Ethoxylates Market to Reach $34.5 Billion by 2034 as Green Surfactants and Regulatory Standards Reshape Global Supply

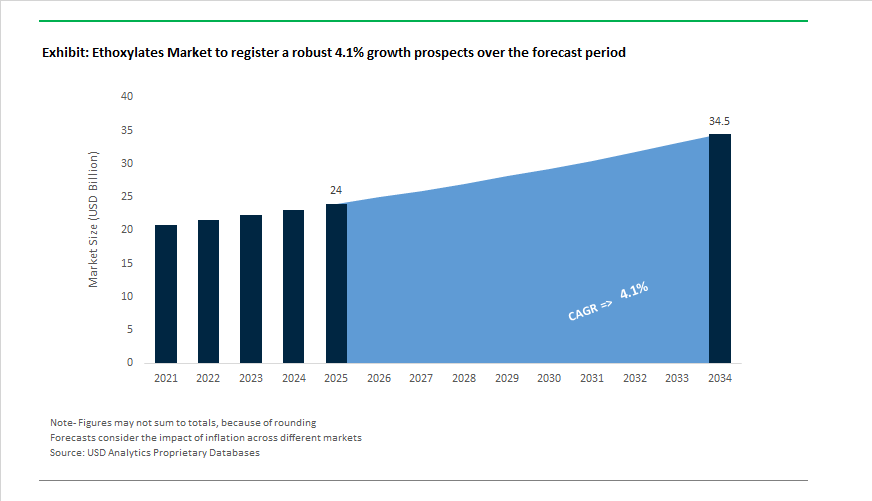

The Ethoxylates Market is projected to expand from $24 billion in 2025 to $34.5 billion by 2034, growing at a CAGR of 4.1%, driven by structural demand in household detergents, agrochemicals, oilfield chemicals, and personal care formulations. The market is transitioning from volume-led commodity growth to performance- and sustainability-driven differentiation. Non-ionic ethoxylates, particularly fatty alcohol ethoxylates, remain foundational to global cleaning chemistry due to their superior wetting, emulsification, and detergency properties across hard and soft water systems. However, increasing regulatory scrutiny on ethylene oxide derivatives and tightening sustainability mandates are accelerating investment in green ethoxylate platforms and traceable supply chains.

A pivotal milestone occurred in June 2024 when Nouryon secured ISCC PLUS certification for its Stenungsund, Sweden site. This certification enables the production of green ethylene oxide and downstream green ethoxylated surfactants using mass-balance renewable feedstocks. The move directly supports multinational home care and institutional cleaning brands seeking measurable reductions in product carbon footprint. The sustainability narrative strengthened further when Nouryon received the 2025 Sustainability Award from Henkel at the 2026 American Cleaning Institute meeting, recognizing its degradable ethoxylate systems optimized for water hardness management in advanced laundry detergents. These developments underscore the strategic shift toward biodegradable and low-carbon surfactant chemistries in North America and Europe.

Asia remains the dominant growth engine. The BASF–Sinopec joint venture BASF-YPC ramped up expanded ethylene oxide and downstream ethoxylate capacity at its Nanjing Verbund site in Q2 2024, targeting East Asia’s surging demand for non-ionic surfactants in personal care and industrial cleaning. Meanwhile, India Glycols Limited approved a strategic demerger in November 2025, retaining its Chemicals Business—including ethoxylates—while separating spirits and bio-pharma assets. This restructuring enables sharper capital allocation toward high-margin green chemistry, particularly bio-based ethoxylates. India also extended Quality Control Order (QCO) enforcement to September 12, 2026, granting manufacturers time to align with Bureau of Indian Standards purity benchmarks. The regulatory calibration is expected to elevate domestic production quality while restricting substandard imports.

Strategic repositioning among global producers is reshaping competitive dynamics. Huntsman Corporation announced a biotechnology alliance in November 2025 to develop renewable fatty alcohol ethoxylates derived from bio-based feedstocks, responding to growing demand for plant-based surfactants in consumer goods. Sasol Chemicals updated its 2025 strategy to prioritize specialty surfactants and margin optimization, citing strong ethoxylate volumes in the U.S. and Eurasia. Clariant initiated a CHF 80 million savings program, consolidating Care Chemicals operations to defend margins amid European demand softness. In parallel, SABIC divested its European petrochemical business to AEQUITA in January 2026, signaling a pivot away from commodity derivatives toward higher-growth engineering plastics and circular materials.

