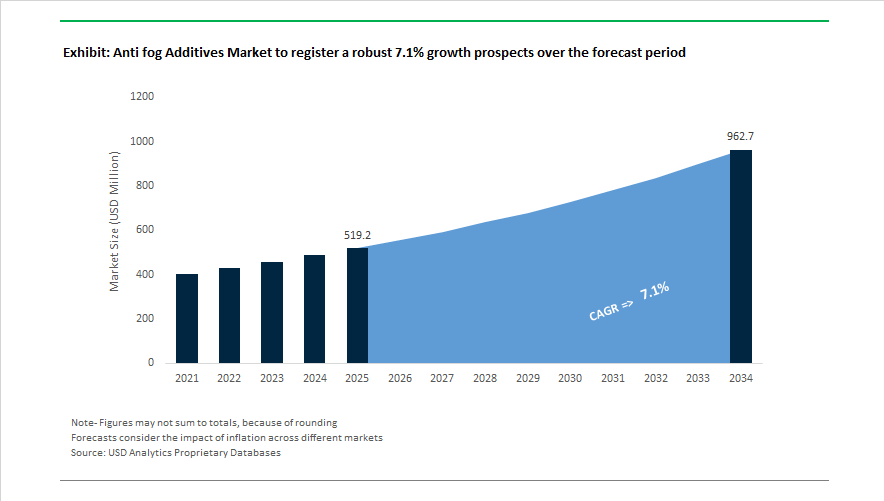

Market Overview: Anti Fog Additives Market to Reach $962.6 Million by 2034 as High-Purity Food-Contact Standards, AI-Formulated Additives, and Plant-Based Chemistries Accelerate Adoption

The global anti fog additives market is projected to grow from $519.2 Million in 2025 to $962.6 Million by 2034, registering a 7.1% CAGR driven by expanding demand across agricultural films, food packaging, medical PPE, automotive glazing, and greenhouse covers. Anti-fog additives function by modifying polymer surface energy, allowing moisture to form a transparent film rather than light-scattering droplets. Growth is supported by rising greenhouse cultivation, demand for high-clarity food-contact packaging, and stricter hygiene standards in healthcare. Market evolution is marked by the transition from ethoxylated amines toward polyglycerol esters, PFAS-free surfactants, bio-based additives, and AI-optimized formulations that deliver stable performance under variable humidity and temperature conditions.

Technology innovation accelerated in December 2023 and early 2024 as Kraton Corporation commercialized Nexar anti-fog films for durable PPE applications. Multifunctional chemistry advanced in 2024 when Palsgaard launched Einar 608 dual-function molecules. AI-assisted formulation entered the market in March 2024 through BASF, followed by automotive nano-coating breakthroughs from FogX AI. Portfolio sustainability strengthened in November 2024 when Clariant completed its PFAS-free transition. Regulatory alignment intensified in March 2025 with the EU implementation of Regulation 2025/351, raising purity requirements for food-contact surfactants and boosting adoption of high-purity PGEs. Product performance innovation continued in June 2025 as Palsgaard showcased Einar 987, and in July 2025 Tosaf introduced the FogFree masterbatch portfolio for polyolefin films.

Sustainability and capacity developments continued through May 2025 as Clariant received a sustainability supplier award and January 2024 vertical integration by Nouryon strengthened precursor supply chains. Agricultural film performance solutions were highlighted in February 2026 when BASF presented advanced stabilizer platforms at Plastindia. Cross-industry technology transfer appeared in February 2025 with Kyowa Hakko Bio introducing stabilized delivery systems applicable to high-clarity packaging.

Trends and Opportunities Reshaping the Anti Fog Additives Market

Regulatory Pressure Is Forcing Anti-Fog Adoption in Sustainable Food Packaging

Anti fog additives are no longer optional in food packaging. Under the EU Packaging and Packaging Waste Regulation (PPWR) and Single-Use Plastics Directive (SUPD), recycled-content packaging now faces optical-performance requirements that directly mandate surface-modifying additives. Since January 1, 2025, the EU requires 25% recycled content in PET beverage bottles, and similar targets are being extended to food trays. rPET-based films naturally lack surface-wetting capabilities, causing condensation that obscures visibility and undermines freshness perception. This has triggered large-scale adoption of polyglycerol ester anti-fog systems that maintain transparency, are non-toxic, and meet recyclable-food-contact restrictions.

