Market Overview: Aminoethylethanolamine Market to Reach $406.6 Million by 2034 as Capacity Expansions, High-Purity Grades, and Digitalized Supply Chains Reshape Specialty Amine Demand

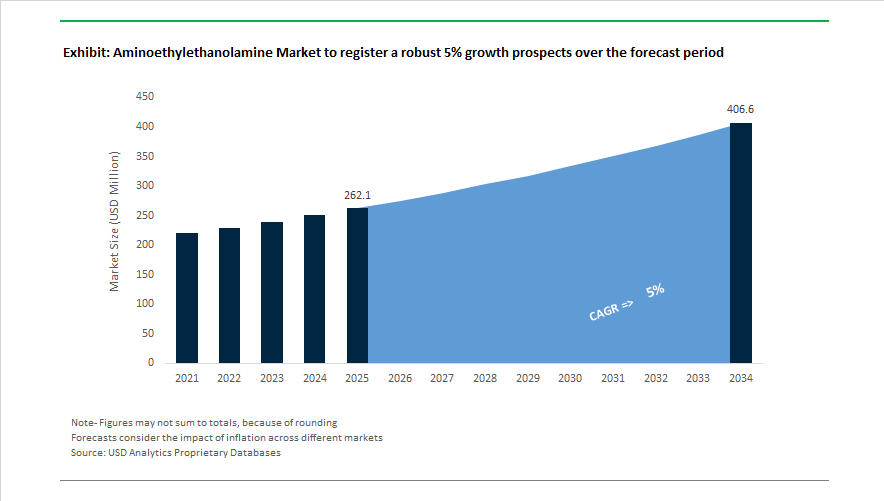

The global aminoethylethanolamine market is projected to grow from $262.1 Million in 2025 to $406.6 Million by 2034, registering a 5% CAGR driven by expanding applications in specialty surfactants, chelating agents, corrosion inhibitors, gas treatment chemicals, personal care intermediates, and medical coatings. Aminoethylethanolamine (AEEA) is a multifunctional amine combining primary and secondary amine groups with hydroxyl functionality, making it critical in oilfield chemicals, textile processing, agrochemical formulations, wood preservation, and cationic surfactant synthesis. Market expansion is closely linked to the growth of high-purity amine demand, regional supply localization, and stricter environmental monitoring standards under global green chemistry initiatives.

Supply-side strengthening began in January 2024 when Nouryon completed the acquisition of ADOB, vertically integrating AEEA-based chelate production for specialty fertilizers. Capacity enhancements followed through 2024 as BASF completed a 50% expansion at its Antwerp Verbund site and finalized the BASF-YPC downstream expansion in Nanjing, reinforcing European and Asian AEEA supply chains. Product purity innovation advanced in 2024 with Tosoh Corporation launching Toa AEEA H-50 and AkzoNobel introducing Berol AEEA 99 for premium personal care applications. Pricing adjustments occurred in September 2024 when Dow implemented North American price increases amid raw material cost pressures. Infrastructure investments expanded in September 2024 as Chemanol secured licensing for new amine capacity supporting Middle Eastern oilfield chemical supply.

Operational modernization accelerated in 2025 with Huntsman advancing its Geismar expansion and major producers implementing Digital Quality Management platforms to provide real-time purity verification. Regulatory monitoring intensified during 2025 when ECHA listed AEEA under enhanced oversight, prompting adoption of closed-loop emission control systems. Production efficiency improved in January 2026 as Dow completed automation upgrades at its Asia-Pacific amines facility, boosting AEEA output and lowering energy intensity. Demand diversification emerged in January 2026 as healthcare reports highlighted rising use of AEEA-derived bio-compatible medical coatings for antimicrobial surgical equipment surfaces.

Strategic Trends and High-Value Opportunities Reshaping the Aminoethylethanolamine Market

Market Regulatory Scrutiny Forces Reformulation Away from AEEA in Consumer-Facing Surfactants

A key trend is the shift away from AEEA-based surfactants in household and personal care formulations due to nitrosamine-risk classifications and evolving toxicology standards. Under EU REACH Annex XVII and the EMA’s tightened nitrosamine thresholds effective December 2025, cosmetic and detergent products must remain below 50 μg/kg nitrosamine content, forcing laundry detergent brands to reformulate ahead of audits. This is accelerating the adoption of ester-quat and plant-based softening systems, particularly among FMCG brands targeting clean-label and allergen-safe categories.

