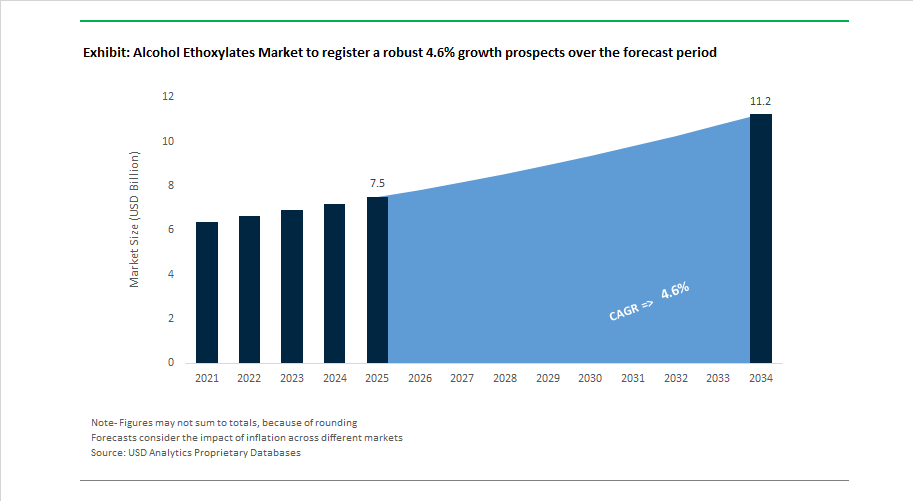

Market Overview: Alcohol Ethoxylates Market to Reach $11.2 Billion by 2034 as Bio-Based Surfactants and High-Biodegradability Formulations Reshape Demand

The global alcohol ethoxylates market is projected to grow from $7.5 billion in 2025 to $11.2 billion by 2034, advancing at a 4.6% CAGR supported by strong demand for non-ionic surfactants in detergents, textile processing, agrochemicals, industrial cleaners, and personal care formulations. Alcohol ethoxylates remain critical for wetting, emulsification, detergency, dispersion, and low-foam performance, particularly in environmentally sensitive applications requiring rapid biodegradability and reduced aquatic toxicity. Market growth is increasingly aligned with the transition toward bio-based fatty alcohol feedstocks, low-carbon ethoxylation routes, and sustainable surfactant supply chains. Regulatory pressure across Europe and North America is accelerating reformulation away from legacy petrochemical inputs, pushing producers toward plant-derived alcohols and improved life-cycle performance metrics.

Sustainability innovation accelerated in January 2024 when LG Chem introduced a textile-focused alcohol ethoxylate designed to reduce water and energy consumption in industrial laundry operations. Agricultural surfactant development advanced in March 2024 with Stepan Company launching high-efficiency wetting agents for pesticide delivery, while Dow formed renewable raw material partnerships to develop fully sustainable ethoxylates under its Ecolibrium and Decarbia platforms. Biodegradability performance improved in late 2024 as Huntsman Corporation reported over 60% of its portfolio meeting rapid biodegradability standards. Agrochemical-focused innovation strengthened in September 2024 when Evonik Industries initiated targeted investments in advanced ethoxylates for crop protection formulations.

Portfolio upgrades and capacity investments intensified through 2025. In January 2025, BASF announced major investment in sustainable alcohol ethoxylate production using plant-based alcohols, followed by February 2025 product introductions from Clariant targeting textile and industrial detergents under stricter biodegradability standards. Pricing pressure surfaced in April 2025 as Indorama Ventures raised prices in response to volatile ethylene oxide feedstocks. Climate-driven supply chain transformation advanced in September 2025 when Croda International strengthened its net zero and deforestation-free sourcing commitments, directly impacting bio-based surfactant sourcing. Regional supply capacity improved in November 2025 as BASF expanded surfactant intermediates production in Thailand, strengthening Asian ethoxylation networks. Forward-looking capacity growth continues with BASF confirming start-up of a new U.S. surfactant facility in January 2026, while Nouryon outlined significant investment plans in green ethoxylate innovation, reinforcing the shift toward sustainable, high-performance non-ionic surfactants across global cleaning and personal care markets.

