Market Overview: Antifog Films and Sheets Market to Reach $6.6 Billion by 2034 as PFAS-Free, AI-Optimized and Recyclable Packaging Films Reshape Visibility Standards

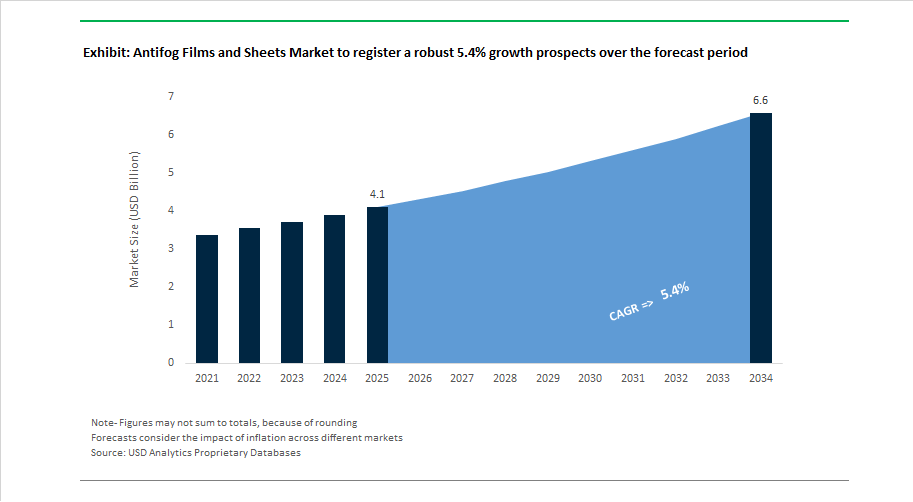

The antifog films and sheets market stands at $4.1 billion in 2025 and is projected to reach $6.6 billion by 2034, expanding at a 5.4% CAGR. Growth is driven by rising demand for anti-condensation packaging films, high-clarity lidding materials, breathable cellulose films, recyclable mono-material sheets, and long-life anti-fog coatings used across fresh food packaging, agricultural films, medical face shields, automotive sensors, and industrial safety visors. The industry is shifting from legacy migratory surfactant systems toward PFAS-free, plant-based, AI-optimized, and nano-engineered surface technologies that maintain optical clarity under rapid humidity and temperature swings. Film producers are prioritizing food-contact compliance, recyclability, compostability, and thermal durability, particularly for chilled foods, hot-fill packaging, bakery items, and high-performance protective glazing.

Technology acceleration began in March 2024 when BASF introduced an AI-driven antifog additive that dynamically adjusts surface energy for consistent clarity. The same month, FogX AI launched NanoClear AI, a non-migratory nano-coating for automotive windshields and sensors. In June 2024, SmartFog Tech commercialized EcoFog Shield for compostable produce packaging. Structural expansion followed in August 2024 when Plaskolite acquired MXL Industries, strengthening optical sheet and visor coating capabilities. Sustainability milestones advanced at FACHPACK in September 2024 where Jindal Films showcased recyclable mono-material PP and PE films with integrated antifog functionality. PFAS-free coating innovation also expanded through 2024 commercialization of Visgard Ultra by FSI Coating Technologies, addressing regulatory pressure on fluorochemicals.

Market consolidation reshaped the competitive landscape in May 2025 when Amcor completed its combination with Berry Global, creating a dominant supplier of antifog lidding and stretch films for chilled foods. Plant-based chemistry gained traction in June 2025 as Palsgaard commercialized Einar 987, a polyglycerol ester antifog additive aligned with clean-label requirements. Throughout 2025, Celanese promoted Clarifoil cellulose films for compostable bakery packaging, while Covestro launched Makrolon transparent flame-retardant grades in September 2025 supporting antifog compatibility in electronics enclosures. PFAS-free oil-resistant packaging advanced in December 2025 as Mitsubishi Chemical Group progressed SoarnoL resin toward 2026 commercialization. Thermal performance boundaries expanded in January 2026 when Toray Industries unveiled a 160°C-resistant PP release film, enabling next-generation antifog sheets for extreme industrial and automotive environments.

