Market Overview: Glass Containers Driving Premiumization and Circular Packaging

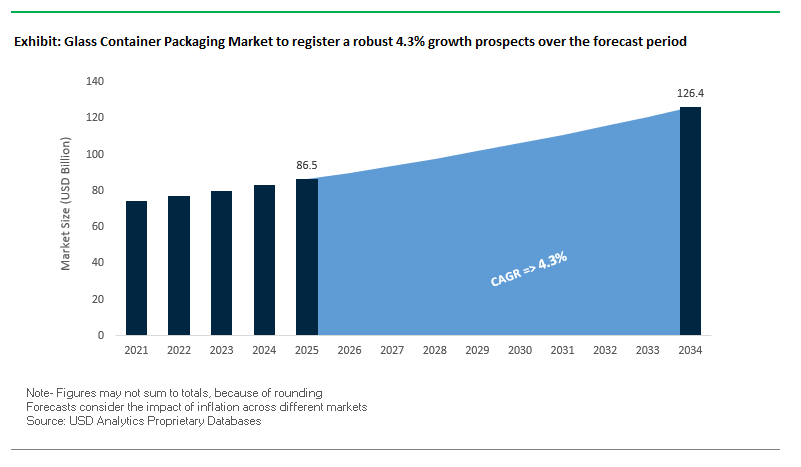

The Global Glass Container Packaging Market is valued at USD 86.5 billion in 2025 and is projected to reach USD 126.3 billion by 2034, growing at a CAGR of 4.3%. Glass container packaging plays a pivotal role across food, beverages, pharmaceuticals, and cosmetics, where it is valued for its premium aesthetics, strong barrier protection, and infinite recyclability. As a “permanent material”, glass can be recycled endlessly without loss of quality, making it a preferred packaging option in an era of strict regulations on plastics and rising consumer preference for eco-friendly solutions.

A major driver for this market is premiumization, particularly in beverages and cosmetics, where glass enhances brand identity and shelf appeal. In pharmaceuticals, the use of borosilicate glass vials and ampoules is crucial for storing sensitive biologics, vaccines, and injectable drugs safely. Lightweighting technology is another critical development, enabling manufacturers to reduce transportation costs and lower carbon emissions while maintaining product integrity.

Key Insights for Industry Professionals:

- Market Value: USD 86.5B (2025) → USD 126.3B (2034).

- CAGR: 4.3% driven by sustainability, premiumization, and pharma demand.

- Sustainability: Infinite recyclability positions glass as a key enabler of the circular economy.

- Lightweighting: New designs lower logistics costs and reduce emissions.

- Healthcare: Growing reliance on inert borosilicate glass for vaccines and injectables.

Market Analysis: Recent Developments in the Glass Container Packaging Industry

The Global Glass Container Packaging Industry has seen significant innovation and partnerships in sustainability, recycling infrastructure, and smart packaging technologies.

In August 2025, DNP participated in Medical Fair Thailand, introducing sustainable glass packaging for medical and pharmaceutical use, reinforcing the trend of eco-friendly solutions in healthcare. In July 2025, Vetropack unveiled an innovative measurement system to detect mechanical stress on production lines, designed to reduce breakage and improve efficiency. That same month, Ardagh Group partnered with CAP Glass, expanding its recycling capacity in North America.

In June 2025, reports highlighted the rise of smart packaging technologies such as QR codes, RFID, and NFC, being integrated into glass containers to ensure traceability and freshness monitoring. In May 2025, O-I Glass partnered with Linde to implement OPTIMELT® TCR technology at its Holzminden plant in Germany, reducing energy use and emissions. Earlier in March 2025, O-I Glass successfully completed a biofuel trial, showcasing its leadership in sustainable glassmaking.

Beyond industrial initiatives, glass is expanding in consumer-facing applications. In February 2025, Olay launched its Super Cream with SPF 30 in a glass jar, reflecting the growing adoption of premium skincare packaging. Meanwhile, Ardagh Glass Packaging North America in April 2025 expanded its range of 12 oz Heritage beer bottles, catering to the growing craft beverage industry.

