Market Overview: Portfolio Restructuring, Low-Carbon Feedstocks, and Catalyst Integration Accelerate Chemical Intermediates Market Expansion

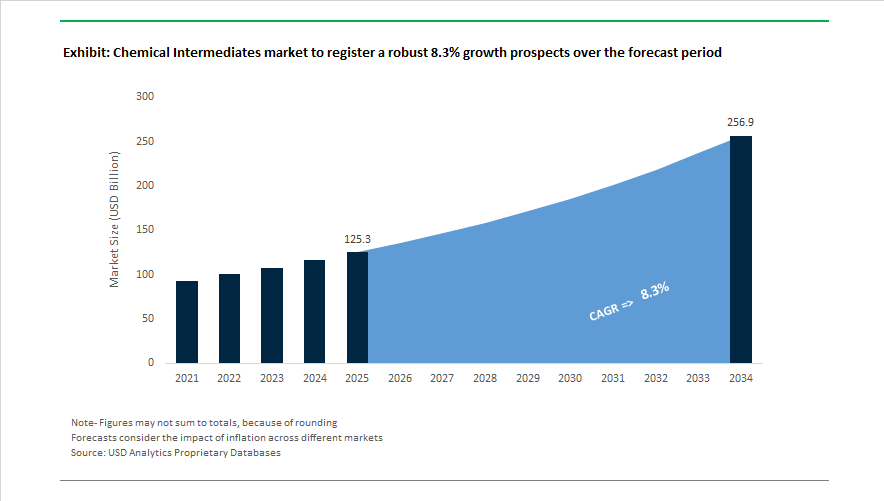

The Chemical Intermediates Market is forecast to grow from USD 125.3 billion in 2025 to USD 256.8 billion by 2034, advancing at a CAGR of 8.3% as producers reconfigure global capacity, integrate catalyst technologies, and transition toward low-carbon intermediate production. Momentum around bio-based and sustainable intermediates strengthened in October 2024 when Mitsubishi Chemical Group expanded BioPTMG capacity, supporting plant-derived polyurethane raw materials for synthetic leather and apparel supply chains. Structural changes intensified during July 2025 when INEOS completed a £30 million hydrogen transition at its Hull site, cutting carbon emissions from acetic acid and acetic anhydride intermediates by 75%. In the same month, Dow approved the shutdown of three energy-intensive European upstream assets following an April 2025 review, signaling a decisive shift away from high-cost European feedstock chains.

Capacity rationalization and portfolio optimization became dominant themes from August 2025 onward. Evonik confirmed the divestment of its Performance Intermediates C4 business to focus on high-margin specialties, while September 2025 saw BASF transition its Geismar standard amines portfolio to 100% renewable electricity credits, lowering product carbon footprints by about 4.5%. In October 2025, BASF inaugurated a world-scale neopentyl glycol plant in Zhanjiang and launched low-carbon NEOL NPG grades for coatings and resin markets. November 2025 marked BASF’s consolidation of Asian PolyTHF production at Caojing, with Ulsan output scheduled to cease by 2026. Restructuring extended into January 2026 as Wacker Chemie initiated its PACE program targeting €300 million in annual savings, and SYNEQT began operating independently to manage Evonik’s German chemical park infrastructure.

Major corporate transactions further reshaped the chemical intermediates landscape between 2025 and early 2026. Honeywell announced the acquisition of Johnson Matthey’s Catalyst Technologies division, with closure expected in the first half of 2026, integrating methanol and hydrogen catalyst portfolios into Honeywell UOP and strengthening intermediate synthesis capabilities. January 2026 saw SABIC divest its European Petrochemical business to AEQUITA and its Engineering Thermoplastics operations to MUTARES to sharpen its Saudi mega-cracker focus. During the same month, Ecovyst completed the $530 million sale of its catalyst intermediates segment to Technip Energies, pivoting toward sulfuric acid regeneration services.

Trends and Opportunities Defining the Future of the Chemical Intermediates Market

Strategic Re-shoring and "Friend-Shoring" to Protect Industrial Sovereignty

Governments are restructuring chemical intermediate supply chains to reduce dependency on vulnerable export sources and to secure continuity for high-tech industries such as semiconductors, pharmaceuticals, energy storage, and EV manufacturing.

