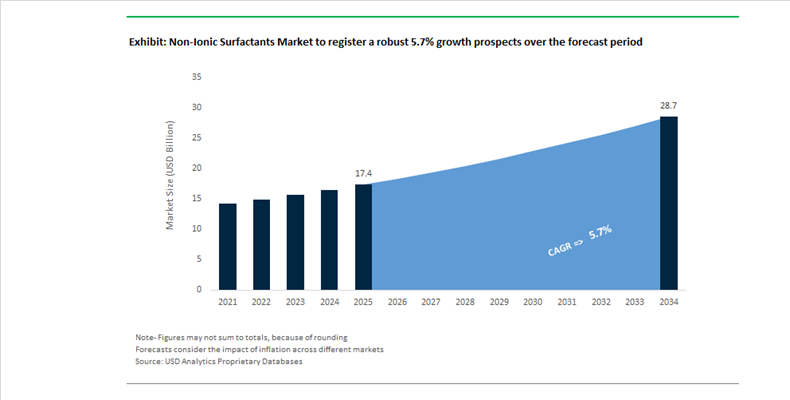

Non-Ionic Surfactants Market Valued at $17.4 Billion in 2025, Advancing Toward $28.7 Billion by 2034 at 5.7% CAGR

The Non Ionic Surfactants Market is valued at $17.4 billion in 2025 and is projected to reach $28.7 billion by 2034, expanding at a CAGR of 5.7%. Growth is underpinned by rising demand for bio-based surfactants, high-performance alcohol ethoxylates, alkyl polyglucosides (APGs), and specialty non-ionic wetting agents across home care, personal care, agrochemicals, pharmaceuticals, and industrial cleaning applications. Regulatory tightening on volatile organic compounds, 1,4-dioxane residues, and carbon intensity of ethoxylation processes is accelerating the shift toward renewable feedstocks, low-foam formulations, and biodegradable surfactant chemistries. Asia-Pacific remains the fastest-growing regional hub due to expanding middle-class consumption, urban sanitation programs, and agrochemical intensity, while North America and Europe focus on premiumization and sustainable reformulation.

In May 2024, Clariant AG finalized the acquisition of Huntsman’s specialty additives business, integrating a broad portfolio of non-ionic surfactants and intermediates into its Care Chemicals division. In the same month, Evonik Industries inaugurated the world’s first industrial-scale rhamnolipid plant in Slovakia, introducing biosurfactants that directly compete with conventional alcohol ethoxylates in premium personal care. In March 2024, Dow Inc. and DuPont announced a strategic collaboration to co-develop advanced non-ionic alkoxylates for agrochemical drift control and enhanced uptake technologies. During 2024 and 2025, Croda International scaled commercialization of its 100% bio-based ECO non-ionic range, manufactured using bio-ethanol at its Delaware facility, reinforcing the renewable ethoxylation trend.

Capacity expansion accelerated into 2025 and 2026. In February 2025, Lonza Group AG secured European Commission approval for its Antwerp site dedicated to pharmaceutical-grade and industrial non-ionic surfactants. In March 2025, Evonik signed an exclusive U.S. distribution agreement with Sea-Land Chemical to expand reach for its REWOQUAT® and TOMADOL® non-ionic cleaning systems in the industrial and institutional segment. In November 2025, BASF SE inaugurated an expanded Alkyl Polyglucoside production facility in Bangpakong, Thailand, strengthening supply of bio-based APGs derived from renewable corn and coconut feedstocks to Asia-Pacific detergent and cosmetics manufacturers. BASF confirmed in late 2025 that its new APG production line in Cincinnati, Ohio, will commence operations in 2026, positioning the site as a primary North American hub for high-purity non-ionic surfactants.

Strategic investments and restructuring reflect a maturing yet innovation-driven market. In 2024, Stepan Company committed $220 million to expand global surfactant capacity by 10% through 2026, targeting specialty low-foam non-ionics for industrial cleaning and crop solutions. In December 2025, Nouryon broke ground on a South American innovation center in Brazil to develop localized eco-friendly non-ionic wetting agents and chelates, with full operations expected by late 2026. In January 2026, Dow launched its “Transform to Outperform” restructuring strategy, focusing on digital sales integration and AI-driven optimization of its surfactant portfolio to improve EBITDA margins and rationalize commodity exposure.

