Green Chelating Agents Market to Reach $5.1 Billion by 2034 at 6.5% CAGR Driven by GLDA Innovation, Portfolio Restructuring, and Sustainable Home Care Reformulation

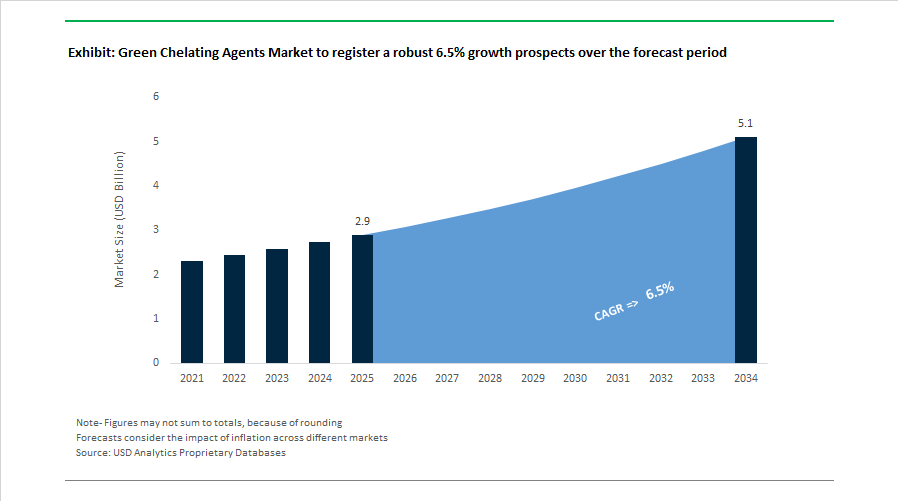

The Green Chelating Agents Market is projected to grow from $2.9 billion in 2025 to $5.1 billion by 2034, registering a CAGR of 6.5%. Expansion is fueled by accelerating substitution of conventional chelants such as EDTA and phosphonates with biodegradable alternatives including GLDA and EDDS across home care, personal care, water treatment, and industrial cleaning formulations. Regulatory pressure on aquatic toxicity, carbon footprint reduction mandates, and multinational brand commitments to sustainable chemistry are reshaping procurement strategies and supplier portfolios across Europe, North America, and Asia-Pacific.

In late 2023 and through 2024, Nouryon expanded the commercial rollout of Dissolvine® GL Premium, positioned as a highly concentrated GLDA-based chelating agent designed to reduce transportation emissions and packaging waste. In July 2024, Nouryon entered a strategic distribution agreement with Brenntag SE, extending North American market access for Dissolvine® green chelants. During 2025, LANXESS AG completed the divestment of its Urethane Systems business to UBE Corporation, formally exiting polymer activities to concentrate on specialty intermediates and consumer protection segments. In December 2025, BASF SE signed an agreement to divest its optical brightening agent business to Catexel, sharpening its strategic emphasis on high-growth sustainable segments within Nutrition & Care.

Product innovation accelerated in 2025. In October 2025, Nouryon introduced next-generation GLDA-based solutions at the SEPAWA Congress, engineered for optimized water hardness control in laundry and dishwashing applications while meeting stringent biodegradability standards. In November 2025, Evonik Industries AG partnered with InVitria to supply animal component-free recombinant human serum albumin, reflecting broader integration of high-purity chelating and stabilization technologies into biopharmaceutical production systems. In August 2025, Evonik consolidated site infrastructure operations into SYNEQT GmbH, operational January 2026, streamlining chemical park efficiency at major production hubs such as Marl where specialty additives are manufactured. In parallel, LANXESS announced plans in August 2025 to streamline its global network, including closure of the Widnes site in 2026, reallocating capital toward efficient, sustainable specialty chemical facilities.

Recognition and regional capacity expansion reinforced growth momentum into 2026. In February 2026, Nouryon received Henkel Consumer Brands’ 2025 Sustainability Award for its degradable water-softening technologies integrated into Henkel AG & Co. KGaA home care formulations, supporting Henkel’s objective to transition toward fully sustainable chemistry. The same month, BASF announced production expansion at its Mangalore, India site, strengthening supply infrastructure for sustainable additives and chelating agents serving South Asian architectural coatings and construction chemical markets. In January 2026, Innospec Inc. highlighted growth within its Performance Chemicals segment, driven by proprietary EDDS-based technologies tailored to clean-label and safety-focused consumer product brands.