Sustainability leadership is becoming a competitive differentiator. Indorama Ventures, through its Indovinya platform, ranked first globally in ChemScore 2025 for chemical safety and environmental stewardship, reinforcing its credibility in non-hazardous surfactant innovation. Concurrently, India Glycols reported that its bio-based chemical segment delivered a 33% EBITDA increase in H1 FY26, benefiting from India’s 20% biofuel blending target, which enhances feedstock economics for green ethoxylates.

Trends and Opportunities in the Ethoxylates Market

Accelerated Shift to Renewable Carbon and CO₂-Derived Feedstocks

- Ethoxylate producers are moving decisively beyond conventional palm and coconut oil dependence toward renewable carbon and captured CO₂ integration. This shift is not cosmetic but structural, aimed at reducing Scope 3 emissions and future-proofing surfactant portfolios against tightening lifecycle carbon scrutiny.

- In June 2025, Econic Technologies commercialized its Recreaire® platform, introducing carbonate ethoxylates incorporating up to 45% captured CO₂ by weight. These surfactants deliver biodegradability comparable to fatty alcohol ethoxylates while achieving up to a 65% reduction in Global Warming Potential, directly aligning with multinational FMCG carbon budgets.

- Parallel circularity strategies are emerging at scale. Through collaboration with LanzaTech Global, Dow introduced the EcoSense™ 2470 Surfactant during 2024–2025. By using recycled industrial carbon as a feedstock, Dow is effectively decoupling ethoxylate production from virgin fossil inputs without sacrificing detergency or foam control, a key requirement for home care and institutional cleaning customers.

- At the upstream level, bio-based ethylene oxide is becoming a competitive differentiator. Producers such as Croda and BASF are scaling 100% bio-EO deployment, enabling ethoxylates that qualify under the USDA BioPreferred Program. This is strategically important as U.S. federal procurement mandates increasingly favor verified bio-based surfactants, locking in long-term institutional demand.

Mandatory Phase-Out of Alkylphenol Ethoxylates and NPE Substitution

- Regulatory enforcement has removed discretion from the transition away from alkylphenol ethoxylates, particularly nonylphenol ethoxylates. The shift is now compliance-driven rather than customer-led, accelerating substitution cycles across textiles, industrial cleaning, and emulsification.

- By November 2025, EU REACH registration fees had risen by nearly 20 %, reflecting expanded toxicological testing and administrative burdens for substances of concern. Simultaneously, Annex XVII enforcement and the EU Chemicals Industry Action Plan effectively eliminated NPEs from textile processing and industrial detergents. Similar pressure is emerging under U.S. EPA safer chemistry initiatives, compressing timelines for global formulation changes.

- Secondary alcohol ethoxylates are emerging as the primary beneficiaries. Global capacity for specialized branched SAE structures reached approximately 30,000 tons by April 2025, driven by their superior grease removal, rapid biodegradation, and improved low-temperature solubility compared with the APEOs they replace. These performance gains are critical for industrial users operating under colder wash cycles and reduced energy inputs.

Low-Foam Ethoxylates for Automated and Low-Energy CIP Systems

- The modernization of Clean-in-Place systems across dairy, beverage, and food processing facilities is creating a structurally attractive niche for low-foam nonionic ethoxylates. As plants transition to automated, closed-loop cleaning and renewable energy heating, surfactant performance under high turbulence has become mission-critical.

- In December 2025, a turnkey CIP upgrade delivered by INOXPA for a major UK food producer demonstrated that low-foam ethoxylate systems enable effective sanitation at reduced temperatures. This directly supports zero-carbon processing goals by lowering thermal energy demand while avoiding foam-induced pump cavitation and sensor interference.

- Low-foam surfactants already accounted for roughly 65% of the nonionic ethoxylate segment in early 2025, and their formulation is increasingly optimized using AI-driven modeling. These tools maximize protein and fat removal efficiency while preserving compatibility with automated conductivity and turbidity sensors used in modern CIP architectures.