In the United States, reshoring momentum is strongest in semiconductors and EV-related intermediates. According to the Reshoring Initiative (2024–2025), while general chemical manufacturing slowed, computer and electronic products and EV battery-linked materials represented approximately 67% of all reshoring-linked job creation. This shows capital allocation flowing specifically toward intermediates that enable advanced chips, electrolytes, cathode materials, and clean energy technologies.

India is following a similar trajectory. Under the ₹76,000 crore India Semiconductor Mission, 3nm design centers opened in Bengaluru and Noida in May 2025. These facilities are fueling demand for ultra-high-purity intermediates—materials that were traditionally imported from Taiwan, South Korea, or Japan. This signals a structural domestic build-out of upstream chemicals that support lithography, deposition, and precursor synthesis.

Commercialization of Bio-Based and Mass-Balance Intermediates Scaling Beyond Pilot Phase

What was once marketed as “sustainable” is now becoming a compliance requirement. Scope 3 reporting frameworks from multinational customers, ESG disclosure mandates, and ISCC PLUS certification thresholds are driving measurable supply-chain transformation.

BASF’s November 2025 expansion of biomass-balanced methanol (now ISCC EU certified) opens the door for drop-in, mass-balance intermediates that meet RED III renewable standards—allowing customers to decarbonize without altering plants or formulas. Meanwhile, Industrial Microbes (iMicrobes) achieved a 100% bio-based acrylic acid milestone in September 2025, supported by a U.S. DoD grant. Acrylic acid is mission-critical for adhesives and coatings, and commercial-scale bio-acrylic unlocks a pathway for carbon-accountable performance materials.

Ultra-High-Purity Chemical Intermediates for <5nm Semiconductor Fabrication

The semiconductor sector is becoming one of the highest-margin end-markets for intermediates due to purity requirements measured at the ppt (parts per trillion) level.

Through November 2025, the U.S. Department of Commerce has allocated over $36 billion in CHIPS Act funding, with TSMC ($6.6B) and Samsung ($6.4B) leading advanced fab developments. TSMC Phoenix Fab 1 began volume output in H1 2025, immediately requiring domestic suppliers of etchants, resist intermediates, and deposition precursors.

In January 2025, Corning secured $32 million in federal funding to expand lithography material production. This validates that domestic chemical intermediates capable of meeting sub-5nm purity standards will be supply-gated, contract-locked, and price-defensible—creating a long-term growth engine for players that invest in high-purity synthesis.

GMP-Grade Lipid Intermediates for mRNA Vaccine and Therapeutic Platforms

The pharmaceutical ecosystem is expanding beyond pandemic-era vaccine production toward oncology, rare diseases, and personalized therapeutics, creating a new premium segment where chemical intermediates sit at the foundation.

The global market for mRNA synthesis inputs reached an estimated $1.73 billion in 2025, with demand driven by GMP-grade modified nucleosides, ionizable lipids, and intermediates for lipid nanoparticle (LNP) delivery systems. CureVac’s 2024–2025 partnership with MD Anderson Cancer Center for off-the-shelf cancer vaccines demonstrates a shift in R&D pipelines toward scalable mRNA formats, which rely on lipid intermediates as essential enabling chemistry.

Producers who can secure GMP certification, cold-chain compatible supply, and batch-traceability (per EU Annex 1 and FDA cGMP expectations) will win long-duration contracts with life-science majors, positioning this segment as one of the most profitable opportunities in the decade.

Chemical Intermediates Market Share and Segmentation Insights

Basic Chemical Intermediates Lead Volume Consumption While Functional Intermediates Deliver Premium Growth

Basic chemical intermediates dominate the global chemical intermediates market with a 42% share in 2025, anchored by high-volume products such as methanol, acetic acid, ethylene oxide, propylene oxide, acrylonitrile, caprolactam, and vinyl chloride monomer (VCM). These core petrochemical intermediates form the backbone of polymer production, solvents, and downstream specialty chemicals, linking demand directly to construction activity, packaging consumption, and industrial manufacturing output. Olefins including ethylene, propylene, and butadiene represent the second-largest segment, driven by polyethylene, polypropylene, synthetic rubber, and EO/EG value chains, with North American ethane crackers and China’s coal-to-olefins capacity reshaping global supply dynamics. Aromatics (BTX and cumene) support polyester, styrenics, and nylon markets. Functional intermediates remain the smallest but fastest-growing category, fueled by pharmaceutical intermediates, specialty amines, and halogenated compounds, supported by contract manufacturing expansion in India and China.

