Oxygenated Solvents Market Surges Toward $1.58 Trillion by 2034 as Battery Electrolytes, Electronics-Grade IPA, and Circular Solvent Technologies Scale

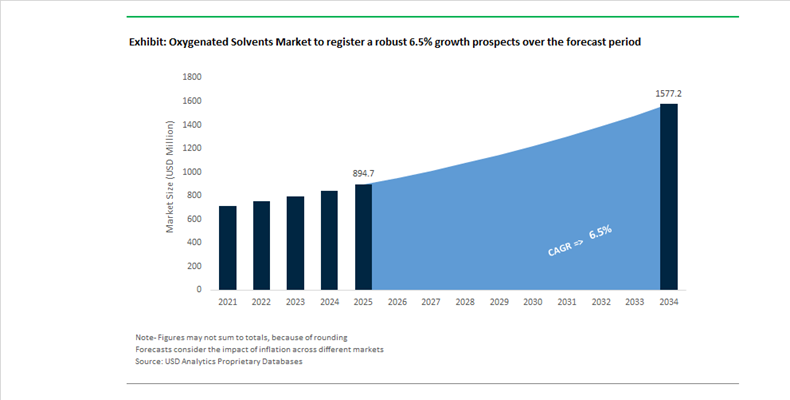

The Oxygenated Solvents Market is valued at $894.7 Million in 2025 and is projected to reach $1,577 Million by 2034, expanding at a CAGR of 6.5%. Growth is anchored in sustained demand for alcohols, glycols, ketones, esters, and carbonate solvents across automotive coatings, adhesives, pharmaceuticals, semiconductors, and lithium-ion batteries. Oxygenated solvents such as isopropyl alcohol (IPA), methanol, ethylene oxide derivatives, propylene carbonate, n-propanol, and n-propyl acetate remain essential for dissolution efficiency, low toxicity profiles, and compatibility with advanced formulations. The market is undergoing structural realignment as producers rationalize European assets, localize high-purity supply chains in North America and Asia-Pacific, and accelerate bio-based and circular solvent production to meet ESG mandates.

In March 2024, Dow announced construction of a world-scale carbonate solvents facility on the U.S. Gulf Coast, targeting lithium-ion battery electrolyte demand for EVs and grid storage. In August 2024, Eastman launched electronic-grade EastaPure™ IPA to strengthen domestic semiconductor solvent supply, addressing ultra-low impurity requirements in wafer fabrication. In May 2024, INEOS acquired LyondellBasell’s Bayport EO and derivatives business, reinforcing its position in ethylene oxide–derived solvents used in pharmaceuticals, cosmetics, and construction chemicals. In December 2024, BASF opened a Catalyst Development and Solids Processing Center in Ludwigshafen to accelerate low-carbon and bio-based solvent production technologies using advanced catalysis.

Portfolio restructuring intensified in 2025. In February 2025, Oxea implemented price increases of $0.07/lb for n-propanol and n-propyl acetate in North America and Mexico amid rising production costs. In May 2025, OQ Chemicals formally rebranded back to Oxea following recapitalization by Strategic Value Partners and Blantyre Capital, reducing debt by approximately €400 million and sharpening focus on oxo-intermediates and core solvent lines. In June 2025, LyondellBasell agreed to sell major European olefins and polyolefins assets to AEQUITA for $2.6 billion, with closure expected in early 2026, reflecting a geographic shift toward cost-competitive regions. Earlier, in October 2024, LyondellBasell had acquired full ownership of APK AG, integrating solvent-based recycling technology that produces high-purity LDPE from flexible packaging waste, embedding circular solvent chemistry into its portfolio.

Sustainability certifications and specialty differentiation are reshaping competitive positioning. In early 2024, Solvay secured Vegan Trademark certification for its Augeo® Crystal and Hexylene Glycol solvents, strengthening its foothold in clean beauty and fragrance markets. In April 2024, BASF launched Efka® PX 4360 dispersing agent for solvent-borne industrial coatings using Controlled Free Radical Polymerization to enhance pigment stability. In December 2024, Oxea divested its Amsterdam esters plant to Perstorp, allowing expansion of specialty ester production while concentrating on core oxo alcohols.

Strategic Trends and High-Impact Opportunities in the Oxygenated Solvents Market

Mandatory Phase-Out of E-Series Glycol Ethers Accelerates Shift to Safer Oxygenated Solvents

The oxygenated solvents market is undergoing a structurally enforced transition as regulatory authorities tighten controls on solvents classified as reproductive toxins. Ethylene glycol ethers, particularly E-series products such as EGBE and EGME, are becoming commercially untenable across coatings, industrial cleaning, and specialty formulations. As of September 2025, intensified enforcement by the United States Environmental Protection Agency and the European Chemicals Agency has transformed solvent selection from a performance-led decision into a compliance-driven necessity.