The Green Chelating Agents Market outlook reflects accelerated GLDA and EDDS adoption, portfolio realignment among major specialty chemical producers, distribution network expansion, infrastructure optimization, and brand-driven sustainability commitments. Competitive differentiation increasingly depends on biodegradability performance, carbon intensity metrics, high-concentration formulations, regulatory compliance across EU and U.S. frameworks, and integration into home care, personal care, water treatment, and biopharmaceutical stabilization applications.

Green Chelating Agents Market Trends and Strategic Growth Opportunities

Regulatory Substitution of Phosphonates in Consumer Detergents

The global green chelating agents market is being reshaped by regulatory pressure to eliminate phosphonates such as EDTMP and HEDP from household and institutional detergents. The revised EU Detergents Regulation introduced during 2024 and implemented through 2025 extends biodegradability requirements to all organic ingredients present at meaningful concentrations, directly targeting persistent chelants linked to aquatic eutrophication. This shift is compelling multinational home care brands to accelerate reformulation timelines and secure compliant chelation solutions that preserve cleaning performance in hard water conditions.

Regulatory milestones are translating into rapid product commercialization. In April 2025, BASF introduced Trilon G, a bio-based GLDA chelant engineered to achieve approximately 60% biodegradation within 28 days. The product is positioned for hand dishwashing and laundry formulations across Europe and North America, where phosphorus thresholds are tightening fastest. In the United States, policy momentum is reinforcing this transition. The fiscal year 2025 National Defense Authorization Act mandates that the Department of Defense procure Environmental Protection Agency Safer Choice-certified cleaning products, directly benefiting green chelants listed on the Safer Chemical Ingredients List by prioritizing them in large-scale institutional purchasing.

Chemical producers are reorganizing portfolios to capture this compliance-driven demand. Nouryon restructured its operations in late 2024 to establish a dedicated Consumer and Life Sciences segment, channeling capital toward its Dissolvine GL and Dissolvine M ranges based on GLDA and MGDA chemistry. This strategic realignment reflects a broader industry consensus that biodegradable chelants are becoming mandatory inputs rather than premium alternatives in mainstream detergent formulations.

Closed-Loop Water Circularity Drives Industrial Uptake

Heavy industries with high water intensity are emerging as a second major growth engine for green chelating agents. Pulp and paper, textiles, and specialty chemicals producers are increasingly adopting zero liquid discharge strategies that rely on recirculated process water. In these closed-loop systems, non-biodegradable chelants accumulate over time and disrupt process chemistry, making biodegradable alternatives essential for long-term operational stability.

In renewable fiber processing, green chelants are enabling more efficient and circular bleaching operations. Industrial programs executed during 2024 and 2025 demonstrated that GLDA-based systems can effectively control iron and manganese ions during hydrogen peroxide bleaching, maintaining fiber brightness even at high recycled content levels. Regulatory pressure is reinforcing adoption in Asia. In 2024, the Ministry of Ecology and Environment issued stricter national standards for heavy metal discharge from industrial parks. This prompted wastewater treatment facilities in Guangdong and Jiangsu to deploy biodegradable chelants that sequester metals for removal without increasing chemical oxygen demand in effluents.

Green chelants are also becoming integral to chemical recycling infrastructure. BASF’s loopamid initiative in Shanghai, launched at commercial scale in 2025, uses advanced depolymerization processes that require stable auxiliaries to manage metal impurities in mixed textile waste. This reflects a wider trend in which biodegradable chelants are embedded within circular manufacturing systems to enable high-purity output while meeting environmental compliance thresholds.

