Ethylene Amines Market to Reach $5.2 Billion by 2034 as Renewable Power Integration and Asian Capacity Expansion Reshape Supply Dynamics

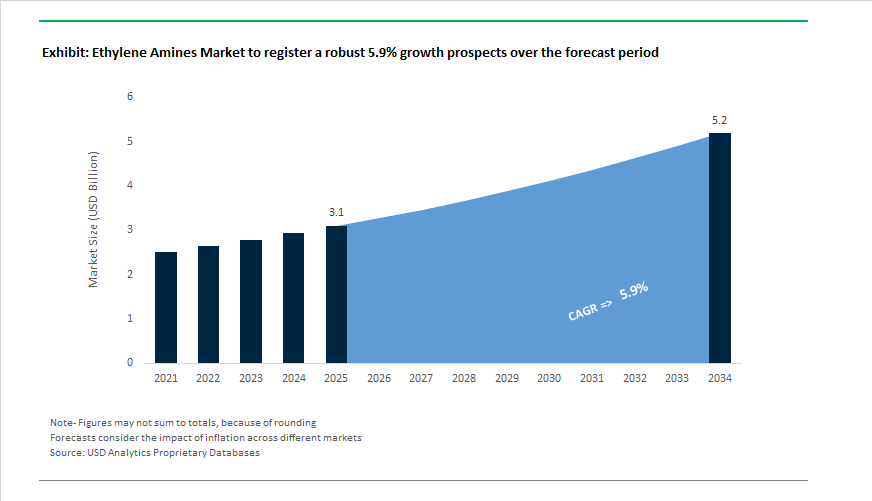

The Ethylene Amines Market is projected to grow from $3.1 billion in 2025 to $5.2 billion by 2034, registering a CAGR of 5.9%. Demand expansion is being driven by multi-sector applications spanning agrochemicals, epoxy curing agents, fuel additives, chelating agents, water treatment chemicals, and pharmaceutical intermediates. While growth remains fundamentally linked to ethylene oxide and ammonia feedstock economics, recent strategic investments, decarbonization initiatives, and tariff-driven trade shifts are redefining competitive positioning across major producing regions.

In July 2025, BASF SE officially started up expanded production facilities for 3-(dimethylamino)propylamine (DMAPA) and polyetheramines (PEA) at its Nanjing Verbund site. The expansion nearly doubled DMAPA capacity and increased PEA output by approximately 25%, strengthening BASF’s foothold in Asia’s personal care and water treatment sectors. This move aligns with China’s accelerating downstream consumption in surfactants, flocculants, and hair-conditioning agents, where amine derivatives serve as critical intermediates.

Sustainability is becoming a structural differentiator. In September 2025, BASF announced that its global standard amine portfolio would transition to production powered entirely by renewable electricity at its Geismar (U.S.) and Nanjing (China) facilities. The shift is projected to reduce the Product Carbon Footprint of its amines by 4%–4.5%, offering customers measurable Scope 3 emission reductions. Similarly, Tosoh Corporation achieved ISCC PLUS certification at its Yokkaichi Complex in November 2025, enabling the commercialization of circular and bio-attributed ethylene amines aligned with European Green Deal procurement requirements.

Portfolio integration strategies are reshaping downstream value capture. Nouryon completed the acquisition of ADOB in January 2024, integrating chelated micronutrients with its upstream amine production. This vertical alignment strengthens its agricultural solutions offering, particularly in specialty fertilizers and crop nutrition formulations where chelating agents derived from ethylene amines are critical for micronutrient stability. Nouryon further reinforced its regional presence by inaugurating a new Innovation Center in Mumbai in November 2024, focusing on localized applications in coatings, agrochemicals, and home care.

Trade policy developments are influencing global supply flows. The introduction of new U.S. tariff measures in late 2025 has reoriented procurement strategies among North American buyers. Import-dependent formulators are accelerating qualification of domestic suppliers such as Dow and Huntsman to mitigate exposure to higher duties on Asian-origin shipments. This shift is expected to compress margins for export-oriented producers while stabilizing regional supply chains.