The policy transition is amplified by broader CMR (Carcinogenic, Mutagenic, Reprotoxic) classifications set for enforcement by September 1, 2025, making continued use of amine-heavy intermediates reputationally risky. Corporate strategy data from leading fabric-softener portfolios indicates that over 60% of consumers in 2025 prioritize hypoallergenic laundry care, creating a direct commercial incentive to reduce AEEA exposure in value chains and shift to bio-derived alternatives that support green marketing claims.

Market High-Purity AEEA Becomes a Priority Input for Semiconductors and Pharma

While low-cost industrial-grade AEEA faces substitution risk, ultra-high-purity (UHP) grades (>99.5 percent) are emerging as premium revenue contributors. Recent expansion at BASF Antwerp, which delivered a 50% production capacity boost, reflects a pivot from commodity outputs toward controlled-impurity, moisture-free AEEA designed for API synthesis, advanced lubricants, and semiconductor lithography chemistries. Pharmaceutical procurement shifts now favor “single-origin purity chains” with digital traceability, linking AEEA quality consistency to reduced risk in cardiovascular and anti-infective drug synthesis. In electronics, ppb-level metallic impurity thresholds make AEEA a precision ingredient—particularly in cleaning and lithography support fluids for advanced nodes where equipment downtime is cost-intensive.

This trend is reshaping pricing power. Industrial AEEA remains margin-constrained, while UHP grades command a significant premium, positioning AEEA more competitively in specialized rather than bulk markets. Producers that can demonstrate impurity mapping, blockchain-based traceability, and quality documentation are gaining procurement preference from chip manufacturers and big-pharma intermediates.

High-Value Commercial Opportunities Expanding AEEA Demand

Market Opportunity: AEEA as a Next-Generation Post-Combustion Carbon Capture (PCC) Solvent

The industrial decarbonization ecosystem is expanding rapidly, and AEEA is gaining traction within next-generation Post-Combustion Carbon Capture (PCC) solutions. Comparative testing by IEAGHG and Khalifa University in 2024-2025 identified AEEA as a prime candidate surpassing monoethanolamine (MEA) on regeneration energy efficiency, thermal degradation resistance, and higher molar absorption capacity for CO₂. These improvements directly lower operational costs—a key success factor as CCUS transitions from demonstration sites to full-scale deployment.

With the global CCUS pipeline forecast to reach 430 million tonnes of CO₂ per year by 2030, AEEA demand is expected to surge as cement, steel, and power-plant operators seek amine systems capable of scaling beyond laboratory conditions. Projects in Norway, the UK, Sweden, and China—now reaching FID stage—signal a major procurement horizon for chemical suppliers that can offer consistent AEEA volumes, solvent blends, and long-term supply contracting aligned with decarbonization targets.

Market Opportunity: AEEA-Derived Chelates for Copper CMP in Semiconductor Manufacturing

The parallel growth engine lies in electronics. As semiconductor fabrication complexity increases, AEEA derivatives are emerging as precursors for chelating agents in Copper Chemical Mechanical Planarization (CMP)—a vital process for wafers used in AI compute, 5G, autonomous vehicles, and HPC. Taiwan and South Korea’s leading foundries are moving from 16 to 23 copper interconnect layers, driving the need for higher-precision CMP slurries that enable defect-free polishing without copper loss or micro-scratching.

The global CMP slurry market is projected to reach USD 2.18 billion in 2025, propelled by 3D NAND and Gate-All-Around (GAA) architectures. AEEA-based chemistry enables chemical removal rate control and surface finishing, directly influencing chip yields—which makes AEEA an indirect beneficiary of the exponential semiconductor-capex cycle. Sustainability mandates in chip fabs are also creating space for AEEA-derived biodegradable dispersants, which reduce environmental risk during slurry disposal and align with OEM-led "green wafer" standards.

Aminoethylethanolamine (AEEA) Market Share and Segmentation Insights

Market Share by Application: Fabric Care Leads While Agrochemical Intermediates Accelerate

Fabric care accounts for approximately 31% of global Aminoethylethanolamine (AEEA) demand in 2025, making it the largest application segment. AEEA is a critical intermediate in aminopolycarboxylate chelating agents such as EDTA and DTPA analogs used in phosphate-free laundry detergents, bleach stabilizers, and industrial fabric washing formulations. Structural substitution away from phosphates has permanently increased chelant consumption, sustaining steady 4 to 5% annual growth tied to population and laundry volumes. Textile additives rank second, where AEEA functions as a dyeing auxiliary, fiber modification intermediate, and antistatic precursor, with demand linked to Asian textile manufacturing output. Agrochemicals represent the fastest-growing application, as AEEA enables formation of water-soluble amine salts in glyphosate, 2,4-D, and other herbicides. Paints and coatings, oil and gas, and pharmaceuticals represent stable to niche segments, with pharmaceuticals delivering the highest purity and margin profile despite limited volumes.