Precision Agriculture and Biodegradable Soil Remediation

Agriculture represents a high-impact opportunity for green chelating agents as regulators and growers move away from persistent synthetic chelates toward biodegradable, amino acid-based alternatives. These chelants improve micronutrient delivery while reducing the risk of heavy metal mobilization into groundwater. Research published during 2024 and 2025 demonstrated that chelants such as GLDA and IDS significantly enhance plant uptake of cadmium, lead, and zinc during soil remediation, while degrading rapidly after application to minimize residual environmental risk.

Field trials have translated these findings into commercial value. Use of Fe-GLDA and similar formulations reduced leaf chlorosis by up to 60% and improved yields by 8 to 10% within a single growing season. This performance is accelerating adoption of bio-active fertilizers that align with export standards for sustainably produced crops. In regenerative and organic farming systems, amino acid chelates are increasingly preferred in precision fertigation due to their high solubility and ability to prevent nutrient lock-up in alkaline and calcareous soils, particularly in large grain-producing regions.

Process Optimization in Biogas and Bio-Refining Operations

The rapid expansion of biogas and bioethanol capacity worldwide is creating a specialized opportunity for green chelating agents in energy production. Anaerobic digesters and fermentation systems require precise control of trace metals to maintain microbial health. Biodegradable chelants enable selective management of these ions, preventing inhibition and stabilizing gas yields across extended operating cycles.

Scale control is another critical application. GLDA-based formulations are increasingly used to descale heat exchangers and boilers in bio-refineries, where operating temperatures can exceed 170 degrees Celsius under alkaline conditions. Unlike EDTA, these chelants provide strong metal binding while remaining biodegradable, allowing effective cleaning without long-term environmental persistence. As sustainability credentials are central to bio-energy economics, producers are standardizing biodegradable auxiliaries as part of their core process design. Nouryon is positioning premium GLDA solutions as direct replacements for legacy chelants, aligning metal control performance with the low-carbon and circular economy objectives of modern bio-refining facilities.

Green Chelating Agents Market Share and Segmentation Insights

Organic Acid-Based Chelants Lead the Green Chelating Agents Market Through Biodegradable Chemical Solutions

Organic Acid-Based Chelants accounted for 42.80% of the Green Chelating Agents Market share in 2025, making them the most widely used product category within sustainable chelation chemistry. These chelating agents include gluconic acid, citric acid, glucaric acid, tartaric acid, and succinic acid, all of which are derived from renewable feedstocks and exhibit strong biodegradability profiles. Their environmental compatibility has made them important alternatives to traditional chelants such as EDTA, NTA, and phosphate-based builders, which face increasing regulatory restrictions due to ecological persistence and water pollution concerns. Organic acid-based chelants are widely applied in detergent formulations, industrial cleaning solutions, water treatment chemicals, and metal processing operations, where they bind metal ions and improve formulation performance. In 2025, innovation within this segment has focused on synergistic chelant blending strategies. Chemical formulators are developing optimized combinations of multiple organic acids together with complementary green additives, enabling improved metal ion sequestration efficiency and formulation stability. These blended systems are increasingly used in phosphate-free automatic dishwasher detergents, industrial descaling agents, and environmentally compliant cleaning products.

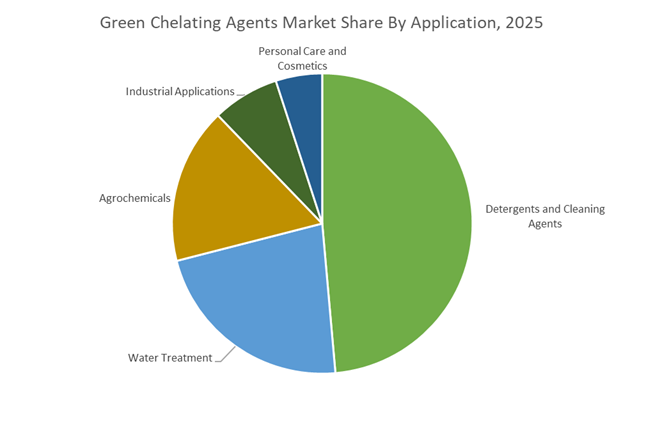

Detergents and Cleaning Agents Drive the Largest Demand for Green Chelating Agents

