Market Overview: Amphoteric Surfactants Market to Reach $22.2 Billion by 2034 as Sulfate-Free Formulations, Bio-Based Inputs, and Circular Chemistry Drive Growth

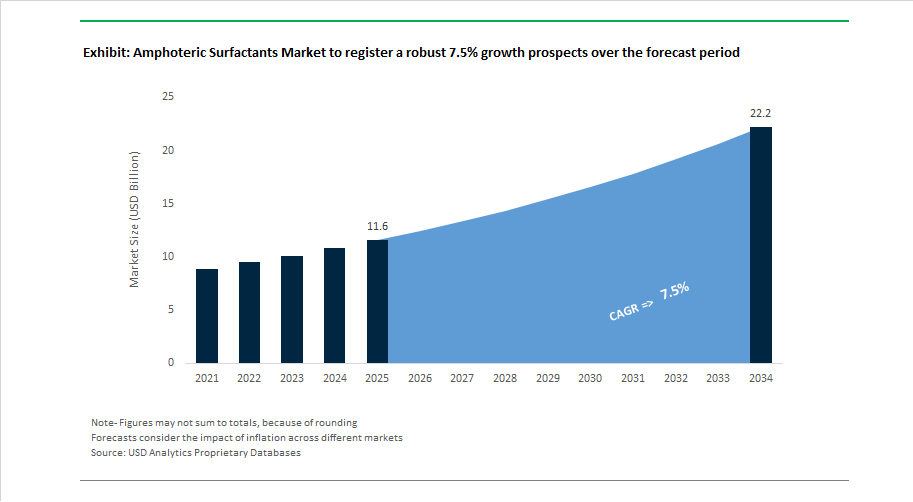

The global amphoteric surfactants market is projected to grow from $11.6 billion in 2025 to $22.2 billion by 2034, registering a 7.5% CAGR driven by rising demand for mild, pH-adaptive, and biodegradable surfactant systems across personal care, home care, and institutional cleaning. Amphoteric surfactants such as cocamidopropyl betaine, amine oxides, and imidazolines are valued for their low irritation profile, foam stabilization, and compatibility with sulfate-free formulations. Market growth is supported by consumer preference for clean label shampoos, sensitive skin cleansers, baby care products, and eco-labeled detergents, alongside regulatory pressure to reduce aquatic toxicity. Industry development is linked to green chemistry initiatives, bio-based feedstock integration, and carbon-reduced manufacturing processes.

Innovation in mild surfactant systems began advancing in April 2024 when Nouryon launched Structure M3, a biodegradable co-surfactant enhancing amphoteric-based cleansing systems. Feedstock strengthening followed in August 2024 as BASF expanded alkyl polyglycoside capacity, supporting bio-based intermediates used in amphoteric blends. Circular chemistry initiatives advanced in October 2024 through a collaboration between Dow and LanzaTech to develop carbon-derived surfactants. Sustainability credentials strengthened in January 2025 when Galaxy Surfactants achieved ISCC PLUS certification. Product performance innovations continued in April 2025 as Nouryon introduced Armocare Aqua 12 for conditioning and mild cleansing. Market consolidation expanded in May 2025 with Solenis completing integration of Diversey and NCH assets for institutional cleaning solutions.

Sustainability investments accelerated in August 2025 as BASF launched green chemistry programs targeting carbon reduction in betaine and amine oxide production. Regional innovation hubs expanded in November 2025 with Nouryon’s Shanghai Innovation Center focusing on sulfate-free surfactant systems, followed by a Brazilian innovation center opening in December 2025 to serve South American formulators. Raw material developments connected to ammonia-based amine synthesis were reinforced in January 2026 as Topsoe validated ammonia cracking technologies that support amine supply chains. In February 2026, Nouryon introduced a fully bio-based CMC polymer designed to work synergistically with amphoteric surfactants in biodegradable detergents.