Market Share By Application, 2025.png)

Market Share by End-Use Industry: Textile & Leather Dominates While Agriculture Expands Rapidly

Textile and leather industries collectively represent around 38% of AEEA consumption in 2025, consolidating demand from fabric care and textile additive applications. AEEA-derived chelants and auxiliaries are essential in fiber pretreatment, dyeing, finishing, leather de-liming, and industrial textile maintenance. The segment is volume-driven and margin-sensitive, with growth closely tied to Asian production hubs and sustainability initiatives such as ZDHC and bluesign programs encouraging substitution of legacy surfactants. Agriculture is the fastest-growing end-use, supported by expansion of generic agrochemical manufacturing in India and China and sustained demand across row and specialty crops. Healthcare and personal care deliver stable, high-margin consumption in chelating agents and pharmaceutical intermediates. Oil and gas remains cyclical, tied to LNG and gas treating capacity, while automotive and infrastructure applications, including epoxy coatings and cement grinding aids, show modest GDP-linked growth.

Aminoethylethanolamine (AEEA) Market Competitive Landscape

The global aminoethylethanolamine market is characterized by high entry barriers driven by feedstock integration, purification complexity, and downstream performance requirements across detergents, agrochemicals, coatings, electronics, and water treatment. Market leaders are competing on production scale, carbon footprint transparency, and specialty-grade purity, while Asia-Pacific continues to emerge as the fastest-growing consumption hub. Strategic capacity expansions in North America and Europe, coupled with localized manufacturing in China and India, are reshaping global supply chains. Key players are leveraging vertical integration into ethylene oxide and ammonia, mass-balance certification, and electronic-grade purification to secure long-term contracts in fabric care, semiconductor manufacturing, and specialty coatings.

Texas-scale integration positions Dow Inc. as the world’s largest AEEA supplier

Dow remains the global heavyweight in aminoethylethanolamine, supplying nearly one-third of worldwide demand from its Texas production hub. In early 2025, the company ramped this facility to full nameplate capacity, reinforcing Dow’s leadership in North American agrochemicals, lubricants, and industrial detergents. Its DOW AEEA Pro grade, launched in 2023–2024, targets oilfield chemicals and high-durability coatings requiring superior amine performance. Dow’s core strength lies in unmatched economies of scale and backward integration into ethylene oxide and ammonia, insulating margins from feedstock volatility. Through its “Digital Reliability” strategy, Dow applies predictive supply-chain analytics to deliver just-in-time AEEA for large fabric care and cleaning manufacturers.

Green AEEA leadership drives BASF SE’s dominance in Europe

BASF has positioned itself as the European leader in sustainable aminoethylethanolamine through aggressive capacity expansion and carbon-transparent production. A 50% increase at its Antwerp site in late 2024 established BASF as the region’s dominant AEEA supplier for 2025–2026. In 2025, BASF introduced mass-balance certified AEEA using bio-attributed feedstocks, enabling downstream customers to meet net-zero commitments. The company dominates chelating agent applications, where AEEA replaces harsher phosphonates in water treatment and industrial cleaning. Operating within its Verbund system, BASF integrates hydrogenative amination of monoethylene glycol into a circular energy-and-waste loop, delivering consistent quality with industry-leading production efficiency.

Electronic-grade purity defines Huntsman Corporation’s specialty AEEA strategy

Huntsman focuses on high-margin E-grade aminoethylethanolamine for semiconductors, automotive electronics, and pharmaceutical synthesis. Its E-GRADE® AEEA delivers ultra-low trace metal content and assays exceeding 99.5%, making it essential for microchip fabrication and advanced electronics. In 2025, Huntsman expanded AEEA capacity at its Geismar, Louisiana facility by 25% to support the accelerating U.S. semiconductor buildout. With deep expertise in alkanolamine chemistry, Huntsman supplies some of the industry’s highest-purity intermediates. Rather than competing in bulk volumes, its “Innovation at the Edge” strategy prioritizes low-volume, specialty AEEA grades that command premium pricing in electronics, healthcare, and precision materials.

