Industrial Degreaser Market to Reach $34 Billion by 2034 at 4.6% CAGR Amid Bio-Based Solvent Innovation and Heavy-Duty Maintenance Expansion

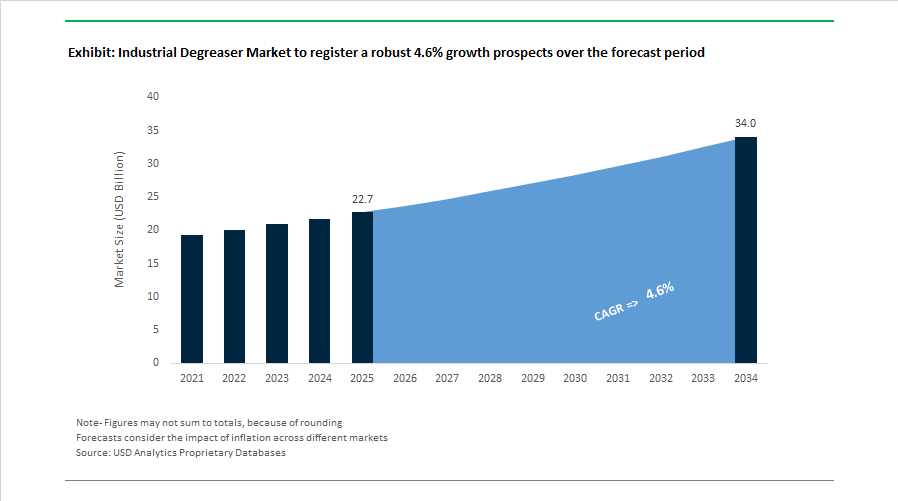

The Industrial Degreaser Market is projected to grow from $22.7 billion in 2025 to $34 billion by 2034, reflecting a CAGR of 4.6%. Demand is being driven by stringent environmental regulations, rising industrial automation, semiconductor manufacturing expansion, and the transition toward biodegradable and low-VOC cleaning chemistries. Industrial degreasers are essential in manufacturing, automotive maintenance, food processing, aerospace, heavy equipment servicing, and precision electronics. Increasing pressure to eliminate chlorinated solvents and reduce hazardous air pollutants is accelerating reformulation strategies across North America, Europe, and Asia-Pacific, pushing manufacturers toward water-based, plant-derived, and USDA-certified alternatives without compromising cleaning efficiency.

Innovation momentum accelerated in early 2024 when CRC Industries launched its Chlor-Free® Universal Degreaser, engineered as a 50-state compliant non-chlorinated solution capable of delivering high-speed removal of oils, grease, and industrial residues while adhering to strict VOC limits. In the same year, Molyslip introduced SLIPCLEAN RD in the UK, targeting multi-soil removal across industrial maintenance environments, including carbon deposits, inks, adhesives, and heavy machinery grease. Zep Inc., following the acquisition of EcoClear, completed brand integration into its AFCO division by 2025, strengthening its footprint in food and beverage sanitation where heavy-duty degreasing must align with hygiene compliance standards.

Sustainability-driven transformation intensified in 2025. In March 2025, Renewable Lubricants launched GreenStrip Bio, a USDA-certified bio-based degreaser designed for agricultural and construction equipment, addressing soil and water contamination concerns. In May 2025, BASF commercialized a breakthrough partnership with RiKarbon to upcycle bio-waste into biodegradable degreasing solvents, positioning plant-based chemistries as viable alternatives to petroleum-derived hydrocarbons. During the same month, IndSpyre Solutions and Lygos collaborated to introduce Soltellus, a renewable polymer additive enhancing degreaser performance in the industrial and institutional segment. In June 2025, Solenis and NCH Corporation finalized a strategic merger, integrating NCH’s middle-market industrial maintenance expertise into Solenis’s global water and hygiene portfolio, significantly strengthening on-site degreasing services across manufacturing and heavy industry sectors.