Non-Ionic Surfactants Market Trends and Opportunities

Trend: Strategic Shift Toward Bio-Based and Narrow-Range Ethoxylates for Sustainable Cleaning Performance

The global non-ionic surfactants market is undergoing a structural transition as home care, institutional cleaning, and industrial formulators move away from broad-range ethoxylates toward bio-based and Narrow-Range Ethoxylates (NREs). This shift is driven by the dual requirement of regulatory compliance and performance optimization, particularly in cold-water washing and low-VOC formulations. Narrow-range ethoxylation technology significantly reduces unreacted alcohol content, which directly lowers volatile organic compound emissions and aquatic toxicity. Comparative industry benchmarking in 2024 confirmed that NREs can cut residual free alcohol levels by up to 50%, resulting in faster wetting, improved detergency at lower temperatures, and easier compliance with EU Ecolabel and EPA Safer Choice certification criteria.

Capacity investments underscore the strategic importance of this transition. In November 2025, BASF commissioned an expanded Alkyl Polyglucosides (APG) production facility in Bangpakong, Thailand, targeting fast-growing Asian demand for 100% naturally derived non-ionic surfactants. This expansion complements BASF’s announced APG capacity build-out in Cincinnati, Ohio, scheduled for 2026, signaling a coordinated transcontinental strategy to serve multinational consumer goods companies seeking renewable carbon surfactant platforms. In parallel, Dow introduced EcoSense™ 2470, a non-ionic surfactant utilizing recycled carbon derived from carbon capture technology. This innovation represents a meaningful decoupling of surfactant carbon content from fossil feedstocks and positions non-ionic surfactants as enablers of Scope 3 emission reduction strategies for global brands.

Trend: Capacity Expansion for High-Purity Non-Ionic Surfactants in Pharma and Agrochemical Formulations

Beyond cleaning applications, demand is accelerating for high-purity non-ionic surfactants such as polysorbates and sorbitan esters, driven by pharmaceutical manufacturing complexity and agrochemical formulation intensity. In pharmaceuticals, non-ionic surfactants function as critical stabilizers for biologics, vaccines, and advanced drug delivery systems, including lipid nanoparticle-based mRNA platforms. Updated 2025 Clean-in-Place guidance from the U.S. Food and Drug Administration has increased scrutiny on surface residues, prompting manufacturers to adopt ultra-low-residue non-ionic surfactants that shorten validation cycles and reduce downtime. This regulatory tightening has translated into an estimated 6.7% growth in adoption of pharmaceutical-grade non-ionic surfactants within controlled manufacturing environments.

In agrochemicals, non-ionic surfactants are evolving from inert formulation aids into performance-enhancing actives. In January 2024, Bionema Group launched Soil-Jet BSP100, a biodegradable non-ionic surfactant engineered to improve the efficacy of biological pesticides. Such innovations allow formulators to reduce total active ingredient dosage while maintaining field performance, aligning with global regulatory pressure to lower chemical load per hectare. Regulatory developments in India further reinforce this trend. The 2024 Draft Surfactants Quality Control Order is pushing domestic producers, including Galaxy Surfactants, to accelerate R&D investment in high-purity, eco-compliant specialty non-ionic surfactants during FY 2024–25.

Opportunity: Low-Foam Non-Ionic Surfactants for Automated Food and Beverage CIP Systems

Automation and resource efficiency in food and beverage processing represent a high-growth opportunity for specialized low-foam non-ionic surfactants. Automated Clean-in-Place systems require surfactants that deliver high detergency without foam interference, ensuring uninterrupted operation of pumps, valves, and sensors at elevated temperatures. In dairy processing, new non-ionic surfactant blends introduced in 2025 enable effective cleaning at temperatures as low as 40°C instead of the conventional 60°C, translating into potential energy savings of 15 to 20% per CIP cycle. These efficiency gains are becoming commercially decisive as energy and water costs rise across processing-intensive industries.

The opportunity is particularly pronounced in Asia-Pacific, where rapid adoption of industrial cleaning machinery is colliding with water conservation mandates. China’s 14th Five-Year Plan explicitly targets a 10% reduction in industrial water usage, incentivizing faster-rinsing, low-foam non-ionic surfactants that minimize rinse cycles. Innovation velocity is also accelerating through digital tools. In 2025, Nouryon deployed AI-driven molecular design platforms such as BeautyCreations AI, reducing development timelines for customized low-foam surfactant systems by approximately 40%. This capability enables rapid tailoring of non-ionic surfactants for food-contact compliance, temperature tolerance, and sensor compatibility.

