Surfactants Market 2025–2034: $85 Billion to $133 Billion at 5.1% CAGR Driven by Bio-Based Surfactants, Oilfield EOR Chemistry, and Sustainable Home Care Innovation

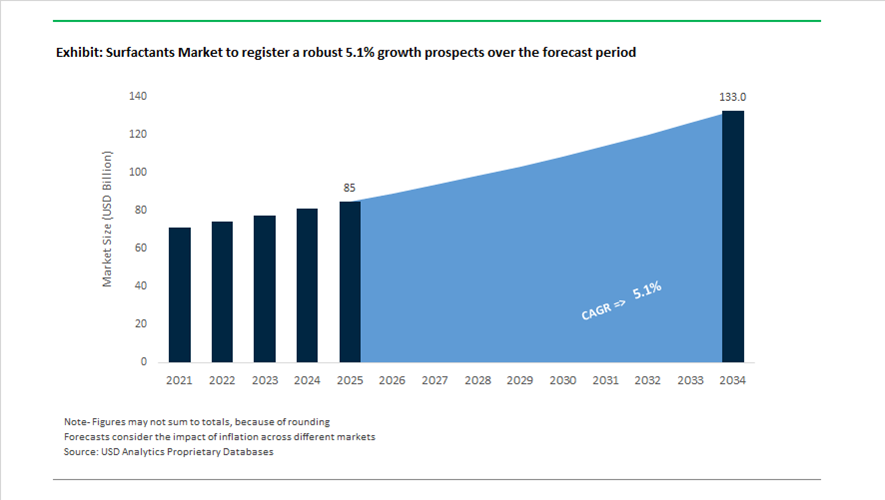

The global surfactants market is valued at $85 billion in 2025 and is projected to reach $133 billion by 2034, expanding at a CAGR of 5.1%. Growth is supported by rising demand for anionic surfactants, nonionic surfactants, cationic surfactants, amphoteric surfactants, alkyl polyglucosides (APGs), alpha olefin sulfonates (AOS), rhamnolipid biosurfactants, and specialty oilfield surfactants across home care, personal care, agriculture, oilfield chemicals, and industrial cleaning applications. Regulatory pressure on palm oil derivatives, PFAS elimination, cold-water detergent performance, and carbon footprint reduction is accelerating the shift toward bio-based, ISCC PLUS-certified, and biodegradable surfactant chemistries. Manufacturers are reallocating capital from commodity coatings and low-margin intermediates toward high-purity performance surfactants and sustainable feedstock innovation.

Industrial-scale biosurfactant commercialization accelerated in 2024 and 2025. In early 2024, Evonik inaugurated the world’s first industrial-scale rhamnolipid plant in Slovakia, enabling production of glycolipid biosurfactants for premium shampoos and eco-labeled household cleaners. In January 2025, Planet Chemical announced a major expansion at its Ohio facility to double alpha olefin sulfonate production capacity by 2027, strengthening North American supply of high-foaming anionic surfactants for detergents and oilfield applications. In April 2025, Nouryon launched Armocare Aqua 12, an ISCC PLUS-certified biodegradable surfactant for hair care formulations aligned with clean beauty standards. In October 2025, BASF finalized the sale of its decorative paints business to focus capital on Performance Chemicals, including bio-based surfactants and APG expansion under its Nutrition & Care and Industrial Solutions segments. During the same month, Sasol introduced LIVINEX IO 7, the first insect oil-derived nonionic surfactant produced from black soldier fly larvae oil, offering a palm-free alternative for home and industrial cleaning. In early 2025, SLB completed its $7.7 billion acquisition of ChampionX, strengthening its portfolio of specialty surfactants for Enhanced Oil Recovery and oilfield production chemicals through integration of digital reservoir modeling with chemical enhancement platforms.