Upstream feedstock expansion in Asia remains a central growth catalyst. China is scheduled to add approximately 8.5 million tons of new ethylene capacity in 2026, significantly strengthening precursor availability for downstream amine units, including joint ventures like BASF-YPC. Improved feedstock integration enhances operational reliability and reduces volatility in ethylene amine pricing, particularly for core grades such as Ethylenediamine (EDA), Diethylenetriamine (DETA), and Aminoethylethanolamine (AEEA).

In India, policy and industrial restructuring are supporting domestic capability development. India Glycols Limited approved a demerger of its specialty chemicals business in November 2025 to sharpen its focus on high-growth amine derivatives serving pharmaceutical and agrochemical export markets. Concurrently, Balaji Speciality Chemicals expanded capacity for high-purity amine derivatives, targeting import substitution under the Make in India initiative.

Trends and Opportunities in the Ethylene Amines Market

Strategic Shift Toward High-Purity Linear Amines for Water Remediation

- Tightening global regulations on phosphorus discharge, heavy metals, and persistent organic pollutants are accelerating the adoption of ethylene amine-based chelating agents and polymeric amines in water treatment and soil remediation.

- In September 2025, BASF Intermediates confirmed that its Geismar, Louisiana amines complex would operate on 100% renewable electricity by Q4 2025. This transition directly supports municipal water utilities and industrial boiler operators seeking to reduce Scope 3 emissions while continuing to rely on ethylene amine-derived scale inhibitors and dispersants. Sustainability-linked procurement is increasingly influencing chemical selection in public infrastructure projects, particularly in North America and Europe.

- Capacity expansion in Asia-Pacific is reinforcing this trend. The BASF-Sinopec joint venture in Nanjing commissioned a major expansion in July 2025, nearly doubling capacity for 3-(dimethylamino)propylamine and increasing polyetheramine output by roughly 25%. This expansion is directly aligned with rising demand from regional water treatment, crop nutrition, and specialty resin manufacturers, improving local supply security for high-performance amine building blocks.

- From a chemistry standpoint, technical-grade ethylene amines such as EDA and DETA are increasingly specified for EDTA synthesis and next-generation iron chelates. Industry sustainability disclosures in October 2025 emphasized that high-purity amines are essential for producing advanced chelates such as HBED, which are critical for micronutrient delivery and soil remediation in high-pH agricultural zones. This is shifting demand away from commodity blends toward tighter-specification linear amines.

Integration into High-Performance Epoxy Curing for Wind Energy and Automotive

- The global push toward renewable energy and electric mobility is creating sustained demand for ethylene amines as curing agents in high-performance epoxy systems.

- During 2024 and 2025, producers such as Huntsman and Nouryon highlighted the role of DETA and TETA in epoxy formulations used for wind turbine blades and structural automotive components. These amines provide fast reactivity and reliable room-temperature curing, which are essential for automated composite manufacturing lines. By 2025, commercial wind turbine blades exceeding 100 meters in length had become standard, amplifying the need for curing agents that ensure uniform crosslinking and long-term fatigue resistance.

- Sustainability considerations are also entering this segment. In December 2025, Tosoh Corporation received certification under Japan’s Hydrogen Society Promotion Act to utilize low-carbon ammonia as a feedstock. This enables the production of lower-footprint ethylene amines targeted at marine, offshore, and heavy industrial coatings where corrosion resistance and long service life are critical selection criteria.

- Advanced amidoamines derived from ethylene amines are now being specified in high-durability primers for C5-M marine environments. These systems are increasingly adopted in offshore wind foundations, ports, and coastal infrastructure, where they are reported to reduce maintenance intervals by up to 20% compared with conventional curing agents. This performance-driven shift is strengthening ethylene amines’ position in infrastructure-grade coatings.

Biopolymer Functionalization for Advanced Medical Hydrogels

- Ethylene amine chemistry is gaining traction in biomedical engineering, particularly in the functionalization of biopolymers for medical applications.

