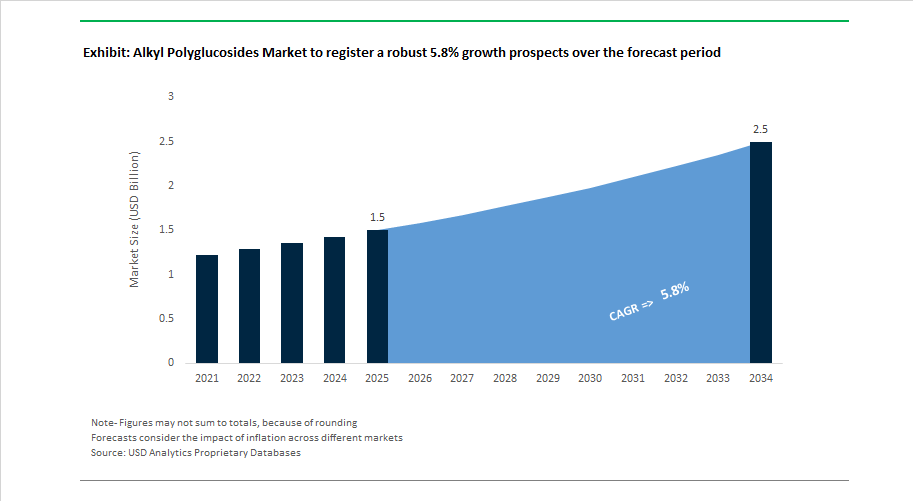

Market Overview: Alkyl Polyglucosides Market to Reach $2.5 Billion by 2034 as Bio-Based Surfactants Gain Regulatory and Consumer Momentum

The global alkyl polyglucosides market is projected to grow from $1.5 billion in 2025 to $2.5 billion by 2034, registering a 5.8% CAGR supported by rising demand for bio-based non-ionic surfactants in home care, personal care, agriculture, and industrial cleaning. Alkyl polyglucosides are valued for high biodegradability, low aquatic toxicity, mildness on skin, and compatibility with eco-labeled formulations, making them central to clean beauty, green detergents, and sustainable industrial cleaning systems. Growth is reinforced by tightening environmental standards on synthetic surfactants, increasing adoption of renewable feedstocks such as glucose and fatty alcohols, and consumer preference for sulfate-free, plant-derived cleansing ingredients. Market expansion is also driven by formulation shifts toward concentrated and refillable cleaning systems that rely on low-foam, high-efficiency surfactants.

Innovation and capacity development accelerated in March 2024 when Stepan Company expanded its agricultural adjuvant portfolio with APG-based wetting agents supporting precision farming. Market analysis in late 2024 confirmed strong valuation growth, with fatty alcohol-derived APGs leading due to demand in clean beauty and eco-detergents. Regulatory drivers intensified in August 2025 as the EU advanced stricter biodegradability rules for detergent capsules, favoring APG adoption. Performance diversification followed in mid-2025 with rising demand for C8-C10 chain APGs for industrial degreasing and concentrated cleaners. Industrial sustainability narratives strengthened in July 2025 when Dow showcased circular surfactant technologies at K 2025, followed by November 2025 launches of bio-based personal care ingredients for Asian markets.

Strategic supply localization gained momentum in November 2025 as BASF inaugurated APG production expansion in Thailand to serve Asia’s home and personal care sectors. In October 2025, Nouryon introduced sustainable surfactant solutions compatible with APG systems for industrial cleaning. Ethical sourcing reached a milestone in December 2025 when Croda International achieved deforestation-risk-free raw material sourcing, a key factor for plant-based surfactant credibility. Governance and strategic focus evolved in January 2026 with Croda’s board appointment reinforcing sustainability-led growth. Capacity expansion in North America was confirmed in January 2026 as BASF scheduled the start-up of its Cincinnati APG line for late 2026. Industry data released in January 2026 showed home care as the dominant application, reflecting accelerating penetration of alkyl polyglucosides in eco-friendly household cleaning formulations worldwide.

Strategic Market Trends and High-Value Opportunities Reshaping the Alkyl Polyglucosides Market

Market Trend: Environmental Regulations Accelerate APG Substitution in Industrial and Institutional Cleaning

A central inflection point in the Alkyl Polyglucosides Market is the large-scale replacement of legacy petrochemical surfactants in Industrial and Institutional (I&I) cleaning. Regulatory enforcement has moved from advisory statements to binding compliance mandates that now determine supplier eligibility.