Bio-based polymers like PLA are expanding fastest in eco-friendly trays and wrap films. However, PLA suffers severe fogging at refrigerator temperatures. Technical briefs published in late-2024 confirm that whey-protein-based hydrophilic coatings enable PLA films to extend produce shelf life by 15–20% by preventing moisture droplets from forming optical barriers. This clarity requirement is directly tied to consumer conversion. In 2024, 51.6% of food packaging films incorporated anti-fog additives primarily for retail shelf appeal; by 2025, it became a procurement standard for e-commerce grocery and meal delivery, where visibility signals hygiene and freshness during home delivery handoffs.

PPE and Protective Eyewear Now Require Permanent Anti Fog Performance Instead of Temporary Coatings

Post-pandemic policy has permanently embedded anti fog requirements into PPE guidelines across hospitals, industrial plants, biological R&D labs, and manufacturing floors. The ANSI Z87.1+ and EN166 standards list fog-resistance as a core safety requirement rather than a premium feature. In 2025, non-prescription safety eyewear represents 66% of PPE eyewear demand, and procurement contracts specify coatings that must resist alcohol-based surface cleaning, especially in aerosol-generating medical procedures.

A market shift is unfolding from disposable face shields to reusable goggles. Field data from 2025 shows that 25% of standard anti fog coatings degrade within 6–12 months, causing vision impairment and productivity loss. To solve this, manufacturers are transitioning to “permanent” hydrophilic nanocoatings designed to last 2–3 years of industrial use without delamination. These coatings form part of a broader CAPEX-driven replacement cycle where enterprise buyers prioritize lifecycle cost-per-use, not unit cost, positioning long-life anti fog additives as margin-rich SKUs.

Automotive and Aerospace Display Technologies Are Driving Demand for High-Temperature-Stable Anti Fog Additives

Automotive interiors are undergoing a structural redesign as OEMs integrate multi-screen OLED dashboards, transparent displays, and smart cabin interfaces. These surfaces accumulate moisture under extreme thermal swings, especially in tropical and sub-zero markets. Automotive-grade anti fog additives must sustain transparency from −40°C to 120°C, and resist UV yellowing and surface outgassing—performance criteria increasingly written into Hyundai, Tata Motors, and BMW procurement specifications for 2025-model dashboard assemblies.

In aviation, anti fog is tied to cockpit safety. Heads-Up Displays (HUDs) must retain optical clarity for FAA-level pilot visibility standards. Aerospace OEMs are piloting photothermal-responsive anti fog films that leverage ambient light to create micro-thermal gradients, actively suppressing condensation without electrical energy loads. High-purity additive requirements are crucial—OLED and HUD components require metal-ion-free surfactants to avoid capacitive interference. This is establishing electronics-grade anti fog chemicals as a discrete, premium-priced sub-market.

Controlled Environment Agriculture (CEA) Is Creating Scale Demand for Anti Fog Agricultural Films

In greenhouses and vertical farming systems, fog formation directly blocks Photosynthetic Active Radiation (PAR), reducing crop yield. Coating benchmarks from FSI Coating Technologies (2025) show that anti fog PE films increase light transmission by 15–50%, enabling earlier harvesting cycles and greater commercial land productivity. Eliminating fog also prevents drip-based fungal outbreaks, reducing pesticide use by up to 10% in high-humidity operations in Japan and the Netherlands.

Government stimulus amplifies this opportunity. In 2025, the agricultural film additives market is projected to reach $8.5 billion, with anti fog agents classified by agriculture ministries as “critical infrastructure additives” for greenhouse lifespan extension in UV-intense climates. As climate-adaptive food production accelerates, non-migratory, long-life anti fog coatings are shifting from a specialty input to standard CEA infrastructure—unlocking multi-year recurring chemical supply contracts.