Market diversification extended into high-tech and automotive applications in late 2025. In October 2025, CRC Industries unveiled Brākleen Foaming Brake Wash at SEMA 2025, signaling a pivot toward safer water-based degreasing formulations with reduced flammability and improved operator safety. In November 2025, Ecolab expanded its Integrated Cooling Program for AI-driven data centers, deploying specialized degreasing and anti-fouling chemistries to maintain liquid-cooled server efficiency and prevent bio-grease accumulation. In December 2025, Ecolab closed its acquisition of Ovivo’s Electronics Ultrapure Water business, strengthening its precision cleaning capabilities for semiconductor fabrication. Entering 2026, BASF expanded its Mangalore production footprint in February, reinforcing surfactant and performance chemical supply chains across Asia. Meanwhile, Henkel reported over €10.9 billion in Adhesive Technologies sales in 2025, highlighting growth in sustainable industrial cleaners and surface-treatment chemistries aligned with its Purposeful Growth strategy.

Industrial Degreaser Market Trends and Opportunities Shaping Next-Generation Cleaning Technologies

Global Regulatory Phase-Out of Chlorinated Solvents Forcing Rapid Reformulation in Industrial Degreasers

The industrial degreaser market is undergoing a structural transformation as regulators phase out legacy chlorinated and brominated solvents historically used in vapor degreasing and metal cleaning applications. Environmental and occupational safety concerns surrounding chemicals such as trichloroethylene (TCE), perchloroethylene (PCE), and methylene chloride are pushing manufacturers toward safer, low-VOC alternatives. This regulatory pressure is accelerating the development of next-generation industrial degreasing formulations, including hydrofluoroethers (HFEs), modified alcohol blends, and aqueous cleaning systems that deliver comparable cleaning efficiency while meeting strict environmental compliance requirements.

Recent regulatory decisions are significantly reshaping the competitive landscape. Under the U.S. EPA’s Toxic Substances Control Act (TSCA) framework, most industrial uses of trichloroethylene (TCE) were banned effective September 15, 2025, with additional restrictions placed on perchloroethylene (PCE). Similarly, a comprehensive commercial ban on methylene chloride will take effect on April 28, 2026, forcing industrial facilities to adopt safer drop-in alternatives such as trans-1,2-dichloroethylene blends and hydrofluoroether-based degreasers. In Europe, the EU REACH Annex XVII expansion under Commission Regulation (EU) 2025/1090 introduced new restrictions on solvents such as N,N-dimethylacetamide (DMAC), with usage limits in industrial mixtures taking effect by December 23, 2026. Additionally, new Existing Chemical Exposure Limit (ECEL) standards for PCE set at 0.14 ppm in 2026 are making legacy solvent-based degreasing systems economically unviable due to high compliance costs, accelerating the industry-wide shift toward safer industrial cleaning chemistries.

Rising Adoption of Aqueous and Bio-Based Degreasers in Food Processing and Hygiene-Critical Manufacturing

The food processing and beverage manufacturing sectors are increasingly adopting aqueous and bio-based industrial degreasers to meet strict food safety regulations and sustainability goals. These formulations eliminate the risk of toxic residues while offering biodegradable and low-VOC alternatives to conventional solvent cleaners. As manufacturers pursue clean-label production environments and safer sanitation practices, plant-derived degreasers and water-based cleaning systems are gaining traction across equipment cleaning, conveyor maintenance, and food-contact surface sanitation.

Industry innovation is supporting this transition. In May 2025, IndSpyre Solutions partnered with Lygos to launch Solellus, a bio-based industrial cleaner utilizing high-performance biopolymers capable of matching petrochemical solvent efficiency while remaining fully biodegradable. Similarly, Renewable Lubricants introduced GreenStrip Bio in March 2025, a USDA-certified bio-based degreaser designed specifically for agricultural and food-processing machinery, offering strong grease removal without VOC emissions associated with mineral spirits. Another rapidly expanding segment involves citrus-based terpene degreasers derived from d-limonene, which have become the fastest-growing solutions in food processing due to their low toxicity and suitability for confined cleaning environments without specialized respiratory protection. Corporate sustainability programs are also supporting this shift. For example, Jabil’s 2025 sustainability report highlighted a 90% landfill diversion rate across 14% of its global facilities, achieved partly by transitioning from hazardous solvent-soaked rags to aqueous degreasing systems with filtration and wastewater recycling capabilities.