Under the EU’s Chemicals Strategy for Sustainability, 2025 marks the phase where "Safe and Sustainable by Design" rules become enforceable, particularly in industrial degreasers and CIP (Clean-in-Place) formulations. APGs satisfy OECD 301 B biodegradability benchmarks, making them a preferred ingredient for regions where wastewater discharge permits require surfactants to be fully metabolized in treatment systems. In the U.S., EPA regulatory tightening on VOC emissions in commercial cleaners has forced petrochemical surfactants to undergo reformulation or exit. APGs gain a strategic advantage because their near-zero VOC profile supports environmental compliance without sacrificing performance.

Technical parity is another catalyst. Clariant’s 2025 Care Chemical data confirms that APGs maintain foam structure and surfactant activity in high-alkaline pH environments above 10, a capability that traditional surfactants often lack. As food-processing plants and cold-chain facilities adopt higher-frequency CIP cycles, APGs are emerging as a mission-critical component that ensures sanitation standards without degrading equipment surfaces or the microbial ecosystem of wastewater plants.

Market Trend: Capacity Expansion and Vertical Integration Strengthen Supply Chain Control

The Alkyl Polyglucosides Market is also being reshaped by supplier-side strategy, where profitability hinges on upstream control over fatty alcohol feedstocks and downstream regional localization. APGs were once treated as a specialty niche, but rising home-care sustainability demand is enabling multi-site, mass-production strategies.

BASF’s November 2025 expansion in Thailand positions the facility near palm-based fatty alcohol supply clusters, which lowers raw-material volatility and regional shipping emissions. Together with sites in Jinshan (China) and Düsseldorf (Germany), BASF is creating a multi-regional network designed to reduce carbon-adjusted transportation costs by 15 to 20% and satisfy regional content requirements imposed by FMCG procurement contracts.

North America is following suit. BASF’s Cincinnati production line is planned for 2026 and is directly tied to U.S. retailer sustainability pledges that now require surfactants with 100% renewable carbon content. Producers such as Croda are integrating ISCC-PLUS mass-balance traceability models, enabling the issuance of Product Carbon Footprint (PCF) certificates. These certificates are now mandatory bid-qualification documents for large-volume detergent contracts with multinational brands. The market is therefore becoming a competitive landscape where carbon transparency is equally as important as performance chemistry.

Market Opportunity: APGs as Technology Enablers for Compact and Ultra-Concentrated Detergent Formats

The global laundry and home-care sector is undergoing structural packaging and formulation disruption. Growth is shifting not by volume but through compactization, where products deliver the same cleaning power at significantly lower weight and water content. APGs play a central role in this transformation. Their high solubility and electrolyte tolerance allow them to remain stable in 3X to 4X concentrated detergents, unlike traditional surfactants that phase-separate in high-salt environments.

APGs are also enabling the next wave of single-dose pods, where avoiding premature dissolution of the PVA capsule is essential. Their use as a non-aqueous surfactant carrier provides formulators the freedom to increase active-ingredient concentration and control viscosity. Regulatory reports across the UK and EU (2024–2025) emphasize that compact formats reduce plastic packaging weight by up to 60% and cut transport emissions by approximately 35 percent, allowing brands to meet Extended Producer Responsibility (EPR) compliance. As detergent innovations move toward concentrated spray formats and dissolvable sheets, APGs will serve as the backbone surfactant category that ensures multi-format stability.

Market Opportunity: Low-Drift Agricultural Adjuvants for Precision Farming and UAV Spraying

Agriculture represents one of the highest-growth adjacency markets for Alkyl Polyglucosides, driven by the need to balance chemical efficacy with environmental controls. APGs have evolved from basic wetting agents to high-value adjuvants that enable pesticide optimization in an era of strict environmental risk reduction mandates.

Scientific studies published in 2024–2025 show that APGs increase spray droplet Volume Median Diameter (VMD), reducing wind-drift of droplets under 100 μm by as much as 59%. This property is especially critical as Agricultural UAV spraying expands in China and Brazil, where ULV applications generate micro-droplets with high drift potential. APGs enhance adhesion to foliage, increase penetration through waxy cuticle surfaces, and reduce bounce-off or evaporation under high-heat conditions.

In alignment with the EU Farm to Fork Strategy, which mandates a 50% cut in pesticide chemical risk by 2030, APGs are positioned as a sustainability-linked ingredient category. Because they increase biological performance of pesticides, farmers can reduce total active-ingredient usage by 15 to 25% without compromising yield. This makes APG-based adjuvants a compliance-support segment where adoption is expected to surge in regulated agricultural markets.