Strategic consolidation and capacity optimization intensified in 2026. In January 2026, Clorox completed its $2.25 billion acquisition of GOJO Industries, combining heavy-duty surface surfactant formulations with skin-compatible hygiene technologies under the Purell brand. In February 2026, Nouryon introduced the industry’s first 100% bio-based and biodegradable carboxymethylcellulose designed to enhance surfactant performance in cold-water laundry systems by improving soil suspension and anti-redeposition efficiency. In February 2026, Stepan confirmed start-up of its Pasadena, Texas site, optimizing regional surfactant supply for agricultural adjuvants and oilfield markets. In January 2026, Syensqo completed the divestiture of its Oil & Gas Business Unit to SNF Group, reallocating R&D resources toward personal care and advanced materials. In January 2026, Clariant appointed new leadership for its Care Chemicals division to accelerate sustainable specialty surfactant growth and integrate high-value cosmetic ingredient portfolios. These structural portfolio realignments, bio-based feedstock innovations, oilfield surfactant integration, and regional capacity expansions are shaping the competitive landscape of the global surfactants market through 2034.

Structural Trends and Opportunity Hotspots in the Global Surfactants Market

Regulatory Reformulation Mandates for 1,4-Dioxane and Ethoxylate Compliance

The global surfactants market is undergoing a non-discretionary reformulation cycle as regulators tighten controls on ethoxylation byproducts, particularly 1,4-dioxane and nonylphenol ethoxylates. Updates to EU REACH Annex XVII, combined with aggressive state-level limits in the United States such as New York’s 1 ppm cap on 1,4-dioxane, have transformed compliance from a labeling issue into a structural demand shift. Major CPG manufacturers are actively redesigning detergent and personal care formulations to eliminate high-risk alcohol ethoxylates and Alkylphenol Ethoxylates, accelerating adoption of Alkyl Polyglucosides and Methyl Ester Sulfonates.

This transition is reinforced by expanded disclosure obligations under the U.S. Toxic Substances Control Act. As of January 2025, TSCA reporting requirements for persistent and byproduct chemicals have forced manufacturers to trace ethoxylation pathways at a molecular level. In response, MES has emerged as a preferred alternative, projected to capture roughly one-third of the bio-derived surfactant segment in 2025 due to its favorable biodegradation profile and cost parity in heavy-duty laundry applications.

Procurement behavior is further influenced by the rapid expansion of the U.S. EPA Safer Chemical Ingredients List. With nearly 1,000 approved substances following the July 2025 update, Safer Choice alignment has become a prerequisite for public sector and institutional cleaning contracts. Surfactants capable of achieving rapid mineralization within 28 days are now structurally advantaged, embedding regulatory performance directly into commercial competitiveness.

World-Scale Fermentation Accelerating the Biosurfactant Transition

A second defining trend is the industrialization of biosurfactants, marking a shift from pilot experimentation to world-scale fermentation assets. Glycolipids such as rhamnolipids and sophorolipids are no longer positioned as niche eco-alternatives but as core functional surfactants with scalable economics. This inflection is underpinned by strategic investments and partnerships designed to de-risk supply and secure consistent quality for global brands.

In May 2024, Evonik commissioned the world’s first industrial-scale rhamnolipid plant in Slovakia, enabling commercial volumes of its Rewoferm® platform. By 2025, these materials are being supplied to multinational CPG companies seeking measurable Scope 3 emission reductions. Evonik’s longer-term strategy targets €1.5 billion in incremental revenue from such next-generation solutions by 2032, underscoring the commercial scale now associated with biosurfactants.

Parallel partnership models are also reshaping the market. In June 2025, AmphiStar and Kensing announced a collaboration to commercialize a portfolio of more than 80 designer microbial biosurfactants in North America, while the Sasol–Holiferm alliance expanded rhamnolipid and MEL pilots in the UK. These initiatives directly address demand for palm-free, bio-based surfactants, particularly in regions where deforestation and ESG scrutiny are influencing ingredient sourcing decisions.

