Methyl Ester Ethoxylates Market 2025–2034: Biodegradability Mandates, Low-Foaming I&I Surfactants, and Oleochemical Integration Driving $362.8 Million Outlook at 4.2% CAGR

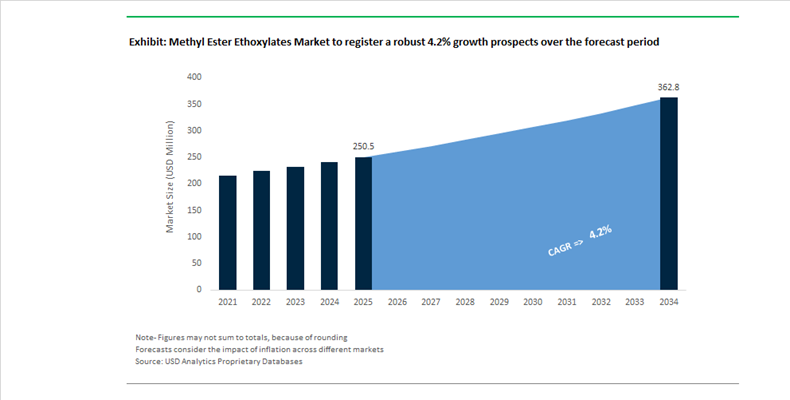

The Methyl Ester Ethoxylates (MEE) Market is projected to grow from $250.5 Million in 2025 to $362.8 Million by 2034, registering a CAGR of 4.2%. Market expansion is being shaped by tightening biodegradability regulations, growing institutional hygiene standards, and the shift toward bio-based, low-foaming nonionic surfactants in consumer and industrial cleaning applications. MEE, derived primarily from palm- or vegetable-based methyl esters through ethoxylation, offers superior soil suspension, improved rinsability, and inherently favorable OECD 301 biodegradability performance compared to traditional surfactants such as linear alkylbenzene sulfonates. Increasing demand for water-efficient and energy-saving detergent formulations across hospitality, healthcare, and commercial laundry sectors is reinforcing the strategic relevance of MEE chemistry.

In 2024, the European Commission proposed a surfactant biodegradability mandate requiring ultimate biodegradation within 28 days under OECD 301 standards, accelerating reformulation efforts toward MEE-based systems across Europe. During the same year, India Glycols reported a surge in bio-based ethoxylate shipments following strengthened hygiene mandates in public institutions, while KLK OLEO expanded logistics capacity with the opening of Terminal 2 at Stolthaven Westport, strengthening global supply of palm-derived feedstocks for methyl ester sulfonates and ethoxylates. In its 2024 annual disclosures, Kao Corporation introduced a one-pass institutional detergent enhanced with MEE, engineered to reduce rinse cycles and lower water and energy consumption in commercial laundering.

Cost dynamics and performance innovation intensified in 2025. In February 2025, Indorama Ventures implemented price increases on monoethylene glycol and diethylene glycol feedstocks, impacting ethoxylation economics and encouraging optimized, lower-dosage MEE blends. In early 2025, Clariant launched a cosmetic-grade ethoxylate line incorporating MEE-inspired chemistry to enhance mildness and emulsification, reporting integration into a significant portion of new European beauty product launches. In August 2025, Kao inaugurated a new U.S. tertiary amine facility supporting localized green intermediate production for high-performance surfactants. In October 2025, Stepan introduced low-foaming ethoxylates for Industrial & Institutional cleaning, responding to increased North American adoption of upgraded MEE-based formulations. In December 2025, Indorama Ventures ranked first in ChemScore 2025, reinforcing sustainable supply credentials, while Lion Corporation reported profitability gains in fabric care through super-concentrated liquid detergents leveraging MEE for high cleaning efficiency at reduced dosage levels.

Methyl Ester Ethoxylates (MEE) Market Trends and Opportunities

Trend: Capacity Expansion for High-Purity MEEs in Ultra-Concentrated Home Care Formulations

The Methyl Ester Ethoxylates market is being reshaped by the rapid shift toward ultra-concentrated and water-efficient home care products, where surfactant performance must be delivered at significantly lower use levels. As brands pursue compact liquids and waterless formats to meet cold-wash and water stewardship targets, MEEs in the C12–C14 and C16–C18 ranges are gaining prominence due to their strong detergency, rapid biodegradability, and favorable cold-water solubility profiles. These attributes directly align with long-term sustainability frameworks such as the LION Eco Challenge 2050, which emphasize reduced water and energy use across the cleaning lifecycle.