Trends and Opportunities Accelerating Innovation in the Antifog Films and Sheets Market

The Global Antifog Films and Sheets Market is entering a regulatory- and technology-driven transformation phase, fueled by bans on single-use plastics, PFAS restrictions, and rapid adoption of engineered multilayer packaging. Food packaging, medical visors, e-commerce mailers, and EV lighting systems are increasingly shifting toward compostable antifog films, PFAS-free antifog coatings, and smart multilayer sheets that combine optical clarity with antimicrobial, UV-blocking, and high-durability performance. These dynamics are reshaping material selection, additive chemistry, and supplier qualification strategies across packaging converters and OEM value chains.

EU PPWR and Global Plastic Treaties Trigger Rapid Shift Toward Compostable Antifog Packaging Films

Regulatory pressure is becoming the single largest catalyst for replacing petrochemical-based antifog films with compostable and recyclable alternatives. The EU Packaging and Packaging Waste Regulation (PPWR), enforced by the European Commission from February 11, 2025, mandates that by August 12, 2026 all packaging must meet strict “design for recycling” criteria, including industrial compostability for labels and stickers applied to fresh produce. This has directly accelerated demand for compostable antifog lidding films, particularly in fruit, vegetable, and ready-meal packaging.

Parallel momentum is coming from the U.S. e-commerce sector. Data released by the U.S. Census Bureau (August 2025) shows Q2 2025 e-commerce sales growth of 5.3%, driving adoption of transparent, breathable antifog mailers and compostable food trays as brands prepare for 2026 compliance deadlines. On a global scale, negotiations under the UN Global Plastic Treaty now involve more than 170 countries aligned on phasing out “non-essential” single-use plastics. As a result, nearly 70% of new compostable film revenue in 2025 is projected to originate from Polylactic Acid (PLA) antifog films, valued for their clarity, moisture control, and compatibility with fresh produce packaging.

Smart Multilayer Antifog Sheets Integrating Active Functions Redefine Performance Standards

Beyond sustainability, the market is rapidly pivoting toward engineered multilayer antifog constructions that deliver extended fog resistance plus active functionality. In 2025, photocatalyst-based antifog coatings captured approximately 33% of the advanced technology segment, leveraging light-activated self-cleaning mechanisms to extend fog-free performance by over 400% versus conventional aqueous systems.

Industrial validation in early 2026 showed polyvinylpyrrolidone-based coatings achieving a 50,000% improvement in wear resistance, enabling antifog sheets to withstand 500+ cleaning cycles in medical visors and industrial face shields without optical degradation. Meanwhile, India’s automotive sector, now exceeding 5 million vehicles annually, is increasingly adopting multilayer sputtered antifog films in EV lighting systems to prevent internal condensation that compromises LED heat dissipation. This cross-sector expansion is strengthening demand for high-durability antifog sheets, antimicrobial multilayer films, and UV-protective optical coatings.

Home-Compostable Antifog Films Create a New Premium Sustainability Segment

A high-value opportunity is emerging around home-compostable antifog coatings and films, which eliminate reliance on industrial composting infrastructure. Article 9 of the EU PPWR calls on member states to prioritize home-compostable packaging formats by January 2030, opening a first-mover advantage for cellulose-based and starch-blend antifog films certified OK compost HOME.

R&D disclosures from CEFLEX (2025) highlight that even minor formulation choices, such as glycerol esters versus ethoxylated sorbitan esters, are now audited for their impact on home-compostability certification. Companies transitioning to 100% bio-based antifog additives marketed as food-grade and ocean-safe are already experiencing adoption rates up to 25% faster among premium organic produce brands in North America, signaling a clear revenue uplift for early innovators in bio-based antifog materials.

PFAS-Free Antifog Coatings Become the Core Competitive Battleground for 2026

The global phase-out of “forever chemicals” is forcing a rapid migration toward PFAS-free antifog systems, making this one of the most commercially significant opportunities in the market. Under new rules from the U.S. Environmental Protection Agency, mandatory reporting of intentionally added PFAS in articles begins April 13, 2026, triggering widespread replacement of fluorinated antifog layers with silicone-based and hydrophilic polymer technologies.