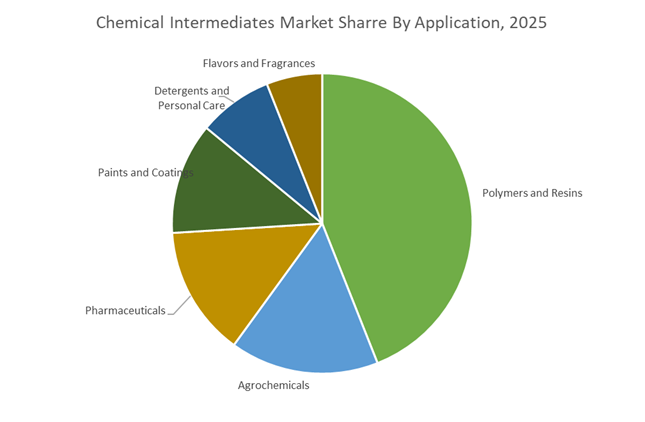

Polymers and Resins Anchor Demand as Agrochemicals and Pharmaceuticals Accelerate Value Creation

Polymers and resins account for 44% of chemical intermediates consumption, making this the largest application segment in 2025. Ethylene, propylene, benzene, and xylene are converted into polyethylene, polypropylene, PET, polystyrene, polycarbonate, and epoxy resins serving packaging, automotive, construction, and consumer goods markets. Demand closely tracks GDP growth and manufacturing activity, while circular economy initiatives and chemical recycling are redefining feedstock strategies. Agrochemicals rank second, utilizing both basic and functional intermediates in herbicides, insecticides, and fungicides, with generic production in India and China driving volume growth. Pharmaceuticals represent a high-value segment, relying on chiral intermediates, heterocycles, and specialty compounds supplied through CDMO networks. Paints and coatings consume solvent and resin intermediates, while detergents and personal care depend on LAB, fatty alcohols, and EO/PO. Flavors and fragrances remain niche but premium, supported by rising disposable incomes and natural-identical ingredient demand.

Competitive Landscape of the Chemical Intermediates Market

The global Chemical Intermediates Market in 2026 is being reshaped by rapid decarbonization initiatives, AI-enabled manufacturing, circular feedstock integration, and downstream specialty optimization. Leading producers are investing heavily in amines, diisocyanates, aromatics, glycols, and inorganic intermediates while aligning portfolios with EV materials, sustainable construction, renewable energy, and advanced electronics. Competitive differentiation now centers on vertical integration, digital hubs, low-SVOC technologies, circular polymers, and CO₂-to-chemicals platforms, as suppliers move beyond commodity production toward high-value, application-specific intermediates for automotive, furniture, batteries, coatings, and green consumer products.

BASF builds AI-driven, low-SVOC intermediate platforms for global green transformation

BASF enters 2026 as the benchmark for integrated chemical intermediates, advancing its “Winning Ways” strategy to decarbonize amines and diisocyanates at scale. The company shifted its standard amine portfolio to 100% renewable electricity across Geismar and European sites, reinforcing its leadership in sustainable intermediates. BASF markets over 300 amines alongside critical products such as Lupranate® TDI, with 2026 price adjustments reflecting strong automotive and furniture demand. Its Near-Zero SVOC technology supports healthier interior coatings, while the new Global Digital Hub in Hyderabad uses AI to optimize yields and reduce Scope 3 emissions, positioning BASF as a core supplier for low-carbon coatings, foams, and specialty materials.

