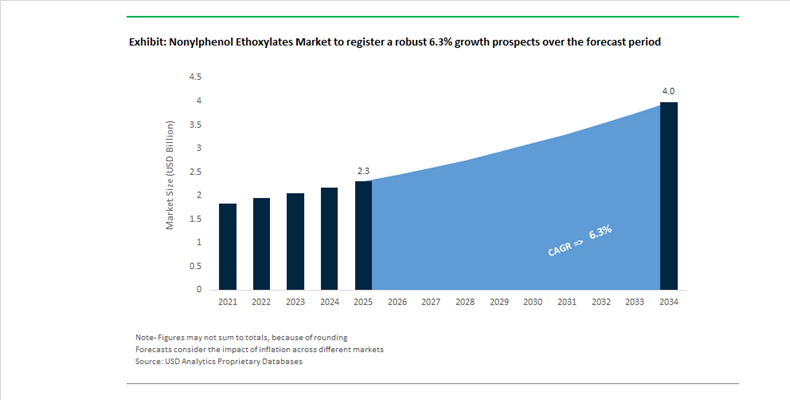

Nonylphenol Ethoxylates Market Valued at $2.3 Billion in 2025, Set to Reach $4 Billion by 2034 at 6.3% CAGR Amid Regulatory Pressure and Reformulation Cycles

The Nonylphenol Ethoxylates Market is valued at $2.3 billion in 2025 and is projected to reach $4 billion by 2034, expanding at a CAGR of 6.3%. Growth is occurring despite intensifying environmental scrutiny, driven by continued demand in industrial cleaning, textile processing, agrochemical emulsifiers, paints and coatings, and metalworking fluids. Nonylphenol ethoxylates (NPEOs) remain highly effective non-ionic surfactants due to their superior wetting, emulsification, and detergent properties, particularly in high-load industrial formulations. However, aquatic toxicity concerns and endocrine-disruption risks associated with nonylphenol degradation are reshaping product development, compliance frameworks, and geographic trade flows. Regulatory classification under EU CLP, California Safer Consumer Products rules, and tightening Asian import thresholds are accelerating the reformulation of legacy NPEO-containing systems.

In January 2024, the European Union issued Commission Delegated Regulation (EU) 2024/197, mandating harmonized classification and labeling for NPEOs with molecular weight ≤ 1,540 g/mol, with full applicability beginning September 2025. In September 2024, California’s Department of Toxic Substances Control added detergents containing alkylphenol ethoxylates to its Safer Consumer Products candidate list, compelling alternatives assessments for manufacturers operating in the state. During the same month, Dow Inc. received the BIG Innovation Award for EcoSense™ 2470, a biodegradable NPE-free surfactant positioned as a direct drop-in replacement for textile and industrial cleaning applications. Throughout 2024, India Glycols Limited maintained leadership in the domestic NPEO market, leveraging integrated ethoxylation capacity to stabilize supply to Indian textile processors amid global price volatility.

Product innovation and regulatory adaptation intensified through 2025 and into 2026. In June 2025, Taiwan finalized a phased import ban on cleaning agents containing NPEOs, prohibiting products with ≥5% concentration from December 2026 and tightening the limit to 0.1% by June 2027. In October 2025, Indovinya launched a $500,000 Open Innovation Challenge to accelerate development of bio-derived, nonylphenol-free surfactants, signaling strategic repositioning by major producers. In November 2025, Huntsman Corporation introduced bio-enhanced NPE formulations for agrochemical dispersants that reduce environmental persistence while preserving adhesion performance. In December 2025, Stepan Company launched NP-9.5 for paints and coatings, engineered for higher pigment loading and faster drying in U.S. industrial manufacturing.

By January 2026, Dow Inc. introduced a new low-foam NPE variant designed for industrial cleaning and metalworking, delivering 20% improved wetting efficiency and optimized biodegradability aligned with updated EPA aquatic toxicity benchmarks. In January 2026, Kao Corporation unveiled a high-purity NPE emulsifier tailored for specialty coatings in Japan, engineered for dispersion stability in water-based systems. Concurrently, Reliance Industries advanced its phenol production complex in Jamnagar, expected to be operational by mid-2026, strengthening upstream phenol supply critical for nonylphenol and downstream NPEO manufacturing in Asia.