Regional bans are intensifying the shift. France’s Decree No. 2025-1376 and Law No. 2025-188 prohibit PFAS-containing waterproofing agents and treated films from January 1, 2026, creating immediate demand for PFAS-free antifog visors and goggles. Innovators such as FSI Coating Technologies have already commercialized next-generation PFAS-free solutions like Visgard Ultra, delivering comparable surface energy reduction while meeting the new 50 ppm fluorine thresholds enforced across EU and U.S. markets.

Antifog Films and Sheets Market Share and Segmentation Insights

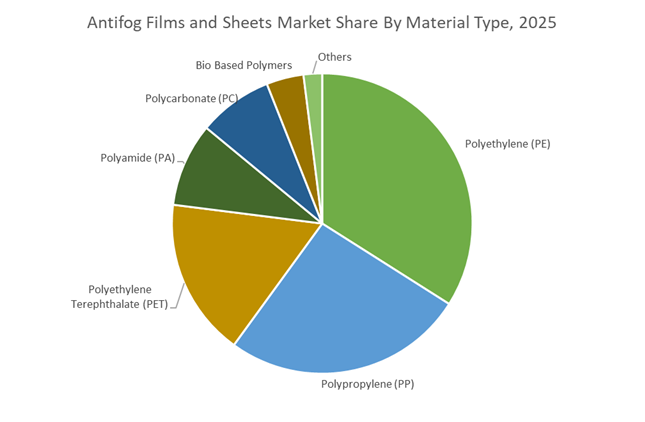

Market Share by Material Type: Polyethylene Leads Volume While Bio-Based Polymers Record Fastest Growth

Polyethylene (PE) commands approximately 34% of the global antifog films and sheets market in 2025, driven by its low cost, flexibility, and widespread use in fresh produce packaging, stretch hoods, and meat trays. Linear low-density polyethylene (LLDPE) is the preferred substrate for antifog blown films due to excellent sealability and compatibility with migratory antifog additives. Polypropylene (PP) follows closely, benefiting from higher clarity and heat resistance in microwavable ready-meal trays and dairy containers, particularly in hot-fill applications. Polyethylene terephthalate (PET) is gaining share in premium and dual-ovenable packaging, supported by the shift toward recyclable PET/PET mono-material structures. Polycarbonate (PC) dominates greenhouse glazing and safety eyewear, relying on surface-applied antifog coatings. Polyamide supports high-barrier vacuum packs for cheese and meats. Bio-based polymers (PLA, PHA, cellulose) represent the fastest-growing segment, propelled by EU Single-Use Plastics Directive compliance and corporate net-zero commitments.

Market Share by Application: Food Packaging Anchors Demand as Agriculture and Medical Uses Expand

Food packaging accounts for roughly 48% of antifog film and sheet consumption in 2025, spanning fresh-cut produce, red meat, poultry, and ready meals, where clear product visibility directly impacts purchase decisions. Modified atmosphere packaging (MAP) relies heavily on antifog functionality to prevent condensation that accelerates spoilage. Agriculture ranks second, with antifog greenhouse films essential for controlled environment agriculture, preventing droplet lensing that causes leaf burn and light loss in high-value crops such as tomatoes and peppers. Medical and healthcare applications require FDA-compliant, non-migratory antifog films for sterile barrier packaging, IV bags, and diagnostic kits. Automotive demand is rising for fog-free instrument cluster lenses and EV displays. Electronics use antifog protection for cameras and wearables, while construction specifies polycarbonate sheets for humid interiors. Solar panels remain an emerging niche, addressing morning condensation losses in floating and tropical photovoltaic installations.

Antifog Films and Sheets Market Competitive Landscape

The antifog films and sheets market is rapidly evolving as packaging, healthcare, automotive, and agriculture industries accelerate adoption of recyclable antifog films, optical-grade antifog sheets, PFAS-free coatings, and mono-material packaging structures. Market leaders are differentiating through nano-multilayer technology, hydrophilic surface chemistry, PCR-based antifog films, and AI-driven material design. Strategic priorities include recycling-ready lidding films, high-clarity medical antifog solutions, greenhouse productivity films, and ESG-aligned lifecycle analytics. With rising demand from fresh protein packaging, EV displays, cold-chain logistics, and medical visors, competition centers on carbon footprint reduction, high-durability antifog performance, and vertically integrated “total system” solutions that combine films, coatings, inks, and adhesives.