Low-Foam, High-Temperature Stable Surfactants for Automated CIP Systems

One of the most attractive near-term opportunities lies in surfactants engineered for automated Clean-in-Place operations across dairy, beverage, and pharmaceutical manufacturing. Modern CIP systems operate under extreme conditions, with temperatures reaching 80°C to 90°C and highly alkaline or acidic environments. Under these parameters, uncontrolled foam formation is not merely inefficient but operationally hazardous, leading to pump cavitation, sensor malfunction, and cross-contamination risks.

To address this, formulators are increasingly specifying cloud-point-engineered non-ionic surfactants that actively defoam above defined temperature thresholds. By 2025, leading CIP formulations are delivering 20% to 30% reductions in water consumption through rapid rinse-off behavior and high electrolyte tolerance, supporting both cost reduction and sustainability objectives.

Advanced industrial markets such as Japan and South Korea are moving further by adopting silicone-synergized surfactant systems designed to suppress micro-foam under high shear. These solutions are increasingly sold through performance-linked, data-driven contracts, where chemical suppliers guarantee measurable uptime improvements and reduced downtime, effectively repositioning surfactants as productivity enablers rather than commodity inputs.

Polymeric Surfactants Enabling High-Solids, Waterborne Coatings

The global shift toward waterborne and high-solids coatings to meet VOC reduction targets has created a structural opportunity for advanced polymeric surfactants. Unlike conventional low-molecular-weight surfactants, these systems must stabilize pigments and ensure substrate wetting while remaining immobilized within the cured film to preserve water resistance and durability.

Insights presented at the European Coatings Show 2025 highlighted the superior performance of polymerizable, or reactive, surfactants. By chemically integrating into the polymer backbone, these surfactants prevent post-cure migration and eliminate the formation of hydrophilic domains that cause water whitening and gloss loss. This performance advantage is particularly critical in architectural and industrial clearcoats exposed to long-term weathering.

In response, additive suppliers such as Nouryon and Clariant have accelerated launches of high-efficiency polymeric stabilizers and rheology modifiers. Products introduced in early 2025, including advanced Bermocoll® grades, enable up to 10% higher formulation efficiency, allowing paint manufacturers to increase solids content while maintaining low VOC levels and improved film integrity. Collectively, these innovations position polymeric surfactants as a foundational technology for the next generation of compliant, high-performance coatings.

Surfactants Market Share and Segmentation Insights

Anionic Surfactants Dominate Global Surfactants Market with High-Volume Detergent Applications

Anionic surfactants accounted for 42.8% of the surfactants market in 2025, supported by their widespread use in laundry detergents, dishwashing liquids, personal care formulations, and industrial cleaning products. Key chemistries such as linear alkylbenzene sulfonates (LAS), alcohol ether sulfates (AES), and alkyl sulfates deliver strong detergency, foaming, and cost efficiency, making them the backbone of high-volume surfactant demand. Their scalability and compatibility with diverse formulations ensure continued dominance across consumer and industrial markets. The 2025 industry shift focuses on concentrated detergent formats and sustainable surfactant production, where high-active formulations and bio-based feedstocks are increasingly adopted to meet performance and environmental requirements.

Home Care Segment Drives Surfactant Consumption with Global Detergent Demand Growth

Home care accounted for 38.6% of surfactants market demand in 2025, making it the largest application segment due to the global consumption of laundry detergents, surface cleaners, and dishwashing products. Surfactants are essential for soil removal, grease cutting, and cleaning performance, supporting daily use across households worldwide. The scale of consumer demand ensures consistent, high-volume surfactant consumption. The 2025 trend emphasizes the cold water cleaning shift, where surfactant systems are optimized for performance at lower temperatures, enabling energy-efficient washing while maintaining cleaning efficacy, with tailored blends of anionic and non-ionic surfactants enhancing solubility and stain removal in modern detergent formulations.