Dow accelerates AI-led productivity across ethylene amines and propylene glycols

Dow’s 2026 strategy is anchored in its “Transform to Outperform” program, deploying AI and automation to simplify intermediate manufacturing and target a $2 billion EBITDA uplift by 2028. The company leads North America in ethylene amines and propylene glycols, essential building blocks for pharmaceuticals, de-icing fluids, and electronics materials. Dow recently unveiled a novel long-chain branched polyethylene architecture, enabling flexible feedstock switching amid market volatility. Its integrated assets connect amines and chelants with materials science expertise, delivering proprietary “Signature Technologies” for mobility and advanced electronics. This scale-driven, digitally optimized platform positions Dow as a preferred supplier for resilient, performance-driven chemical intermediates.

SABIC leverages crude-to-chemicals integration and TRUCIRCLE™ circularity leadership

Backed by Saudi Aramco, SABIC dominates petrochemical-to-intermediate conversion in 2026, using its TRUCIRCLE™ platform to commercialize certified circular polymers derived from plastic waste. The company is reshaping its portfolio toward low-carbon ammonia and methanol, positioning these intermediates as future clean fuels for shipping and energy. SABIC also supplies phenol and acetone to support Saudi Vision 2030 electronics and specialty plastics manufacturing. With ongoing asset expansion across Asia and the US, SABIC capitalizes on regional feedstock advantages while scaling circular intermediates. Its circularity edge and crude-to-chemicals integration make SABIC a strategic partner for global packaging, energy, and advanced materials markets.

LG Chem pivots intermediates toward batteries, semiconductors, and CO₂ upcycling

LG Chem is redefining its chemical intermediates portfolio in 2026 through AI transformation and R&D-driven innovation. The company is collaborating with Acies Bio to deploy OneCarbonBio™ technology, converting captured CO₂ and plastic waste into high-value intermediates via microbial biotechnology. While remaining a global leader in ABS and PVC intermediates, LG Chem is prioritizing “Winning Tech” electronic materials and semiconductor inputs. Its Automation Lab accelerates process innovation, supporting traditional PVC customers while scaling advanced battery material intermediates. This technology-first approach positions LG Chem at the intersection of circular chemistry, cleantech, and next-generation electronics manufacturing.

Shell integrates circular aromatics and bio-based surfactants across energy-chemical parks

Shell Chemicals operates five integrated Energy and Chemical Parks in 2026, enabling customized production of ethylene oxide, glycols, styrene monomer, and high-purity C9–C11 plasticizer alcohols. Shell is also a major supplier of aromatics such as benzene, toluene, and xylene for global fiber and resin markets. Its Chemical Recycling program converts plastic waste into pyrolysis oil, which feeds directly into crackers to create circular intermediates identical to fossil-based grades. Through NEODOL® bio-based surfactants and low-carbon aromatics, Shell delivers sustainable intermediates at scale for construction, cables, and green personal care applications.

Tata Chemicals anchors inorganic intermediates for solar glass and battery ecosystems

Tata Chemicals leads the inorganic chemical intermediates segment in 2026, with soda ash and silica at the core of its renewable energy strategy. A ₹8,000 crore capex program through 2027 is expanding capacity for high-purity battery and semiconductor ingredients. Tata remains a top global soda ash producer, supplying the booming solar glass industry as renewable installations accelerate worldwide. Its 2026 portfolio focuses on “Sunrise Sectors” including medical devices and electronics, supported by integration within the Tata Group ecosystem. This enables close alignment with automotive and electronics demand, positioning Tata as India’s cornerstone supplier of sustainable inorganic intermediates.

United States: AI-Driven Cost Reset, Asset Rationalization, and Low-Carbon Hydrogen for Chemical Intermediates

The United States chemical intermediates industry is entering a structural efficiency cycle defined by automation, asset optimization, and regional supply chain resilience. In January 2026, Dow Inc. launched its “Transform to Outperform” initiative, targeting a $2 billion Operational EBITDA uplift. The program integrates AI-driven process control, predictive analytics, and advanced automation to simplify upstream derivative production and enhance yield efficiency across key intermediate chemical platforms. As part of this reset, Dow announced a global workforce reduction of approximately 4,500 roles to streamline cost structures within its core operating segments, directly addressing prolonged trough cycles in petrochemical margins. In Q2 2025, the company recorded asset rationalization charges between $630 million and $790 million, primarily targeting energy-intensive upstream units to improve long-term capital productivity.