Nonylphenol Ethoxylates (NPEs) Market Trends and Opportunities

Trend: Accelerated Global Phase-Out of NPEs Driven by Digital Product Passport and Import Enforcement

The Nonylphenol Ethoxylates market has entered an irreversible contraction phase as regulatory controls move beyond disclosure requirements toward active market exclusion. In 2025, enforcement mechanisms across the EU, North America, and Asia have shifted from advisory restrictions to hard compliance gates that directly block non-compliant products from entering downstream value chains. Under Commission Regulation (EU) 2024/197, effective September 1, 2025, NPEs with an average molecular weight of 1,540 g/mol or below are subject to tighter classification, labeling, and packaging obligations, significantly raising compliance costs for Industrial and Institutional cleaning formulators. This is compounded by the EU Toy Safety Regulation 2025/2509, which introduces the Digital Product Passport as a mandatory traceability tool. The DPP requires a verifiable digital audit trail demonstrating that NPE concentrations remain below 0.1 percent by weight across all textile and plastic components, effectively eliminating tolerance for undocumented legacy surfactants.

In the United States, California has emerged as a de facto regulatory bellwether. Effective October 1, 2024, the California Department of Toxic Substances Control classified laundry detergents containing NPEs as a Priority Product. Manufacturers selling into California were required to submit Priority Product Notifications by December 2024, triggering mandatory Alternatives Analysis and placing NPE-based formulations on a defined phase-out pathway. Similar alignment is now visible in Asia. In June 2025, Taiwan announced a phased ban on detergents containing more than 5% NP or NPEO, with enforcement beginning December 2026. This decision is strategically significant, as Taiwan functions as a critical manufacturing and export hub for formulated surfactants. Collectively, these policies are compressing the addressable market for NPEs and accelerating a structural transition toward APEO-free chemistries across global I&I supply chains.

Trend: Brand-Led Elimination of NPEs in Textile Wet Processing and Scouring

The textile sector, historically the largest consumer of NPEs, is undergoing rapid detoxification driven by brand-led compliance rather than national regulation alone. Global apparel brands have operationalized chemical management through the Zero Discharge of Hazardous Chemicals program, making NPE elimination a prerequisite for supplier qualification. According to the 2024 Impact Report published by the ZDHC Foundation, registered supplier facilities increased by 49% between 2022 and 2024, reaching nearly 13,000 sites worldwide. More than 70% of these suppliers now consistently meet ZDHC MRSL wastewater criteria, which explicitly prohibit the intentional use of NPEOs in textile processing.

The substitution pathway is centered on fatty alcohol ethoxylates and other APEO-free surfactants. Toxicity modeling conducted by ZDHC in 2024 shows that replacing NPEs with alcohol ethoxylates reduces freshwater ecotoxicity by approximately 51%. While this transition can marginally increase climate impact due to higher dosage requirements, brands are prioritizing the removal of persistent endocrine disruptors to meet ESG disclosure requirements and Science Based Targets. This shift has material export implications. A 2024 assessment by Toxics Link highlighted that Indian textile exporters face elevated risk due to continued domestic NPE usage, with estimated annual consumption ranging from 14,900 to over 200,000 tonnes. As EU and US retailers tighten supplier audits, manufacturers in the Global South are being forced to adopt APEO-free systems to preserve access to high-margin export markets.

Opportunity: Engineering High-Performance, Readily Biodegradable Industrial Degreasers

The structural decline of NPEs in heavy-duty degreasing and industrial cleaning has created a clear performance gap that is driving innovation in bio-based and readily biodegradable surfactant systems. Industrial users still require rapid wetting, strong oil penetration, and solvency under high-load conditions, but without the regulatory and reputational liabilities associated with alkylphenols. One of the most commercially successful alternatives emerging in 2024–2025 is methyl soyate, a soybean-derived solvent that has scaled rapidly in North America for oil spill remediation and industrial degreasing. Methyl soyate offers a high flash point and low vapor pressure, improving worker safety while delivering solvency performance comparable to legacy NPE-based systems.

Beyond single-molecule substitutions, formulators are developing synergistic platforms that replicate the broad-spectrum performance of NPEs. Large agro-industrial suppliers have launched NPE-free degreaser systems that combine bio-solvents with advanced wetting agents to achieve fast penetration and uniform coverage in high-stress environments. Field studies on modern biodegradable degreasers demonstrate tangible operational benefits. Products such as next-generation enzymatic and solvent-assisted cleaners have been shown to remove crude oil residues from pipelines with minimal agitation and no rinsing, reducing cleaning cycle times and lowering wastewater treatment costs. These efficiency gains are critical for industrial operators seeking to offset the slightly higher unit cost of NPE-free formulations.