- In 2025, peer-reviewed studies published across MDPI and PMC demonstrated that ethylene amine derivatives play a critical role in crosslinking chitosan-based hydrogels used in antimicrobial wound dressings. By converting imine linkages into secondary amines, researchers achieved improved mechanical stability and controlled drug release profiles for insulin and other sensitive bio-actives. These advances position ethylene amines as enabling inputs in a global medical hydrogel market valued well above USD 10 billion.

- Beyond wound care, next-generation injectable hydrogels are being developed using amine-amide crosslinked matrices. These systems respond to pH and temperature changes, enabling localized and time-controlled release of anti-inflammatory and regenerative agents in post-surgical recovery. As regulatory pathways for advanced biomaterials mature, demand for pharmaceutical-grade ethylene amine derivatives is expected to accelerate.

Synthesis of Agrochemicals with Novel Modes of Action

- The agrochemical industry is undergoing a fundamental transition as resistance management and environmental compliance reshape active ingredient development. Ethylene amines are emerging as core building blocks in this shift.

- In August 2025, Bayer submitted regulatory dossiers for Icafolin-methyl, the first new herbicide mode of action introduced for post-emergent weed control in nearly three decades. Ethylenediamine and related homologues serve as critical precursors in the synthesis of such complex heterocyclic structures, enabling lower application rates and more selective weed control.

- Formulation innovation is further reinforcing demand. New products such as Corteva Enversa acetochlor formulations, which gained commercial traction in 2025, rely on encapsulation technologies and amine-stabilized carriers. These systems improve soil retention and reduce runoff, helping growers comply with EPA regulations and the EU Water Framework Directive while maintaining high residual efficacy.

Ethylene Amines Market Share and Segmentation Insights

Ethylenediamine Leads Product Portfolio with Broad Multi-Industry Utility

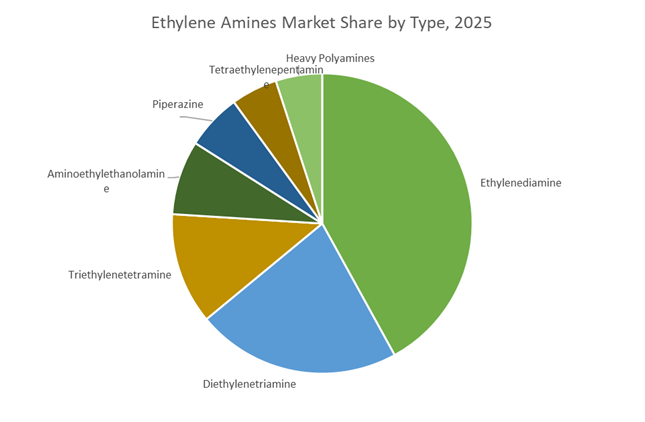

Ethylenediamine (EDA) accounts for 42% of total ethylene amines market share in 2025, reflecting its status as the most versatile and high-volume amine in the portfolio. EDA is a critical precursor for chelating agents such as EDTA, fungicides, paper wet-strength resins, fuel additives, and epoxy curing agents, supporting demand across agriculture, construction, automotive, and water treatment industries. Diethylenetriamine (DETA) holds a significant share due to its polyfunctional reactivity in epoxy systems, asphalt additives, and lubricant formulations. Triethylenetetramine (TETA) maintains importance in corrosion inhibitors and flexible epoxy curing systems for coatings and composites. Aminoethylethanolamine (AEEA) is gaining traction in surfactants and fabric softeners, while piperazine serves pharmaceutical and gas treatment applications. Tetraethylenepentamine (TEPA) and heavy polyamines remain niche but essential in oilfield chemicals and specialty intermediates requiring higher amine functionality.

Agriculture Drives End-Use Demand Supported by Construction and Energy Applications

Agriculture represents 22% of global ethylene amines consumption in 2025, driven by their central role in chelated micronutrients, dithiocarbamate fungicides, and crop protection intermediates. The need for improved nutrient efficiency and crop yield optimization sustains this segment’s leadership. Building and construction form a major secondary market, utilizing ethylene amines in epoxy floor coatings, structural adhesives, and cement additives. Automotive and transportation sectors incorporate these amines in lightweight composites, fuel additives, and polyamide resins for under-hood durability. Oil and gas applications remain critical, particularly for corrosion inhibitors, H₂S scavengers, and drilling fluid additives. Healthcare and pharmaceuticals maintain steady demand through API synthesis and disinfectant production, while water management is an expanding segment leveraging amine-based chelating agents and corrosion control solutions in municipal and industrial treatment systems.