Decarbonization and feedstock transition are reshaping the competitive landscape. In mid-2025, BASF inaugurated its 54 MW Hy4Chem-EI water electrolysis plant at Ludwigshafen (operational Q1 2025), supplying low-carbon hydrogen for intermediate synthesis across global supply chains, including the U.S. market. Meanwhile, the April 2025 introduction of Demeon® ReNu100, a 100% bio-based propellant, signaled a pivot toward renewable intermediates in aerosol formulations. Facing trade volatility, U.S. manufacturers adopted regionalized production models in late 2025 to mitigate tariff exposure and geopolitical disruptions, strengthening domestic resilience in specialty and bulk chemical intermediates.

China: Xinjiang Capacity Surge, Aromatics Expansion, and Green Manufacturing Enforcement

China’s chemical intermediates sector is expanding through integrated refinery-petrochemical upgrades and value-chain elevation. In September 2025, Sinopec commenced a major upgrade of its Tahe complex in Xinjiang, increasing crude processing capacity to 8.5 million metric tons per year and adding 16 units dedicated to ethylene, paraxylene, and aromatics. This strategic pivot reflects China’s 2026 industrial objective of moving from low-margin fuels to high-value petrochemical intermediates for synthetic fibers, engineering plastics, and advanced manufacturing inputs.

Financial commitment underscores the scale of expansion. Sinopec allocated 27.6 billion yuan ($3.9 billion), or 63% of its H1 2025 capital expenditure, toward upstream exploration and new capacity construction in Xinjiang and Fujian. While South Korea is trimming naphtha-based output, China added approximately 18.7 million tons of new chemical capacity in 2024–2025, positioning itself for the anticipated 2026–2027 upcycle. Concurrently, Beijing accelerated the retirement of inefficient legacy assets in late 2025, replacing them with low-carbon proprietary technologies aligned with the 15th Five-Year Plan. By early 2026, six government departments enforced green building material standards targeting 300 billion yuan in revenue, further stimulating demand for sustainable chemical intermediates.

India: PLI-Backed Import Substitution, Bulk Drug Parks, and 9% Production Growth Outlook

India’s chemical intermediates industry is expanding rapidly under policy-driven localization and pharmaceutical ecosystem development. As of September 2025, the Production Linked Incentive (PLI) scheme for Bulk Drugs attracted cumulative investments of ₹40,890 crore, exceeding initial projections for Key Starting Materials (KSMs) and Drug Intermediates (DIs). The initiative enabled domestic production of 726 APIs, KSMs, and DIs, including 191 intermediates manufactured in India for the first time, significantly reducing import dependency.

Infrastructure acceleration is reinforcing cost competitiveness. By November 2025, the government released ₹180 crore for shared infrastructure in three bulk drug parks, lowering utilities and logistics costs for intermediate manufacturers. Despite global output deceleration, India’s chemical production is forecast to grow 9% in 2026, supported by domestic consumption and “Make in India” incentives. Agrochemical exports reached $5.4 billion in late 2025, boosting demand for cationic and anionic intermediates used in pesticide stabilization. In February 2026, BASF India expanded its Mangalore site with a new specialty line targeting construction and industrial detergent sectors, reinforcing India’s specialty intermediate footprint.

Saudi Arabia: Jafurah Feedstock Expansion, CCS Deployment, and Oil-to-Chemicals Integration

Saudi Arabia is leveraging unconventional gas resources to transform its chemical intermediates value chain. In early 2026, Saudi Aramco commenced production at the Jafurah gas project, one of the world’s largest unconventional gas developments. The project is expected to deliver 630,000 barrels per day of liquid hydrocarbons and 420 million cubic feet per day of ethane, forming a robust feedstock backbone for downstream ethylene and derivative intermediate expansion. Aramco has committed over $100 billion across the project lifecycle, targeting 2 billion cubic feet per day of gas output by 2030.