Opportunity: Closed-Loop and Precision Agricultural Adjuvants Without NPEs

While open-field agricultural use of NPEs is increasingly restricted, a high-value opportunity is emerging in controlled and closed-loop agricultural systems that demand precision surfactant performance. Modern NPE-free adjuvants are being engineered to deliver superior spreading, sticking, and penetration without the phytotoxicity risks historically associated with alkylphenol ethoxylates. Precision adjuvant technologies introduced in 2024–2025 have demonstrated measurable yield benefits by improving fungicide and nutrient uptake deeper into crop canopies. These NPE-free spreader-activators are now favored to avoid developmental issues linked to older surfactant chemistries.

Regulatory alignment is reinforcing this opportunity. Under India’s Fertilizer Control Twelfth Amendment Order of 2025, new standards for liquid fertilizers and Organic Carbon Enhancers require traceability and QR-code-based compliance, creating demand for surfactants that can be certified as compatible with soil health and sustainability objectives. Parallel innovation is occurring in greenhouse and protected agriculture. Operators are piloting membrane filtration and recovery systems that capture and recycle surfactants from irrigation and wash water. These closed-loop models allow continued use of high-efficacy ethoxylate-based systems within a zero-discharge framework, aligning performance needs with environmental safeguards. Together, these applications represent a transition from volume-driven NPE consumption to smaller, higher-value niches built around precision, containment, and regulatory compliance.

Nonylphenol Ethoxylates Market Share and Segmentation Insights

Medium Ethoxylation Nonylphenol Ethoxylates Lead the Market Due to Optimal HLB for Industrial Formulations

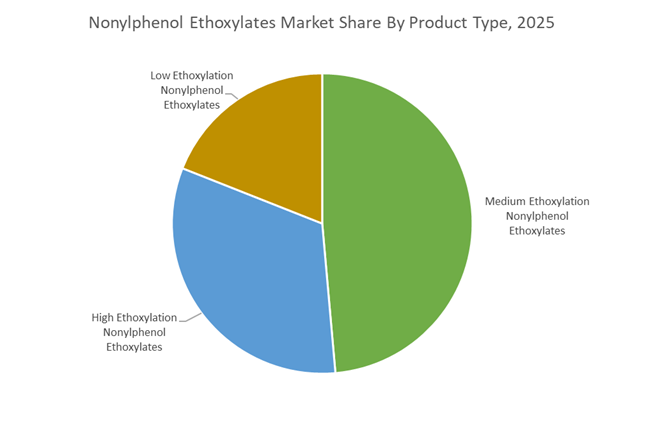

Medium ethoxylation nonylphenol ethoxylates accounted for 48.60% of the Nonylphenol Ethoxylates Market share in 2025, making them the most widely used product type in industrial surfactant formulations. Typically containing 9–10 moles of ethylene oxide, these surfactants provide an optimal hydrophilic-lipophilic balance (HLB) that supports strong wetting, emulsification, and detergency performance across multiple industrial processes. Medium ethoxylation NPEs are widely used in industrial and institutional cleaning products, textile processing chemicals, agrochemical emulsifiers, metal treatment formulations, and oilfield chemicals, where their strong emulsifying capability and tolerance to alkaline and hard-water conditions enable stable formulations. Their balanced molecular structure allows them to function effectively as wetting agents, dispersants, and solubilizers in demanding industrial environments. In 2025, the market is experiencing formulation migration pressure driven by tightening environmental regulations and restrictions on nonylphenol derivatives in regions such as Europe and North America, where concerns about aquatic toxicity and endocrine disruption have accelerated the transition toward alternative surfactants such as alcohol ethoxylates and alkyl polyglucosides. Despite this shift, medium ethoxylation NPEs continue to maintain significant demand in Asia, Latin America, and parts of the Middle East, particularly in applications where replacement surfactants have not yet achieved equivalent performance or cost efficiency.

Nonylphenol Ethoxylates Market Competitive Landscape

The nonylphenol ethoxylates (NPE) market in 2026 operates under a dual-track dynamic, balancing regulatory phase-out in developed markets with sustained demand in Asia-Pacific. Competitive positioning hinges on formula retrofitting, ethoxylation efficiency, and strategic localization to support textile, agrochemical, and industrial surfactant demand.