Trends and Opportunities Transforming the Amphoteric Surfactants Market

Reformulation Acceleration for CAPB Driven by Purity, Regulatory, and Allergy Controls

Reformulation is now a commercial necessity for amphoteric surfactants, particularly Cocamidopropyl Betaine (CAPB), as dermatological and regulatory bodies highlight allergen risks arising from its synthesis impurities. A 2025 dermatology review confirmed that the main sensitizers in CAPB products are Dimethylaminopropylamine (DMAPA) and amidoamine, impurities that in commercial-grade surfactants can reach up to 3%. The market is shifting toward Ultra-High-Purity (UHP) CAPB engineered to meet sub-ppm impurity levels for baby care and facial-use applications. The FDA FY 2025 OTC Monograph Order enforces new listing updates for drug-listed cleanser categories, triggering higher demand for USP-grade amphoterics with <0.01% total impurities. In parallel, the U.S. EPA’s 2024 exemption for CAPB residue limits in agricultural uses (Reg. No. 2024-10182) reflects a dual-tiered structure: strict purity for consumer-facing products and relaxed regulatory conditions for industrial/agri surfactants, shaping supply prioritization and price segmentation.

Rise of “Primary Amphoteric” Systems Replaces Boosting-Only Role

The market is transitioning away from amphoterics being used as secondary foam boosters toward “Primary Amphoteric Surfactant Systems”, engineered from proprietary blends of betaines, amphoacetates, and sultaines. Technical evaluations from 2025 briefings indicate that pairing amphoacetates with non-ionics such as APGs reduces skin irritation scores by 30% against SLES-based baselines while delivering viscosity and foam structure comparable to sulfate systems. The August 2024 commercial launch of Galaxy Surfactants’ zwitterionic cleansing base—designed to support microbiome-friendly claims—demonstrates a performance-oriented pivot where amphoterics allow brands to achieve tear-free, pH-balanced cleansing without thickening polymers. This shift is highly consumer-driven, supported by 2025 witnessing 70% of global consumers view sulfate-free credentials as a hygiene and wellness benchmark.

Pharmaceutical Ionizable Amphoteric Lipids as Critical Components of LNP Delivery

Amphoteric derivatives are gaining relevance in drug-delivery pipelines as ionizable lipids, where they function as pH-switchable carriers within Lipid Nanoparticles (LNPs). Their charge-neutral behavior at physiological pH minimizes cytotoxicity, while internal protonation inside endosomes enables mRNA cargo release. A 2025 industry dossier specifies that ionizable lipids typically make up ~50% of an LNP composition, placing amphoterics at the economic core of vaccine-grade lipid systems. The $220 million Evonik pharmaceutical lipid facility in Lafayette, Indiana (coming online in 2025), backed by $150 million federal BARDA support, validates the scaling trajectory. Structural shifts such as Evonik’s divestment of legacy keto-acid lines at Ham and Wuming also demonstrate a move toward high-margin amphoteric lipid excipients for oncology, cancer immunotherapy, and protein-replacement therapies.

Low-VOC Amphoterics for Industrial & Institutional Cleaning and Oilfield Systems

The Industrial and Institutional (I&I) sector is increasingly a performance-led commercialization avenue. As of late 2024, updated U.S. and EU facility permits require Near-Zero VOC cleaning chemistries, which elevates demand for amphoterics such as amine oxides and amphoacetates that maintain stability in acidic to highly alkaline ranges (pH 2–12). Technical formulation data from 2024-2025 reveals that ~30% of new I&I cleaning SKUs are leveraging amphoteric-anionic blends to prevent precipitation in hard-water and saline environments, enabling ultra-high dilution concentrates for food-grade and industrial Clean-in-Place (CIP) cleaning frameworks. Beyond cleaning, amphoterics are gaining traction in enhanced oil-recovery (EOR) applications, where their pH-adaptive surface activity supports interfacial tension reduction without relying on PFAS-based foams—an attribute that aligns with oilfield decarbonization and ESG disclosure requirements.