- With food and beverage applications representing about 40% of global CIP detergent revenue in 2025, ethoxylate suppliers offering high-solvency, low-impact molecules are positioned for stable, regulation-resilient growth.

Advanced Ethoxylated Adjuvants for Biological and Precision Agrochemicals

- Agriculture is rapidly shifting toward biological actives, reduced application volumes, and precision spraying, creating demand for ethoxylates that function as high-efficiency adjuvants rather than commodity surfactants.

- In October 2025, Indovinya launched the SURFOM® ETHOS range, specifically engineered for biologically based crop protection formulations. These ethoxylates stabilize microbial and enzyme-based actives while ensuring consistent leaf wetting and adhesion under variable field conditions.

- For conventional herbicides, ethoxylates remain indispensable penetration enhancers. Research published in 2025 shows that ethoxylated fatty amines significantly improve systemic uptake in waxy-leaf species, allowing formulators to reduce total active ingredient loading without compromising efficacy. This directly supports regulatory targets to lower chemical intensity while preserving yield outcomes.

- As global agrochemical leaders such as Syngenta and Corteva continue investing in high-efficacy, low-dose products, ethoxylates that deliver precision, rainfastness, and compatibility with biologicals represent one of the most defensible growth avenues in the surfactants value chain.

Ethoxylates Market Share and Segmentation Insights

Alcohol Ethoxylates Dominate Non-Ionic Surfactant Consumption Across Cleaning and Industrial Uses

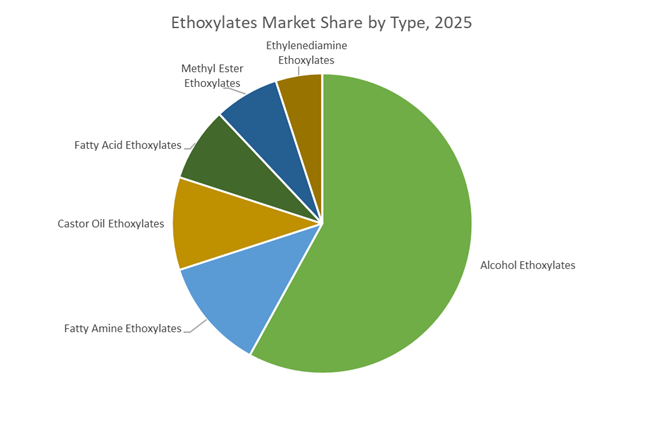

Alcohol ethoxylates command approximately 58% of total ethoxylates market share in 2025, reflecting their status as the primary non-ionic surfactants for detergents, household cleaners, and industrial formulations. Their strong wetting, emulsifying, and detergency characteristics, combined with favorable biodegradability profiles, make them indispensable in laundry, dishwashing, and hard surface cleaning products. Fatty amine ethoxylates represent a significant secondary segment, valued for corrosion inhibition and antistatic performance in agrochemicals, textiles, and metalworking. Castor oil ethoxylates maintain importance in personal care and pharmaceutical applications where mildness and compatibility with sensitive ingredients are required. Fatty acid ethoxylates remain steady in industrial emulsification, while methyl ester ethoxylates are gaining traction as sustainable alternatives in detergents. Ethylenediamine ethoxylates serve niche roles in chelation and dispersion for specialty chemical applications.

Household and Personal Care Drives Nearly Half of Global Ethoxylate Demand

Household and personal care account for roughly 48% of ethoxylates consumption in 2025, led by widespread use in laundry detergents, dishwashing liquids, and personal hygiene products requiring reliable cleaning efficacy and foam control. Industrial and institutional cleaning forms a major secondary segment, utilizing ethoxylates in degreasers and sanitizers for healthcare, food service, and commercial environments. Agrochemicals represent an important application area, employing ethoxylates as wetting agents and emulsifiers to improve pesticide stability and crop coverage. Textiles and leather processing rely on ethoxylates for scouring, dye leveling, and finishing operations. Oil and gas applications remain steady through demulsifiers and corrosion inhibitors, while pharmaceuticals and biotechnology occupy a smaller but high-value niche, demanding high-purity ethoxylates for excipients and drug delivery systems.