Additive Manufacturing Growth Creating Demand for Precision Degreasers for 3D Printed Components

The rapid expansion of industrial additive manufacturing (3D printing) is creating a specialized niche within the industrial degreaser market. Complex printed components often require precise removal of uncured photopolymer resins, support materials, and surface contaminants without damaging delicate geometries or porous structures. Traditional solvents such as isopropyl alcohol (IPA) are increasingly being replaced by high-performance aqueous detergents and specialty cleaning chemistries designed specifically for additive manufacturing workflows.

Technological advancements in post-processing are driving this opportunity. According to PostProcess Technologies’ 2025 industry report, automated resin-removal detergents now last up to ten times longer than traditional IPA cleaning baths, reducing chemical waste significantly and improving operational efficiency in aerospace and medical additive manufacturing facilities. Additionally, the replacement of IPA in dental and healthcare laboratories is accelerating due to its flammability and VOC risks, with facilities adopting non-flammable aqueous degreasing systems integrated into automated cleaning stations to meet upcoming 2026 ISO safety standards. Another emerging segment involves vapor smoothing technologies, such as the PostPro SF series, which utilize controlled solvent vapors to smooth 3D printed surfaces and deliver an injection-molded finish. This trend creates opportunities for chemical suppliers to develop material-specific solvents optimized for polymers like Nylon and ABS, expanding the role of advanced degreasing chemistries in additive manufacturing post-processing.

Closed-Loop Solvent Recovery Systems Driving Circular Economy Opportunities in Industrial Cleaning

The increasing cost of virgin chemicals and rising hazardous waste disposal fees are encouraging industries to adopt closed-loop solvent recovery systems, creating a major opportunity in the industrial degreaser market. These systems allow companies to reclaim and reuse solvents used in metal cleaning, electronics manufacturing, and pharmaceutical production, reducing both operational costs and environmental impact. As regulatory agencies tighten VOC emission limits and industrial waste regulations, solvent recycling technologies are becoming a strategic investment for solvent-intensive manufacturing sectors.

Industrial waste management companies are already demonstrating the economic benefits of solvent recovery. In early 2026, Veolia reported that advanced distillation-based solvent reclamation systems can recover up to 95% of used solvents, reducing approximately 172,000 tonnes of CO₂ emissions annually compared with producing virgin solvents. Meanwhile, the plastic recycling industry is increasingly adopting solvent-based dissolution processes to recover materials such as PET and polypropylene, accounting for more than 50% of investments in advanced recycling technologies by 2026. Breakthroughs in membrane-based solvent separation technologies, reported in late 2025, are also improving energy efficiency by recovering high-purity solvents directly at the point of use, particularly in pharmaceutical and semiconductor cleaning operations. Regulatory momentum is also strong in Asia-Pacific, where China’s stricter VOC emission standards introduced in 2025 have already driven a 35% increase in closed-loop degreasing system adoption among automotive and electronics component manufacturers, reinforcing the shift toward sustainable industrial cleaning solutions.

Industrial Degreasers Market Share and Segmentation Insights

Water-Based Industrial Degreasers Lead the Market Through Low-VOC Cleaning Technologies

Water-based degreasers accounted for 48.6% of the Industrial Degreaser Market share in 2025, making them the dominant degreasing technology across industrial maintenance and manufacturing cleaning operations. These formulations typically combine alkaline or acidic aqueous solutions with surfactants, emulsifiers, and specialty additives to remove oils, grease, machining fluids, and industrial contaminants from metal surfaces and equipment. Their strong adoption is driven by the ability to deliver effective cleaning performance while significantly reducing volatile organic compound (VOC) emissions, fire hazards, and hazardous waste handling requirements compared with traditional solvent-based degreasers. Regulatory pressure and corporate sustainability goals have accelerated the transition toward water-based degreasing technologies in industries seeking safer and environmentally compliant cleaning solutions. In 2025, technological innovation has enabled advanced surfactant packages and performance additives that improve soil penetration, emulsification, and rinsability, allowing modern water-based degreasers to achieve cleaning efficiency comparable to solvent-based systems in most industrial applications while supporting lower environmental impact and improved workplace safety.