Amphoteric Surfactants Market Share and Segmentation Insights

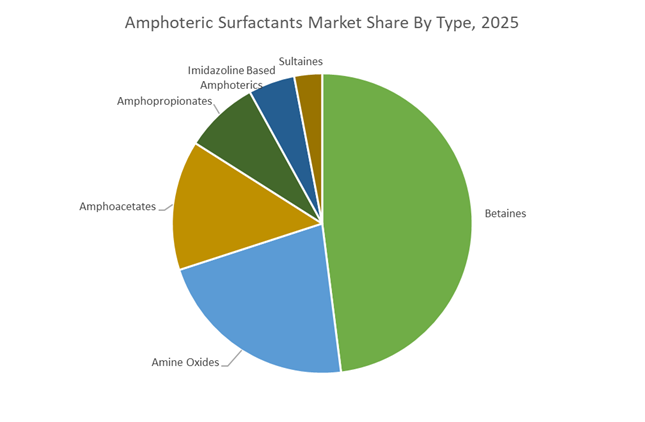

Market Share by Type: Betaines Lead Volume While Sultaines Deliver Premium Expansion

Betaines account for approximately 48% of the global amphoteric surfactants market in 2025, led by cocamidopropyl betaine (CAPB), the industry-standard co-surfactant for viscosity building, foam stabilization, and mildness enhancement in shampoos and liquid soaps. Despite periodic impurity scrutiny related to amidoamine and 3-DMA, CAPB remains unmatched in cost-performance. Coco-betaine variants are gaining traction in premium purity formulations. Amine oxides rank second and are expanding at +7.8% YoY, supported by strong grease-cutting performance and hypochlorite compatibility in household and institutional cleaners. Amphoacetates and amphopropionates serve high-mildness and alkaline-stable niches respectively, with steady demand in baby care and industrial systems. Imidazoline-based amphoterics are mature and declining. Sultaines are the fastest-growing segment, driven by superior mildness and high-electrolyte stability in sulfate-free, natural-certified personal care formulations where premium pricing is justified.

Market Share by Application: Personal Care Dominates While PFAS-Free Foams Create High-Growth Niche

Personal care and cosmetics represent roughly 52% of amphoteric surfactant consumption in 2025, anchored by shampoos, body washes, facial cleansers, and baby products. The global shift toward sulfate-free systems remains the primary growth catalyst, with amphoterics delivering foam, viscosity, and irritation reduction in SLS/SLES-free formulations. Home care ranks second, dominated by amine oxides in dishwashing liquids and hard surface cleaners. Industrial and institutional cleaning remains volume-driven, leveraging amphoteric stability in caustic and acid environments. Oilfield chemicals represent a cyclical, high-value niche tied to enhanced oil recovery and drilling fluids. Agrochemicals show steady 5 to 6% growth as wetting agents and compatibility adjuvants. Firefighting foams form the smallest but most transformative segment, as regulatory phase-outs of fluorinated surfactants accelerate adoption of PFAS-free fluorine-free foam systems, driving double-digit growth from a low base.

Amphoteric Surfactants Market Competitive Landscape

The global amphoteric surfactants market is shaped by sustainability-driven reformulation, rapid growth in sulfate-free personal care, and rising demand from Industrial & Institutional (I&I) cleaning, baby care, and agrochemical applications. Leading manufacturers are competing on bio-based feedstocks, carbon transparency, cold-process manufacturing, and sensory performance. Capacity expansions across Asia-Pacific and North America, combined with digital formulation tools and backward oleochemical integration, are redefining supply chains. Market leadership increasingly depends on mildness profiles, pH stability, and multifunctional blends that reduce water usage and energy consumption while meeting clean-label and regulatory compliance requirements for global FMCG, cosmetics, and hygiene brands.