Corporate R&D investment is accelerating this transition. In August 2025, Lion Corporation relaunched its NANOX one detergent platform, leveraging high-purity methyl ester derivatives within an advanced enzyme–surfactant system. The formulation targets deep-root bacterial soils while maintaining low environmental impact, reinforcing Lion’s position on the CDP Water Security A List for the fifth consecutive year. Parallel capacity expansion is underway in North America. Kao Chemicals commissioned a new tertiary amine and specialty surfactant facility in Texas in August 2025, designed specifically to support bio-based surfactants for compact liquid detergents.

From a performance standpoint, advances in ethoxylation technology are enabling narrow-range MEEs with less than 0.5% unreacted alcohol. This level of purity is critical for preventing hazing in clear formulations and ensuring rapid biodegradation, positioning MEEs as a preferred surfactant class under the EU’s 2025–2032 green chemistry roadmap.

Trend: Mandatory APEO Substitution in Industrial and Institutional Cleaning

The global phase-out of alkylphenol ethoxylates has moved from voluntary substitution to mandatory compliance across industrial and institutional cleaning supply chains. MEEs have emerged as the leading drop-in alternative, offering comparable hydrophilic–lipophilic balance values while delivering markedly superior ecotoxicity and biodegradation profiles.

Regulatory pressure intensified in June 2025 with the adoption of Commission Regulation (EU) 2025/1090 under REACH Annex XVII, signaling a broader enforcement wave against persistent surfactants. Industrial cleaning products exceeding the 0.1% APEO threshold now face exclusion from the European Economic Area, forcing formulators to accelerate reformulation timelines. In response, Stepan Company introduced a new generation of low-foaming ethoxylates in early 2025. Company disclosures indicate that more than one-third of new industrial cleaning products launched in North America since 2020 now incorporate MEE-based systems to meet EPA Safer Choice criteria.

Institutional adoption is further reinforced by procurement standards. The EPA’s Safer Chemical Ingredients List update in September 2025 continues to classify ethoxylated esters as Green Circle ingredients, making them a prerequisite for contracts in hospitals, schools, and government facilities. This has effectively converted regulatory compliance into a structural demand driver for MEEs across the I&I segment.

Opportunity: Low-Foam MEEs for Food and Beverage Clean-in-Place Systems

Automated Clean-in-Place systems in food and beverage processing are creating a high-value opportunity for low-foam, high-detergency MEEs. These systems require surfactants that deliver effective soil removal while minimizing foam generation to reduce rinse times, water consumption, and energy load.

In March 2025, NSF guidance reiterated that product registration is essential for acceptance in food processing environments, accelerating the uptake of NSF/ANSI-compliant MEE formulations in breweries and dairy plants. MEEs demonstrate effective cleaning performance at temperatures as low as 40°C, materially lowering the thermal intensity of CIP cycles. Environmental disclosures published in December 2025 by leading chemical suppliers show that MEE-based low-foam systems can cut rinse water usage by up to 20% compared with traditional sulfonate surfactants, a decisive advantage in water-stressed regions such as the U.S. Southwest and Northern India.

Sustainable sourcing is becoming equally critical. In March 2025, Kao Chemicals secured alternative palm-oil feedstocks through an agreement with Future Origins, ensuring deforestation-free inputs for food-grade MEE cleaners and compliance with the EU Deforestation Regulation.

Opportunity: Multi-Functional MEEs as Agricultural Adjuvants for Drift Reduction

Precision agriculture and UAV-based spraying are opening a differentiated growth avenue for MEEs as multi-functional adjuvants that combine wetting, penetration, and drift control in a single formulation. As farms adopt drone spraying and variable-rate application to reduce chemical use, demand is rising for surfactants that enhance efficacy while limiting off-target movement.