Strategic Market Trends and High-Value Opportunities Reshaping the Alcohol Ethoxylates Market

Market Trend: Global Phase-Out of NPEs Drives Rapid Transition to Biodegradable Linear Alcohol Ethoxylates

The strongest regulatory forcing mechanism in the market is the accelerated elimination of NPEs, driven by environmental and toxicology concerns. Under the U.S. EPA Safer Detergents Stewardship Initiative and TSCA rule changes, approximately 60% of industrial cleaning formulations in North America have already shifted away from NPEs, with replacement driven primarily by linear alcohol ethoxylates. Regulatory scrutiny is accelerating further due to endocrine disruption and aquatic toxicity associated with NPE breakdown intermediates.

Unlike NPEs, which degrade into persistent hydrophobic metabolites, linear alcohol ethoxylates demonstrate greater than 90% biodegradation in municipal wastewater treatment, according to environmental performance assessments published in August 2024. Market change is not only policy-driven; it is commercially reinforced by retailer influence. Walmart’s Chemicals of Concern list now includes NPEs, compelling multinational formulators such as P&G and Unilever to fully eliminate them from laundry detergents and consumer cleaning product portfolios. This retail direction is driving suppliers toward safer, more transparent ingredient systems compatible with labeling claims required for ESG-oriented consumers.

Market Trend: Strategic Decarbonization and Bio-Carbon Integration Transform Ethoxylate Production Models

Decarbonization goals are reshaping capacity planning. Traditional ethoxylate production relied on crude-oil-derived fatty alcohol feedstocks; however, carbon-neutral chemistry is now becoming a regulatory and commercial expectation across home care, personal care, and institutional cleaning. BASF’s November 2025 expansion in Bangpakong, Thailand marks one of the largest global commitments to bio-surfactants, positioning alcohol ethoxylates alongside APGs in a renewable feedstock-based value chain.

In parallel, mass-balance certification is gaining traction as a scalable pathway for Scope 3 reduction without requiring physical separation of renewable and fossil-derived inputs. Shell’s NEODOL portfolio expansion with ISCC PLUS certified solutions enables finished product producers to claim up to 100% bio-based carbon content while using their existing equipment and formulations. Catalytic efficiency is adding another layer of differentiation: Clariant’s chromium-free HySat catalyst platform enables fatty-alcohol production without Cr-VI substances, aligning compliance with EU REACH SVHC phase-outs. These reforms collectively position the sector to deliver low-carbon surfactants at industrial scale, a key procurement criterion for multinational CPGs.

Market Opportunity: Alcohol Ethoxylates as Critical Dispersants for High-Energy-Density Lithium-Ion and Solid-State Batteries

The electrification of transportation, grid storage, and consumer electronics is creating an entirely new industrial-grade demand class for high-purity alcohol ethoxylates. Battery engineering requires uniform electrode slurry composition to enable capacity retention and energy density. Technical disclosures from 2025 battery summits emphasize that ultra-pure ethoxylates act as rheology modifiers supporting 15–20% increases in energy density through optimized dispersion of carbon black and cathode powders.

This opportunity is being catalyzed by the industry shift away from toxic NMP solvents toward water-based cathode processing. Alcohol ethoxylates with precise ethylene-oxide ratios support adhesion of aqueous slurries to copper and aluminum collectors—an essential requirement in high-capacity cathodes and anodes. Because trace contaminants can compromise the Solid Electrolyte Interphase (SEI), electronic-grade ethoxylates must meet thresholds of less than 1 ppm total impurities, an attribute Shell recently positioned as a core differentiator within its NEODOL high-purity portfolio. This segment represents a premium-priced, specification-locked market where long-term supply agreements are anticipated.

Market Opportunity: Precision Agriculture Creates New Demand for Low-Drift, Yield-Enhancing AE Adjuvants

Agriculture is becoming one of the most strategically important demand drivers due to the EU Farm-to-Fork mandate requiring a 50% pesticide-use reduction by 2030. Achieving reductions without reducing yield requires innovations in spray efficiency and deposition control. Alcohol ethoxylates are emerging as foundational ingredients in low-drift adjuvant systems that can reduce spray drift by more than 50 percent, ensuring that active ingredients reach crop surfaces rather than dispersing into surrounding soil and water.