Opportunity: Advanced Non-Ionic Surfactant Systems for Chemical Enhanced Oil Recovery

Mature oil fields and declining primary recovery rates are sustaining long-term demand for Chemical Enhanced Oil Recovery solutions, positioning non-ionic surfactants as core functional materials. Unlike anionic surfactants, non-ionic alcohol alkoxylates maintain performance under high salinity and high-temperature reservoir conditions, making them particularly suitable for challenging geological formations. Field pilots conducted by National Oil Companies during 2024–2025 demonstrated that modern non-ionic surfactant formulations can achieve ultra-low interfacial tension below 10⁻³ mN/m, mobilizing trapped oil and improving recovery factors by 5 to 15%.

Digitalization is amplifying this opportunity. Machine-learning-driven reservoir modeling now allows operators to precisely match surfactant hydrophilic-lipophilic balance to reservoir mineralogy, optimizing slug design and chemical efficiency. At the same time, environmental scrutiny of upstream operations is driving interest in bio-derived non-ionic surfactants for EOR. Operators in the North Sea and the Gulf of Mexico are increasingly qualifying renewable-feedstock surfactants as part of broader decarbonization strategies aimed at reducing the carbon intensity per barrel produced. This convergence of performance necessity, digital optimization, and sustainability positioning is elevating non-ionic surfactants from commodity chemicals to strategic enablers within the global energy transition.

Non Ionic Surfactants Market Share and Segmentation Insights

Alcohol Ethoxylates Lead Non Ionic Surfactants Market Through Versatile Detergent and Cleaning Performance

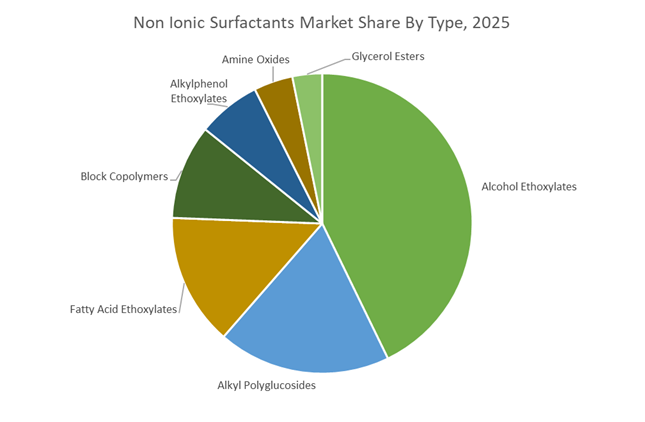

Alcohol ethoxylates accounted for 42.8% of the Non Ionic Surfactants Market share in 2025, making them the most widely used class of non-ionic surfactants across cleaning, personal care, and industrial formulation markets. Alcohol ethoxylates are favored due to their excellent detergency, strong grease removal capability, high wetting efficiency, and compatibility with both anionic and cationic surfactants, enabling flexible formulation across a broad range of products. These surfactants are widely incorporated into laundry detergents, dishwashing liquids, industrial cleaners, textile processing chemicals, agrochemical formulations, and oilfield additives, where they function as emulsifiers, wetting agents, and dispersants. Their key advantage lies in the ability to precisely control ethylene oxide chain length, allowing formulators to tailor the hydrophilic-lipophilic balance (HLB) for specific applications. In 2025, a major industry trend has been the shift toward bio-based alcohol ethoxylates derived from natural fatty alcohols obtained from vegetable oils such as palm and coconut oil, enabling surfactant manufacturers to offer renewable and RSPO-certified product lines that align with sustainability commitments while maintaining equivalent cleaning performance and formulation stability.

Household Detergents Drive the Largest Demand for Non Ionic Surfactants

Household detergents accounted for 34.8% of the Non Ionic Surfactants Market share in 2025, representing the largest application segment due to the enormous global consumption of cleaning products for residential use. Non-ionic surfactants play a critical role in laundry detergents, dishwashing liquids, surface cleaners, and multipurpose household cleaning formulations, where they provide strong grease removal, soil suspension, and compatibility with water hardness conditions. Their non-ionic nature allows them to maintain high cleaning efficiency even in hard water environments and low-temperature washing conditions, making them essential ingredients in modern detergent formulations. The expansion of global urban populations, rising hygiene awareness, and the growing penetration of premium detergent products in emerging economies continue to drive demand for high-performance non-ionic surfactants. In 2025, the detergent industry has accelerated its transition toward concentrated liquid detergents and unit-dose detergent pods, which require surfactants with optimized solubility, controlled cloud point characteristics, and stability in high-active formulations. Alcohol ethoxylates and alkyl polyglucosides are particularly suited to these advanced formulations, supporting efficient cold-water washing while enabling compact detergent formats that reduce packaging and transportation requirements.