Competitive Landscape of the Ethoxylates Market

The global ethoxylates market in 2026 is defined by large-scale ethylene oxide integration, bio-based surfactant innovation, and tightening regulatory limits on dioxane and carbon intensity, with multinational chemical leaders competing across home care, personal care, agrochemicals, battery materials, and industrial detergents.

BASF commands 26.9% global alcohol ethoxylates share through biomass-balanced integration

BASF SE leads the ethoxylates market with a 26.9% global share in alcohol ethoxylates as of 2026, supported by €59.7 billion in 2025 sales and a high-margin Care Chemicals division. Leveraging its Verbund integration, BASF controls feedstocks from ethylene oxide to finished surfactants. In early 2026, it scaled Lutensol® ultra-low dioxane grades to meet stringent 1 ppm limits in California and New York detergent regulations. Under Chairman Markus Kamieth’s Winning Ways strategy, BASF is prioritizing Product Carbon Footprint transparency for every batch. Its biomass-balanced platform replaces fossil carbon with renewable inputs from the start of ethoxylation, strengthening its ESG leadership.

Dow restructures assets to accelerate bio-based and battery-grade ethoxylates

Dow Inc. remains a North American powerhouse, advancing multifunctional alcohol ethoxylates for coatings, electronics, and energy storage. In January 2026, Dow launched its Transform to Outperform plan targeting a $2 billion EBITDA uplift through AI-enabled manufacturing and asset optimization, including 4,500 role reductions. The company is prioritizing ECOSURF™ and TERGITOL™ grades, with Ecolibrium bio-based ethoxylates gaining traction in premium coatings. Dow also confirmed the shutdown of energy-intensive European upstream assets in Böhlen and Schkopau to focus on high-margin derivatives. Increasingly, its high-purity ethoxylates serve as dispersants in lithium-ion and solid-state battery electrode formulations.

Clariant advances 100% bio-based VITA ethoxylates in Asia-Pacific

Clariant AG is positioning itself as the sustainability specialist in ethoxylation, rapidly expanding plant-based production. In late 2025, Clariant completed an CHF 80 million expansion at its Daya Bay site in China, doubling ethylene oxide derivatives and pharmaceutical-grade ethoxylate capacity. Its VITA portfolio offers 100% bio-based alcohol ethoxylates with a Renewable Carbon Index of 100%. The company introduced a chromium-free catalyst system in 2025 to improve environmental safety in narrow-range ethoxylate production. Daya Bay now operates as Clariant’s integrated multi-purpose plant for APAC personal care and pharmaceutical customers, reinforcing its leadership in green surfactants.

Shell commercializes recycled-carbon NEODOL ethoxylates for agrochemical efficiency

Shell plc leverages its global petrochemical footprint to supply high-volume synthetic and bio-hybrid alcohol ethoxylates. Its NEODOL® series remains a benchmark for linear alcohol ethoxylates, offering biodegradability above 80% linearity. In 2026, Shell expanded ISCC PLUS certified bio-based NEODOL grades using mass-balance methods to reduce carbon intensity. The company also commercialized recycled-carbon surfactants derived from plastic-waste syngas feedstocks. Shell’s ethoxylates are widely specified in agrochemical adjuvants, enabling 15% to 25% reductions in pesticide application volumes while maintaining crop yield, reinforcing its performance and sustainability positioning.

Sasol strengthens dual-track natural and synthetic ethoxylate supply security

Sasol Limited operates one of the industry’s most versatile platforms, producing both synthetic and natural alcohol ethoxylates. Reporting R122.4 billion turnover in H1 FY26 with a 1.6x net debt to EBITDA ratio, Sasol maintained stability during a volatile cycle. In early 2026, it secured 300 MW of renewable energy to decarbonize its Secunda ethoxylation operations. Its dual-track sourcing strategy supports FMCG leaders such as Unilever, ensuring resilience against palm oil price volatility. Sasol captured additional share in the narrow-range ethoxylate segment, achieving a 3% sales volume increase in early 2026, particularly in low-foaming industrial detergent applications.