Alkyl Polyglucosides (APG) Market Share and Segmentation Insights

Market Share by Product Type: C12–C14 APGs Lead as Specialty Chain Lengths Expand

C12–C14 alkyl polyglucosides account for approximately 38% of global APG consumption in 2025, retaining leadership due to their optimal balance of foaming, detergency, and skin mildness. Derived primarily from lauryl alcohol sourced from coconut and palm kernel oil, this grade is the standard surfactant for hand dishwashing liquids, premium laundry detergents, and sulfate-free body washes, commanding the highest price point in consumer APG portfolios. C10–C12 APGs rank second, favored for superior wetting and grease-cutting in industrial degreasers, hard-surface cleaners, and agrochemical emulsifiers, with strong caustic stability supporting dairy and bottle-washing applications. C8–C10 APGs serve high-foam specialty cleaners and cold-water laundry as rapid-biodegrading co-surfactants. C14–C16 APGs remain the smallest but highest-margin segment, used in premium skincare and fabric care where enhanced emulsification and mildness justify higher costs despite viscosity handling challenges.

Market Share by Application: Home Care Dominates While Agrochemicals Deliver Fastest Growth

Home care represents roughly 41% of APG demand in 2025, driven by phosphate-free automatic dishwashing gels and concentrated laundry liquids where APGs provide foam control, hard-water tolerance, and enzyme compatibility. Regulatory bans on phosphates across major regions have structurally lifted APG usage, sustaining steady 5 to 6% annual growth. Personal care ranks second and is the premium segment, with APGs anchoring sulfate-free shampoos, baby washes, and sensitive skin products backed by renewable feedstocks and ECO/COSMOS certifications, often priced two to three times higher than industrial grades. Industrial and institutional cleaning delivers volume through food processing, dairy sanitation, and vehicle wash concentrates, aligned with LEED and EU Ecolabel procurement standards. Agricultural chemicals are the fastest-growing application, as APGs replace APEOs in herbicides and fungicides, improving wetting and rainfastness. Oil & gas remains smallest, with niche growth from offshore “green chemistry” programs.

Market Share By Application, 2025.png)

Competitive Landscape: Sugar-Based Surfactants and Sulfate-Free Formulations Driving the Alkyl Polyglucosides Market

The global Alkyl Polyglucosides (APG) Market is accelerating as formulators replace petrochemical surfactants with biodegradable, non-ionic alternatives derived from renewable sugars and fatty alcohols. Competitive differentiation now centers on global manufacturing scale, sulfate-free formulation expertise, eco-label compliance, and application-specific APG systems for home care, personal care, agrochemicals, and industrial cleaning. Market leaders are expanding capacity across Asia-Pacific and North America while investing in sensory performance, low-foam variants, and customized blends that enable brands to move away from LAS without sacrificing cleaning efficacy or consumer experience.

BASF SE scales global APG capacity to support sulfate-free care formulations

BASF SE remains the undisputed leader in alkyl polyglucosides, operating the industry’s most extensive APG manufacturing network across Europe, the United States, China, and Thailand. In November 2025, BASF expanded its Bangpakong facility to meet surging Asia-Pacific demand, while a new Cincinnati APG line scheduled for 2026 will support North America’s transition toward sulfate-free personal and home care. Its Glucopon® and Plantacare® brands are benchmark non-ionic biosurfactants made from 100% natural feedstocks. Through its Care Chemicals division, BASF enables formulators to replace LAS with mild, high-performance APGs without compromising detergency.

Clariant AG advances premium sugar surfactants with eco-label compliance

Clariant AG has repositioned around Natural Resources, emphasizing high-purity APGs for premium care applications. Its GlucoPure® and GlucoTain® series leverage sorbitol-based chemistry to deliver a creamy foam profile favored in facial cleansers and shampoos. During 2025–2026, Clariant expanded its Eco-Label-certified APG portfolio, ensuring alignment with EU Ecolabel and Nordic Swan standards. With integrated global manufacturing and 68 subsidiaries, Clariant supports customers transitioning to fully renewable formulations. Its Synergy Blending expertise also enables APG systems that stabilize actives in cosmetics and agrochemical formulations.

Dow Inc. embeds APGs into agrochemical and industrial cleaning platforms

Dow Inc. applies its materials science scale to deploy APGs across industrial and agricultural markets where conventional surfactants are being phased out. Through its TRITON™ CG series, Dow leads in agrochemical adjuvants, improving pesticide wetting and penetration while maintaining low-toxicity profiles. In early 2026, Dow launched its Transform to Outperform initiative, using AI and automation to modernize specialty chemical delivery. Strategically, Dow is pursuing Circular Chemistry, exploring APG production from waste plant biomass in partnership with research institutions to further reduce carbon intensity across I&I cleaning and crop protection applications.