Transformative Trends and High-Value Opportunities in the Glass Container Packaging Market

Strategic Investment in Furnace Electrification and Hybrid Technology

A major trend redefining the glass container packaging industry is the accelerated investment in furnace electrification and hybrid technologies. Glass manufacturing is one of the most energy-intensive industrial processes, traditionally dependent on natural gas, making it a key contributor to carbon emissions. Rising fossil fuel costs and stricter carbon reduction mandates are pushing manufacturers to adopt hybrid and fully electric furnaces.

The European BEAR project, which received €2.2 million in funding, is a benchmark initiative demonstrating that a hybrid furnace sourcing 40% of its heat from electricity can cut natural gas usage by more than 50% and avoid nearly 100,000 tonnes of CO₂ over a decade. Such initiatives highlight not only environmental benefits but also long-term cost competitiveness. Companies like Kanthal are advancing semi-electric solutions tailored to different glass types, particularly oxidized glass, to enable a phased transition.

For manufacturers, electrification provides a competitive advantage, aligning with regulatory frameworks such as the EU’s Green Deal while improving operational efficiency. The transition is also reshaping the supply chain, requiring closer collaboration with renewable energy providers to guarantee a stable, cost-efficient power supply. Beyond emissions reduction, electric melting ensures higher thermal efficiency since energy is transferred directly into the glass melt, minimizing losses. This makes furnace electrification both an environmental necessity and an economic growth avenue.

Lightweighting Through Advanced Manufacturing and Design

Another major trend is the lightweighting of glass bottles and jars using advanced forming and design technologies such as narrow-neck press-and-blow (NNPB) and CAD-based simulation tools. Lightweighting reduces raw material consumption, lowers furnace energy demand, and decreases logistics costs—all while maintaining the durability and performance expected from glass containers.

Vetropack highlights that lightweight wine bottles can weigh 50 grams less, saving 34 tonnes of CO₂ per million bottles produced. NNPB technology achieves weight reductions of 15–30% by improving glass distribution within molds, while FEM analysis allows engineers to identify stress points and optimize bottle strength.

This trend is aligned with both sustainability mandates and brand-owner cost priorities, making lightweight glass highly attractive for beverages, pharmaceuticals, and cosmetics packaging. By reducing transportation weight, brands can also cut logistics emissions, further enhancing their environmental footprint. Collaboration between designers, engineers, and manufacturers is key to scaling lightweighting, ensuring bottles retain performance standards despite thinner walls. For the glass container packaging market, lightweighting represents a strategic balance between cost efficiency and sustainability leadership.

Expansion into Premium Non-Alcoholic and Functional Beverages

The surging demand for premium non-alcoholic beverages, including craft sodas, kombucha, functional waters, and zero-proof spirits, is creating a lucrative opportunity for glass packaging manufacturers. Glass offers unmatched flavor preservation and a premium aesthetic that aligns with the clean-label, high-quality positioning of these beverages.

A European consumer study revealed that 65% of shoppers trust products more when packaged in glass, underscoring its role in premium brand perception. Brands such as Malaki and leading bottled water producers are leveraging elegant glass packaging to signal purity and exclusivity. Functional beverage companies are also increasingly adopting custom-designed bottles with embossing, vibrant labeling, and unique forms to stand out in crowded markets.

This opportunity highlights glass as more than just a container—it is a strategic branding asset. The tactile weight, clarity, and recyclability of glass resonate with eco-conscious and quality-focused consumers. Manufacturers that can deliver customizable, visually distinctive designs are well-positioned to secure long-term contracts with premium beverage players. For the glass container packaging market, this growth avenue strengthens its relevance in segments where perception and performance are equally critical.

Closed-Loop Recycling Systems with Enhanced Cullet Processing

While glass is infinitely recyclable, the quality of cullet (recycled glass) remains a bottleneck. A high-purity cullet stream allows manufacturers to substitute greater amounts of recycled material, cutting energy consumption and CO₂ emissions significantly. One tonne of cullet saves 1.2 tonnes of virgin raw materials and lowers energy use by 2.5% for every 10% added to the batch.

The industry is now moving toward closed-loop recycling models, where manufacturers partner with waste management companies, beverage brands, and municipalities to collect and process post-consumer glass directly. Advanced cullet cleaning technologies like laser purification are being deployed to remove contaminants and produce food-grade cullet at scale.