Detergents and Cleaning Agents represented 48.60% of the Green Chelating Agents Market share in 2025, making this sector the primary demand center for environmentally friendly chelating systems. Chelating agents are essential components of cleaning formulations because they bind calcium, magnesium, and other metal ions present in hard water, preventing these ions from interfering with surfactant activity and improving cleaning efficiency. The shift toward green chelating agents has accelerated as governments and environmental agencies increasingly regulate the use of phosphate builders and non-biodegradable chelants in household and industrial detergents. In response, detergent manufacturers have adopted biodegradable chelant systems derived from organic acids and other renewable feedstocks, allowing them to meet regulatory requirements while maintaining product performance. In 2025, the expansion of phosphate bans across multiple global regions, including North America, Europe, and emerging markets in Latin America and Asia, is significantly influencing detergent formulation strategies. Multinational consumer goods companies increasingly prefer standardized global detergent formulations incorporating green chelating systems, creating economies of scale that reduce ingredient costs and accelerate adoption across both regulated and non-regulated markets.

Competitive Landscape in Green Chelating Agents Market

BASF SE Leads Bio-Based GLDA and MGDA Commercialization

BASF SE remains the global volume leader in biodegradable chelating agents, leveraging its Verbund integration to optimize cost, purity, and feedstock efficiency. In April 2025, BASF launched Trilon® G, a GLDA-based chelate containing approximately 56% renewable carbon and achieving around 60% biodegradation within 28 days. The company is positioning Trilon® M, based on MGDA chemistry, as the benchmark phosphate-free builder for automatic dishwashing detergents. In early 2025, BASF introduced Lasanol B, derived from renewable raw materials, targeting agricultural micronutrient stabilization and water treatment applications. Its Care Chemicals division is scaling bio-based capacity to support formulators aiming to meet 2030 ESG commitments without sacrificing performance or cost efficiency.

Nouryon Strengthens GLDA Leadership Through High-Solubility Innovation

Nouryon holds a strong patent portfolio in bio-based amino acid chemistry and leads the high-solubility GLDA segment through its Dissolvine® GL brand. Produced from monosodium L-glutamic acid, Dissolvine® GL is marketed as an eco-friendly strong chelate with effective metal ion sequestration across a pH range of 2 to 12. In May 2025, Nouryon completed the acquisition of AkzoNobel’s legacy chelating agents business, consolidating global supply and customer relationships. Its 2026 R&D focus emphasizes metal ion control and biocide boosting performance in disinfectants and personal care formulations. The Dissolvine® GL Premium line is optimized for compatibility with PVOH films, addressing rapid growth in unit-dose and detergent pod markets.

Dow Inc. Expands Biodegradable Alternatives in North America

Dow Inc. is accelerating the shift from traditional chelating agents toward readily biodegradable alternatives under a collaborative innovation strategy. In March 2025, Dow partnered with Corbion to develop next-generation biodegradable chelates using lactide-based dextrose technology. Its VERSENE™ portfolio includes partially neutralized variants for food and pharmaceutical uses, while 2026 expansions emphasize biodegradable grades for textile processing and pulp and paper applications. Dow is applying AI-driven analytics to manage raw material volatility across its non-EDTA portfolio. The company continues supplying both legacy and green chelates, incentivizing conversion through volume-based pricing strategies.

Jungbunzlauer Dominates Sodium Gluconate Fermentation Segment

Jungbunzlauer Suisse AG leads the natural fermentation segment, with sodium gluconate accounting for approximately 39.5% of total green chelating agent volume in 2026. Produced from non-GMO corn-based feedstocks, sodium gluconate is widely used as a concrete admixture, set retarder, and industrial cleaning chelate due to its biodegradability and food-safe profile. In early 2026, the company published comparative data demonstrating superior copper chelation at 40°C compared to MGDA and GLDA in certain applications. Its NAGLUSOL® line is expanding within green construction, providing non-corrosive, non-toxic retarder systems. Fermentation excellence and vertical integration underpin Jungbunzlauer’s competitive strength in large-volume industrial segments.