Competitive Landscape of the Ethylene Amines Market

The global ethylene amines market in 2026 is defined by vertically integrated chemical majors and specialty innovators competing on feedstock security, high-purity EDA/DETA/TETA portfolios, and sustainability-driven process technology for epoxy resins, water treatment, electronics, and pharmaceuticals.

Huntsman Corporation drives specialty ethylene amines with JEFFAMINE leadership

Huntsman Corporation operates one of the most comprehensive ethylene amine portfolios globally, led by its JEFFAMINE® platform alongside EDA, DETA, and TETA for polyetheramines and high-performance epoxy systems. In early 2026, Huntsman accelerated portfolio refinement, divesting lower-margin assets to prioritize high-purity amines for semiconductor and pharmaceutical intermediates. Its core strength lies in a global manufacturing footprint spanning 70+ facilities across 30 countries, enabling a resilient “local-for-local” supply model amid tariff volatility. Deep backward integration into ethylene oxide further stabilizes feedstock costs, positioning Huntsman as a premium supplier for coatings, adhesives, electronics encapsulation, and advanced composites.

Nouryon pioneers low-waste EO technology for higher ethylene amines

Nouryon is reshaping the ethylene amines market through its breakthrough EO-based production technology, selectively producing higher amines such as DETA and TETA with significantly reduced waste. In 2026, Nouryon scaled this Swedish-demonstrated platform to commercial levels, targeting nearly 50% carbon intensity reduction. The company also expanded its IMCD distribution partnership across EMEA to strengthen textile and leather chemical penetration. A dominant player in asphalt and road additives, Nouryon’s amidoamines enhance pavement durability across infrastructure projects. Its circular chemistry focus and catalytic innovation position the company as a sustainability benchmark in specialty ethylene amines and performance additives.

Dow Inc. leverages feedstock scale to dominate high-volume EDA supply

Dow Inc. brings unmatched feedstock integration to ethylene amines, benefiting from its global ethylene production scale. In January 2026, Dow launched its “Transform to Outperform” program, targeting a $2 billion operational EBITDA uplift through AI-driven manufacturing and streamlined operations. High-purity ethylenediamine (EDA), which commands roughly 62.9% of total ethylene amine volumes, anchors Dow’s portfolio for water treatment, agrochemicals, EV batteries, and electronics. The company also accelerated digital R&D in 2025 to 2026, using AI modeling to optimize amine formulations, reinforcing Dow’s position as a cost leader and innovation driver in industrial-grade amines.

Tosoh Corporation expands Asian amine capacity for catalysts and water treatment

Tosoh Corporation remains a leading Asian supplier of ethylene amines, offering EDA, DETA, TETA, TEPA, and piperazine through continuous EDC process optimization since 1967. During 2025 to 2026, Tosoh expanded specialized production of RZETA® amine catalysts to support Southeast Asia’s polyurethane foam construction boom. Its ethylene amines also serve chelating agents and ion exchange resins, critical for large-scale water treatment projects across China and India. With strong EDC process excellence and regional manufacturing reliability, Tosoh delivers consistent high-purity products for coatings, resins, and environmental applications.

BASF SE integrates sustainable ethylene amines through its Ludwigshafen Verbund

BASF SE anchors the European ethylene amines market via its Ludwigshafen Verbund, the global benchmark for cross-plant heat and material integration. Reporting €59.7 billion in 2025 sales, BASF targets €6.7 to €7.2 billion EBITDA in 2026 while divesting non-core assets to sharpen focus on crop protection and pharmaceutical intermediates. In early 2026, BASF launched bio-attributed ethylene amines for sustainable surfactants, aligning with EU REACH and environmental directives. Its deep integration significantly lowers energy cost per ton, positioning BASF as a strategic supplier of low-carbon amines for specialty chemicals, agriculture, and life sciences.