Croda International Plc innovates low-foam and bio-based APG derivatives for niche performance needs

Croda International operates as a niche innovator, developing APG derivatives with specialized functionality beyond basic cleansing. Its Atlox™ AL-2575 LF addresses excessive foaming in glyphosate and herbicide spray tanks, solving a long-standing agrochemical formulation challenge. Croda’s ECO Range offers one of the widest portfolios of 100% bio-based surfactants, including APG hybrids produced using bio-ethanol. The company is also scaling self-cleaning textile technologies incorporating APGs and provides deep formulation support for SMEs launching green-label brands, reinforcing Croda’s role in high-value specialty applications.

SEPPIC targets clean beauty with sensory-optimized APG systems

SEPPIC, a subsidiary of Air Liquide, specializes in the sensory dimension of green chemistry. Its SIMULSOL® APG portfolio spans C8 to C16 chain lengths, enabling precise control of foaming and viscosity. SEPPIC holds particular strength in C8–C10 APGs, increasingly adopted in 2026 by minimalist and eco-conscious brands seeking gentle yet effective cleansing. The company is expanding into bio-emulsifiers, using APG technology to stabilize water-in-oil systems without synthetic polymers, while strategically aligning with the Clean Beauty movement for sensitive and baby skin care.

Fenchem democratizes APGs through cost-competitive biosurfactant supply

Fenchem represents the rising influence of Chinese biosurfactant manufacturing, supplying high-volume, value-segment APGs under its FenEco® range, including caprylyl/capryl, lauryl, decyl, and coco glucosides. In 2025, Fenchem expanded overseas distribution centers, adopting a local-stock model in Europe and North America to compete on lead times with Western producers. The company also offers blended surfactant bases combining APGs with betaines, providing ready-to-use systems for shampoo and body wash manufacturers. Fenchem’s strategy focuses on affordability, making APGs accessible to price-sensitive consumers across Asia and Latin America.

Thailand Alkyl Polyglucosides Market: ASEAN-Centered Scale and Bio-Circular Policy Alignment

Thailand has emerged as a strategic production and logistics hub for APGs in Southeast Asia. In November 2025, BASF inaugurated a world-scale expansion at its Bangpakong site, a move directly tied to accelerating demand for sustainable care chemicals across ASEAN. The facility is designed to operate as a high-agility export hub, shortening lead times and improving supply flexibility for personal care and home care formulators compared with Europe-sourced alternatives.

Operational excellence is central to the expansion. The new Bangpakong line integrates advanced automated process controls to ensure batch-to-batch consistency required for sensitive skin and baby care mildness benchmarks. Policy tailwinds reinforce the investment, as Thailand’s Bio-Circular-Green economic model has created a supportive regulatory environment for oleochemical derivatives, positioning the country as a preferred base for bio-based surfactant manufacturing in Asia-Pacific.

United States Alkyl Polyglucosides Market: Supply Security, Clean Beauty Alignment, and Pet Care Uptake

The United States is reinforcing domestic APG supply while expanding downstream use cases. BASF confirmed that a high-volume APG production line in Cincinnati, Ohio, is progressing toward startup in 2026, strengthening North American resilience for non-ionic surfactants. This investment responds to formulators’ preference for regionally sourced, bio-based inputs amid evolving consumer and regulatory expectations.

Regulatory alignment is catalyzing formulation shifts. In December 2025, the U.S. Food and Drug Administration advanced new sunscreen ingredient proposals, accelerating the use of APGs as emulsifiers for mineral UV filters in clean beauty portfolios. Product innovation continues as Dow debuted DEXCARE polymers and high-performance APG blends in 2025, emphasizing sulfate-free hair care performance. Beyond human care, the Kansas Animal Health Corridor reported record APG adoption in premium pet shampoos and tearless grooming products, supported by dermatological safety data for animals.

Germany Alkyl Polyglucosides Market: Digital Traceability, Biodegradability, and Low-Carbon Production

Germany is setting the regulatory and sustainability benchmark for APGs in Europe. Following the December 2025 approval of the new EU Detergents and Surfactants Regulation, German manufacturers began implementing Digital Product Passports with a 3.5-year transition window. This ensures full traceability of palm and coconut feedstocks, reinforcing transparency across APG supply chains.

Environmental criteria further favor APGs. Germany’s Federal Environment Agency influenced EU mandates for stricter ultimate biodegradability requirements, positioning APGs ahead of conventional ethoxylated alcohols. On the innovation front, BASF launched Sokalan Eco GP 790 L in late 2024, a bio-based anti-redeposition polymer engineered to work synergistically with APG-based detergents. Production decarbonization is also progressing, with Düsseldorf sites reporting a 12% reduction in Scope 1 and 2 emissions through 2025 by transitioning high-temperature synthesis steps to green electricity.