In the United States, precision agriculture adoption has reached 27% of farms, driving uptake of UAV-ready adjuvant systems. MEEs used in products such as UPL’s Li-1000 act as integrated surfactant–penetrant–drift retardants, ensuring that high-cost actives reach the leaf surface efficiently. Improved leaf wetting enabled by MEEs can increase active ingredient absorption by up to 15%, supporting compliance with tightening Maximum Residue Limits across the EU, where pesticide sales declined nearly 10% in 2023.

Beyond conventional crop protection, MEEs are increasingly favored in agricultural biologicals and regenerative agriculture. Their biocompatibility ensures they do not impair microbial biostimulants or biofungicides, positioning MEEs as the preferred sticker-spreader technology for low-residue, sustainability-aligned farming systems.

Methyl Ester Ethoxylates Market Share and Segmentation Insights

Palm Oil–Based Feedstocks Lead Methyl Ester Ethoxylates Market Due to Cost Efficiency and Surfactant Performance

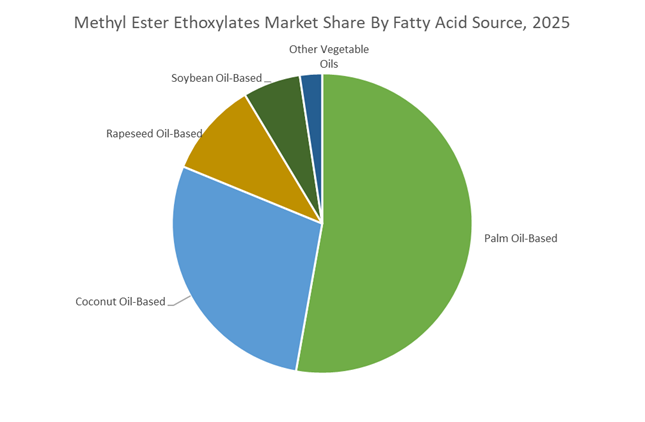

Palm oil–based methyl ester ethoxylates (MEE) accounted for 52.80% of the Methyl Ester Ethoxylates Market share in 2025, making palm-derived fatty acids the dominant feedstock for nonionic surfactant production. Palm oil provides a highly suitable C16–C18 fatty acid composition, which is ideal for manufacturing methyl ester ethoxylates used in detergents, cleaning formulations, and industrial surfactants. The feedstock also offers strong advantages including high agricultural yield per hectare, cost-effective production economics, and a well-developed global supply chain, particularly across Southeast Asia where palm oil production is concentrated. These factors have positioned palm oil as the most widely utilized raw material for large-scale MEE manufacturing. In 2025, sustainability concerns surrounding palm cultivation have significantly influenced procurement strategies across the surfactant industry. Major detergent and consumer goods companies increasingly require RSPO-certified palm oil supply chains, encouraging methyl ester ethoxylate manufacturers to adopt mass balance certification systems and traceable sourcing programs that ensure compliance with global sustainability commitments while maintaining the cost advantages associated with palm-derived feedstocks.

Household Cleaning Products Drive the Largest Application Demand for Methyl Ester Ethoxylates

Household cleaning accounted for 48.60% of the Methyl Ester Ethoxylates Market share in 2025, making laundry detergents, dishwashing liquids, and multi-purpose cleaning products the largest application segment for these renewable surfactants. Methyl ester ethoxylates are widely used in liquid laundry detergents, automatic dishwashing formulations, surface cleaners, and hard-surface degreasers due to their excellent detergency, emulsification capability, biodegradability, and compatibility with other surfactant systems. Compared with traditional petroleum-based surfactants, MEE offers the advantage of renewable vegetable oil sourcing and improved environmental performance, aligning with regulatory and consumer demand for sustainable cleaning products. The global expansion of household cleaning markets, particularly in emerging economies, continues to support high-volume consumption of MEE surfactants. In 2025, detergent manufacturers have also accelerated the shift toward concentrated liquid detergents and unit-dose laundry pods, requiring surfactant systems capable of maintaining high active ingredient levels while remaining compatible with water-soluble polymer films used in pod packaging. MEE chemistry has been optimized to support these formulations while maintaining cleaning efficiency in modern detergent formats.