China: Ethylene Abundance Driving Integrated Ethylene Amine Scaling

China’s ethylene amines market is structurally advantaged by the country’s world-scale upstream ethylene expansion. By the end of 2025, national ethylene capacity exceeded 62 million metric tons, creating a cost-efficient feedstock base for ethylene amine derivatives such as ethylenediamine (EDA) and diethylenetriamine (DETA). This upstream dominance is translating into aggressive downstream integration, particularly in epoxy curing agents, surfactants, and automotive additives. A key example is the BASF–YPC Verbund complex in Nanjing, where the expanded ethylene amines unit reached full commercial ramp-up in 2025, enabling tightly integrated production that minimizes logistics costs and energy losses while serving domestic demand growth.

Specialty and purity upgrades are equally central to China’s strategy. In November 2024, Evonik initiated a major expansion of its Nanjing specialty amines facility, with completion targeted for 2026 to address demand for high-purity grades in agrochemical formulations and automotive coatings. Regulatory pressure is reinforcing this shift. Stricter VOC caps in the Yangtze River Delta are accelerating the replacement of solvent-heavy systems with high-performance ethylene amine curing agents. Parallel to this, China’s push for automotive self-sufficiency, with vehicle output targeting 35 million units by 2025, is driving domestic synthesis of ash-free fuel additives derived from ethylene amines. The successful startup of Wanhua Chemical’s Phase II ethylene project in April 2025 further strengthens the availability of ethylene oxide intermediates, reinforcing China’s control over the full ethanolamine and ethylene amine value chain.

United States: Price Discipline and Functional Repositioning

The U.S. ethylene amines market in 2025–2026 is characterized by price realignment and functional repositioning rather than capacity expansion. Major producers, including Dow, implemented price increases for products such as aminoethyl ethanolamine and piperazine during late 2024 and early 2025, reflecting higher feedstock costs and tighter supply chain discipline. This correction phase is coinciding with a regulatory-driven pivot toward sustainability-oriented applications.

Under the EPA’s SNAP program evolution for 2025–2026, ethylene amines are increasingly prioritized as intermediates for green chelating agents designed to replace phosphate-based systems in industrial water treatment. At the same time, the U.S. Department of Agriculture is channeling AFRI grants into biodegradable pesticide delivery systems that rely on ethylene amine building blocks. On the supply side, Gulf Coast infrastructure upgrades in 2025 focused on AI-driven process control retrofits, improving yields of heavier amines such as TETA and TEPA. These grades are seeing rising demand from shale gas drilling, where amine-based corrosion inhibition and gas treatment remain critical.

India: Import Substitution and Agrochemical-Led Growth

India’s ethylene amines market is entering a phase of structural strengthening driven by policy-backed localization. The NITI Aayog–led chemical hubs initiative announced in July 2025 is creating shared infrastructure and viability gap funding to catalyze domestic production of specialty amines. This framework directly supports the reduction of import dependency for EDA and related derivatives, particularly in pharmaceuticals and textiles. Complementing this, Production-Linked Incentive schemes extended in 2025 are encouraging private investment in localized ethylene amine synthesis.

Demand-side momentum is led by agrochemicals. Under the Aatmanirbhar Bharat mission, India’s use of ethylene amines in pesticide and herbicide formulations reached record levels in 2025, supported by robust export demand for generic intermediates. Feedstock security is improving in parallel. The HPCL Rajasthan Refinery, scheduled for full operational status by late 2025, is engineered to maximize olefin outputs, providing a stable domestic base for amine producers.

Germany & Benelux: Cost Reset and Regulatory Precision

In Europe, the ethylene amines market is being reshaped by a rare combination of feedstock innovation and regulatory tightening. The upcoming ethane-fed cracker in Antwerp, developed by INEOS, is expected to start up in the 2026–2027 window. With 1.45 million metric tons of ethylene capacity, this project introduces a lower-cost alternative to naphtha-based ethylene, disrupting the regional cost curve for downstream amines.