Initiatives such as “Close the Glass Loop” in Europe aim to achieve a 90% glass collection rate by 2030, underscoring the potential of collaborative models. For manufacturers, offering branded closed-loop systems enhances supply security, meets corporate sustainability pledges, and reduces reliance on virgin raw materials. This approach also improves customer loyalty by allowing brands to promote 100% recycled-content bottles as part of their sustainability story.

Competitive Landscape: Leading Companies in Glass Container Packaging

The Glass Container Packaging Market is shaped by a mix of global leaders, each leveraging innovation, sustainability, and operational efficiency to expand their market positions.

O-I Glass, Inc. focuses on sustainable glassmaking innovation

O-I Glass is a global leader with a strong presence across beverages, food, and non-alcoholic categories. In July 2025, its “Fit to Win” program delivered USD 145 million in cost savings, improving resilience against macroeconomic pressures. The company is advancing lightweighting and biofuel-powered furnaces, reinforcing its decarbonization agenda. O-I’s strategy combines operational efficiency with pioneering sustainable glass technologies.

Ardagh Group S.A. expands lightweight beer and wine glass portfolio

Ardagh Group’s dual-material portfolio (glass and metal) positions it strongly in global packaging. In April 2025, it expanded its 12 oz Heritage beer bottle line in North America, targeting craft brewers. In July 2025, it announced a partnership with CAP Glass to strengthen recycling. Ardagh is a leader in lightweighting, developing sub-300 g spirit and wine bottles, and continues to drive innovation for circular glass solutions.

Verallia S.A. commits to CO2 reduction and circular economy goals

Verallia operates 35 production facilities in 12 countries, making it the third-largest global producer. Its CSR initiatives earned the EcoVadis Platinum Medal, ranking in the top 1% globally. Verallia’s CO2 emissions reduction target (-46% by 2030) is validated by SBTi, underscoring its strong climate commitments. Its strategy focuses on co-innovation with customers and suppliers to “re-imagine glass for a sustainable future.

Gerresheimer AG strengthens pharmaceutical glass solutions

Gerresheimer specializes in high-value glass vials, ampoules, and syringes, essential for sensitive biologics and injectable drugs. The company is expanding its injectable drug delivery portfolio and investing heavily in pharma containment solutions. Its products are critical for oncology, vaccines, and diabetes treatments, reinforcing Gerresheimer as a trusted partner in global healthcare packaging.

Vidrala S.A. diversifies with Brazilian acquisition and efficiency focus

Vidrala produces over 9.5 billion glass containers annually for 1,600+ customers. In 2023, it acquired Vidroporto in Brazil, entering a high-growth market and strengthening global partnerships. With operations in Iberia, the UK, and Brazil, Vidrala emphasizes cost efficiency and logistics services alongside glass manufacturing. Its Select Series® food wraps and antimicrobial films further enhance its diversified offerings, positioning the company for long-term expansion.

Glass Container Packaging Market Share Insights

Bottles Dominate Market Share by Product in Glass Container Packaging

Bottles account for nearly 65% of the glass container packaging market in 2025, underscoring their overwhelming importance in the global beverage sector. Their dominance is driven by the unmatched role of glass bottles in packaging beer, wine, spirits, soft drinks, and premium juices, where product purity, taste preservation, and brand image are paramount. Glass’s impermeability ensures no flavor migration or chemical interaction, making it the material of choice for both alcoholic and non-alcoholic beverages. Jars represent the next major product type, providing reliable packaging for sauces, jams, pickles, and dry goods while maintaining product freshness through wide-mouth convenience. Vials and ampoules, though a smaller volume segment, are a high-value, regulation-driven niche in pharmaceuticals, where Type I borosilicate glass ensures sterility and chemical resistance for injectables and vaccines. Other containers, such as decorative formats for cosmetics and specialty bottles for perfumes, highlight the premium, aesthetic-driven appeal of glass in luxury categories. This segmentation illustrates how bottles dominate by scale, jars anchor the food sector, and vials drive compliance-driven value in healthcare.