Stepan restructures global surfactant operations to prioritize high-efficiency assets and specialty intermediates

Stepan Company is executing a structural reset through Project Catalyst, targeting US$100 million in pre-tax savings by optimizing manufacturing efficiency and consolidating production into modern facilities. The planned closure of its Fieldsboro site reflects declining demand for commodity NPEs in North America and a shift toward high-margin industrial surfactants. Strategic divestitures of Philippines and Lake Providence assets enable capital reallocation into agricultural and oilfield surfactant segments. The company is absorbing US$70–80 million in restructuring costs to enhance long-term operational agility. Its merchant surfactant model remains focused on productivity gains and inflation mitigation. This transformation positions Stepan to remain competitive amid regulatory contraction in legacy NPE markets.

Indorama Ventures scales integrated surfactant platform under SOAR strategy to drive EBITDA expansion

Indorama Ventures is advancing its SOAR roadmap (2026–2028) with a target to double EBITDA through operational excellence and platform integration. Approximately 95% of earnings will be driven by advantaged segments, including surfactants, PET, and packaging. The company has restructured leadership to streamline execution and improve capital allocation efficiency. Its integrated EO/EG turnaround program is focused on restoring profitability across the shale-to-surfactant value chain. By consolidating global surfactant assets, IVL is strengthening its presence in Asia-Pacific markets where NPE demand remains robust. This disciplined, margin-focused strategy enhances resilience in a volatile regulatory environment.

India Glycols leverages green chemistry and corporate restructuring to strengthen surfactant exports

India Glycols is capitalizing on India’s fast-growing chemical sector through strategic demergers aimed at unlocking value across its chemical and bio-pharma divisions. The company reported an 18.94% increase in net profit and 13.04% revenue growth in FY 2025/2026, driven by strong demand for glycol derivatives and industrial surfactants. A ₹467 crore capital raise and ₹7.5/share dividend highlight financial strength and investor confidence. Its pivot toward second-generation ethanol and green solvent exports aligns with global sustainability trends and NPE substitution pressures. The company is positioning itself as a key exporter in the Asia-Pacific supply chain. This integration of green chemistry and financial restructuring strengthens its competitive positioning.

Huntsman pivots to semiconductor-grade surfactants and high-purity performance chemicals amid NPE decline

Huntsman Corporation is shifting away from commodity NPE exposure toward high-purity specialty surfactants and semiconductor-grade chemicals. Its E-GRADE® portfolio targets precision applications such as etching and stripping, where ultra-low impurities are critical. The company is integrating carbonate solvents into lithium-ion battery supply chains, diversifying beyond traditional surfactant markets. JEFFAMINE® polyetheramines continue to support high-performance epoxy systems in wind energy and automotive lightweighting. Huntsman’s Ecolibrium R&D platform focuses on reducing carbon intensity in ethoxylation processes while maintaining performance. This transition toward advanced materials and electronics-grade chemistry ensures long-term resilience.

PCC Group expands Asian ethoxylation footprint with high-performance surfactant specialization

PCC Group is strengthening its global position through the PCG PCC Oxyalkylates joint venture in Malaysia, now operating at full capacity as a regional hub for ethoxylates. Its VOXA™ product line targets high-performance applications in automotive, footwear, and upholstery sectors requiring precise surfactant behavior. The company emphasizes intelligent R&D, ensuring compliance with evolving environmental regulations and accelerating the transition away from NPE-based systems. Advanced ethoxylation capabilities with narrow EO distribution enhance product consistency and requalification speed. PCC’s vertical integration and safety-focused EO handling provide a competitive edge in specialty surfactants. This Asia-centric expansion aligns with the industry’s localization trend.

China: Regulatory Tightening with Export-Oriented Rebalancing

China is entering a decisive transition phase for the nonylphenol ethoxylates industry, driven by tightening food-contact and environmental standards alongside continued industrial demand. In July 2025, the China National Center for Food Safety Risk Assessment issued a draft amendment to GB 9685 proposing the removal of nonylphenol derivatives from the approved additives list for food-contact materials. This move represents a structural regulatory inflection point, effectively closing downstream exposure routes while accelerating substitution toward biodegradable ethoxylates. In parallel, provincial enforcement of the 2025 Green Manufacturing Standards in Jiangsu and Qingdao has prompted large surfactant producers to reconfigure legacy ethoxylation lines toward cleaner reaction pathways.