Under the revised TSCA risk evaluation framework released in September 2025, the EPA now requires solvent risk assessments based on specific conditions of use. This approach directly targets high-volume E-series glycol ethers, exposing manufacturers to higher compliance costs, workplace controls, and potential usage bans for non-essential applications. In parallel, the European Commission’s REACH Annex XVII update, effective September 1, 2025, added 16 new substances to the Carcinogenic, Mutagenic, or Reproductive Toxic restriction list. This has forced rapid reformulation in industrial cleaners and architectural coatings, where oxygenated alternatives with equivalent solvency power but lower toxicity profiles are now preferred.

As a result, propylene glycol ethers have become the default replacement across professional and industrial markets. Supplier disclosures from mid-2025 indicate that P-series solvents now account for more than 85% of new project specifications in North America and Europe. Their lower vapor pressure, reduced inhalation risk, and safer-by-design positioning make them particularly attractive for manufacturers seeking to future-proof formulations while maintaining application performance.

Bio-Based Acetates and Fermentation-Derived Alcohols Gain Strategic Momentum

Decarbonization commitments are emerging as a second powerful force reshaping the oxygenated solvents landscape. To meet Science-Based Targets initiative goals and respond to customer pressure, chemical producers are scaling production of bio-based ethyl acetate, ethanol, and related oxygenates that can be directly substituted into existing formulations. These renewable solvents offer an immediate pathway to reduce Scope 3 emissions without requiring capital-intensive process changes for downstream users.

A landmark investment illustrating this shift is the €120–€130 million bio-ethyl acetate facility being developed by CropEnergies AG in Zeitz, Germany. Initiated in April 2024 and scheduled for commissioning in late 2025, the plant will produce ethyl acetate from renewable ethanol, reducing fossil carbon intensity by more than 70% compared to petrochemical routes. This model is gaining traction as long-term offtake agreements for bio-ethanol and bio-acetates rose by roughly 40% year over year, according to 2025 sustainability disclosures from publicly traded chemical companies.

Demand is particularly strong from cosmetics, pharmaceuticals, and personal care brands, where renewable carbon content is now a procurement requirement rather than a marketing differentiator. In 2025, several leading consumer product companies confirmed the transition of nail polish and fragrance formulations to solvents with more than 99% bio-based content. Government support is reinforcing this trend, with combined EU and U.S. subsidies for renewable chemical projects exceeding $1 billion annually, lowering the cost gap between bio-based and fossil-derived oxygenated solvents.

High-Boiling Oxygenated Solvents Unlock Efficiency Gains in Lithium-Ion Battery Manufacturing

The rapid scale-up of lithium-ion battery production is creating a high-value opportunity for advanced oxygenated solvents. As cathode chemistries shift toward high-nickel formulations and electrode coatings become thicker, traditional solvent systems are facing both performance and sustainability constraints. While N-methyl-2-pyrrolidone remains widely used, its toxicity profile and energy-intensive drying requirements are prompting manufacturers to explore safer alternatives.

Research published in 2025 demonstrates that replacing NMP with oxygenated solvents such as DMF or novel glyme-based systems can reduce electrode drying energy consumption by up to four times. This is a material advantage for gigafactories seeking to lower operational costs and carbon intensity simultaneously. With grid-scale energy storage capacity surpassing 7.5 gigawatts in 2024, as documented by the U.S. Department of Energy, demand for high-purity, recoverable solvents in battery slurries is accelerating.

In response, solvent suppliers are developing multi-component oxygenated blends that deliver lower volatility and improved thermal stability. These formulations help prevent cracking and delamination in ultra-thick electrodes while supporting solvent recovery and reuse. Government-backed battery programs in South Korea and the EU are further funding water-compatible oxygenated co-solvents that reduce volatile organic compound emissions by an estimated 30%, positioning this segment as one of the fastest-growing opportunity areas in the oxygenated solvents market.

Non-Hazardous Oxygenated Degreasing Systems Replace Chlorinated Solvents

The full enforcement of the U.S. ban on trichloroethylene for industrial degreasing in September 2025 has created an immediate and sizable replacement market for non-hazardous oxygenated solvent blends. Industries ranging from aerospace to automotive manufacturing are under pressure to identify alternatives that match the cleaning power of chlorinated solvents without their environmental and health liabilities.

New-generation oxygenated degreasers, typically based on tailored blends of modified alcohols and esters, are gaining rapid approval. These systems offer high flash points above 60 degrees Celsius, meet OECD 301 F biodegradability standards, and deliver strong solvency for oils and machining residues. In early 2025, major aerospace original equipment manufacturers approved biodegradable oxygenated cleaners for precision components, citing zero residue performance and significantly improved worker safety profiles.