Non-Ionic Surfactants Market Competitive Landscape

The non-ionic surfactants market in 2026 is shaped by bio-based transition, Asia-Pacific localization, and carbon footprint transparency. Competitive leadership is driven by APGs, glucamides, and low-toxicity ethoxylates, with manufacturers focusing on PCF disclosure, regional production, and high-performance biodegradable formulations for home care, pharma, and industrial applications.

BASF expands Asia-Pacific surfactant capacity with flexible production and low-carbon specialty portfolio

BASF is reinforcing its leadership through Verbund integration and strategic localization of non-ionic surfactant production. Its Seosan, South Korea JV with Hannong Chemicals enhances supply flexibility via advanced swing tank systems tailored for specialty NIS formulations. With €59.7 billion in 2025 sales, BASF continues to prioritize its Nutrition & Care segment as a key growth driver. The divestiture of its decorative paints business allows reallocation toward sustainable surfactants and green chemistry innovation. Its expansion of BPA/BPS-free, food-contact compliant materials aligns with tightening EU regulations. BASF’s integrated production and PCF-driven transparency strengthen its position in high-growth regional markets.

Croda accelerates biodegradable surfactant innovation with high-value plant-based emulsifiers and life sciences integration

Croda International is advancing its “Smart Science” strategy by focusing on biodegradable, plant-derived non-ionic surfactants. Its Natrineo™ CR8 emulsifier and NeutraFresh™ BD technology highlight leadership in replacing synthetic ethoxylates with high-performance bio-based alternatives. The company targets a 3–6% CAGR through 2028, supported by growth in patented New & Protected Products. Its partnership with Amino GmbH strengthens integration of surfactants into pharmaceutical delivery systems. Croda’s innovations meet strict 28-day biodegradability requirements, aligning with EU sustainability mandates. This focus on premium, high-margin ingredients positions Croda at the forefront of circular home care and personal care markets.

Stepan optimizes global footprint to prioritize high-margin bio-based surfactants and operational efficiency

Stepan Company is restructuring its global operations to enhance efficiency and focus on specialty non-ionic surfactants. Through Project Catalyst, the company aims to achieve US$100 million in cost savings by consolidating production into modern facilities. Site closures and divestitures, including assets in the U.S. and Asia, reflect a shift away from commodity surfactants toward high-margin specialty applications. Stepan remains a leading merchant producer, emphasizing bio-based, low-toxicity formulations for agriculture and oilfield sectors. Its strategy enhances operational agility while mitigating cost pressures from inflation and logistics. This repositioning strengthens its competitiveness in value-added surfactant markets.

Clariant advances bio-based surfactants and NPE replacement technologies for agrochemical and industrial applications

Clariant is strengthening its non-ionic surfactant portfolio through innovation in sugar-based and NPE-free formulations. Its Synergen™ Guard 100 enhances biological pesticide performance through nano-emulsion technology, while Sapogenat™ T serves as a high-performance alternative to restricted nonylphenol ethoxylates. The company’s Glucotain® and Glucopure® ranges provide VOC-free, biodegradable solutions for personal care and coatings industries. Clariant’s “local-for-local” production strategy ensures regional supply resilience and reduced carbon footprint. Its focus on sustainable, high-performance surfactants aligns with regulatory and environmental demands. This positions Clariant as a key player in green surfactant innovation.

Evonik transforms portfolio toward specialty biosolutions and high-value surfactant platforms for advanced applications

Evonik Industries is repositioning itself as a specialty chemicals leader through portfolio transformation and innovation in biosolutions. With €1.87 billion EBITDA in 2025, the company is focusing on high-return segments and divesting lower-margin intermediates. Its growth strategy targets €1.5 billion in additional sales by 2032 from innovation-driven applications, including circular economy technologies. Evonik’s non-ionic surfactants are integral to polyurethane foams and advanced drug delivery systems, emphasizing performance and precision. Stable sales in its Care division reflect strong positioning in high-value markets. This transformation supports Evonik’s leadership in next-generation, sustainable surfactant solutions.