India Alkyl Polyglucosides Market: PLI-Backed R&D and Export-Oriented Specialization

India’s APG ecosystem is expanding through policy-driven investment and export readiness. By mid-2025, realized investments under the Specialty Chemicals Production Linked Incentive scheme reached ₹1.76 lakh crore, enabling companies such as Galaxy Surfactants to advance R&D into indigenous corn- and coconut-derived APG variants. These efforts support both cost competitiveness and feedstock security.

Export strategy is explicit. India’s 2025 Chemical Industry Roadmap identifies APGs as a high-potential category for the European Union due to strong alignment with Green Deal sustainability criteria. Infrastructure modernization in the Gujarat Petroleum, Chemicals and Petrochemicals Investment Region has added distillation and ethoxylation-alternative units, enabling local production of high-viscosity APG grades tailored for industrial degreasing and institutional cleaning.

China Alkyl Polyglucosides Market: Local Feedstock Integration and Eco-Certified Demand

China’s APG market is characterized by consolidation and sustainability-led demand resilience. Throughout 2025, regional producers such as Shanghai Fine Chemical and Yangzhou Chenhua intensified competition by scaling feedstock-integrated plants, challenging multinational suppliers on cost and responsiveness.

Policy signals are reinforcing adoption. In late 2025, the Ministry of Industry and Information Technology introduced a Green Disinfectant label, accelerating APG use as co-surfactants in eco-certified household cleaners. Despite a contraction in broader chemical sales during 2025, the care chemicals segment remained resilient, supported by rapid uptake of mild surfactants across domestic e-commerce beauty channels.

Country-Level Strategic Positioning in Alkyl Polyglucosides

Alkyl Polyglucosides Market County Level Snapshot

|

Country

|

Strategic Focus

|

Implication for APGs

|

|

Thailand

|

World-scale capacity and BCG policy

|

ASEAN supply hub with high consistency standards

|

|

United States

|

Domestic supply security and clean beauty

|

Expanded use in sunscreens, hair care, and pet care

|

|

Germany

|

Digital traceability and biodegradability

|

Regulatory preference for APGs and low-carbon production

|

|

India

|

PLI-backed R&D and EU-oriented exports

|

Indigenous APG variants and industrial grades

|

|

China

|

Feedstock integration and eco-label demand

|

Competitive pricing and resilient care chemicals uptake

|

Alkyl Polyglucosides Market Report Scope

Alkyl Polyglucosides Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.5 Billion

|

|

Market Size (2034)

|

$2.5 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Product Type (C8 to C10 Alkyl Polyglucosides, C10 to C12 Alkyl Polyglucosides, C12 to C14 Alkyl Polyglucosides, C14 to C16 Alkyl Polyglucosides), By Raw Material (Fatty Alcohols, Sugars), By Application (Personal Care, Home Care, Industrial and Institutional Cleaning, Agricultural Chemicals, Oil and Gas), By Form (Liquid, Powder and Granular), By Distribution Channel (Direct Sales, Specialty Chemical Distributors)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc, Clariant AG, Croda International Plc, Galaxy Surfactants Limited, Shanghai Fine Chemical Company, Yangzhou Chenhua New Material, Nouryon, Stepan Company, Seppic SA, Pilot Chemical Company, Huntsman Corporation, LG Household and Health Care, Fenchem Biotek, Spec Chem Industry

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Alkyl Polyglucosides Market Segmentation

By Product Type

- C8 to C10 Alkyl Polyglucosides

- C10 to C12 Alkyl Polyglucosides

- C12 to C14 Alkyl Polyglucosides

- C14 to C16 Alkyl Polyglucosides

By Raw Material

By Application

- Personal Care

- Home Care

- Industrial and Institutional Cleaning

- Agricultural Chemicals

- Oil and Gas

By Form

- Liquid

- Powder and Granular

By Distribution Channel

- Direct Sales

- Specialty Chemical Distributors

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Alkyl Polyglucosides Industry

- BASF SE

- Dow Inc

- Clariant AG

- Croda International Plc

- Galaxy Surfactants Limited

- Shanghai Fine Chemical Company

- Yangzhou Chenhua New Material

- Nouryon

- Stepan Company

- Seppic SA

- Pilot Chemical Company

- Huntsman Corporation

- LG Household and Health Care

- Fenchem Biotek

- Spec Chem Industry

*- List not Exhaustive