Bio-based scale leadership positions BASF SE at the forefront of amphoteric innovation

BASF leads the amphoteric surfactants market through its Verbund infrastructure and aggressive expansion of bio-based capacity. In late 2025, BASF inaugurated a major surfactant expansion in Bangpakong, Thailand, strengthening its footprint in the high-growth APAC personal care market. The launch of Lamesoft® OP Plus in early 2026 introduced a biodegradable opacifier alternative to synthetic acrylates for sulfate-free systems. A new APG and amphoteric blends line in Cincinnati comes online mid-2026, targeting North America’s clean-label trend. BASF further differentiates through its Surfactant Navigator digital tool, enabling rapid simulation of skin-lipid interactions and accelerating product development for premium beauty brands.

High-purity betaines anchor Evonik Industries AG’s specialty surfactant strategy

Evonik has repositioned its Care Solutions portfolio toward biotechnology and custom-engineered amphoteric surfactants under its Tailor Made efficiency program. Its TEGO® Betain series remains a benchmark for ultra-low residual by-products, supporting non-irritating formulations for baby care and medical-grade hygiene. In 2025, Evonik expanded specialty amine derivatives capacity to serve sultaines for high-salinity oilfield applications. Early 2026 marked a strategic pivot toward Superforce green chemistry projects, backed by a new dividend and investment policy. Evonik’s competitive edge lies in high-purity production, specialty customization, and circularity-focused R&D that targets high-margin applications across healthcare, energy, and sensitive skin care.

Amphoacetate leadership defines Syensqo in ultra-mild formulations

Following its separation from Solvay, Syensqo operates as a pure-play science company with strong positioning in amphoacetates through its Miranol® platform. These surfactants are widely regarded as among the mildest available, making them essential for tear-free pediatric and ocular products. In 2025, Syensqo launched AgRHEA LifeXtend Plus, extending amphoteric technology into agricultural adjuvants to improve bio-pesticide rain-fastness. Its Value Chain Resilience strategy introduced localized sourcing to mitigate tariff volatility. Deep integration into guar and natural polymer chains enables Syensqo to offer fully plant-based cleansing and conditioning systems, supporting clean beauty and sustainable home care markets.

Purpose-driven design strengthens Clariant AG’s global amphoteric portfolio

Clariant’s amphoteric strategy centers on Purposeful Design, focusing on reduced rinse-off water consumption and high sensory performance. The GlucoTain® and GlucoPure® ranges scaled in 2025, leveraging sugar and amino acid chemistry to replicate creamy and voluminous foam without synthetic additives. Clariant dominates I&I cleaning with amphoteric surfactants stable across extreme pH conditions, from acidic to highly alkaline systems. Expansion of its Cangzhou site in late 2025 localized production for Asian textile and personal care markets. As a Renewable Carbon Initiative member, Clariant now delivers batch-level CO2-equivalent data, aligning its portfolio with global CPG sustainability mandates.

Rheology-driven differentiation powers Lubrizol Corporation’s premium blends

Lubrizol specializes in sensory science, combining amphoteric surfactants with advanced polymers to engineer differentiated textures. Its Chembetaine™ and Schercoteric™ brands, particularly Schercoteric™ MS-2 50, are widely adopted in premium shampoos for superior wet-comb performance. After divesting commodity assets in 2024–2025, Lubrizol consolidated high-value surfactant production in Texas and Europe. The company excels in synergistic formulations, blending amphoterics with Carbopol® polymers to create clear, suspended-particle body washes. In 2025, Lubrizol introduced cold-processable amphoteric blends, enabling manufacturers to bypass heating steps and reduce energy consumption by up to 25%.

Value-added green chemistry accelerates growth for Galaxy Surfactants Ltd.

Galaxy Surfactants has emerged as a global force by targeting value-added green solutions for mass and mass-prestige markets. Its Galsoft® range supports mild cleansing, while the Galseer® Tresscon solid shampoo base scaled in 2025 to meet rising demand for waterless beauty formats. Galaxy focuses on enabling sulfate-free transitions in emerging economies across India, Africa, and Southeast Asia. Strong backward integration into oleochemicals stabilizes Cocamidopropyl Betaine supply amid palm oil volatility. In 2025, Galaxy achieved Water Positive status at major Indian facilities, strengthening partnerships with sustainability-focused FMCG leaders and reinforcing its role in affordable, eco-conscious amphoteric surfactants.