Despite domestic contraction in household detergents, China remains a dominant global exporter. Investment in UV-light-assisted ethoxylation chambers at major chemical parks has improved technical-grade purity by reducing residual free nonylphenol, supporting export-grade 9-mole and 10-mole NPE shipments. The FOB Qingdao Price Index reflects elevated inventory levels oriented toward overseas industrial markets, particularly metalworking fluids, automotive degreasing, and heavy-duty industrial washing. Technological differentiation is also emerging through low-foam NPE variants optimized for high-pressure systems in automotive manufacturing, partially offsetting regulatory-driven demand erosion at home.

United States: Federal Scrutiny Meets Industrial Entrenchment

The United States nonylphenol ethoxylates landscape is defined by regulatory escalation layered over entrenched industrial use cases. In September 2025, the U.S. Environmental Protection Agency proposed amendments to the TSCA procedural framework, reshaping how cumulative exposure pathways are evaluated for surfactants such as NPEs. At the state level, California’s Department of Toxic Substances Control classified laundry detergents containing NPEs as a Priority Product effective October 2024, obligating alternative analysis submissions by late 2025 and accelerating reformulation timelines for consumer-facing products.

Industrial demand, however, remains resilient. Stepan Company commissioned a new alkoxylation facility in Pasadena, Texas in May 2025 with an annual capacity of 75,000 metric tons, primarily focused on high-performance substitutes but also reinforcing domestic alkoxylation infrastructure. NPEs continue to be utilized as cost-effective wetting agents in Midwest agrochemical formulations and as emulsifiers in Permian Basin hydraulic fracturing and enhanced oil recovery fluids. The Safer Detergents Stewardship Initiative is further guiding a voluntary phase-down in institutional laundry, emphasizing liquid-to-solid format transitions rather than abrupt elimination.

Germany: Authorization Pressure and Green Chemistry Substitution

Germany represents one of the most regulation-intensive environments for nonylphenol ethoxylates, with industrial use increasingly constrained by EU-level oversight. Manufacturers are navigating upcoming REACH Annex XIV authorization reviews, with several permissions for branched NPE applications approaching expiry or reassessment from January 2026. This regulatory pressure has redirected R&D spending toward functional substitutes that replicate NPE performance while meeting the biodegradability and aquatic toxicity thresholds of the EU Water Framework Directive.

BASF SE introduced a new high-purity ethoxylate series during 2024–2025 engineered to match NPE efficacy without endocrine-disrupting profiles. At the Höchst Industrial Park, firms such as WeylChem have upgraded ethoxylation units to process carbon-neutral and alternative feedstocks. Pilot programs are also underway for CO₂-derived alkoxylates under carbon capture utilization schemes. Concurrently, the Federal Environment Agency has intensified monitoring of NPE residues in industrial wastewater, stimulating demand for advanced effluent treatment and reinforcing the shift toward OEKO-TEX® and ZDHC-compliant textile auxiliaries.

India: Dual-Speed Market Between Exports and Domestic Agriculture

India’s nonylphenol ethoxylates industry is expanding along two divergent tracks. On the supply side, India Glycols Limited continues to upgrade large-scale ethoxylation capacity to serve technical-grade surfactant demand in Gujarat and Maharashtra textile clusters. Infrastructure investments at Mundra Port, including dedicated tank terminals, are improving the logistics of ethylene oxide and alkylphenol imports, reinforcing India’s role as a regional processing hub.

On the demand side, NPE consumption is rising sharply in domestic agrochemicals, where wetting efficiency and cost competitiveness remain decisive for herbicide and fungicide formulations. At the same time, export-oriented textile processors are actively transitioning to NPE-free chemistries to maintain access to European and North American apparel supply chains. Policymakers are evaluating new Quality Control Orders to align surfactant standards with GHS norms, indicating a gradual tightening trajectory rather than abrupt restriction. In rural markets, subsidized crop protection programs continue to support the use of low-cost NPE-based sprays, sustaining baseline volumes.