Food and Beverages Secure Largest Market Share by Application in Glass Packaging

The food and beverage industry commands 70% of the global glass container packaging market in 2025, cementing its position as the undisputed demand center. Glass’s perception as a safe, pure, and infinitely recyclable material resonates strongly with beverage and food brands, particularly those seeking to emphasize sustainability and premium positioning. Its strength in premium beer, wine, and spirits markets, combined with the growing demand for healthier juice and dairy beverages, reinforces its leadership. Pharmaceuticals and healthcare, while smaller in volume, represent an irreplaceable high-value segment where glass vials, ampoules, and cartridges are mandated for sterility and chemical stability in sensitive formulations. Cosmetics and personal care utilize glass primarily for perfumes, serums, and luxury skincare, where brand prestige and aesthetic differentiation are critical. Meanwhile, niche demand from chemical and industrial sectors focuses on laboratory reagents and high-purity substances, where glass’s inert properties are non-negotiable. This segmentation highlights how food and beverages dominate by scale, while pharmaceuticals and cosmetics reinforce glass’s premium and compliance-driven positioning.

United States Glass Container Packaging Market Accelerates with Lightweighting and Sustainability Trends

The U.S. glass container packaging market is shaped by a fragmented regulatory landscape, with California’s SB-54 Extended Producer Responsibility (EPR) law encouraging a 25% reduction in plastics by 2032. While primarily targeting plastics, this regulation indirectly favors glass as a sustainable alternative. Technological advancements are driving lightweighting initiatives, exemplified by O-I Glass’s Estampe wine bottle, which reduces the carbon footprint by 25% compared to traditional bottles.

Corporate investments, including Amcor’s planned acquisition of Berry Global Group, are fueling R&D for sustainable packaging solutions, influencing the broader packaging ecosystem. Key applications span premium beverages, food, and pharmaceuticals, with craft beer and spirits particularly driving demand for customized, aesthetically appealing glass containers. The market’s strong focus on sustainability is fueled by recyclability, non-toxic properties, and state-supported recycling programs, positioning glass as a preferred material for eco-conscious consumers and businesses.

Germany Glass Container Packaging Market Strengthened by Circular Economy and Advanced Manufacturing

Germany’s glass container market is governed by the EU Packaging and Packaging Waste Regulation (PPWR), effective February 2025, which mandates fully recyclable or reusable packaging by 2030. The well-established Packaging Act (VerpackG) and deposit-refund system encourage design for recyclability, supporting high recycling rates.

Corporate investments are significant, with Gerresheimer AG expanding its production of environmentally friendly glass, and government-supported initiatives, such as the EUR 9.9 million Bavarian project, promoting sustainable glass manufacturing. Technological innovations allow manufacturers to quickly swap colors and molds, appealing to craft brewers and small brands. The market is particularly strong in pharmaceuticals, food, and beverages, as well as cosmetics and perfumery, driven by Germany’s robust manufacturing base and strong export orientation.

China Glass Container Packaging Market Supported by Government Green Policies and Automation

China’s glass container packaging market benefits from government initiatives aligned with the “dual carbon” goal, aimed at promoting recycling and sustainable materials. The March 2024 Action Plan for Large-Scale Equipment Updates and Consumer Goods Replacement, alongside the GB/T 31268 standard on excessive packaging, is transforming industry practices, particularly in e-commerce.

Technological advancements, including automation and AI, are enhancing production efficiency and cost optimization. Foreign corporate expansions, such as SGD Pharma’s launch of glass vials at its Zhanjiang plant in September 2024, highlight the market’s move toward environmentally friendly luxury packaging. Key applications include beverages, food, and personal care products, with the growing e-commerce and domestic manufacturing sectors driving substantial demand for high-quality glass containers.

India Glass Container Packaging Market Expands Through Circular Economy Initiatives and Local Manufacturing

India’s glass container market is growing due to circular economy initiatives and the Make in India campaign, which encourages domestic manufacturing and technology development. Technological advancements, including automation in food processing plants, are increasing the demand for high-performance, specialized glass containers.

Corporate investments are robust, with AGI Glaspac planning a $50 million plant in Cuttack and an additional $18.5 million investment in NNPB technology and glass recycling equipment. Key applications are in food and beverage, pharmaceuticals, and exports, where modern, high-performance glass packaging is essential to meet international safety standards. The market is further supported by FSSAI regulations emphasizing consumer safety and labeling transparency.

Japan Glass Container Packaging Market Driven by Precision Manufacturing and Sustainable Packaging Policies

Japan is a leader in precision manufacturing, with the glass container market benefiting from sustainable production trends. The Plastic Resource Circulation Act, effective April 2022, encourages eco-friendly materials and reduces single-use plastics, supporting glass as a preferred recyclable alternative.