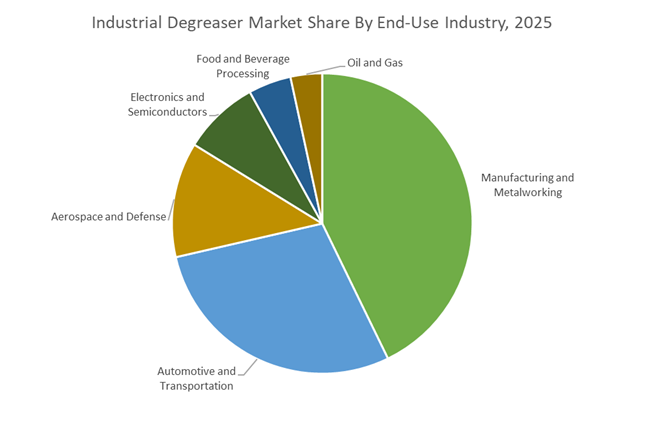

Manufacturing and Metalworking Operations Drive the Largest Industrial Degreaser Demand

Manufacturing and Metalworking represented 42.8% of the Industrial Degreaser Market share in 2025, establishing it as the largest end-use sector for industrial degreasing chemicals. Metal fabrication and machining processes generate significant volumes of cutting oils, lubricants, coolants, stamping fluids, and metalworking residues, all of which must be removed between processing stages to maintain product quality and ensure proper adhesion during coating, plating, or assembly operations. Industrial degreasers are therefore used continuously in machining lines, stamping plants, fabrication workshops, and equipment maintenance operations, creating sustained demand across the manufacturing sector. In 2025, global supply chain restructuring has triggered a near-shoring and regional manufacturing revival in North America and Europe, increasing industrial production capacity and strengthening demand for industrial cleaning and degreasing chemicals. At the same time, these regions are implementing stricter environmental and workplace safety regulations, pushing manufacturers to adopt water-based and bio-based degreasing formulations that comply with evolving VOC limits while maintaining the high cleaning performance required for modern metalworking and industrial processing environments.

Competitive Landscape in Industrial Degreaser market

Ecolab Expands Omnichannel and Semiconductor Footprint

Ecolab Inc. is reinforcing its leadership by extending professional-grade degreasers into retail-industrial hybrid channels. During 2025–2026, its Ecolab Scientific Clean™ line expanded into more than 180 Home Depot locations across North America, including a new 5-gallon industrial format for heavy-duty users. The late-2025 acquisition of Ovivo’s Electronics Ultrapure Water business enhances its position in semiconductor and AI-driven data center cleaning, where contamination control is critical. Core products include aluminum-safe Fast Action Degreaser and bio-based Heavy Duty Citrus Degreaser formulations. In 2026, Ecolab is emphasizing water and energy resilience through AI-enabled benchmarks and its Water Use Efficiency Index, helping industrial clients reduce cleaning cycle water consumption and energy intensity.

Henkel Advances Low-Temperature Metal Degreasing

Henkel AG & Co. KGaA is positioning energy-efficient degreasing as a decarbonization lever for automotive and manufacturing customers. In February 2026, it launched Bonderite C-AD 20202, a low-temperature dip-degreasing surfactant capable of operating at 35–40°C, reducing energy consumption by up to 35% compared to traditional 65°C systems. A new Science Park hub in Singapore, opened in January 2026, strengthens electronics and APAC supply integration. Improved CDP and EcoVadis sustainability scores reinforce its “Green Chemistry” positioning. Digitalized customer service integration with SAP enhances technical response times for global metal-processing clients.