Methyl Ester Ethoxylates Market Competitive Landscape

The methyl ester ethoxylates (MEE) market in 2026 is driven by biodegradable, low-dioxane, RSPO-certified surfactants with high Renewable Carbon Index (RCI). Oleochemical integration, narrow-range ethoxylation, and cold-water detergency performance are key differentiators, positioning MEE as a sustainable alternative to alcohol ethoxylates in detergents and personal care.

Lion Corporation leads carbon-neutral MEE innovation with RSPO-certified palm-based surfactants

Lion Specialty Chemicals (Lion Corporation) is the global pioneer in methyl ester chemistry, leveraging decades of expertise in palm-based oleochemicals. Its MEE and MES portfolios are positioned as carbon-neutral surfactants with full RSPO-certified traceability through its leadership in JaSPON. The company’s narrow-range ethoxylation capabilities deliver superior rinsing, low residue, and high detergency performance, particularly in cold-water washing systems. Lion’s products are widely used in compact liquid detergents across ASEAN markets, optimized for high-efficiency washing machines. Its strong control over feedstock sourcing ensures sustainability compliance and supply reliability. Lion continues to lead the transition toward bio-based, high-performance surfactants in global cleaning formulations.

KLK OLEO strengthens integrated oleochemical value chain with high-RCI MEE surfactants

KLK OLEO is a major vertically integrated player, controlling the full value chain from palm plantations to methyl ester ethoxylates production. Its GREENBENTIN product line offers high Renewable Carbon Index (~1.0) surfactants that meet stringent clean-label and safety requirements. The company’s PALMERE feedstock integration enables consistent quality and traceability for multinational FMCG clients. Strategic collaboration in agricultural adjuvants expands its application footprint into crop protection, enhancing pesticide efficiency. Its low-foaming MEE solutions for textile and leather processing reduce water consumption and improve process efficiency. KLK OLEO’s scale, integration, and sustainability positioning make it a dominant force in global bio-based surfactants.

Stepan expands ethoxylation capacity to accelerate bio-based surfactant adoption in North America

Stepan Company is strengthening its position in the MEE market through expanded ethoxylation capacity at its Illinois facility, targeting rising demand for renewable surfactants. Its low-foaming ethoxylates are gaining traction in Industrial & Institutional (I&I) cleaning, offering superior wetting and quick-rinse performance. The company is actively replacing nonylphenol ethoxylates (NPEs) with MEE-based alternatives across industrial and agricultural applications. Stepan’s expertise in tailoring Hydrophilic-Lipophilic Balance (HLB) enables precise formulation for diverse end uses, from personal care to heavy-duty degreasers. Its Bio-Surfactant Roadmap aligns with global sustainability goals, targeting a majority renewable portfolio by 2030. This positions Stepan as a key supplier in the Western bio-based surfactant market.

INEOS advances low-carbon ethoxylation and high-purity precursors for industrial MEE applications

INEOS (Inovyn) is focusing on decarbonized chemical production and advanced ethoxylation technologies to support MEE growth. Investments of £150 million in the UK and €250 million in France are modernizing production infrastructure, enhancing efficiency and sustainability. Its NEOVYN™ product line offers a 37% lower carbon footprint, aligning with net-zero targets and regulatory pressures. INEOS supplies high-purity methyl ester intermediates used in non-ionic surfactant synthesis for oilfield and lubricant applications. Its MEE-based systems are critical for Enhanced Oil Recovery (EOR), reducing interfacial tension and improving extraction efficiency. The company’s focus on circular feedstocks and industrial-scale integration strengthens its role in specialty surfactant supply chains.

Huntsman delivers tailored narrow-range MEE surfactants for agrochemical and industrial applications

Huntsman Corporation is a leading innovator in specialty methyl ester ethoxylates, focusing on high-performance, narrow-range surfactants. Its latest MEE products demonstrate strong stability across extreme pH conditions, making them suitable for metalworking and industrial cleaning applications. In agrochemicals, Huntsman’s MEE-based adjuvants enhance pesticide delivery while remaining non-phytotoxic and environmentally safe. The company is also expanding into sustainable packaging, where MEE acts as a wetting agent in eco-friendly inks and coatings. Its global manufacturing footprint enables localized supply and customization for diverse markets. Huntsman’s ability to precisely control ethoxylation levels positions it as a preferred partner for advanced formulation requirements.