Field trials from 2024–2025 show that AE-based wetting agents support 15–25% pesticide-volume reductions while maintaining yield, helping producers remain profitable while meeting sustainability and residue-limit regulations. Chemical players such as Clariant and Shell are commercializing smaller-chain, C9-C11 ethoxylates for agrochemical systems due to their rapid surface-tension reduction, which is critical for next-generation biologic and low-toxicity pesticides. As crop protection markets shift toward bio-based alternatives, ethoxylates will play a decisive role in enabling formulation performance.

Alcohol ethoxylates are evolving from commodity surfactants into high-performance, compliance-critical formulation components across cleaning chemicals, batteries, and agriculture. Companies positioned with bio-based mass-balance production, electronic-grade quality control, and agrochemical-ready molecular profiles will capture the steepest margin expansion and procurement-locked demand through 2030.

Alcohol Ethoxylates Market Share and Segmentation Insights

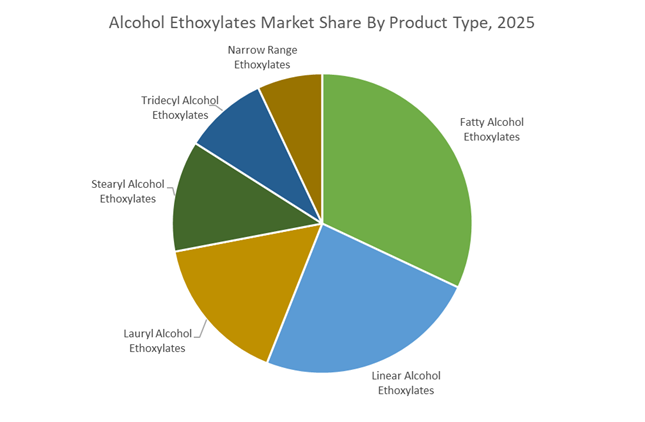

Market Share by Product Type: Fatty Alcohol Ethoxylates Lead as Narrow Range Grades Accelerate

Fatty alcohol ethoxylates account for approximately 32% of global alcohol ethoxylates demand in 2025, supported by their renewable origin from coconut and palm kernel oil, excellent biodegradability, and widespread use in heavy-duty laundry and dishwashing liquids. Sustainability-driven purchasing in Europe and North America, combined with growing emphasis on RSPO-certified supply chains, continues to favor this segment. Linear alcohol ethoxylates rank second, remaining the dominant petrochemical-based option due to superior wetting and degreasing in industrial and institutional cleaners, particularly in emerging markets where natural alcohols carry cost penalties. Lauryl alcohol ethoxylates benefit from premiumization in personal care, while stearyl variants serve niche textile and pharmaceutical uses. Tridecyl alcohol ethoxylates offer cold-water performance but face biodegradability scrutiny. Narrow range ethoxylates are the fastest-growing segment, driven by tighter EO distribution, lower odor, reduced VOCs, and rising adoption in high-performance industrial and sensitive personal care formulations.

Market Share by End-Use Industry: Household Products Dominate While Agrochemicals Drive Growth

Household & personal care represent roughly 41% of alcohol ethoxylates consumption in 2025, anchored by laundry detergents, dishwashing liquids, shampoos, and body washes. The shift toward concentrated formats and pods is increasing demand for high-efficiency, readily biodegradable surfactants aligned with major brand sustainability commitments. Industrial & institutional cleaning ranks second, propelled by the global phase-out of alkylphenol ethoxylates, making alcohol ethoxylates the primary replacement in janitorial, food service, and vehicle wash formulations. Agrochemicals are expanding, with ethoxylates serving as non-ionic emulsifiers and wetting agents in herbicides and adjuvants, although strict ecotoxicity regulations govern formulation choices. Textiles and leather processing remain mature, while oil & gas demand fluctuates with drilling activity. Metalworking fluids form a niche performance segment, and pharmaceuticals, though smallest by volume, deliver the highest margins under USP/NF-grade requirements.

Competitive Landscape: Biomass-Balanced Surfactants and Narrow-Range Ethoxylation Reshaping the Alcohol Ethoxylates Market

The global Alcohol Ethoxylates Market is transitioning from volume-driven commodity surfactants toward low-dioxane, bio-based, and narrow-range ethoxylated systems tailored for personal care, household detergents, agrochemicals, and industrial cleaning. Competitive differentiation increasingly centers on vertical integration into ethylene oxide and fatty alcohols, biomass-balanced feedstocks, and precision ethoxylation that delivers tighter molecular weight distribution and improved biodegradability. Leading producers are accelerating investments in Asia-Pacific and the Americas while embedding circular carbon and renewable raw materials into their portfolios to meet tightening regulatory standards and FMCG sustainability mandates.