Thailand: Bio-Based Capacity Build as ASEAN Supply Anchor

Thailand has emerged as a strategic production hub for bio-based non-ionic surfactants, anchored by the November 2025 inauguration of BASF’s expanded Alkyl Polyglucoside (APG) production plant at Bangpakong. This facility is purpose-built to resolve a long-standing regional bottleneck in high-performance, plant-derived non-ionic surfactants for personal care and home care formulations. By localizing APG output within Southeast Asia, BASF has structurally reduced lead times and logistics-related emissions associated with imports from Europe and North America, directly improving supply chain resilience for multinational FMCG customers operating in ASEAN markets.

From a technology standpoint, the Bangpakong site represents a step change in green surfactant manufacturing. The plant deploys proprietary low-waste synthesis routes using 100% renewable feedstocks derived from plant oils and sugars. This positions Thailand as a critical launchpad for 2026 consumer product portfolios built around clean label, sulfate-free, and biodegradable claims. The expansion also strengthens Thailand’s role as a regional export base, supplying neighboring markets where regulatory pressure and consumer preference are converging toward mild, non-toxic non-ionic surfactant systems.

United States: Domestic APG Localization and Performance-Driven Blends

In the United States, the non-ionic surfactants market is undergoing a structural realignment toward domestic production and performance-specific formulations. BASF confirmed that its world-scale APG production line in Cincinnati, Ohio, remains on track for a Q1 2026 start-up. This greenfield project is a cornerstone of BASF’s synchronized global production strategy, designed to ensure consistent quality and availability of sustainable non-ionic surfactants across North America while insulating customers from transcontinental supply disruptions.

Regulatory and performance factors are reinforcing this shift. Several Shell NEODOL alcohol ethoxylate grades retained their EPA Safer Choice ingredient listing through late 2025, accelerating their adoption in high-volume green laundry detergents and institutional cleaners. At the same time, Pilot Chemical Company expanded its 2025 R&D focus toward low-foam non-ionic systems, launching the Aspire blend series. These formulations are optimized for high-efficiency washing machines and automated industrial degreasing, where rapid wetting and controlled foaming are decisive performance parameters.

Germany: Innovation-Led Shift Toward Low-Carbon Non-Ionics

Germany’s non-ionic surfactants market is defined by innovation intensity and sustainability-driven differentiation. In mid-2025, Clariant’s German research centers introduced the Genapol Complete line, positioned as the first all-in-one non-ionic surfactant optimized for automatic dishwashing tablets. By combining rinse aid, wetting, and cleaning functionality in a single low-carbon footprint molecule, the product addresses both formulation simplification and EU sustainability benchmarks.

Clariant further extended its portfolio in October 2025 with Velsan Flex, a sugar-based non-ionic surfactant that also functions as a preservative booster. This dual functionality allows personal care brands to reduce synthetic preservative load while maintaining microbial stability, a decisive advantage ahead of 2026 reformulation cycles. In parallel, Dow’s 2025 European asset review signaled a strategic pivot away from energy-intensive upstream production toward higher-margin, low-carbon derivative surfactants, with operating EBITDA benefits expected to materialize from 2026 onward.

India: Export-Oriented Mild Surfactants and Domestic Capacity Push

India continues to strengthen its position as both a manufacturing base and export hub for non-ionic surfactants. Galaxy Surfactants reported exports to more than 80 countries in 2025, underscoring India’s growing influence in global personal care supply chains. The company is actively scaling its mild surfactant portfolio, with a strong emphasis on non-ionic ethoxylates tailored for premium facial cleansers, baby care, and sulfate-free shampoos.

On the domestic front, policy support is accelerating capacity expansion. Government initiatives promoting sustainable agriculture are driving the uptake of non-ionic surfactants as agrochemical adjuvants, where they enhance wetting and adhesion of active ingredients on crop surfaces. Simultaneously, large Indian chemical groups are leveraging the Production Linked Incentive scheme to invest in domestic ethoxylation infrastructure, targeting a meaningful reduction in dependence on imported fatty alcohol ethoxylates by late 2026.

China: Feedstock Integration and Regulatory-Driven Adoption

China remains the volume and growth engine of the global non-ionic surfactants market, supported by upstream integration and regulatory mandates. SABIC’s Fujian petrochemical complex is advancing toward its 2026 completion milestones, integrating world-scale ethylene and ethylene oxide capacity. This captive EO supply materially lowers feedstock costs for downstream non-ionic surfactant production and enhances supply security for domestic formulators.