Recycling-ready mono-material antifog lidding defines Amcor plc market leadership

Amcor leads the global antifog films and sheets market following its 2025 integration of Berry Global, strengthening its dominance in high-performance lidding. The AmPrima™ Plus portfolio features mono-PE and PP antifog lidding films delivering over 95% recycling-stream compatibility while maintaining high-gloss clarity for fresh protein packaging. In late 2025, Amcor introduced a fully PP retort pouch with a 60% lower carbon footprint versus foil alternatives, retaining antifog performance after high-pressure processing. At Packaging Innovations 2026, the company emphasized price-shield contracts for brands transitioning to high-barrier, plastic-free coatings. Its Amcor ASSET™ lifecycle assessment platform positions Amcor as an ESG partner for global CPG manufacturers.

Optical-grade hydrophilic antifog technology anchors 3M Company in healthcare and electronics

3M remains the technical benchmark for optical antifog films, leveraging advanced hydrophilic chemistry and nanostructured coatings. Its flagship 3M™ Anti-Fog Hydrophilic Film 9962 is widely adopted for medical visors and surgical enclosures requiring biocompatibility and high transparency. In early 2026, 3M scaled its Sustain-Clear bio-based antifog line for food packaging, reducing reliance on petroleum surfactants. The company’s coatings deliver up to 50,000% higher wear resistance than commodity alternatives, extending service life in industrial goggles and electronics. Strategically, 3M is targeting autonomous vehicle sensors and HUD applications, ensuring antifog layers remain compatible with polarized light and LiDAR systems.

Nano-multilayer durability drives Toray Industries, Inc. growth across automotive and agriculture

Toray dominates nano-multilayer antifog film technology, supplying high-durability polyester solutions for automotive glazing and greenhouse applications. In 2025, Toray launched a 50-micron PICASUS™ Nano-Multilayer film that improves heat shielding by 40% while maintaining permanent antifog properties without chemical leaching. January 2026 saw the debut of a 160°C-resistant polypropylene release film, enabling fluorine-free IC substrate processing. Toray leads agricultural greenhouse films with over 90% light transmission, preventing condensation-related yield loss. Its 2025 to 2026 Asia-Pacific expansion in India and Vietnam supports rising demand from horticulture and cold-chain logistics, reinforcing Toray’s green specialty footprint.

Affordable sustainability positions UFlex Limited as emerging-market powerhouse

UFlex is accelerating global penetration through vertically integrated antifog packaging solutions spanning films, inks, and adhesives. The company announced a 54,000-tonne BOPP line in Karnataka and commissioned a 12-billion-pack aseptic facility in Egypt to serve MEA markets. Its FSSAI-compliant PCR-based antifog films utilize up to 100% recycled PET, maintaining food safety and clarity during long-distance transport. UFlex’s Noida recycling project, operational by March 2026, will convert nearly 40,000 tonnes of waste annually into rPET and rPE. With full control over graphics and surface chemistry, UFlex delivers total-system antifog solutions optimized for emerging-market sustainability requirements.

PFAS-free barrier innovation differentiates Mitsubishi Chemical Group

Mitsubishi Chemical Group focuses on integrating gas-barrier science with advanced antifog surface functionality. In late 2025, the company introduced SoarnoL™ EVOH-coated paper substrates, enabling PFAS-free, oil-resistant, antifog fast-food packaging. Under its KAITEKI Vision 35 strategy, Mitsubishi is transitioning toward green specialty materials, including Makrolon® RP bio-based polycarbonate that cuts carbon emissions by 60%. Its antifog sheets are widely used in EV touchscreens and instrument lenses. Through ISCC PLUS-certified supply chains, Mitsubishi enables OEMs to trace sustainability metrics from monomer to finished sheet, reinforcing leadership in mobility and high-end electronics antifog applications.