Innospec Targets Clean Beauty and Selective Chelation Applications

Innospec Inc. operates as a niche innovator in specialty biodegradable chelates for personal care and high-performance cleaning systems. Its Natrlquest® E30, based on trisodium ethylenediamine disuccinate, offers transition-metal selectivity, preferentially binding iron and copper over calcium and magnesium. This selectivity supports antioxidant stabilization and foam preservation in shampoos and conditioners by preventing trace-metal-induced discoloration. In 2026, Innospec introduced Natrlquest® E80 in high-active powder form to reduce transportation emissions and plastic packaging waste. The company is capitalizing on the Clean Beauty trend by promoting EDTA alternatives that minimize aquatic toxicity and skin sensitization risk while maintaining strong chelation efficiency.

United States: Regulatory Pull Accelerates Bio-Based Chelant Adoption

The United States green chelating agents industry is being reshaped by regulatory demand signals and formulation reformulation across household, industrial, and energy applications. The Environmental Protection Agency has set a clear performance objective to expand the Safer Choice portfolio to 2,300 certified products by late 2026, up from 1,724 in 2024. This expansion explicitly prioritizes readily biodegradable chelators such as MGDA and GLDA, accelerating their substitution for legacy EDTA in detergents, hard-surface cleaners, and institutional sanitation products. As a result, formulators are redesigning recipes to optimize surfactant efficiency under lower dosage constraints.

Commercial momentum intensified with the April 2025 launch of Trilon® G by BASF in the U.S. market. The GLDA-based chelant, approximately 56% bio-based, is positioned to enhance detergency performance in laundry and manual dishwashing systems while meeting Safer Choice criteria. In parallel, updated TSCA reporting rules effective May 2026 require more detailed environmental fate and transport data for biodegradable aminopolycarboxylates, raising entry barriers for new submissions. Beyond cleaning, oilfield chemistry in the Permian Basin is shifting toward green chelants for scale inhibition, replacing EDTA to align with stricter state-level groundwater protection requirements. To reduce import risk, U.S. producers are also onshoring bio-succinic acid production, strengthening domestic supply chains for EDDS precursors.

Germany: Portfolio Focus and Circular Feedstock Innovation

Germany remains the strategic nerve center for green chelant development in Europe, driven by portfolio rationalization and sustainability-led feedstock innovation. In December 2025, BASF signed an agreement to divest its optical brightening agent business to Catexel, a move designed to concentrate capital and R&D on higher-growth segments such as biodegradable chelating agents. This sharpened focus aligns with BASF’s emphasis on Trilon M and other next-generation chelants positioned for EU Green Deal compliance in 2026.

German producers have also expanded ISCC PLUS certification across bio-circular chelant lines, enabling mass-balance claims that satisfy procurement requirements from European consumer goods and industrial clients. At the Marl chemical cluster, a 2025 waste-to-chelant pilot has demonstrated the feasibility of producing IDSA through fermentation routes using agricultural side-streams such as sugars and amino acids. This approach reduces reliance on petrochemical feedstocks while reinforcing Germany’s leadership in low-carbon specialty chemical manufacturing.

India: Policy-Led Scale-Up and Application Diversification

India’s green chelating agents market is being propelled by policy alignment and rapid application uptake in food processing, agriculture, and water reuse. Under the BioE3 policy introduced in 2025, the government designated bio-based chemicals and enzymes as a priority vertical, positioning India as a global biomanufacturing hub through public-private partnerships. This framework is catalyzing investment in fermentation-based chelants and localized scale-up of GLDA and IDSA production.

Regulatory momentum is equally significant. The Food Safety and Standards Authority of India has introduced new purity benchmarks for additives used in food-contact surface cleaning, effective early 2026. These rules explicitly favor GLDA over phosphate-based systems in food-processing sanitation. In agriculture, Indian innovators showcased HBED chelates in October 2025 to address micronutrient deficiencies in high-pH soils, supporting climate-resilient crop programs. Meanwhile, the Central Pollution Control Board wastewater reuse guidelines issued in 2025 have driven increased adoption of biodegradable sequestering agents to prevent membrane scaling in industrial recycling plants.