Surfactants Market Competitive Landscape

The Surfactants market in 2026 is defined by formula agility, with leaders prioritizing low-carbon concentrated surfactants, biodegradable chemistries, and multifunctional mildness enhancers. Strategic investments in on-pipe ethoxylation and ISCC PLUS mass-balance certification are enabling Scope 3 transparency and high-performance formulations across home and personal care applications.

BASF Expands APG Capacity Globally to Strengthen Bio-Based Surfactant Leadership

BASF continues to dominate bio-based surfactants through its integrated Verbund model and global Alkyl Polyglucosides (APG) expansion strategy. The November 2025 capacity expansion in Thailand and the upcoming Cincinnati APG facility in 2026 significantly enhance regional supply capabilities. Under its “Winning Ways” framework, BASF has optimized its Performance Chemicals structure to support next-generation surfactant intermediates. The Care Chemicals division maintained strong profitability, contributing to €6.6 billion EBITDA in 2025. Automation initiatives at Ludwigshafen are improving operational efficiency and cost control. BASF’s integrated bio-refining network enables flexible sourcing of renewable feedstocks for personal care and industrial surfactant markets.

Syensqo Accelerates Circular Surfactant Innovation with ISCC PLUS Certified Production

Syensqo is emerging as a leader in circular surfactants, focusing on deep decarbonization and bio-circular raw materials. The launch of Rhodasurf® B7 UP in February 2026 marks a major advancement, offering a 90% reduction in carbon footprint using upcycled ethylene oxide. Its Moerdijk facility’s ISCC PLUS certification enables seamless integration of sustainable surfactants into existing detergent formulations. The company reported €1.21 billion EBITDA in 2025, supported by stable Consumer Care performance. Its UP Circular Solutions portfolio is aligned with Ecocert and Ecolabel standards demanded by global FMCG brands. This positions Syensqo as a key supplier of drop-in, low-carbon surfactant alternatives.

Stepan Optimizes Production Footprint with High-Capacity Alkoxylation and Project Catalyst

Stepan is transforming its surfactant business through Project Catalyst, focusing on structural optimization and high-efficiency production. The closure of its Fieldsboro plant and consolidation into the Pasadena facility enhances capacity utilization with a 75,000 tonne-per-year alkoxylation unit. The company reported strong growth in agricultural and oilfield surfactants, offsetting weaker household detergent demand. Planned restructuring investments of $70–$80 million in 2026 aim to improve long-term margins. Stepan’s flexible ethoxylation and propoxylation capabilities allow rapid adaptation across industrial and consumer applications. This operational agility strengthens its positioning in high-performance surfactant segments.

Clariant Integrates Active Ingredients with Surfactants to Drive Margin Expansion

Clariant is advancing its surfactant portfolio through performance improvement programs and formulation-level integration. The company achieved a 17.8% EBITDA margin in 2025, supported by cost savings and operational efficiencies. Integration of Lucas Meyer Cosmetics enables bundling of surfactants with high-value cosmetic actives, creating differentiated “full-formulation” solutions. Its CLARITY™ platform is expanding into predictive surfactant performance monitoring across industrial applications. The company is targeting a 19–21% EBITDA margin by 2027 through bio-based and high-performance surfactant innovation. This strategy positions Clariant strongly in premium personal care and specialty chemical markets.

Indorama Ventures Strengthens Integrated Surfactant Platform with Biodegradable Portfolio Expansion

Indorama Ventures is scaling its Indovinya division under the IVL 2.0 and SOAR strategies, focusing on sustainable and integrated surfactant production. The company aims to double EBITDA by 2028, with surfactants as a key growth driver. Its portfolio now includes 80% biodegradable products, highlighted by innovations such as SURFONIC® H-1000, a green hydrotrope replacing conventional chemicals. Leveraging its integrated ethylene oxide value chain, IVL maintains cost leadership amid feedstock volatility. Its extensive manufacturing footprint across Asia and the Americas supports localized supply for emerging markets. This integration enhances competitiveness in personal care, home care, and industrial surfactant applications.