BASF SE strengthens ultra-low dioxane ethoxylates through Verbund integration

BASF SE remains the world’s most vertically integrated alcohol ethoxylates producer, leveraging its Verbund manufacturing system to optimize resource efficiency and supply security. In early 2026, BASF expanded its Lutensol® portfolio with ultra-low 1,4-dioxane grades targeting North American personal care formulations under tighter regulatory limits. The company is rapidly scaling Biomass Balanced ethoxylates, replacing fossil feedstocks with renewable inputs at the start of production. Core brands Sokalan® and Lutensol® anchor high-performance laundry and industrial cleaning markets. BASF’s internal EO and fatty alcohol production at Antwerp and Ludwigshafen provides resilience against global feedstock volatility.

Shell Chemicals advances narrow-range ethoxylation with recycled-carbon surfactants

Shell Chemicals differentiates through its proprietary SHOP process, producing highly linear synthetic alcohols for superior biodegradability. Its NEODOL® alcohol ethoxylates deliver rapid wetting and high solubility, making them dominant in premium liquid detergents and cold-water washing capsules. In 2025, Shell integrated carbon-capture technology from LanzaTech, enabling ethoxylate production from recycled emissions via an ethanol-to-ethylene route. Shell’s mastery of narrow-range ethoxylation produces surfactants with tighter molecular weight distribution, lower odor, and improved processing, reinforcing its leadership in high-performance liquid cleaning systems.

Sasol Limited scales dual-track synthetic and bio-based ethoxylates globally

Sasol Limited operates a unique dual-track model combining synthetic and natural fatty alcohols, positioning it as a global powerhouse in alcohol ethoxylates. In 2025, Sasol expanded ethoxylation capacity at Lake Charles and Nanjing to serve fast-growing Asia-Pacific personal care demand. Under its Living Green initiative, Sasol is targeting 50% bio-based alcohols by 2027. NOVEL® and SAFOL® ethoxylates are widely used in agrochemical emulsifiers and oilfield chemicals. Backward integration into both coal-to-liquids and oleochemical alcohols provides pricing stability and feedstock flexibility unmatched by most competitors.

Clariant AG delivers fully bio-based ethoxylates for care chemicals and textiles

Clariant AG has repositioned as a specialty pure player, emphasizing low-carbon, customized alcohol ethoxylates for its Care Chemicals segment. A strategic collaboration with OMV in 2025–2026 secured low-carbon ethylene oxide, reducing the footprint of Clariant’s European ethoxylates by roughly 20%. In 2026, Clariant launched its Eco-Premium range using 100% plant-based EO via its IGL joint venture. The company specializes in tailor-made ethoxylates for textile processing and green crop protection, precisely tuning HLB and foaming profiles to customer specifications.

Indovinya accelerates circular surfactants across the Americas

Indovinya, the surfactants platform of Indorama Ventures, has rapidly climbed global rankings following acquisitions of Huntsman and Oxiteno assets. It now operates one of the most integrated EO-surfactant value chains in the Americas, from natural gas through finished ethoxylates. SURFONIC® and ALKONAT® series dominate Latin American I&I cleaning markets. In 2026, Indovinya launched Circular Surfactants in Brazil using alcohols derived from chemically recycled plastics. Strategically, the company is replacing alkylphenol ethoxylates with biodegradable alcohol ethoxylates in coatings and paints.

Stepan Company boosts North American capacity with energy-efficient ethoxylation

Stepan Company ranks among the top global merchant surfactant producers, known for technical agility and strong FMCG partnerships. In mid-2025, Stepan commissioned a new alkoxylation facility in Pasadena, Texas, expanding capacity for specialty nonionic surfactants. Its BIO-SOFT® ethoxylate blends enable cold-process detergent manufacturing, cutting energy consumption by up to 30%. Proprietary continuous sulfonation and ethoxylation technology delivers higher efficiency and superior color control versus batch processes. Stepan supplies major consumer brands with alcohol ethoxylates for dish soaps, surface cleaners, and shampoos.