BASF Prioritizes Near-Zero SVOC Formulations

BASF SE is sharpening focus on high-performance surfactants and chelating agents for industrial degreasers following the March 2026 divestiture of its optical brightening agent business. In early 2026, BASF commercialized Near-Zero SVOC technology to improve indoor air quality and reduce semi-volatile emissions in industrial cleaning dispersions. With approximately €60 billion in 2025 sales, BASF is channeling capital toward its Nutrition & Care and Industrial Solutions segments. Investments in local production, including new dispersion lines in Mangalore, India (February 2026), strengthen supply for fast-growing regional manufacturing hubs. The company’s positioning centers on circular-economy alignment and low-emission formulations.

ITW Pro Brands Focuses on Precision and Safety

ITW Pro Brands, part of Illinois Tool Works, specializes in precision degreasing for aerospace, military, and heavy equipment maintenance. Its LPS MAX® Instant Super Degreaser 2.0 eliminates brominated solvents, TCE, and perchloroethylene while remaining non-flammable. Recent formulation upgrades reduced Global Warming Potential by 19% without compromising rapid evaporation or residue-free performance. In 2026, the company highlighted flood restoration cleaning systems targeting machinery recovery after extreme weather events. User-centric packaging innovations, including locking flip-straw actuators and ergonomic embossed cans, enhance worker safety and reduce chemical waste.

CRC Industries Accelerates Aqueous MRO Solutions

CRC Industries continues leading in MRO-oriented degreasing chemistry with solvent-alternative aqueous systems. HydroForce® Industrial Strength Degreaser delivers solvent-like cleaning strength while remaining non-flammable and non-abrasive for machinery and concrete. NSF C1 and K1 registrations expand its footprint in meat and poultry processing facilities, a growing 2026 segment. The T-Force® Next Generation Degreaser introduces a non-conductive, fast-evaporating formula suited for electric motors and air tools—critical as electrified equipment adoption rises. CRC’s strategic positioning centers on VOC reduction pathways while maintaining high flash points and corrosion protection.

Dow Supplies Oxygenated and Silicone Solvent Foundations

Dow Inc. provides foundational oxygenated solvents and silicone-based systems that underpin modern degreaser formulations. Under its “Transform to Outperform” initiative, Dow targets $2 billion in EBITDA improvement by 2028, with portfolio optimization underway in Europe. Surpassing 1,000 megawatts of renewable electricity sourcing in 2025 strengthens its sustainability credentials. The DOWSIL™ and ECOLIBRIUM™ brands emphasize silicone-based and bio-derived solvents offering high solubility for heavy oils with reduced toxicity. Dow’s role in the degreaser market is primarily upstream, supplying performance solvents that enable next-generation low-VOC and high-efficiency industrial cleaners.

United States Industrial Degreaser Market: Regulatory Bans Driving Solvent Substitution and Bio-Based Scale-Up

The United States industrial degreaser market is entering a forced transition cycle shaped by regulatory prohibition, aerospace innovation, and federal supply chain incentives. Under the revised Toxic Substances Control Act, the EPA has mandated the prohibition of most commercial uses of methylene chloride for vapor degreasing by April 28, 2026. This rule effectively removes dichloromethane from large segments of metal finishing, electronics, and maintenance operations, accelerating industrial adoption of alternative vapor-phase solvents such as hydrofluoroethers and engineered hydrocarbon blends. Parallel enforcement pressure on trichloroethylene is reinforcing this shift. EPA scrutiny of TCE aerosols has triggered a 2026 enforcement phase that is pushing workshops toward closed-loop solvent systems and water-based degreasing platforms to meet occupational exposure limits.