Decarbonization and circularity are embedded into expansion plans. By 2026, Aramco aims to deploy seven advanced technologies, including gigascale Carbon Capture and Storage hubs, targeting a 15% emissions reduction across chemical intermediate operations. In late 2025, the company introduced a circular petrochemicals initiative designed to reduce industrial waste by 10% through closed-loop recycling and conversion of byproducts. Meanwhile, SABIC is evaluating a large-scale oil-to-chemicals (O2C) complex in Ras Al-Khair, integrating refinery streams directly into high-value intermediate production.

Germany: Steam Cracker Decarbonization, eFurnace Trials, and 1,700 Product Carbon Footprints

Germany’s chemical intermediates industry is restructuring to offset high energy costs while accelerating decarbonization. In July 2025, Dow Inc. announced shutdowns of upstream assets in Böhlen and Schkopau, aiming to complete rationalization by 2027 to restore regional profitability. In February 2026, BASF confirmed accelerated progress on its €1.1 billion restructuring plan to stabilize EBITDA margins.

Technological decarbonization is advancing rapidly. In Q1 2025, BASF began constructing a heat pump system at Ludwigshafen to cut formic acid production emissions by 98% upon 2027 commissioning. In collaboration with SABIC and Linde plc, BASF tested an eFurnace demonstration plant in late 2024, marking a breakthrough in electrified steam cracking. By January 2026, German producers validated over 1,700 product carbon footprints (PCFs), enabling downstream customers to quantify Scope 3 emissions across intermediate supply chains.

South Korea: $7 Billion Shaheen CTC Project and Ethylene Yield Optimization

South Korea is reinforcing its position as a high-efficiency chemical intermediates hub through large-scale crude-to-chemicals (CTC) investments. S-Oil is investing $7 billion in the Shaheen project in Ulsan, majority-backed by Saudi Aramco. Scheduled for completion in 2026, the complex will produce 3.2 million metric tons of petrochemicals and intermediates annually using Aramco’s advanced thermal CTC technology, maximizing ethylene and high-value derivative yields while minimizing lower-margin fuel outputs.

Energy efficiency improvements complement expansion. At the Yeosu site, Korean producers integrated advanced heat exchangers in late 2025, reducing annual CO₂ emissions by approximately 9,000 tons. The Shaheen complex is engineered to optimize feedstock conversion, strengthening South Korea’s competitive advantage in high-purity petrochemical intermediates and polymer precursors within the Asia-Pacific region.

Chemical Intermediates Market Report Scope

Chemical Intermediates market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$125.3 Billion

|

|

Market Size (2034)

|

$256.8 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Product Type (Olefins, Aromatics, Basic Chemical Intermediates, Functional Intermediates), By Feedstock (Petrochemical-based, Bio-based, Recycled Feedstock), By Purity Grade (Industrial Grade, Pharmaceutical Grade, Electronic Grade, Food Grade), By Application (Agrochemicals, Pharmaceuticals, Polymers and Resins, Paints and Coatings, Detergents and Personal Care, Flavors and Fragrances)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow, Sinopec, Reliance Industries, SABIC, Mitsubishi Chemical Group, LyondellBasell Industries, INEOS Group, Evonik Industries, Lotte Chemical, Sumitomo Chemical, Nouryon, Syensqo, Arkema, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Chemical Intermediates Market Segmentation

By Product Type

- Olefins

- Aromatics

- Basic Chemical Intermediates

- Functional Intermediates

By Feedstock

- Petrochemical-based

- Bio-based

- Recycled Feedstock

By Purity Grade

- Industrial Grade

- Pharmaceutical Grade

- Electronic Grade

- Food Grade

By Application

- Agrochemicals

- Pharmaceuticals

- Polymers and Resins

- Paints and Coatings

- Detergents and Personal Care

- Flavors and Fragrances

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Chemical Intermediates Industry

- BASF SE

- Dow

- Sinopec

- Reliance Industries

- SABIC

- Mitsubishi Chemical Group

- LyondellBasell Industries

- INEOS Group

- Evonik Industries

- Lotte Chemical

- Sumitomo Chemical

- Nouryon

- Syensqo

- Arkema

- Huntsman Corporation

*- List not Exhaustive