AI-driven polymer engineering advances Celanese Corporation antifog sheet performance

Celanese specializes in engineered polymers and high-transparency antifog sheets for industrial and architectural markets. In February 2026, the company implemented price adjustments across Zytel® and Frianyl® lines to fund circular economy R&D. Its POM ECO-C expansion showcased low-carbon solutions offering enhanced sliding properties and chemical resistance for demanding antifog environments. Celanese leverages AI-driven material design and digital experimentation to accelerate antifog coating validation. Strategically, it is replacing thermoset rubbers with Santoprene® TPV and Hytrel® TPC in dynamic weather seals, embedding antifog functionality directly into automotive glazing and building envelope systems.

India Antifog Films and Sheets Market: Regulatory Enforcement Meets Packaging and Agri-Tech Scale-Up

India represents one of the most regulation-driven transformation markets for antifog films and sheets. In 2025, the Ministry of Environment, Forest, and Climate Change enforced the Plastic Waste Management Second Amendment Rules, mandating 30% recycled content in Category I rigid packaging for the 2025–26 period. This has directly altered material selection and processing strategies for antifog PET and polycarbonate sheets, forcing manufacturers to reformulate coatings that remain effective on recycled substrates.

Food safety regulation is amplifying this shift. The Food Safety and Standards Authority of India initiated consultations in late 2025 to restrict PFAS and Bisphenol A in food-contact materials. This has triggered accelerated adoption of fluorine-free antifog coatings for lidding films used in ready-to-eat exports. On the supply side, domestic capacity is expanding rapidly. Cosmo Films and Jindal Poly Films announced investments in high-speed BOPP co-extrusion lines to serve export-grade food packaging. Demand is further reinforced by government-subsidized anti-drip greenhouse films under the National Mission on Edible Oils and by cold-chain investments from Adani Group and Reliance Industries, which have doubled domestic usage of antifog lidding in fresh produce packaging. The rollout of the CPCB digital traceability portal in 2025 has added another compliance layer, making recycled resin verification a core purchasing criterion.

United States Antifog Films and Sheets Market: Defense, Medical, and Smart Packaging Innovation

The United States antifog films and sheets landscape is increasingly defined by high-value applications rather than volume packaging alone. In early 2025, the Air Force Research Laboratory awarded development contracts for UV-curable antifog coatings with extreme abrasion resistance, designed for military flight helmets and heads-up displays. This has elevated performance benchmarks for durability, optical clarity, and long-term antifog persistence.

Sustainability policy is influencing material choices. Federal Bio-Preferred procurement guidelines introduced in 2025 have incentivized PLA-based antifog films, prompting NatureWorks to expand capacity for renewable, high-clarity sheets. In parallel, smart packaging is emerging as a differentiator. Berry Global entered a strategic partnership in mid-2025 to integrate AI-enabled sensors into antifog lidding, enabling real-time shelf-life monitoring for protein packaging. Medical and industrial PPE demand has also surged following updated OSHA safety standards, while FSI Coating Technologies launched high-durability antifog films in late 2025 for electric vehicle infotainment displays that must perform under extreme thermal cycling.

China Antifog Films and Sheets Market: Verbund Integration and Multi-Sector Deployment

China’s antifog films and sheets industry is scaling through integrated feedstock supply and multi-sector adoption. The BASF Zhanjiang Verbund site achieved key operational milestones in 2025, enabling localized supply of high-purity polyamide and ethylene precursors for high-barrier antifog lidding films. This integration reduces reliance on imports and improves formulation consistency for food and pharmaceutical packaging.

Policy-driven adoption is expanding beyond packaging. Under updates to the 14th Five-Year Plan, subsidies are supporting nanotechnology-enabled agricultural films that combine antifog and UV-filtering properties, particularly in controlled berry cultivation. Mobility and energy applications are also gaining traction. Weetect Inc. expanded its Shanghai facility in 2025 to produce photochromic antifog sheets for autonomous vehicles and smart helmets. In the energy sector, solar glass manufacturers began mass-applying antifog nanocoatings in humid southern provinces, reporting measurable gains in annual energy yield. These developments position China as a cross-sector deployment hub rather than a single-end-use market.