Innovation and supply-side restructuring are advancing in tandem. In October 2025, Henkel launched Bonderite C-AK DW 805 AERO, a non-flammable dry-wash aircraft degreaser that eliminates water rinsing, reduces maintenance downtime, and aligns with FAA-supported sustainability objectives for 2026. At the formulation layer, Evonik finalized an exclusive U.S. distribution agreement with Sea-Land Chemical in March 2025 to scale rhamnolipid-based biosurfactants for heavy manufacturing degreasing. The bio-based pivot is reinforced by Renewable Lubricants, which introduced GreenStrip Bio in March 2025, a USDA-certified degreaser engineered for high-torque agricultural and construction equipment. These shifts are underpinned by Facility Readiness grants issued under the 2025 Federal Supply Chain Task Force, incentivizing domestic synthesis of high-purity hydrocarbon degreasers and reducing dependence on imported solvents.

European Union Industrial Degreaser Market: Clean Industrial Deal, PFAS Exit, and Decarbonized Production

Across Germany, France, and Belgium, the industrial degreaser industry is being reshaped by capital-backed decarbonization, PFAS disclosure mandates, and tighter occupational exposure standards. In February 2025, the European Commission launched the Clean Industrial Deal, mobilizing more than €100 billion to accelerate made-in-Europe clean manufacturing. Industrial formulators are leveraging these subsidies to transition toward bio-based, circular degreasing chemistries that reduce solvent toxicity and lifecycle emissions. The regulatory trajectory is equally decisive. The proposed Annex XV PFAS restriction framework requires manufacturers to declare all PFAS content by early 2026, impacting an estimated 10,000 fluorinated substances and triggering a rapid R&D shift toward siloxane-acrylic hybrid degreasers and fluorine-free alternatives.

Performance-focused innovation is progressing alongside compliance. In April 2025, BASF commercialized Trilon G, a GLDA-based chelating agent with approximately 56% renewable carbon content that improves soil removal efficiency of industrial degreasers in hard water conditions. German chemical clusters are also piloting green hydrogen in etherification processes for oxygenated solvents, targeting a 12% reduction in production energy intensity by the end of 2026. Regulatory oversight is tightening further as the European Chemicals Agency prepares to evaluate twenty additional substances in 2026, with a specific focus on solvents used in metal degreasing to align with updated occupational exposure limits. Collectively, these measures are compressing timelines for reformulation while rewarding scalable, low-carbon degreasing platforms.

China Industrial Degreaser Market: Policy-Led Upgrading, VOC Tax Pressure, and Digital Traceability

China’s industrial degreaser market is advancing through mandatory standards, fiscal disincentives for high-VOC formulations, and large-scale upgrading of solvent purity. Under the MIIT petrochemical growth roadmap for 2025–2026, seven departments jointly targeted an average annual expansion of the chemical sector while prioritizing the upgrading of traditional products. High-purity alcohols and hydrocarbon solvents for precision degreasing are explicitly identified as focus areas, supporting automotive, electronics, and equipment manufacturing. Regulatory enforcement is accelerating substitution. The Ministry of Finance has intensified the 4% consumption tax on industrial cleaning agents exceeding 420 g/l VOCs, driving rapid adoption of water-based aqueous degreasers across the automotive manufacturing belt.

Standards and feedstock security are reinforcing this transition. National Standard GB 30981.1-2025, effective June 1, 2026, mandates reductions in harmful substances across coatings and cleaning auxiliaries, effectively curbing chlorinated solvent use. On the supply side, PetroChina Guangdong surpassed performance guarantees for its STRATCO alkylation unit in 2025, securing a domestic source of high-purity aliphatic hydrocarbons suitable for industrial degreasing. Looking ahead, China’s 2026 AI plus Petrochemicals mandate requires degreaser manufacturing facilities to implement blockchain-based traceability across hazardous chemical lifecycles, elevating compliance, auditability, and downstream waste accountability.

India Industrial Degreaser Market: Acquisition-Led Capability and Incentivized Localization

India’s industrial degreaser industry is transitioning from import dependence toward localized capability building supported by acquisitions, fiscal incentives, and industrial infrastructure. In the first quarter of 2026, the Indian group Praana, parent of Galata Chemicals, is expected to close the acquisition of a major global plastic additives and modifiers business. The transaction includes critical intermediates used in high-performance industrial degreaser synthesis, immediately expanding India’s access to advanced formulation chemistries and global customer linkages.