Corporate expansions, including Coca-Cola Bottlers Japan Inc.’s increased PET bottle production, demonstrate the country’s strong focus on high-performance packaging solutions. Innovations focus on specialty and value-added containers with superior barrier properties, IoT-enabled tracking, easy-open tear notches, and resealable closures, catering to aging populations and single-person households. Japan’s emphasis on sustainable, technologically advanced packaging positions its glass container market for steady growth.

Mexico Glass Container Packaging Market Driven by Beverage Tradition and Strategic Global Exports

Mexico’s glass container market is experiencing robust growth, supported by corporate investments like Vitro Glass Containers’ $70 million furnace expansion in Toluca, which increases capacity for perfumery and liquor by more than 50%. Technological advancements have enabled the production of 5.3 billion containers in 2023, with the country’s 94 glass plants operating at 95% capacity.

Key applications are rooted in the nation’s strong alcoholic beverage culture, particularly tequila and mezcal, as well as non-alcoholic beverages and pharmaceuticals. Sustainability is increasingly influencing market dynamics, with Mexican companies adopting innovative technologies to meet eco-conscious consumer demands. Mexico’s strategic location and growing exports, particularly to the U.S., solidify its significant position in the global glass container packaging market.

Glass Container Packaging Market Report Scope

Glass Container Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$86.5 Billion

|

|

Market Size (2034)

|

$126.3 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Product (Bottles, Jars, Vials & Ampoules, Other Containers), By Application (Food & Beverage, Pharmaceuticals & Healthcare, Cosmetics & Personal Care, Chemical & Industrial), By Color (Flint, Amber, Green, Other Colors)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

O-I Glass, Inc., Ardagh Group S.A., Verallia S.A., Vitro, S.A.B. de C.V., Nippon Sheet Glass Co., Ltd., Gerresheimer AG, Vidrala S.A., BA Glass S.A., Shandong Pharmaceutical Glass Co., Ltd., Consol Glass (Pty) Ltd, SGD Pharma, HNGIL, Piramal Glass Pvt Ltd, AGI Glaspac, Heinz-Glas GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glass Container Packaging Market Segmentation

By Product

- Bottles

- Jars

- Vials & Ampoules

- Other Containers

By Application

- Food & Beverage

- Pharmaceuticals & Healthcare

- Cosmetics & Personal Care

- Chemical & Industrial

By Color

- Flint

- Amber

- Green

- Other Colors

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Glass Container Packaging Market

- O-I Glass, Inc.

- Ardagh Group S.A.

- Verallia S.A.

- Vitro, S.A.B. de C.V.

- Nippon Sheet Glass Co., Ltd.

- Gerresheimer AG

- Vidrala S.A.

- BA Glass S.A.

- Shandong Pharmaceutical Glass Co., Ltd.

- Consol Glass (Pty) Ltd

- SGD Pharma

- HNGIL

- Piramal Glass Pvt Ltd

- AGI Glaspac

- Heinz-Glas GmbH

* List Not Exhaustive

Methodology

USDAnalytics conducted an in-depth, integrated research approach to assess the Global Glass Container Packaging Market, combining primary and secondary research to deliver precise insights for industry professionals. Primary research involved interviews with key stakeholders, including glass container manufacturers, beverage and pharmaceutical companies, design and packaging engineers, and sustainability regulators, capturing first-hand insights on technological advancements, lightweighting trends, furnace electrification, and circular economy initiatives. Secondary research encompassed analysis of company reports, press releases, industry publications, trade journals, patent filings, and government policies to validate market drivers, regulatory impacts, and competitive strategies. Market sizing and forecasts were derived using historical data, trend analysis, and econometric modeling, emphasizing growth areas such as premium beverage packaging, pharmaceutical vials, and high-value cosmetic containers. Regional dynamics covering the United States, Germany, China, India, Japan, and Mexico were analyzed to highlight regulatory frameworks, sustainability programs, automation adoption, and strategic investments. Competitive landscape evaluation examined leading players such as O-I Glass, Ardagh Group, Verallia, Gerresheimer, and Vidrala, focusing on innovation, energy-efficient production, recycling initiatives, and lightweighting technologies, providing a comprehensive, forward-looking market perspective for professionals navigating global glass container packaging opportunities.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.