Thailand Surfactants Market Positioned as Southeast Asia’s Bio-Based Production Anchor

Thailand has consolidated its position as a strategic surfactants manufacturing hub in Southeast Asia, underpinned by capacity expansion in natural and bio-based chemistries. In November 2025, BASF inaugurated a major expansion of Alkyl Polyglucosides production at its Bangpakong site, reinforcing Thailand’s role as a regional supply node for 100% bio-based surfactants used across personal care and home care applications. This investment aligns closely with Thailand’s Biocircular-Green economy framework, which actively incentivizes the use of locally available sugarcane and cassava feedstocks. The result is a structurally lower-cost, renewable raw material base that reduces exposure to imported petrochemical volatility while supporting biodegradable surfactant synthesis.

From a supply chain perspective, the Bangpakong expansion reflects a deliberate localized-for-local manufacturing strategy. By shortening lead times by an estimated 30 to 40%, Thai producers have insulated regional customers from the logistics disruptions experienced in late 2024. Regulatory and sustainability alignment further strengthens export competitiveness. As of early 2026, Thailand recorded a 25% increase in domestic surfactant facilities achieving RSPO Mass Balance certification, a critical requirement for access to European buyers. Beyond consumer formulations, Thai producers are also pivoting toward agricultural adjuvant surfactants, supporting the country’s push toward precision farming and higher-value agrochemical inputs.

United States Surfactants Market Driven by Circular Carbon and Semiconductor Purity

The United States surfactants industry is evolving along two parallel axes: circular carbon integration and high-purity specialty formulations. Capacity expansion in conventional anionic surfactants continues, exemplified by Pilot Chemical’s Middletown, Ohio investment to more than double Alpha Olefin Sulfonate output. This expansion responds to resilient domestic demand from detergents and institutional cleaning while reinforcing supply security for North American formulators. At the same time, the U.S. market is increasingly defined by next-generation feedstock innovation. Dow, in collaboration with LanzaTech, scaled production of the EcoSense 2470 surfactant in 2025, utilizing recycled carbon emissions as a primary feedstock and signaling a structural shift toward circular carbon economics in detergents.

Policy alignment has accelerated bio-based innovation. Updates to the USDA BioPreferred Program in late 2025 raised mandatory bio-content thresholds for federal procurement, catalyzing R&D in fermentation-derived biosurfactants such as rhamnolipids. In parallel, the CHIPS Act has reshaped demand profiles by driving the expansion of ultra-low-metal surfactants required for semiconductor wafer cleaning. These electronic-grade surfactants demand contamination control well beyond conventional specifications, creating a high-margin niche. Sustainability differentiation extends into silicone-based surfactants as well, with low-carbon silicone elastomer blends entering the clean beauty pipeline ahead of the 2026 product cycle.

European Union Surfactants Market Reshaped by Biosurfactants and Digital Compliance

Within the European Union, regulatory reform has become the dominant market-shaping force. A landmark development is the industrial-scale biosurfactant platform in Slovakia, where Evonik brought the world’s first large-scale rhamnolipid plant to full capacity by early 2026. This palm-free, fermentation-derived output is increasingly favored by global FMCG brands seeking to future-proof formulations against tightening biodegradability and deforestation criteria. Germany remains the strategic backbone of European surfactants, with sustained capital commitments to modernize care chemical and surfactant assets at the Ludwigshafen site.

Regulatory certainty has been reinforced through the New EU Detergents and Surfactants Regulation approved in December 2025. The introduction of a Digital Product Passport and stricter ultimate biodegradability standards will materially alter formulation economics over the 3.5-year transition period. Additional mandates supporting refill and bulk-dispensing models require enhanced formulation stability under variable storage conditions, pushing R&D toward more robust non-ionic systems. The reaffirmed prohibition on animal testing has further accelerated investment in in-silico and in-vitro safety modeling, raising the technical entry barrier for smaller producers and favoring well-capitalized incumbents.