Anti-Fog Additives Market Share and Segmentation Insights

Market Share by Type: Glycerol Esters Lead Volume While Polyglycerol Esters Drive Premium Growth

Glycerol esters account for approximately 31% of global anti-fog additives demand in 2025, led by glycerol monostearate (GMS) and glycerol monooleate (GMO) used as internal migratory anti-fog agents in PVC, BOPP, PET clamshells, and polyolefin food films. Their FDA food-contact approval and low cost underpin leadership, although humidity sensitivity and surface dust pickup limit performance in premium formats. Sorbitan esters rank second, offering higher thermal stability for injection molding and agricultural films. Polyglycerol esters are the fastest-growing segment, favored for reduced migration, clarity retention, and non-ethoxylated “clean label” positioning in high-end packaging and automotive interiors. Ethoxylated sorbitan esters (polysorbates) dominate spray-on coatings but face 1,4-dioxane scrutiny. PEG and polyoxyethylene esters remain cost-driven niches. Organic anti-fog additives show ~10% growth in vision panels, while inorganic TiO₂/silica coatings stay confined to hard surfaces.

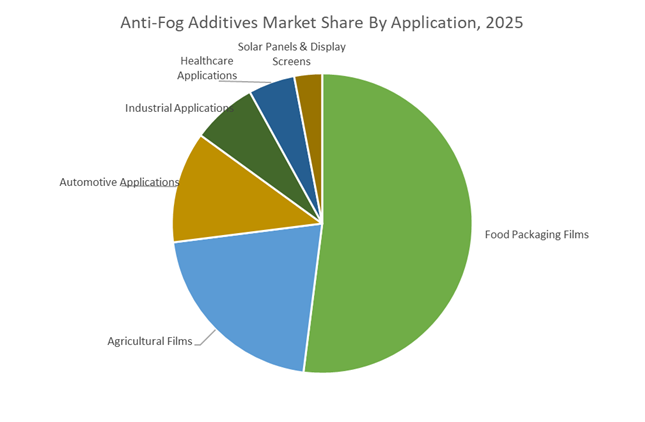

Market Share by Application: Food Packaging Dominates as Agricultural Films Accelerate

Food packaging films represent roughly 52% of anti-fog additive consumption in 2025, spanning fresh produce trays, meat overwrap, bakery packs, and prepared meals, where visible condensation directly impacts purchase intent. Growth of 5 to 6% annually is supported by e-grocery expansion and reformulation toward mono-material PE/PP structures, increasing reliance on internal anti-fog chemistries. Agricultural films are the fastest-growing application, driven by controlled environment agriculture and the need for drip-free greenhouse covers that reduce leaf burn and fungal pressure, favoring migration-resistant polyglycerol esters for multi-season durability. Automotive applications form a high-value niche in interior displays, headlamp lenses, and ADAS optics, demanding multifunctional anti-fog coatings. Industrial safety eyewear remains mature, while healthcare uses command premiums under biocompatibility requirements. Solar panels and display glass are smallest today, with TiO₂ photocatalytic coatings offering long-term upside tied to BIPV and smart glazing adoption.

Anti Fog Additives Market Competitive Landscape

The global anti fog additives market is rapidly evolving as food packaging, agricultural films, medical devices, and high-clarity coatings demand longer-lasting fog resistance, PFAS-free chemistries, and fully recyclable solutions. Competitive intensity is rising around bio-based surfactants, anti-fog masterbatches, and in-resin integration for mono-material PE/PP films. Leading players are differentiating through ISCC PLUS certification, mass-balance feedstocks, and multifunctional additives that combine anti-fogging with slip, antiblock, and antimicrobial performance. Regional innovation hubs in Asia, expanded distribution networks in North America, and regulatory-driven reformulation (REACH, non-PFAS) are reshaping supplier strategies, with sustainability, clarity retention, and processing efficiency emerging as decisive purchasing criteria.

