and Green Packaging Transition

The China vaccine packaging market is shaped by tightening regulations under the State Administration for Market Regulation (SAMR) and the National Medical Products Administration (NMPA). The new Pharmaceutical Packaging Materials Annex to the GMP, issued in June 2025, establishes stricter safety and compliance standards. China also enforces a vaccine lot release system, requiring mandatory batch inspections before products are distributed or imported—making traceable and tamper-proof packaging critical.

At the same time, the government’s “carbon neutrality” pledge is pushing adoption of biopolymer-based and recyclable packaging formats, including for unit dose vaccine packs. Domestic biologics and generics manufacturers are scaling up production, driving strong demand for high-quality, internationally compliant packaging solutions. This regulatory tightening, combined with China’s growing role in cross-border pharma trade, positions the country as both a large consumer and increasingly sophisticated producer of vaccine packaging.

India: Digital Vaccine Monitoring and EPR-Compliant Packaging

The India vaccine packaging market is being transformed by digital health and sustainability initiatives. The Electronic Vaccine Intelligence Network (eVIN) has successfully digitized vaccine stock and cold chain monitoring, achieving a 99% availability rate, and is now setting expectations for real-time traceability in packaging. In parallel, the Plastic Waste Management (Amendment) Rules, 2024 and Extended Producer Responsibility (EPR) mandates (effective April 2025) require producers and brand owners to adopt traceable, recyclable materials. From July 2025, all plastic vaccine packaging must include barcodes or QR codes for accountability.

The Food Safety and Standards Authority of India (FSSAI) is also contributing by enhancing packaging safety guidelines, boosting the adoption of secure, tamper-evident unit dose formats for vaccines and biologics. With India’s rapidly growing e-commerce and retail healthcare markets, the focus is expanding beyond public immunization campaigns to sustainable, digitally traceable vaccine packaging that ensures both safety and supply chain integrity.

Japan: High-Performance Vaccine Packaging for an Aging Population

The Japan vaccine packaging market reflects the country’s dual priorities: addressing its aging population and advancing circular economy goals. The Plastic Resource Circulation Strategy (2025) and the Plastic Resource Circulation Promotion Law mandate the redesign of single-use packaging into reusable or compostable alternatives, influencing vaccine vial and blister pack design. Meanwhile, the Ministry of Health, Labor and Welfare (MHLW) has introduced a positive list system (June 2025) to regulate which materials are considered safe for food and pharmaceutical packaging.

Japanese manufacturers such as Nipro Corporation are leading with innovations in high-quality glass vials and ampoules, catering to both traditional vaccines and next-generation biologics. Packaging solutions are increasingly designed to improve adherence among elderly patients, with formats that are easy to open, lightweight, and secure. This combination of regulatory rigor and demographic demand positions Japan as a leader in specialized vaccine packaging for advanced healthcare needs.

Brazil: Public Immunization Programs and Digital Packaging Innovations

The Brazil vaccine packaging market is strongly influenced by public health policies and sustainability regulations. The National Solid Waste Policy (PNRS) emphasizes recycling, reuse, and environmentally responsible packaging, while the Brazilian Health Regulatory Agency (Anvisa) introduced RDC 885 in July 2024 to pilot digital package leaflets with QR codes. This initiative modernizes vaccine packaging by reducing paper waste and enhancing digital access to medical information.

Brazil’s extensive immunization campaigns and public health programs require a robust cold chain supported by reliable packaging formats such as multi-dose vials, pre-filled syringes, and tamper-evident containers. Growing collaboration with international pharma players and regional suppliers is further improving vaccine packaging infrastructure. With sustainability and digital integration converging, Brazil is emerging as a Latin American hub for innovative and eco-friendly vaccine packaging solutions.

Vaccine Packaging Market Report Scope

Vaccine Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.3 Billion

|

|

Market Size (2034)

|

$5.9 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Product Type (Vials, Ampoules & Cartridges, Syringes, Blister Packs, Bags & Pouches), By Material (Glass, Plastics, Paper & Paperboard, Metals), By Application (Human Vaccines, Veterinary Vaccines), By End-Use Industry (Pharmaceuticals & Biotechnology, Hospitals & Clinics, Research & Development, Government Agencies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Gerresheimer AG, West Pharmaceutical Services, Inc., Nipro Corporation, SCHOTT AG, SGD Pharma, Amcor plc, AptarGroup, Inc., Stevanato Group, Becton, Dickinson & Co., Corning Incorporated, Tekni-Plex, Inc., DWK Life Sciences, Nelipak Healthcare Packaging, Datwyler Holding Inc., Catalent Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Vaccine Packaging Market Segmentation

By Product Type

- Vials

- Ampoules & Cartridges

- Syringes

- Blister Packs

- Bags & Pouches

By Material

- Glass

- Plastics

- Paper & Paperboard

- Metals

By Application

- Human Vaccines

- Veterinary Vaccines

By End-Use Industry

- Pharmaceuticals & Biotechnology

- Hospitals & Clinics

- Research & Development

- Government Agencies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Vaccine Packaging Market

- Gerresheimer AG

- West Pharmaceutical Services, Inc.

- Nipro Corporation

- SCHOTT AG

- SGD Pharma

- Amcor plc

- AptarGroup, Inc.

- Stevanato Group

- Becton, Dickinson & Co.

- Corning Incorporated

- Tekni-Plex, Inc.

- DWK Life Sciences

- Nelipak Healthcare Packaging

- Datwyler Holding Inc.

- Catalent Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and industry-focused research methodology to evaluate the global vaccine packaging market, integrating primary insights from key stakeholders—including pharmaceutical and biotech manufacturers, packaging solution providers, regulatory bodies, and healthcare organizations—with secondary data from corporate reports, scientific publications, and regulatory frameworks. Our research analyzes market dynamics driven by cold chain innovations, patient safety requirements, regulatory compliance, and sustainability trends, with a particular focus on pre-filled syringes, ready-to-use vials, ultra-low temperature packaging, and anti-counterfeiting technologies. USDAnalytics also provides granular segmentation by product type, material, application, and end-use industry, alongside detailed regional insights covering North America, Europe, Asia-Pacific, China, India, Japan, and Latin America. Strategic investments, mergers and acquisitions, and technological advancements in smart packaging, digital traceability, and eco-friendly materials are examined to provide actionable intelligence for industry professionals aiming to navigate growth, compliance, and innovation in the evolving vaccine packaging landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.