United States: Bio-Based Scale-Up and Regulatory-Led Reformulation

The United States methyl ester ethoxylates market is undergoing a decisive structural shift driven by bioeconomy investments, regulatory compliance, and domestic capacity expansion. In August 2025, Kao Corporation commissioned a new tertiary amine and surfactant production facility in Pasadena, Texas, with an annual capacity of 20,000 tons. The plant is strategically designed to integrate ethoxylation derivatives for disinfectants and industrial cleaners, reducing reliance on imported intermediates while improving lead times for North American formulators. This infrastructure pivot reflects broader efforts to localize surfactant value chains amid tightening environmental standards.

Regulatory momentum is accelerating adoption. In preparation for the January 2026 EPA Safer Choice compliance window, U.S. manufacturers such as Stepan Company expanded low-foaming ethoxylate portfolios that meet stringent aquatic toxicity thresholds, replacing petroleum-based surfactants in more than one-third of new industrial cleaning product launches. Federal policy alignment is reinforcing this trend. The United States Department of Energy rolled out 2025 bioeconomy funding rounds to scale enzymatic production pathways, targeting a 12% reduction in manufacturing costs for methyl ester derivatives by 2026. Concurrently, the United States Department of Agriculture fast-tracked BioPreferred certification for plant-derived non-ionic surfactants, shifting federal procurement toward MEEs sourced from domestic soy and palm FAME. Price actions, including Indorama Ventures’ January 2025 increase on its Surfonic L24 series, signal margin stabilization strategies amid volatile feedstocks and rising compliance costs.

Japan: Precision Interface Control and AI-Enabled Purity

Japan’s methyl ester ethoxylates market is advancing through precision chemistry, circular policy alignment, and digital manufacturing control. Under its K27 mid-term plan, Kao Corporation has positioned interface control technology as a core pillar, with near-term milestones focused on integrating advanced MEE formulations into flagship Attack and CuCute brands. These formulations are engineered for superior biodegradability and environmental performance, aligning with the company’s long-term objective of carbon-negative surfactants by 2050.

Policy signals are reinforcing demand. Japan’s Recycling-Oriented Society framework encourages adoption of biodegradable surfactants, and data from the Ministry of Internal Affairs show that nearly one-quarter of chemical sector sales in 2025 came from products meeting strict environmental conformity. On the production side, Japanese chemical leaders began deploying machine learning in late 2025 to optimize ethoxylation reactions. AI-driven control is being used to suppress discoloration and hydrolysis, historically limiting large-scale production of high-purity methyl ester derivatives. This capability is positioning Japan as a supplier of premium MEEs where consistency and performance tolerance are critical.

China: Bio-Based Substitution and Circular Feedstock Integration

China’s methyl ester ethoxylates market is being reshaped by policy-led substitution of legacy surfactants and aggressive circular economy integration. The Ministry of Industry and Information Technology’s 2025–2026 work plan targets 5% growth in specialty chemicals, with explicit prioritization of innovation platforms for bio-based surfactants. This agenda is accelerating the phase-down of alkylphenol ethoxylates and creating a favorable environment for MEEs in household and institutional cleaning applications.

Capacity expansion underpins localization. In 2025, global suppliers including Nouryon and Sun Chemical scaled operations at the Nansha hub to enable domestic production of MEEs for eco-certified laundry detergents. Feedstock strategy is also evolving. China’s 2026 policy roadmap emphasizes Internet-enabled recycling platforms, driving development of circular MEEs synthesized from reclaimed vegetable oils. This approach supports the broader oleochemical sector’s ambition to exceed 15 million metric tons of domestic production while reducing exposure to virgin petrochemical inputs.

India: Specialty Chemical Zones and Green Manufacturing Incentives

India’s methyl ester ethoxylates market is expanding through infrastructure-led industrialization and sustainability-linked fiscal reform. Under the NITI Aayog 2025 strategy, the development of dedicated specialty chemical zones has enabled companies such as India Glycols Limited to commercialize sugar-based and methyl ester-derived surfactants. These products achieved an estimated 38% adoption rate among domestic natural and personal care manufacturers in 2025, reflecting strong alignment with clean-label and bio-based positioning.