Germany: Verbund Optimization and Regulatory-Led Formulation Leadership

Germany continues to anchor the European ethoxylates market through deep integration, regulatory stewardship, and premium formulation innovation. BASF is executing a multi-year optimization of its ethylene oxide value chain, concentrating non-ionic surfactant production at its Ludwigshafen and Antwerp Verbund sites by 2026. This consolidation enhances backward integration, reduces logistics intensity, and improves cost resilience amid volatile European energy pricing. BASF disclosed annual savings of €65 million in late 2025 driven by continuous catalyst upgrades and advanced process control across its EO assets, underscoring the role of digital operations in sustaining competitiveness.

On the product side, Germany remains the primary testing ground for next-generation biodegradable ethoxylate formulations under the 2026 REACH recast, with a particular focus on minimizing trace 1,4-dioxane content. In parallel, innovation is moving beyond conventional ethoxylates. At in-cosmetics Global in April 2025, BASF introduced Lamesoft® OP Plus, a wax-based, readily biodegradable opacifier dispersion positioned as an ethoxylate-free alternative for responsible beauty formulations. Local producers are also increasingly adopting bio-attributed ethylene oxide using mass-balance approaches to supply lower-carbon ethoxylates to the premium European household and personal care sectors, reinforcing Germany’s leadership in sustainable surfactant chemistry.

United States: Bio-Attributed EO Scaling and Specialty Manufacturing Pivot

The U.S. ethoxylates market in 2025–2026 is characterized by rapid bio-feedstock commercialization and a decisive shift toward specialty and contract manufacturing. INEOS Oxide entered a major scale-up phase for bio-attributed ethylene oxide in 2025, sourcing renewable residues to deliver a feedstock with more than 100% greenhouse gas reduction versus fossil-derived EO. This material is becoming a critical input for next-generation U.S.-manufactured ethoxylates aimed at meeting retailer and brand owner decarbonization commitments.

Specialty demand is further reinforced by downstream technology sectors. Huntsman Corporation inaugurated its E-GRADE® unit in Conroe, Texas in May 2025, supplying high-purity amines and alkoxylates for advanced semiconductor manufacturing and AI server cleaning applications. According to the SOCMA 2026 Outlook, ethoxylation demand among U.S. specialty chemical firms has nearly doubled since 2024, accelerating capital deployment toward automated, GMP-compliant production lines. Regulatory pressure is also reshaping product portfolios. The U.S. EPA’s tightened 1,4-dioxane guidelines for 2025–2026 are driving a rapid transition toward stripped ethoxylates in laundry detergents. At the same time, Eastman Chemical Company and peers implemented global price increases effective January 1, 2026 to fund carbon capture and decarbonization infrastructure. Sustained investment in the Permian Basin is additionally boosting demand for alcohol ethoxylates used in enhanced oil recovery and corrosion inhibition.

India: Capacity Build-Out and Bio-Feedstock Security

India’s ethoxylates market is expanding through domestic capacity additions and bio-feedstock availability aligned with national fuel policy. In October 2025, Bhageria Industries commenced commercial production of a new ethoxylate and plasticizer line at its Tarapur facility after receiving environmental clearance from the Maharashtra Pollution Control Board. This marks a significant step toward import substitution in non-ionic surfactants for detergents, agrochemicals, and industrial formulations.

Policy-driven demand is reinforcing this expansion. The Department of Chemicals and Petrochemicals has reported rising domestic output of tallow amine ethoxylates to support India’s ambition of becoming a global hub for generic pesticide formulations by 2026. The Ministry of Petroleum and Natural Gas advanced the E20 ethanol blending target to the 2025–26 supply year, increasing the requirement for ethoxylate-based corrosion inhibitors compatible with high-ethanol gasoline. Feedstock security is further strengthened by the allocation of 52 lakh metric tonnes of surplus FCI rice for ethanol production in 2025–26, ensuring a stable bio-derived input stream for ethoxylation plants. Complementing this, the Rs. 28,602 crore PLI scheme for specialty chemicals is funding three new world-scale ethoxylation units aimed at structurally reducing reliance on imported surfactants.