India Surfactants Market Accelerated by Policy Protection and Export Substitution

India’s surfactants industry is entering a structurally accelerated phase, driven by coordinated industrial policy and rising export relevance. By March 2025, realized investments under the Production Linked Incentive framework reached ₹1.76 lakh crore, enabling domestic production of higher-value specialty surfactants for pharmaceutical, electronics, and institutional cleaning applications. Budget 2025–26 allocations to the Ministry of Chemicals and Fertilizers further prioritized the expansion of Petroleum, Chemicals and Petrochemicals Investment Regions in Odisha and Gujarat, creating scale-ready infrastructure for downstream surfactant manufacturing.

Regulatory tightening has also played a protective role. The implementation of enhanced Quality Control Orders by the Bureau of Indian Standards in February 2025 curtailed the inflow of sub-standard imported surfactants, improving price realization for compliant domestic producers. Export momentum underscores this shift, with organic chemical exports reaching $2.75 billion in the first four months of FY26. Looking ahead, bio-surfactant innovation is gaining institutional backing, as the Department of Biotechnology’s 2026 Waste-to-Surfactant pilot program channels agricultural residues such as rice husk and bagasse into low-cost biosurfactant pathways, reinforcing India’s position as a credible alternative supply base to China.

Comparative Snapshot: Surfactants Industry by Country

Surfactants Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Policy or Regulatory Lever

|

Structural Advantage

|

|

Thailand

|

APGs and agro-adjuvant surfactants

|

BCG economy incentives, RSPO compliance

|

Renewable feedstock base and regional logistics resilience

|

|

United States

|

Circular carbon and electronic-grade surfactants

|

BioPreferred Program, CHIPS Act

|

High-margin purity niches and carbon capture integration

|

|

European Union

|

Biosurfactants and digital traceability

|

Detergents Regulation 2025, DPP

|

Regulatory-led premiumization and sustainability compliance

|

|

India

|

Specialty and bio-surfactant substitution

|

PLI scheme, QCO enforcement

|

Export growth with cost-competitive manufacturing

|

Surfactants Market Report Scope

Surfactants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$85 Billion

|

|

Market Size (2034)

|

$133 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Type (Anionic Surfactants, Non-Ionic Surfactants, Cationic Surfactants, Amphoteric and Zwitterionic Surfactants, Biosurfactants), By Origin (Synthetic Surfactants, Bio-Based Surfactants), By Application (Home Care, Personal Care, Industrial and Institutional Cleaning, Agrochemicals, Oil and Gas, Textiles and Leather)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Evonik Industries AG, Stepan Company, Clariant AG, Nouryon, Kao Corporation, Croda International Plc, Solvay SA, Huntsman Corporation, Pilot Chemical Company, Indorama Ventures, Godrej Industries Limited, Sasol Limited, Galaxy Surfactants Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Surfactants Market Segmentation

By Type

- Anionic Surfactants

- Non-Ionic Surfactants

- Cationic Surfactants

- Amphoteric and Zwitterionic Surfactants

- Biosurfactants

By Origin

- Synthetic Surfactants

- Bio-Based Surfactants

By Application

- Home Care

- Personal Care

- Industrial and Institutional Cleaning

- Agrochemicals

- Oil and Gas

- Textiles and Leather

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Surfactants Industry

- BASF SE

- Dow Inc.

- Evonik Industries AG

- Stepan Company

- Clariant AG

- Nouryon

- Kao Corporation

- Croda International Plc

- Solvay SA

- Huntsman Corporation

- Pilot Chemical Company

- Indorama Ventures

- Godrej Industries Limited

- Sasol Limited

- Galaxy Surfactants Limited

*- List not Exhaustive