Surface-chemistry leadership drives Evonik Industries AG’s premium anti-fog portfolio

Evonik has strengthened its position in high-performance anti fog additives through deep expertise in surface chemistry and biosurfactants. In early 2025, the company received the Ringier Technology Innovation Award for TEGO® Wet 580 Terra, a biosurfactant delivering superior wetting and anti-fogging for coatings and inks while supporting eco-efficiency goals. Evonik is advancing its TEGO® eCO portfolio, emphasizing mass-balance and bio-based feedstocks to help customers reduce Scope 3 emissions. A streamlined U.S. and Canada distribution network launched in January 2026 improves lead times for plastic and coating additives. Evonik’s solutions perform reliably across extreme environments, from greenhouse films to chilled food display packaging.

Biodegradable innovation anchors Nouryon’s packaging-focused strategy

Nouryon leverages its surfactant and polymer expertise to accelerate biodegradable anti-fog systems for flexible packaging. In February 2026, the company launched the industry’s first 100% bio-based, biodegradable carboxymethylcellulose (CMC), enabling water-soluble, eco-friendly anti-fog formulations. The opening of its Shanghai Innovation Center in November 2025 strengthens localized development for Asia’s fast-growing food packaging market. Nouryon supplies non-ionic surfactants such as glycerol and sorbitan esters, valued for cost efficiency and compatibility with PE and PP films. A strategic EMEA distribution agreement with IMCD in late 2025 further expands Nouryon’s reach across Europe, the Middle East, and Africa.

Masterbatch integration defines Avient Corporation’s functional additives approach

Avient has emerged as a key supplier of anti-fog masterbatches for food packaging and horticultural films, led by its Cesa™ Anti-Fog range that modifies surface tension to prevent droplet formation. At Pharmapack 2026, Avient highlighted its transition to non-PFAS additives for medical and pharmaceutical packaging. By early 2026, ISCC PLUS certification across sites in Sweden, Taiwan, and Singapore enabled global delivery of mass-balance bio-based polymer solutions. Avient differentiates through its Mevopur™ healthcare portfolio, combining anti-fogging with antimicrobial and slip/antiblock properties for surgical visors and medical device packaging, reducing formulation complexity for converters.

Renewable ester chemistry positions Croda International Plc as a bio-based pioneer

Croda focuses on surfactant-based and polymeric anti-fog agents derived from renewable vegetable oils, supporting clean beauty, medical films, and agricultural applications. Following divestment of legacy industrial assets, Croda has concentrated on Life Sciences and Consumer Care, where high-purity esters are essential. During 2025–2026, the company ramped North American pharmaceutical-grade lipid capacity, creating R&D synergies with its anti-fog ester technologies. Croda’s Sustainability-by-Design strategy proactively aligns formulations with REACH requirements, ensuring glycerol esters meet upcoming purity standards. In agricultural films, Croda additives enhance greenhouse light transmission, directly supporting crop yield optimization.

PFAS-free processing solutions expand Clariant AG’s anti-fog ecosystem

Clariant integrates anti-fog performance with advanced polymer processing aids through its AddWorks® platform. The 2025 launch of AddWorks™ PPA introduced PFAS-free processing aids that work synergistically with anti-fog agents to enable defect-free film extrusion. Ahead of ChinaPlas 2026, Clariant is showcasing halogen-free and bio-based wax technologies used as carriers for high-performance anti-fog masterbatches. Its ready-to-use additive combinations reduce total cost of ownership for film producers. Clariant is also strengthening its footprint in Asian mobility and electronics markets, where anti-fog additives support automotive sensors and high-clarity display applications.

In-resin recyclability strategy differentiates LyondellBasell Industries

LyondellBasell applies its polyolefin leadership to integrate anti-fog additives directly into LDPE and LLDPE matrices, advancing the mono-material packaging trend. This in-resin approach preserves full recyclability without requiring coating removal, simplifying downstream processing for converters. Leveraging massive scale and vertical integration, LyondellBasell supplies drop-in anti-fog polyolefin grades widely used in refrigerated ready-to-eat meal packaging. The company is also investing in molecular recycling technologies to ensure anti-fog-treated films can be regenerated without quality loss. High-performance concentrates address both hot- and cold-fog conditions, supporting food freshness and shelf visibility.