Regulatory signals are reinforcing demand growth. The Ministry of Industry and Information Technology implemented new Green Manufacturing guidelines in 2025, mandating a 2.5 to 3.0 percent increase in biodegradable surfactant usage in industrial textile processing. China’s broader chemical sector expanded by nearly 8% in Q3 2025, with firms such as Yantai Oriental Protein Tech leading innovation through the integration of pea-based starches into surfactant matrices, aligning cost efficiency with sustainability goals.

Saudi Arabia: Portfolio Optimization and Downstream Value Chain Support

Saudi Arabia’s non-ionic surfactants landscape is shaped by strategic portfolio optimization rather than immediate capacity additions. In August 2025, SABIC confirmed an internal transformation program to concentrate on core high-growth chemical segments, including surfactants derived from oxygenated intermediates. This review includes optimization of the Petrokemya affiliate to strengthen competitiveness in export-oriented surfactant value chains.

Supporting this direction, pilot commissioning of a one million metric ton MTBE project in Q3 2025 is expected to reinforce the availability of oxygenated intermediates that underpin specialty surfactant synthesis. While indirect, this investment enhances the robustness of Saudi Arabia’s broader chemical ecosystem, positioning the Kingdom as a reliable upstream partner for global non-ionic surfactant producers.

Summary Table: Non-Ionic Surfactants Market – Country-Level Strategic Positioning

Non-Ionic Surfactants Market County Level Snapshot

|

Country

|

Strategic Emphasis

|

Key Developments

|

Structural Impact

|

|

Thailand

|

Bio-based APG scale-up

|

Bangpakong APG expansion

|

ASEAN supply resilience and clean-label growth

|

|

United States

|

Domestic APG and specialty blends

|

Cincinnati APG plant, low-foam innovations

|

Reduced import reliance and performance differentiation

|

|

Germany

|

Innovation-led low-carbon surfactants

|

Genapol Complete, Velsan Flex

|

Premium EU-compliant formulations

|

|

India

|

Export leadership and capacity build

|

Galaxy exports, PLI-backed ethoxylation

|

Global supply hub and import substitution

|

|

China

|

Feedstock integration and mandates

|

Fujian EO integration, MIIT guidelines

|

Cost-efficient scale and regulatory pull

|

|

Saudi Arabia

|

Portfolio optimization

|

Petrokemya review, MTBE pilot

|

Upstream strength for specialty surfactants

|

Non-Ionic Surfactants Market Report Scope

Non-Ionic Surfactants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.4 Billion

|

|

Market Size (2034)

|

$28.7 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Type (Alcohol Ethoxylates, Alkylphenol Ethoxylates, Fatty Acid Ethoxylates, Alkyl Polyglucosides, Amine Oxides, Glycerol Esters, Block Copolymers), By Origin (Synthetic, Bio-Based), By Application (Household Detergents, Personal Care and Cosmetics, Industrial and Institutional Cleaning, Agrochemicals, Oil and Gas, Textiles and Leather, Food and Beverage), By Functionality (Emulsifiers, Wetting Agents, Detergents, Dispersants, Foam Control Agents)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Dow, Clariant, Stepan, Evonik Industries, Croda International, SABIC, Shell Chemicals, Nouryon, Kao, Huntsman, Galaxy Surfactants, Indorama Ventures, Sasol, Arkema

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Non-Ionic Surfactants Market Segmentation

By Type

- Alcohol Ethoxylates

- Alkylphenol Ethoxylates

- Fatty Acid Ethoxylates

- Alkyl Polyglucosides

- Amine Oxides

- Glycerol Esters

- Block Copolymers

By Origin

By Application

- Household Detergents

- Personal Care and Cosmetics

- Industrial and Institutional Cleaning

- Agrochemicals

- Oil and Gas

- Textiles and Leather

- Food and Beverage

By Functionality

- Emulsifiers

- Wetting Agents

- Detergents

- Dispersants

- Foam Control Agents

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Non Ionic Surfactants Market

- BASF

- Dow

- Clariant

- Stepan

- Evonik Industries

- Croda International

- SABIC

- Shell Chemicals

- Nouryon

- Kao

- Huntsman

- Galaxy Surfactants

- Indorama Ventures

- Sasol

- Arkema

*- List not Exhaustive