China: Localization, Digital Manufacturing, and Stewardship Recognition

China’s green chelating agents industry is advancing through localized R&D, digitalized manufacturing, and corporate stewardship initiatives. In 2025, Nouryon received the Responsible Care® Company Award from the Association of International Chemical Manufacturers, recognizing its contributions to freshwater conservation and sustainable manufacturing across seven Greater China sites. This recognition reflects rising expectations for environmental performance among multinational and domestic suppliers alike.

To deepen market relevance, Nouryon opened a dedicated Innovation Center in Shanghai in November 2025, focused on tailoring MGDA and GLDA formulations for Chinese personal care and home care brands. On the production side, chelant manufacturers in the Shandong cluster are transitioning to Smart Green Workshop models under the 2026 industrial modernization plan. These facilities integrate AI-driven catalytic monitoring, reducing byproduct formation in MGDA synthesis by an estimated 10 to 15% and improving overall process efficiency.

The Netherlands and Belgium: European Control Hub and Low-Carbon Manufacturing

The Netherlands and Belgium play a pivotal role in coordinating Europe’s transition away from phosphate-based chelation systems. Nouryon’s dual-headquarters structure in Amsterdam and Radnor has centralized strategic oversight of Dissolvine® GL and Dissolvine® M production, enabling faster alignment with EU detergent and industrial cleaning regulations. This centralized model supports consistent product specifications as European customers accelerate reformulation timelines.

In Belgium, a major renewable energy project completed in Mons in August 2025 has materially reduced the cradle-to-gate carbon footprint of chelating agents and surfactants produced at the site. By integrating wind and solar power into manufacturing operations, producers are positioning their green chelants to meet 2026 sustainability thresholds demanded by multinational consumer goods companies and public procurement frameworks across the European Union.

Comparative Snapshot: Green Chelating Agents Industry by Country

Green Chelating Agents Market County Level Snapshot

|

Country / Region

|

Primary Strategic Driver

|

Structural Impact on Industry

|

|

United States

|

Safer Choice expansion and TSCA oversight

|

Rapid substitution of EDTA in cleaning and energy

|

|

Germany

|

Portfolio focus and circular feedstocks

|

Advanced bio-circular chelant innovation

|

|

India

|

BioE3 policy and wastewater reuse

|

Fast scale-up across food, agri, and utilities

|

|

China

|

Localization and smart manufacturing

|

Cost-efficient MGDA and GLDA production

|

|

Netherlands & Belgium

|

EU coordination and renewable energy

|

Low-carbon supply for phosphate-free transition

|

Green Chelating Agents Market Report Scope

Green Chelating Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.9 Billion

|

|

Market Size (2034)

|

$5.1 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Product Type (Aminopolycarboxylates, Organic Acid-Based Chelants, Polymeric Green Chelants, Other Bio-Based Chelants), By Form (Liquid, Solid), By Application (Detergents and Cleaning Agents, Agrochemicals, Water Treatment, Personal Care and Cosmetics, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Nouryon, Dow Inc., Akzo Nobel N.V., LANXESS AG, Kemira Oyj, Innospec Inc., Jungbunzlauer Suisse AG, Deepak Nitrite Limited, Mitsubishi Chemical Group, Hebei Think-Do Chemicals, Aquapharm Chemical Pvt. Ltd., Ava Chemicals Private Limited, Tate & Lyle PLC, Archer Daniels Midland Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Green Chelating Agents Market Segmentation

By Product Type

- Aminopolycarboxylates

- Organic Acid-Based Chelants

- Polymeric Green Chelants

- Other Bio-Based Chelants

By Form

By Application

- Detergents and Cleaning Agents

- Agrochemicals

- Water Treatment

- Personal Care and Cosmetics

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Green Chelating Agents Market

- BASF SE

- Nouryon

- Dow Inc.

- Akzo Nobel N.V.

- LANXESS AG

- Kemira Oyj

- Innospec Inc.

- Jungbunzlauer Suisse AG

- Deepak Nitrite Limited

- Mitsubishi Chemical Group

- Hebei Think-Do Chemicals

- Aquapharm Chemical Pvt. Ltd.

- Ava Chemicals Private Limited

- Tate & Lyle PLC

- Archer Daniels Midland Company

*- List not Exhaustive