United States Alcohol Ethoxylates Market: World-Scale Integration and Domestic Supply Chain Reinforcement

The United States remains the most strategically integrated market for alcohol ethoxylates, anchored by large-scale investments in upstream and downstream capacity. In late 2024, Shell Chemicals finalized the expansion of its Geismar, Louisiana complex, adding a fourth alpha olefin unit that directly supports downstream linear alcohol ethoxylates for the North American detergent sector. This expansion strengthens domestic supply reliability at a time when tariff-related cost pressures are reshaping sourcing decisions.

Product innovation and sustainability are advancing in parallel. Throughout 2024 and 2025, Dow launched a new portfolio of low-VOC alcohol ethoxylates for industrial and institutional cleaning, formulated to meet stringent state-level air quality requirements. Dow also entered renewable feedstock partnerships in March 2024 to develop 100% bio-based alcohol ethoxylates, lowering lifecycle emissions versus petrochemical routes. In agriculture, Stepan Company introduced specialized ethoxylates in early 2024 to improve wetting and spreading performance in herbicide formulations across the U.S. Midwest. Tariff impacts in 2025 increased landed costs from Indonesia and South Africa, accelerating a shift toward domestic sourcing. This trend is reinforced by more than $500 million in smart manufacturing upgrades across the Gulf Coast corridor in 2025, where AI-driven process controls are optimizing ethylene oxide consumption and improving cost efficiency.

Germany Alcohol Ethoxylates Market: Verbund Economics, Biodegradability, and REACH-Driven Innovation

Germany continues to lead Europe in alcohol ethoxylates through integrated production economics and regulatory-driven innovation. In October 2025, BASF outlined intensified investment in its ethylene oxide value chain at Ludwigshafen, scaling non-ionic surfactant capacity with new units scheduled to start through 2026. This Verbund-based integration enhances margin resilience while supporting downstream detergent and specialty formulations.

Product differentiation is increasingly centered on sustainability and performance. BASF launched a readily biodegradable specialty alkoxylate in 2025 for concentrated laundry detergents, designed to deliver strong stain removal at lower wash temperatures of 20 to 30 degrees Celsius. Regulatory compliance is also shaping technology choices, as German manufacturers transition toward chromium-free catalyst platforms such as Clariant’s HySat to align with evolving EU REACH requirements on substances of very high concern. In bio-based surfactants, Clariant expanded its Vita range in 2025, offering 100% bio-based fatty alcohol ethoxylates with a Renewable Carbon Index of 100 for personal care and textile markets. Energy efficiency mandates under Germany’s 2025 Energy Efficiency Act further strengthened competitiveness, with BASF reporting around four million euros in annual savings from improved steam utilization at its ethoxylation and EO assets.

India Alcohol Ethoxylates Market: Ethanol Surplus, Industrial Parks, and Export Readiness

India is emerging as a structurally attractive production base for alcohol ethoxylates, supported by feedstock availability and policy-driven industrialization. In August 2025, the Ministry of Petroleum and Natural Gas accelerated the Ethanol Blending Program, creating a significant surplus of ethanol feedstock that incentivizes domestic production of ethyl alcohol-based ethoxylates. This shift is reducing dependence on imported fatty alcohol intermediates while improving cost competitiveness.

Industrial policy is reinforcing this momentum. The Make in India initiative has driven the establishment of three specialty chemical parks in Gujarat, purpose-built to host ethoxylation units serving textile and leather processing clusters. Regulatory alignment is also advancing export potential. In 2025, the Bureau of Indian Standards updated surfactant quality benchmarks to align with global ISO norms, easing market access for Indian-made alcohol ethoxylates into Europe and North America. These developments position India as both a domestic consumption hub and an export-oriented manufacturing platform.

South Africa Alcohol Ethoxylates Market: Feedstock Security and Global Logistics Optimization

South Africa plays a critical role in the global alcohol ethoxylates supply chain through upstream alcohol production and export logistics. In its September 2025 production and sales metrics, Sasol reported that its Chemicals segment now accounts for 57% of total production volumes, underscoring a strategic shift away from fuels toward higher-value chemical feedstocks.