Downstream surfactant integration strengthens Nouryon’s global AEEA footprint

Nouryon leverages aminoethylethanolamine as both a merchant product and a critical internal building block for surfactants and chelates. Its Berol AEEA 99, launched in 2023, has become a preferred intermediate for amphoacetate surfactants used in tear-free baby shampoos. In 2025, Nouryon formed a joint venture in Ningbo to localize AEEA production for Asia’s textile and personal care markets. Deep downstream integration makes Nouryon its own largest AEEA customer, supplying cationic softeners and asphalt additives. Supported by a strong EMEA and APAC distribution network, the company delivers localized technical service to textile finishing and specialty chemical customers.

Specialty purification expertise elevates Tosoh Corporation in Asia-Pacific

Tosoh is the technological benchmark for high-stability and high-viscosity amine derivatives in the Asian AEEA market. In 2025, it scaled production of Toa AEEA H-50, engineered specifically for Japan’s pharmaceutical sector as a precursor for complex drug molecules. Tosoh’s strategy centers on specialty purification, removing color-forming impurities to support premium latex paints, clear adhesives, and high-end coatings. The company is also a key supplier of wet-adhesion monomers across Asia-Pacific, preventing paint peeling in humid climates. Looking ahead, Tosoh is investing in smart warehousing in 2026 to improve shelf-life stability of hygroscopic AEEA during regional distribution.

Cost-competitive exports position Prasol Chemicals Pvt. Ltd. in the value segment

Prasol Chemicals represents the fast-growing value-driven segment of the global aminoethylethanolamine market, supplying high volumes to detergent, textile, and corrosion inhibitor manufacturers. In 2025, Prasol secured REACH registration for higher tonnage bands, unlocking aggressive export expansion into the European Union. Its strength lies in cost-efficient Indian manufacturing focused on industrial-grade AEEA below 99% purity, widely used in bulk fabric softeners. Prasol dominates dye-fixing agent applications across South Asian textile corridors. In 2026, the company announced a transition toward renewable energy at its manufacturing sites, aligning production with sustainability requirements from global consumer packaged goods partners.

Belgium Aminoethylethanolamine Market: Integrated Verbund Expansion Anchors European Supply Security

Belgium has reinforced its position as a strategic European production hub for AEEA through large-scale capacity expansion and supply chain integration. In late 2024, BASF completed a 50% expansion of aminoethylethanolamine capacity at its Antwerp Verbund site. The project was fast-tracked to meet rising regional demand for high-purity intermediates used in coatings, textiles, and specialty chemicals.

The Antwerp facility benefits from a fully integrated production chain spanning ethylene oxide through ethyleneamines, which strengthens localized sourcing and reduces logistics-related emissions. Energy transition initiatives are also reshaping the site’s footprint, with offshore North Sea wind power being progressively integrated into processing units. Belgium’s AEEA output is increasingly directed toward advanced fabric softeners and textile additives that comply with EU Eco-label biodegradability criteria, reinforcing its relevance in regulated downstream markets.

United States Aminoethylethanolamine Market: Oilfield Chemicals and Low-VOC Coatings Drive High-Purity Demand

In the United States, AEEA demand is being driven by energy, coatings, and specialty materials, supported by targeted capacity investments. In 2025, Huntsman Corporation completed a 25% capacity expansion at its Geismar, Louisiana site, prioritizing high-purity AEEA for oilfield chemicals and aerospace coatings. This expansion aligns with record demand from shale operations in the Permian Basin, where AEEA-derived imidazoline corrosion inhibitors are critical for managing high-CO2 environments.

Regulatory updates are reinforcing this shift. The U.S. Environmental Protection Agency’s 2025 revisions under the Toxic Substances Control Act have accelerated adoption of ultra-low VOC AEEA variants in paints and coatings. Innovation is also extending into life sciences, with Dow Chemical showcasing AEEA-based biocompatible coatings in 2025 for medical devices and pharmaceutical packaging, signaling broader diversification beyond traditional industrial applications.

Japan Aminoethylethanolamine Market: Semiconductor-Grade Purity and Export-Oriented Specialty Amines

Japan’s AEEA landscape is defined by precision manufacturing and alignment with semiconductor expansion. In late 2024 and early 2025, Tosoh Corporation commercialized Toa AEEA H-50, a high-purity grade engineered for applications requiring purity levels above 99.5%. This product is increasingly used in semiconductor and pharmaceutical processes where contamination thresholds are extremely low.

With the expansion of domestic wafer fabrication capacity during 2025, AEEA demand has risen for specialized photoresist strippers and advanced cleaning agents. Policy support has reinforced export momentum, as Japan’s Ministry of Economy, Trade and Industry included specialty amines in its 2025 Chemical Export Roadmap, facilitating AEEA shipments to Southeast Asian electronics manufacturing hubs and strengthening Japan’s role in high-value amine exports.