China Anti Fog Additives Market: Verbund Integration and Green Power Redefine Additive Scale Economics

China continues to strengthen its position as a global manufacturing anchor for anti-fog additives through large-scale capacity commissioning and integrated chemical infrastructure. In late 2025, BASF commissioned a new high-performance dispersant and additive line in Nanjing using Controlled Free Radical Polymerization technology. This facility supports advanced anti-fog solutions for industrial, automotive, and electronics coatings, where long-lasting clarity and surface uniformity are critical.

Structural advantages are reinforced by the Zhanjiang Verbund project, where dedicated polymer additive units are being localized to serve South China’s electronics and food packaging clusters. Parallel investments by Clariant, through its joint venture with Beijing Tiangang, expanded stabilizer production in Cangzhou to meet rising demand from agricultural films and textile plastics. Policy alignment under the 14th Five-Year Plan is accelerating the replacement of legacy chemistries with food-grade, non-toxic additives such as polyglycerol esters. The availability of renewable electricity from the BASF–Mingyang offshore wind project further improves the product carbon footprint of domestically produced anti-fog agents, strengthening China’s export competitiveness.

United States Anti Fog Additives Market: Medical-Grade Purity and Packaging Demand Drive Reformulation

The United States anti fog additives market is being reshaped by portfolio realignments, stricter food-contact scrutiny, and growth in cold-chain packaging. During 2024–2025, DuPont streamlined its business focus toward Water and Healthcare, redirecting R&D toward medical-grade, anti-fog polymers used in diagnostic equipment and optical housings. This strategic shift has elevated purity, extractables control, and long-term optical performance as key differentiators.

At the same time, Celanese Corporation integrated the Mobility and Materials business acquired from DuPont, strengthening its presence in anti-fog films and sheets for automotive glazing and interior displays. State-level regulations in New Jersey and New York have intensified oversight of food-contact materials, driving rapid adoption of PFAS-free anti-fog coatings. The rise of online grocery delivery has added another demand vector, with refrigerated lidding films increasingly specified with anti-fog additives to maintain visibility during transit.

Germany Anti Fog Additives Market: Circular Economy Compliance and Bio-Based Leadership

Germany remains a benchmark market for sustainability-led anti-fog innovation. At the K 2025 trade fair in Düsseldorf, German producers showcased solutions under the VALERAS® and REWOFERM® platforms that leverage mass-balanced certified processes to significantly lower embedded emissions. These developments signal a broader industry pivot toward traceable, low-carbon anti-fog chemistries aligned with EU climate and materials policy.

Circular compatibility is a defining theme. Evonik introduced TEGO® antifoam and anti-fog grades in 2025 that retain functionality in post-consumer recycled plastic streams, addressing a key technical barrier in circular packaging. German laboratories also commercialized fully bio-based sorbitan esters that comply with BlueSign and GOTS 7.0 standards, reinforcing Germany’s leadership in environmentally sensitive applications spanning food packaging, textiles, and personal care films.

India Anti Fog Additives Market: Bio-Fermentation and Protected Agriculture Accelerate Adoption

India’s anti fog additives landscape is expanding through policy-backed bio-manufacturing and strong pull from protected agriculture. The BioE3 Policy implemented during 2024–2025 provides a regulatory tailwind for domestic producers to scale bio-fermented surfactants and esters. Companies such as Fine Organics are leveraging this framework to expand capacity for food-safe and agricultural-grade anti-fog additives.

Demand-side momentum is reinforced by capital inflows into greenhouse farming. NABARD-supported venture funding announced in 2025 has accelerated the adoption of advanced greenhouse films incorporating anti-fog additives to improve light transmission and crop yields. On the supply side, the PLI scheme has encouraged domestic esterification investments in the Gujarat chemical corridor, reducing reliance on imported anti-fog masterbatches and improving cost stability for Indian converters.

Saudi Arabia Anti Fog Additives Market: Feedstock Advantage and Vision 2030 Diversification

Saudi Arabia is positioning itself as a regional hub for anti-fog additives by combining polymer feedstock access with downstream diversification under Vision 2030. Clariant has expanded masterbatch production in the Kingdom to serve Middle East and Africa markets, leveraging proximity to polymer raw materials for agricultural film and industrial cooling applications.