Operational reconfiguration at Secunda is central to this strategy. Sasol is prioritizing chemical intermediates such as C12 to C15 alcohols to ensure stable supply for global ethoxylation partners through 2026. On the logistics front, late-2025 changes in export vessel scheduling were implemented to improve delivery reliability to European and Asian markets during peak seasonal demand. While coal quality challenges persist upstream, the pivot toward chemicals enhances South Africa’s relevance as a feedstock anchor for the global surfactants industry.

South Korea Alcohol Ethoxylates Market: Textile Efficiency and Environmental Leadership

South Korea’s alcohol ethoxylates market is characterized by application-specific innovation and strong environmental governance. In early 2024, LG Chem introduced a tailored alcohol ethoxylate for industrial laundry in the textile sector. The formulation reduces water and energy consumption by 15% during scouring and bleaching, aligning with sustainability goals in textile manufacturing.

Environmental performance is becoming a competitive differentiator at the national level. South Korea-linked producers, including Indorama Ventures with significant ethoxylation assets, ranked first globally in the ChemScore 2025 index for chemicals management and safety. This recognition strengthens buyer confidence in South Korean supply, particularly for export markets with stringent environmental and social governance requirements.

Country-Level Positioning in the Alcohol Ethoxylates Industry

Alcohol Ethoxylates Market County Level Snapshot

|

Country

|

Strategic Focus Area

|

Market Implication

|

|

United States

|

World-scale AO integration, low-VOC and bio-based innovation

|

Margin resilience and domestic supply security

|

|

Germany

|

Verbund economics, biodegradable and REACH-compliant surfactants

|

Premium sustainable formulations

|

|

India

|

Ethanol surplus, chemical parks, ISO alignment

|

Cost-competitive production and export growth

|

|

South Africa

|

C12–C15 alcohol feedstocks, logistics optimization

|

Global feedstock reliability

|

|

South Korea

|

Textile efficiency, ESG leadership

|

High-value niche applications and buyer trust

|

Alcohol Ethoxylates Market Report Scope

Alcohol Ethoxylates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.5 Billion

|

|

Market Size (2034)

|

$11.2 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Type (Fatty Alcohol Ethoxylates, Lauryl Alcohol Ethoxylates, Linear Alcohol Ethoxylates, Stearyl Alcohol Ethoxylates, Tridecyl Alcohol Ethoxylates, Narrow Range Ethoxylates), By Feedstock (Natural and Vegetable Based Feedstocks, Synthetic Petrochemical Based Feedstocks, Bio Based and Renewable Feedstocks), By End Use Industry (Household and Personal Care, Industrial and Institutional Cleaning, Agrochemicals, Textiles and Leather Processing, Oil and Gas, Pharmaceuticals, Metalworking Fluids), By Application (Emulsifiers, Detergents and Cleansing Agents, Wetting Agents, Dispersing Agents, Foaming Agents)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Shell plc, Sasol Limited, Clariant AG, Stepan Company, Dow Inc., Indorama Ventures Public Company Limited, Evonik Industries AG, Huntsman Corporation, INEOS Group Limited, Croda International Plc, Solvay SA, LG Chem Ltd, Kao Corporation, India Glycols Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Alcohol Ethoxylates Market Segmentation

By Product Type

- Fatty Alcohol Ethoxylates

- Lauryl Alcohol Ethoxylates

- Linear Alcohol Ethoxylates

- Stearyl Alcohol Ethoxylates

- Tridecyl Alcohol Ethoxylates

- Narrow Range Ethoxylates

By Feedstock

- Natural and Vegetable Based Feedstocks

- Synthetic Petrochemical Based Feedstocks

- Bio Based and Renewable Feedstocks

By End Use Industry

- Household and Personal Care

- Industrial and Institutional Cleaning

- Agrochemicals

- Textiles and Leather Processing

- Oil and Gas

- Pharmaceuticals

- Metalworking Fluids

By Application

- Emulsifiers

- Detergents and Cleansing Agents

- Wetting Agents

- Dispersing Agents

- Foaming Agents

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Alcohol Ethoxylates Industry

- BASF SE

- Shell plc

- Sasol Limited

- Clariant AG

- Stepan Company

- Dow Inc.

- Indorama Ventures Public Company Limited

- Evonik Industries AG

- Huntsman Corporation

- INEOS Group Limited

- Croda International Plc

- Solvay SA

- LG Chem Ltd

- Kao Corporation

- India Glycols Limited

*- List not Exhaustive