Environmental compliance is becoming a competitive lever. Late-2025 GST reductions on effluent treatment and renewable chemical production equipment are encouraging MEE producers to adopt Zero Liquid Discharge systems. These investments are increasingly essential to meet 2026 Green Industry certification requirements, particularly for exporters supplying multinational consumer goods brands. As a result, India is strengthening its position as a cost-efficient yet compliant manufacturing base for bio-derived non-ionic surfactants.

Malaysia and Thailand: Palm-Based Traceability and Regional Supply Expansion

Malaysia and Thailand play a critical upstream role in the methyl ester ethoxylates market through sustainable oleochemical feedstocks and regional capacity build-out. In 2025, KLK OLEO and Wilmar International achieved full traceability for palm-based methyl esters, reinforcing ESG credentials demanded by global surfactant buyers. KLK OLEO showcased its PALMERE fractionated methyl esters at VietnamPlas in August 2025, positioning them as primary raw materials for MEE and MES production across Southeast Asia.

Downstream performance indicators are supportive. Indorama Ventures reported solid performance for its Indovinya business unit in early 2025 under the IVL 2.0 transformation program. The strategy emphasizes capacity additions in high-growth markets such as India and Africa, ensuring supply continuity for 2026 surfactant demand while leveraging Southeast Asia’s feedstock advantages.

Country-Level Strategic Positioning in the Methyl Ester Ethoxylates Market

Methyl Ester Ethoxylates Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Demand Driver

|

Policy or Industry Catalyst

|

Competitive Positioning

|

|

United States

|

Bio-based scale and compliance

|

Industrial cleaners, federal procurement

|

EPA Safer Choice, USDA BioPreferred

|

Localized, regulation-ready supply

|

|

Japan

|

Precision purity and circularity

|

Premium home care

|

Recycling-Oriented Society policy

|

High-purity, AI-controlled production

|

|

China

|

Bio-based substitution and recycling

|

Eco-certified detergents

|

MIIT growth plan, circular mandates

|

Large-scale localization

|

|

India

|

Specialty zones and green compliance

|

Natural and personal care

|

NITI Aayog strategy, GST reforms

|

Cost-efficient sustainable manufacturing

|

|

Malaysia & Thailand

|

Traceable palm feedstocks

|

Oleochemical surfactants

|

ESG and traceability standards

|

Feedstock leadership with scale

|

Methyl Ester Ethoxylates Market Report Scope

Methyl Ester Ethoxylates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$250.5 Million

|

|

Market Size (2034)

|

$362.8 Million

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Fatty Acid Source (Palm Oil-Based, Coconut Oil-Based, Rapeseed Oil-Based, Soybean Oil-Based, Other Vegetable Oils), By Type (C12–C14 Methyl Ester Ethoxylates, C16–C18 Methyl Ester Ethoxylates), By Product Form (Liquid, Paste, Solid), By Application (Household Cleaning, Industrial and Institutional Cleaning, Personal Care, Agrochemicals, Textile and Leather, Oilfield Chemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kao Corporation, Lion Corporation, KLK Oleo, Wilmar International, Indorama Ventures, Huntsman Corporation, BASF, Dow, Shell Chemicals, INEOS, Clariant, Stepan Company, India Glycols, Nouryon, Evonik Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Methyl Ester Ethoxylates Market Segmentation

By Fatty Acid Source

- Palm Oil-Based

- Coconut Oil-Based

- Rapeseed Oil-Based

- Soybean Oil-Based

- Other Vegetable Oils

By Type

- C12–C14 Methyl Ester Ethoxylates

- C16–C18 Methyl Ester Ethoxylates

By Product Form

By Application

- Household Cleaning

- Industrial and Institutional Cleaning

- Personal Care

- Agrochemicals

- Textile and Leather

- Oilfield Chemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Methyl Ester Ethoxylates Market

- Kao Corporation

- Lion Corporation

- KLK Oleo

- Wilmar International

- Indorama Ventures

- Huntsman Corporation

- BASF

- Dow

- Shell Chemicals

- INEOS

- Clariant

- Stepan Company

- India Glycols

- Nouryon

- Evonik Industries

*- List not Exhaustive