China: Smart Verbund Scale and Bio-Based Differentiation

China’s ethoxylates landscape is being reshaped by large-scale integration and a gradual pivot toward green exports. BASF is progressing toward full completion of its Zhanjiang Smart Verbund by late 2026, including a dedicated non-ionic surfactants unit powered entirely by renewable electricity. The site’s highly automated logistics and integrated utilities position it as a benchmark for low-emission ethoxylate production serving domestic and Asia-Pacific demand.

To address overcapacity in basic chemicals, producers in the Guangdong cluster are investing in bio-based ethylene oxide derived from corn and sugarcane residues. This strategy targets export-grade green surfactants for multinational FMCG customers. In parallel, Sinopec and regional partners expanded high-purity ethoxylate lines in Nanjing in late 2025 to support the 2026 ramp-up of advanced node semiconductor lithography, signaling a clear move toward electronics-grade solvent and cleaning applications.

Saudi Arabia: Electrification-Oriented Specialties and Oilfield Synergies

Saudi Arabia is aligning ethoxylate development with electrification and energy transition priorities. SABIC has positioned specialized ethoxylates as part of its BlueHero™ initiative, focusing on applications in EV battery thermal management fluids and high-voltage insulation materials for the 2025–2026 cycle. This reflects a strategic shift from purely volume-driven surfactants toward performance-critical specialties.

Upstream scale continues to underpin this transition. The Petrokemya affiliate project, which reached 95% completion in August 2025, is scheduled to achieve full ethoxylation throughput in the first quarter of 2026. The complex is designed to supply global oilfield chemicals and gas treatment markets, reinforcing Saudi Arabia’s role as a competitive export base while supporting downstream diversification into higher-value ethoxylate derivatives.

Strategic Snapshot: Ethoxylates Market by Country

Ethoxylates Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key End-Use Focus

|

Structural Direction

|

|

Germany

|

Verbund consolidation and REACH leadership

|

Personal care, household surfactants

|

Premium, low-dioxane formulations

|

|

United States

|

Bio-attributed EO and specialty manufacturing

|

Semiconductors, detergents, oilfield

|

High-purity and contract production

|

|

India

|

Domestic capacity and ethanol policy

|

Agrochemicals, fuels, detergents

|

Import substitution with bio-feedstocks

|

|

China

|

Smart Verbund scale and green exports

|

FMCG, semiconductors

|

Integrated, low-carbon expansion

|

|

Saudi Arabia

|

Electrification and oilfield synergy

|

EV fluids, gas treatment

|

Specialty-led diversification

|

Ethoxylates Market Report Scope

Ethoxydiglycol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1015 Million

|

|

Market Size (2034)

|

$1574.6 Million

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Type (Cosmetic Grade, Pharmaceutical Grade, Industrial Grade), By Functionality (Solubilizers and Co-Solvents, Humectants and Skin-Conditioning Agents, Penetration Enhancers, Viscosity Modifiers, Fragrance Fixatives), By Application (Skin Care, Hair Care, Sun Care, Pharmaceuticals, Personal Hygiene, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Huntsman Corporation, Clariant AG, Croda International Plc, Eastman Chemical Company, INEOS Oxide, LyondellBasell Industries N.V., India Glycols Limited, Arakawa Chemical Industries, Ltd., Givaudan SA, Alzo International Inc., Guangdong KOMO Co., Ltd., Finetech Industry Limited, Merck KGaA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethoxylates Market Segmentation

By Type

- Alcohol Ethoxylates

- Fatty Amine Ethoxylates

- Fatty Acid Ethoxylates

- Ethylenediamine Ethoxylates

- Methyl Ester Ethoxylates

- Castor Oil Ethoxylates

By End-Use Industry

- Household and Personal Care

- Agrochemicals

- Oil and Gas

- Pharmaceuticals and Biotechnology

- Industrial and Institutional Cleaning

- Textiles and Leather Processing

By Function

- Emulsifiers and Dispersants

- Wetting Agents

- Foaming and Defoaming Agents

- Solubilizers

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethoxylates Industry

- BASF SE

- Dow Inc.

- Clariant AG

- Huntsman International LLC

- INEOS Oxide

- SABIC

- Sasol Limited

- Nouryon

- Evonik Industries AG

- Shell Chemicals

- Kao Corporation

- Croda International Plc

- India Glycols Limited

- Stepan Company

- Wilmar International Limited

*- List not Exhaustive