China Amphoteric Surfactants Market: Scale Leadership Meets Clean Beauty and Export Momentum

China remains the most influential production and consumption hub for amphoteric surfactants, combining large-scale capacity with rapid innovation cycles. In November 2025, Clariant commissioned expanded facilities at its Daya Bay site following an CHF 80 million investment. The upgraded multi-purpose plant is dedicated to mild surfactants, directly addressing domestic demand from the fast-growing clean beauty and sulfate-free facial cleanser segments.

Local champions such as Tinci Materials and Sino Lion have pivoted toward amino acid-based amphoterics since late 2024, targeting premium skincare formulations. China also remains the largest consumer of amine oxides, driven by industrial detergents and household cleaning. Policy support is reinforcing sustainability, with the Shanghai Green Chemical Innovation Hub offering incentives for PFAS-free firefighting foams using amphoteric blends, while Yangtze River Delta mandates pushed major producers to adopt closed-loop water systems, cutting effluent volumes by 22%. Export competitiveness strengthened further in 2025 as cocamidopropyl betaine shipments to Southeast Asia rose under the RCEP framework.

Slovakia Amphoteric Surfactants Market: Biosurfactant Commercialization Redefines Mildness Standards

Slovakia has emerged as a strategic innovation node for next-generation amphoteric-compatible biosurfactants. In May 2024, Evonik inaugurated the world’s first industrial-scale rhamnolipid biosurfactant plant in Slovenská Ľupča. This facility, representing a triple-digit million-euro investment, produces fermentation-derived glycolipids designed to work synergistically with conventional amphoterics.

The plant’s reliance on renewable corn feedstocks and biocircular processes establishes a new global benchmark for sustainable surfactant manufacturing. By early 2025, the site became the primary launch platform for Evonik’s REWOFERM® series, which is now being integrated into premium global personal care brands seeking ultra-mild, low-irritation cleansing systems.

India Amphoteric Surfactants Market: Policy-Led Scale-Up of Green Amphoterics

India’s amphoteric surfactants industry is benefiting from strong regulatory tailwinds and domestic demand growth. The BioE3 Policy, operationalized in late 2024, has provided a clear framework for scaling bio-based chemicals, enabling companies such as Galaxy Surfactants to expand amphoteric production aligned with sustainability goals. In 2025, Galaxy reported a marked increase in its green surfactant portfolio, driven by shampoos, baby-care products, and mild cleansing formulations.

Infrastructure incentives have accelerated this momentum. A 20% Capex subsidy introduced by the Ministry of Chemicals in 2025 supported new green chemistry units, particularly sulfobetaine expansion in the Gujarat corridor. At the same time, stricter import purity norms enforced by the Directorate General of Foreign Trade in early 2025 encouraged domestic synthesis of high-grade amphoteric technicals, strengthening India’s position as a regional supply base.

United States Amphoteric Surfactants Market: Regulatory Purity and Pet Care Drive Premium Demand

In the United States, amphoteric surfactant demand is being reshaped by regulatory scrutiny and diversification into pet care. In March 2025, Evonik entered an exclusive distribution agreement with Sea-Land Chemical Company to scale its mild cleaning solutions across the U.S. market.

The Kansas Animal Health Corridor emerged as a notable demand center in 2025, as pet grooming brands increasingly adopted amphopropionates for tearless and hypoallergenic formulations. Regulatory drivers are equally important. Proposed FDA labeling requirements targeting 1,4-dioxane-free certifications in rinse-off products have boosted demand for high-purity betaines. On the supply side, Stepan Company completed modernization at its Pasadena, Texas facility in late 2024, integrating advanced alkoxylation technologies to deliver low-VOC amphoteric surfactants.