Policy support is accelerating domestic production. The 2026 Union Budget expanded Production-Linked Incentive schemes for high-end polymer and chemical additives, offering tax rebates for enzyme-based and bio-based industrial cleaners. Infrastructure readiness is being addressed through the fast-tracked development of Petroleum, Chemical, and Petrochemical Investment Regions in Gujarat, designed to attract global degreaser manufacturers and integrate compliant waste management systems. This coordinated approach aims to reduce import dependency by 2027 while positioning India as a competitive production base for next-generation industrial degreasing solutions.

Industrial Degreaser Industry: Country-Level Strategic Summary

Industrial Degreaser Market County Level Snapshot

|

Region

|

Primary Regulatory or Policy Driver

|

Key Technology Shift

|

Structural Impact

|

|

United States

|

TSCA methylene chloride ban, TCE enforcement

|

HFEs, bio-based and closed-loop systems

|

Rapid solvent substitution and onshoring

|

|

European Union

|

Clean Industrial Deal, PFAS restriction

|

Siloxane-acrylic hybrids, GLDA chelation

|

Decarbonized, fluorine-free reformulation

|

|

China

|

VOC taxation, GB 30981.1-2025

|

Water-based systems, high-purity hydrocarbons

|

Policy-led upgrading with digital traceability

|

|

India

|

PLI expansion, strategic acquisition

|

Enzyme-based and bio-based degreasers

|

Localized capability and reduced imports

|

Industrial Degreaser Market Report Scope

Industrial Degreaser Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$22.7 Billion

|

|

Market Size (2034)

|

$34 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Type (Water-Based Degreasers, Solvent-Based Degreasers, Bio-Based Degreasers), By Form (Liquid Concentrates, Ready-to-Use Sprays, Aerosols, Wipes and Impregnated Substrates, Powders and Granules), By Application Method (Vapor Degreasing, Ultrasonic Cleaning, Dip and Immersion Tanks, Spray and Wipe Applications, Clean-in-Place Systems), By End-Use Industry (Automotive and Transportation, Aerospace and Defense, Manufacturing and Metalworking, Electronics and Semiconductors, Food and Beverage Processing, Oil and Gas)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc., BASF SE, Henkel AG & Co. KGaA, Dow Inc., Exxon Mobil Corporation, 3M Company, Evonik Industries AG, Solvay S.A., Nouryon B.V., Illinois Tool Works Inc., NCH Corporation, Castrol, Clariant AG, Sinopec, A.W. Chesterton Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Degreaser Market Segmentation

By Type

- Water-Based Degreasers

- Alkaline

- Acidic

- Neutral

- Enzymatic

- Solvent-Based Degreasers

- Petroleum Hydrocarbons

- Chlorinated Solvents

- Oxygenated Solvents

- Fluorinated Solvents

- Bio-Based Degreasers

- Plant-Based Oils

- Terpenes

- Sugar-Based Surfactants

By Form

- Liquid Concentrates

- Ready-to-Use Sprays

- Aerosols

- Wipes and Impregnated Substrates

- Powders and Granules

By Application Method

- Vapor Degreasing

- Ultrasonic Cleaning

- Dip and Immersion Tanks

- Spray and Wipe Applications

- Clean-in-Place Systems

By End-Use Industry

- Automotive and Transportation

- Aerospace and Defense

- Manufacturing and Metalworking

- Electronics and Semiconductors

- Food and Beverage Processing

- Oil and Gas

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Industrial Degreaser Industry

- Ecolab Inc.

- BASF SE

- Henkel AG & Co. KGaA

- Dow Inc.

- Exxon Mobil Corporation

- 3M Company

- Evonik Industries AG

- Solvay S.A.

- Nouryon B.V.

- Illinois Tool Works Inc.

- NCH Corporation

- Castrol

- Clariant AG

- Sinopec

- A.W. Chesterton Company

*- List not Exhaustive