Germany Aminoethylethanolamine Market: Electronic-Grade Pivot and Circular Amine Synthesis

Germany is positioning AEEA within its broader semiconductor and sustainability agenda. In October 2025, BASF announced plans for a new electronic-grade facility in Ludwigshafen, designed to support Europe’s semiconductor value chain by 2027. This move reflects rising demand for ultra-clean amines used in chip manufacturing, coatings, and advanced materials.

Circular economy principles are increasingly embedded in German AEEA production. Manufacturers are leading adoption of ex-situ catalyst regeneration in amine synthesis, reducing waste volumes by 12% compared with 2023 benchmarks. In parallel, the Federal Ministry of Education and Research allocated funding in 2025 for green amine synthesis programs, targeting bio-based catalysts and more efficient reaction pathways to reduce energy intensity across the AEEA value chain.

China Aminoethylethanolamine Market: Urbanization-Driven Demand and Sustainability Recognition

China continues to expand its AEEA footprint through a combination of domestic capacity additions and sustainability initiatives. Rapid urbanization drove a 15% increase in consumption of AEEA-based chelating agents during 2025, particularly for industrial water treatment and high-performance detergents used in municipal and manufacturing infrastructure.

Capacity growth has followed demand. Regional producers in Jiangsu and Shandong commissioned new AEEA distillation units in 2025 to serve automotive coatings and adhesive manufacturers. Sustainability performance is also gaining prominence, with Nouryon receiving the 2025 Responsible Care® Awards in China for freshwater conservation and emission reductions across its production sites, reinforcing the country’s transition toward greener amine chemistry.

Country-Level Strategic Positioning in Aminoethylethanolamine

Aminoethylethanolamine Market County Level Snapshot

|

Country

|

Strategic Focus

|

Industry Implication

|

|

Belgium

|

Integrated Verbund expansion and renewable energy

|

Secure European supply of low-carbon, high-purity AEEA

|

|

United States

|

Oilfield chemicals and low-VOC coatings

|

Rising demand for high-purity and compliant AEEA variants

|

|

Japan

|

Semiconductor-grade purity and exports

|

Strengthened role in electronics and specialty amine supply

|

|

Germany

|

Electronic-grade facilities and circular synthesis

|

Alignment with semiconductor growth and green chemistry

|

|

China

|

Urbanization-driven demand and sustainability

|

Scaled domestic capacity with improving environmental performance

|

Aminoethylethanolamine Market Report Scope

Aminoethylethanolamine Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$262.1 Million

|

|

Market Size (2034)

|

$406.6 Million

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Purity Grade (High Purity Grade, Technical Grade), By Product Function (Chemical Intermediates, Surfactants and Emulsifiers, Chelating Agents, Corrosion Inhibitors, Lube Oil Additives), By Application (Textile Additives, Fabric Care, Agrochemicals, Pharmaceuticals, Oil and Gas, Paints and Coatings), By End Use Industry (Oil and Gas, Textile and Leather, Agriculture, Healthcare and Personal Care, Automotive and Infrastructure)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc, Huntsman International LLC, Tosoh Corporation, Nouryon, Akzo Nobel NV, Delamine BV, TCI Chemicals India Pvt Ltd, Diamines and Chemicals Limited, Zhengzhou Meiya Chemical Products, Balaji Amines Limited, Shandong IRO Amine, Ashland Inc, Sumitomo Chemical, Evonik Industries AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Aminoethylethanolamine Market Segmentation

By Purity Grade

- High Purity Grade

- Technical Grade

By Product Function

- Chemical Intermediates

- Surfactants and Emulsifiers

- Chelating Agents

- Corrosion Inhibitors

- Lube Oil Additives

By Application

- Textile Additives

- Fabric Care

- Agrochemicals

- Pharmaceuticals

- Oil and Gas

- Paints and Coatings

By End Use Industry

- Oil and Gas

- Textile and Leather

- Agriculture

- Healthcare and Personal Care

- Automotive and Infrastructure

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Aminoethylethanolamine Industry

- BASF SE

- Dow Inc

- Huntsman International LLC

- Tosoh Corporation

- Nouryon

- Akzo Nobel NV

- Delamine BV

- TCI Chemicals India Pvt Ltd

- Diamines and Chemicals Limited

- Zhengzhou Meiya Chemical Products

- Balaji Amines Limited

- Shandong IRO Amine

- Ashland Inc

- Sumitomo Chemical

- Evonik Industries AG

*- List not Exhaustive