At the same time, the 2026 REACH recast is compelling manufacturers across Germany and the Benelux to upgrade purification, handling, and trace-impurity control systems, particularly for personal care and cosmetic-grade ethylene amines. Competitive intensity is increasing following BASF’s commissioning of a world-scale hexamethylenediamine plant in France in June 2025. This expansion enhances regional amine precursor availability and exerts pricing and margin pressure across Europe’s broader amine portfolio.

Brazil: Feedstock Reinforcement for Downstream Amines

Brazil’s role in the global ethylene amines market is strengthening through upstream petrochemical investment rather than direct derivative capacity announcements. In October 2025, Braskem approved a R$ 4.2 billion expansion of its Rio de Janeiro complex, increasing ethylene capacity by 220,000 tons under the REIQ framework. This feedstock reinforcement secures long-term availability for downstream amine production, particularly for regional demand in resins, agriculture, and industrial chemicals. While derivative expansion remains selective, Brazil’s strategy is clearly oriented toward feedstock resilience and cost stability through the 2025–2026 cycle.

Strategic Summary: Ethylene Amines Market by Country (2025–2026)

Ethylene Amines Market County Level Snapshot

|

Country / Region

|

Core Strategic Driver

|

Value Chain Focus

|

Competitive Implication

|

|

China

|

World-scale ethylene integration

|

EDA, DETA, specialty amines

|

Global cost and volume leadership

|

|

United States

|

Price discipline and sustainability

|

Chelants, gas treatment, agrochemicals

|

Functional, high-margin repositioning

|

|

India

|

Import substitution and policy support

|

Agrochemicals, pharma, textiles

|

Rapid domestic capacity build-out

|

|

Germany & Benelux

|

Ethane cracking and REACH compliance

|

High-purity personal care amines

|

Cost reset with regulatory precision

|

|

Brazil

|

Upstream ethylene expansion

|

Feedstock for downstream amines

|

Long-term supply security

|

Ethylene Amines Market Report Scope

Ethylene Amines Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2034)

|

$5.2 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Type (Ethylenediamine, Diethylenetriamine, Triethylenetetramine, Tetraethylenepentamine, Aminoethylethanolamine, Piperazine, Heavy Polyamines), By Application (Resins and Coatings, Agrochemicals, Chelating Agents, Water Treatment, Petroleum and Fuel Additives, Pharmaceuticals, Personal Care, Textiles), By End-Use Industry (Agriculture, Automotive and Transportation, Building and Construction, Oil and Gas, Healthcare and Pharmaceuticals, Water Management)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Huntsman International LLC, Nouryon, Tosoh Corporation, Delamine B.V., Eastman Chemical Company, China Petroleum & Chemical Corporation, Diamines and Chemicals Limited, Evonik Industries AG, Arabian Amines Company, Mitsui Chemicals, Inc., Resonac Corporation, Hebei Chengxin Co., Ltd., Akzo Nobel N.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ethylene Amines Market Segmentation

By Type

- Ethylenediamine

- Diethylenetriamine

- Triethylenetetramine

- Tetraethylenepentamine

- Aminoethylethanolamine

- Piperazine

- Heavy Polyamines

By Application

- Resins and Coatings

- Agrochemicals

- Chelating Agents

- Water Treatment

- Petroleum and Fuel Additives

- Pharmaceuticals

- Personal Care

- Textiles

By End-Use Industry

- Agriculture

- Automotive and Transportation

- Building and Construction

- Oil and Gas

- Healthcare and Pharmaceuticals

- Water Management

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ethylene Amines Industry

- BASF SE

- Dow Inc.

- Huntsman International LLC

- Nouryon

- Tosoh Corporation

- Delamine B.V.

- Eastman Chemical Company

- China Petroleum & Chemical Corporation

- Diamines and Chemicals Limited

- Evonik Industries AG

- Arabian Amines Company

- Mitsui Chemicals, Inc.

- Resonac Corporation

- Hebei Chengxin Co., Ltd.

- Akzo Nobel N.V.

*- List not Exhaustive