Vision 2030 investments are channeling capital into high-performance additives for water-intensive infrastructure such as desalination and district cooling. Anti-fog agents designed for harsh thermal and humidity conditions are increasingly specified in these systems, creating a differentiated demand profile compared with consumer packaging markets.

Japan Anti Fog Additives Market: Ultra-High Purity and Food Loss Prevention

Japan’s anti fog additives industry is defined by ultra-high purity standards and application-specific precision. In early 2025, Tosoh and Sumitomo Bakelite intensified their focus on semiconductor- and medical-optics-grade anti-fog agents, where trace impurities can compromise optical performance.

Public policy is also shaping demand. The Ministry of Agriculture, Forestry and Fisheries promoted anti-fog technologies in 2025 as a core tool for reducing condensation-driven food spoilage. This has increased adoption of anti-fog films in fresh produce packaging, reinforcing Japan’s emphasis on functional additives that support food security and waste reduction.

Strategic Positioning by Country in the Anti-Fog Additives Industry

Anti-fog Additives Market County Level Snapshot

|

Country

|

Strategic Focus

|

Industry Implication

|

|

China

|

Verbund integration and renewable-powered scale

|

Cost-efficient, export-ready anti-fog additives

|

|

United States

|

Medical-grade purity and cold-chain packaging

|

Rapid shift to PFAS-free, high-clarity formulations

|

|

Germany

|

Circular economy and bio-based compliance

|

Benchmark for low-carbon, recycled-compatible solutions

|

|

India

|

Bio-fermentation and greenhouse agriculture

|

Rising domestic demand and import substitution

|

|

Saudi Arabia

|

Feedstock access and Vision 2030

|

Regional hub for industrial and agricultural films

|

|

Japan

|

Ultra-high purity and food waste reduction

|

Precision anti-fog additives for optics and packaging

|

Anti-fog Additives Market Report Scope

Anti fog Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$519.2 Million

|

|

Market Size (2034)

|

$962.6 Million

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Type (Glycerol Esters, Polyglycerol Esters, Sorbitan Esters, Ethoxylated Sorbitan Esters, Polyoxyethylene Esters, Polyethylene Glycol, Organic Anti Fog Additives, Inorganic Anti Fog Additives), By Application (Food Packaging Films, Agricultural Films, Automotive Applications, Healthcare Applications, Industrial Applications, Solar Panels and Display Screens), By Substrate Material (Polyethylene, Polypropylene, Polyvinyl Chloride, Polyethylene Terephthalate, Polycarbonate), By Form (Powder and Granules, Liquid, Masterbatches)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Clariant AG, Croda International Plc, Evonik Industries AG, Dow Inc, DuPont, Nouryon, Fine Organics, Avient Corporation, Emery Oleochemicals, Palsgaard, Corbion, Tosaf Compounds, SABIC, Ampacet Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Anti Fog Additives Market Segmentation

By Type

- Glycerol Esters

- Polyglycerol Esters

- Sorbitan Esters

- Ethoxylated Sorbitan Esters

- Polyoxyethylene Esters

- Polyethylene Glycol

- Organic Anti Fog Additives

- Inorganic Anti Fog Additives

By Application

- Food Packaging Films

- Agricultural Films

- Automotive Applications

- Healthcare Applications

- Industrial Applications

- Solar Panels and Display Screens

By Substrate Material

- Polyethylene

- Polypropylene

- Polyvinyl Chloride

- Polyethylene Terephthalate

- Polycarbonate

By Form

- Powder and Granules

- Liquid

- Masterbatches

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Anti Fog Additives Industry

- BASF SE

- Clariant AG

- Croda International Plc

- Evonik Industries AG

- Dow Inc

- DuPont

- Nouryon

- Fine Organics

- Avient Corporation

- Emery Oleochemicals

- Palsgaard

- Corbion

- Tosaf Compounds

- SABIC

- Ampacet Corporation

*- List not Exhaustive