Germany Antifog Films and Sheets Market: Compliance Leadership and Circular Design

Germany continues to set the regulatory and innovation benchmark for antifog films and sheets in Europe. In late 2025, Evonik Industries transitioned its entire coating additive portfolio to zinc-free and PFAS-free alternatives, directly influencing antifog film compliance across EU markets. This move has accelerated adoption of next-generation additives compatible with recycled and bio-based polymers.

Infrastructure and circular design are reinforcing demand. Deutsche Bahn updated its 2025 technical specifications to require permanent antifog and anti-scratch polycarbonate sheets for all new ICE train window replacements, linking passenger safety to materials performance. At the innovation frontier, SmartFog Tech secured patents for biodegradable antifog films that maintain clarity for extended refrigerated storage, aligning antifog performance with circular economy principles.

Saudi Arabia Antifog Films and Sheets Market: Downstream Diversification and Vision 2030 Alignment

Saudi Arabia is emerging as a strategic production and export base for antifog sheets through petrochemical downstream diversification. SABIC introduced LEXAN™ HP92AF in early 2025, an antifog polycarbonate sheet engineered for medical devices and industrial safety visors requiring high impact resistance and optical stability. This product reflects the Kingdom’s push toward higher-value specialty materials.

Vision 2030 investments are accelerating localization. In 2025, Saudi Arabia committed $150 million to develop a Specialty Films Park focused on antifog lidding for regional food security initiatives. This infrastructure is designed to integrate resin production, sheet extrusion, and coating application, positioning the country as a supply hub for the Middle East and adjacent export markets.

Structural Drivers by Country in the Antifog Films and Sheets Industry

Antifog Films and Sheets Market County Level Snapshot

|

Country

|

Primary Growth Catalyst

|

Strategic Direction

|

|

India

|

Recycled content and food safety regulation

|

Fluorine-free coatings, BOPP capacity, traceable recycling

|

|

United States

|

Defense, medical PPE, smart packaging

|

High-durability coatings, bio-based films, sensor integration

|

|

China

|

Verbund integration and policy subsidies

|

Multi-sector deployment across food, mobility, and energy

|

|

Germany

|

PFAS-free mandates and rail safety

|

Circular design, biodegradable antifog solutions

|

|

Saudi Arabia

|

Vision 2030 downstream investment

|

Medical-grade sheets and regional food packaging hub

|

Antifog Films and Sheets Market Report Scope

Antifog Films and Sheets Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.1 Billion

|

|

Market Size (2034)

|

$6.6 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polycarbonate, Polyamide, Bio Based Polymers), By Technology (Additive Based, Coating Based, Nanotechnology Based, Plasma Surface Treatment), By Form (Films, Sheets), By Application (Food Packaging, Agriculture, Automotive, Medical and Healthcare, Electronics and Displays, Architecture and Construction, Solar Panels)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, SABIC, Amcor plc, Berry Global Inc, Celanese Corporation, Toray Industries, Sumitomo Bakelite, DuPont Teijin Films, FSI Coating Technologies, Kafrit Industries, Cosmo Films, Jindal Poly Films, Coveris Group, Weetect, Uflex

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Antifog Films and Sheets Market Segmentation

By Material Type

- Polyethylene

- Polypropylene

- Polyethylene Terephthalate

- Polycarbonate

- Polyamide

- Bio Based Polymers

By Technology

- Additive Based

- Coating Based

- Nanotechnology Based

- Plasma Surface Treatment

By Form

By Application

- Food Packaging

- Agriculture

- Automotive

- Medical and Healthcare

- Electronics and Displays

- Architecture and Construction

- Solar Panels

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Antifog Films and Sheets Industry

- 3M Company

- SABIC

- Amcor plc

- Berry Global Inc

- Celanese Corporation

- Toray Industries

- Sumitomo Bakelite

- DuPont Teijin Films

- FSI Coating Technologies

- Kafrit Industries

- Cosmo Films

- Jindal Poly Films

- Coveris Group

- Weetect

- Uflex

*- List not Exhaustive