Brazil: Agrochemical Backbone with Environmental Recalibration

Brazil’s nonylphenol ethoxylates demand is anchored in large-scale agriculture and industrial processing. The USD 150 million Agrochemical Fund for 2023–2027 is supporting the development of stable surfactant platforms for soybean and sugarcane cultivation, where NPEs remain valued for formulation robustness. Industrial usage also persists in leather tanning operations in southern Brazil, although mounting environmental scrutiny is driving adoption of closed-loop water and surfactant recovery systems.

Supply chain resilience has improved through new distribution partnerships in São Paulo, enhancing availability of industrial-grade surfactants for construction chemicals and concrete additives. Regulatory momentum is building as ANVISA reviews surfactant safety profiles used in sanitizers, aligning with global endocrine disruptor monitoring trends. Offshore expansion in pre-salt oilfields continues to sustain demand for high-stability NPE emulsifiers in drilling fluids, reinforcing Brazil’s industrial reliance despite rising compliance expectations.

Japan: Precision Applications Under Intensified Oversight

Japan’s nonylphenol ethoxylates industry is increasingly confined to high-precision, low-volume applications. In November 2025, domestic chemical producers launched high-purity NPE-based emulsifiers tailored for specialty electronics, optical coatings, and semiconductor-adjacent cleaning processes where performance tolerances remain difficult to replicate. These niche uses persist even as regulatory oversight tightens.

Revisions to the Chemical Substances Control Law have classified certain alkylphenols as Monitoring Chemical Substances, mandating detailed annual reporting of production and use volumes. Collaborative research between industry and the National Institute of Advanced Industrial Science and Technology is focusing on degradation kinetics and aquatic toxicity reduction across ethoxylate chain lengths. Concurrently, manufacturers are shifting toward highly concentrated industrial cleaners to reduce packaging waste and transport emissions, aligning industrial hygiene practices with Japan’s broader decarbonization goals.

Summary Table: Nonylphenol Ethoxylates Industry – Country-Level Strategic Signals

Nonylphenol Ethoxylates Market County Level Snapshot

|

Country

|

Regulatory Direction

|

Industrial Reality

|

Strategic Implication

|

|

China

|

Food-contact removal, green standards

|

Export-driven industrial use

|

Export resilience amid domestic contraction

|

|

United States

|

TSCA and state-level scrutiny

|

Energy and agriculture demand

|

Gradual phase-down, not elimination

|

|

Germany

|

REACH authorization pressure

|

Rapid substitution R&D

|

Accelerated green chemistry transition

|

|

India

|

Emerging standards

|

Agrochemical-led growth

|

Dual-speed market evolution

|

|

Brazil

|

Increasing safety review

|

Agriculture and oilfield use

|

Environmental recalibration

|

|

Japan

|

Monitoring classification

|

Precision electronics niches

|

High-purity, low-volume continuity

|

Nonylphenol Ethoxylates Market Report Scope

Nonylphenol Ethoxylates Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.3 Billion

|

|

Market Size (2034)

|

$4 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Product Type (Low Ethoxylation Nonylphenol Ethoxylates, Medium Ethoxylation Nonylphenol Ethoxylates, High Ethoxylation Nonylphenol Ethoxylates), By Grade (Technical Grade, Industrial Grade, Specialty Grade), By Application (Textiles and Leather, Agrochemicals, Industrial and Institutional Cleaning, Paints and Coatings, Oil and Gas, Pulp and Paper)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Dow, Clariant, Huntsman, Stepan, Sasol, India Glycols, SABIC, Kao, Evonik Industries, Nouryon, Solvay, Indorama Ventures, Nizhnekamskneftekhim, Harcros Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nonylphenol Ethoxylates Market Segmentation

By Product Type

- Low Ethoxylation Nonylphenol Ethoxylates

- Medium Ethoxylation Nonylphenol Ethoxylates

- High Ethoxylation Nonylphenol Ethoxylates

By Grade

- Technical Grade

- Industrial Grade

- Specialty Grade

By Application

- Textiles and Leather

- Agrochemicals

- Industrial and Institutional Cleaning

- Paints and Coatings

- Oil and Gas

- Pulp and Paper

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Nonylphenol Ethoxylates Industry

- BASF

- Dow

- Clariant

- Huntsman

- Stepan

- Sasol

- India Glycols

- SABIC

- Kao

- Evonik Industries

- Nouryon

- Solvay

- Indorama Ventures

- Nizhnekamskneftekhim

- Harcros Chemicals

*- List not Exhaustive