Germany Amphoteric Surfactants Market: Responsible Sourcing and Natural-Based Innovation

Germany is setting benchmarks for sustainability and traceability in amphoteric surfactants. In 2025, BASF launched its Longevity Ecosystem at in-cosmetics Global, highlighting natural-based amphoterics such as Lamesoft® OP Plus, a wax-based opacifier developed to replace synthetic acrylates in mild cleansing systems.

Regulatory pressure from the Supply Chain Due Diligence Act has forced a rapid shift toward RSPO-certified palm and coconut oil feedstocks across German amphoteric production. Innovation is further supported by industry recognition, with Evonik receiving the 2024 European Responsible Care® Award for its glycolipid technology, now increasingly blended with conventional amphoterics to create ultra-mild, bio-based personal care products.

Japan Amphoteric Surfactants Market: Precision Manufacturing for Aging and Premium Skincare

Japan’s amphoteric surfactants industry reflects its focus on precision, automation, and demographic-driven innovation. In 2025, Ajinomoto and Kao Corporation completed automation upgrades of their specialty surfactant lines, concentrating on glycinate-amphoteric blends tailored for premium skincare.

An aging population has become a key innovation driver. Japanese formulators launched geriatric skincare cleansers in 2025 that rely on high-bioavailability amphoterics to preserve skin barrier integrity, reinforcing Japan’s leadership in high-performance, skin-compatible cleansing technologies.

Country-Level Strategic Positioning in Amphoteric Surfactants

Amphoteric Surfactants Market County Level Snapshot

|

Country

|

Strategic Focus

|

Industry Implication

|

|

China

|

Scale expansion and clean beauty alignment

|

Dominant producer with growing exports and sustainability compliance

|

|

Slovakia

|

Industrial biosurfactant commercialization

|

Global benchmark for bio-based, ultra-mild amphoterics

|

|

India

|

Policy-driven green chemistry scale-up

|

Rising regional supplier of bio-based amphoterics

|

|

United States

|

Regulatory purity and pet care demand

|

Strong pull for high-purity, low-contaminant surfactants

|

|

Germany

|

Responsible sourcing and natural innovation

|

Leadership in traceable, eco-certified amphoterics

|

|

Japan

|

Automation and age-specific skincare

|

Precision-driven premium amphoteric formulations

|

Amphoteric Surfactants Market Report Scope

Amphoteric Surfactants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.6 Billion

|

|

Market Size (2034)

|

$22.2 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Type (Betaines, Amine Oxides, Amphoacetates, Amphopropionates, Sultaines, Imidazoline Based Amphoterics), By Form (Liquid, Powder, Granular and Paste), By Source (Natural Based, Synthetic Based, Bio Fermented), By Application (Personal Care and Cosmetics, Home Care, Industrial and Institutional Cleaning, Oilfield Chemicals, Agrochemicals, Firefighting Foams)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Evonik Industries AG, Clariant AG, Ajinomoto, Stepan Company, Kao Corporation, Galaxy Surfactants Limited, Nouryon, Croda International Plc, Solvay SA, Innospec Inc, Lubrizol Corporation, Sino Lion, Tinci Materials Technology, Enaspol

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Amphoteric Surfactants Market Segmentation

By Type

- Betaines

- Amine Oxides

- Amphoacetates

- Amphopropionates

- Sultaines

- Imidazoline Based Amphoterics

By Form

- Liquid

- Powder

- Granular and Paste

By Source

- Natural Based

- Synthetic Based

- Bio Fermented

By Application

- Personal Care and Cosmetics

- Home Care

- Industrial and Institutional Cleaning

- Oilfield Chemicals

- Agrochemicals

- Firefighting Foams

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Amphoteric Surfactants Industry

- BASF SE

- Evonik Industries AG

- Clariant AG

- Ajinomoto

- Stepan Company

- Kao Corporation

- Galaxy Surfactants Limited

- Nouryon

- Croda International Plc

- Solvay SA

- Innospec Inc

- Lubrizol Corporation

- Sino Lion

- Tinci Materials Technology

- Enaspol

*- List not Exhaustive