Occupational exposure limits are reinforcing adoption beyond the United States. Several EU member states lowered permissible exposure thresholds for aromatic solvents in 2025, triggering a surge in acetate-based degreasing solutions within the automotive components sector. Adoption in this segment rose by approximately 25% as manufacturers sought operator-friendly, regulation-aligned solvents that deliver consistent cleaning performance while reducing compliance risk. Collectively, these dynamics are repositioning oxygenated solvents as the backbone of next-generation, non-hazardous industrial cleaning systems.

Oxygenated Solvents Market Share and Segmentation Insights

Alcohol-Based Oxygenated Solvents Lead Market Demand with Versatile Industrial Solvency

Alcohols accounted for 38.60% of the Oxygenated Solvents Market by product type in 2025, establishing them as the dominant solvent class used across industrial and specialty chemical applications. Methanol, ethanol, isopropanol, and butanol are widely used in paints and coatings, pharmaceutical processing, and industrial cleaning formulations due to their effective solvency, controlled evaporation characteristics, and compatibility with both aqueous and organic chemical systems. Established production infrastructure and global chemical supply chains support large scale alcohol solvent consumption. In 2025, increasing investment in bio alcohol production technologies is influencing market growth, with fermentation derived ethanol, bio methanol, and bio butanol gaining adoption as renewable solvents that align with green chemistry initiatives and sustainability commitments in chemical manufacturing.

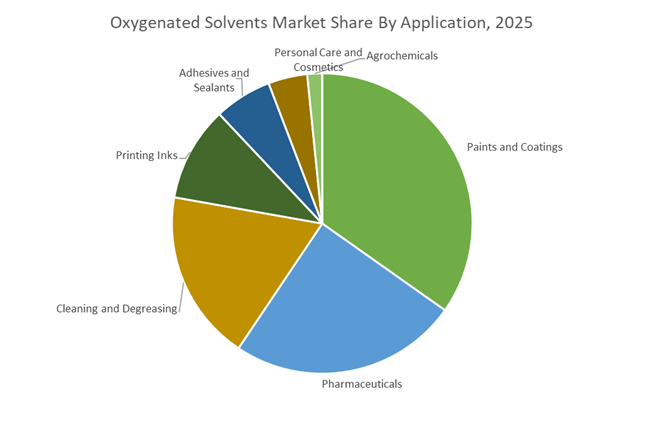

Paints and Coatings Sector Drives Oxygenated Solvent Consumption in Industrial Coating Formulations

Paints and coatings represented 34.80% of the Oxygenated Solvents Market by application in 2025, reflecting the critical role solvents play in coating formulation, viscosity adjustment, and film formation during coating application. Oxygenated solvents dissolve resins and additives in solvent borne coatings and function as coalescing agents in waterborne paint systems used in architectural, industrial, and automotive coatings. The large global scale of coating production continues to sustain strong solvent demand across multiple manufacturing industries. In 2025, the industry shift toward high solids and waterborne coating formulations is influencing solvent usage patterns, reducing solvent content per unit of coating while maintaining demand for specialty oxygenated solvents used in advanced industrial coating technologies.

Oxygenated Solvents Market Competitive Landscape

The Oxygenated Solvents Market is shifting toward bio-based intermediates, high-purity electronic-grade solvents, and circular production models. Leading players are focusing on AI-driven process optimization, carbon footprint reduction, and advanced recycling technologies to meet stringent regulatory requirements across coatings, electronics, pharmaceuticals, and energy storage applications.

BASF strengthens Verbund-driven solvent production with cost optimization and Asia expansion

BASF SE is reinforcing its leadership in oxygenated solvents through its integrated Verbund model, enabling efficient production of alcohols, glycols, and esters at global scale. The operationalization of its Zhanjiang Verbund site significantly enhances regional supply capacity for Asia-Pacific markets, particularly in coatings and adhesives. With projected EBITDA of €6.2–€7.0 billion in 2026, BASF is benefiting from strong demand for sustainable intermediates in its Chemicals and Nutrition & Care segments. The company achieved €1.7 billion in cost savings in 2025 and is targeting €2.3 billion by 2026 to improve operational efficiency. Its divestment of the decorative paints business sharpens focus on upstream solvent and monomer production. This integration of scale, efficiency, and portfolio optimization strengthens BASF’s competitive positioning.

Dow accelerates AI-driven solvent innovation with bio-circular and electronics-focused investments

Dow Inc. is advancing its oxygenated solvents portfolio through its Transform to Outperform strategy, targeting $2 billion in EBITDA improvement via automation and digitalization. The company is leveraging AI to modernize production and customer engagement in its Industrial Intermediates & Infrastructure segment. Its ISCC PLUS-certified Freeport facility enables mass-balanced bio-circular solvent production, aligning with sustainability targets. The Cooling Science Studio in Shanghai supports development of high-purity solvents for semiconductor and electronics thermal management applications. A CAD $1.62 billion financial inflow strengthens Dow’s ability to invest in advanced recycled and renewable solvent technologies. This combination of innovation, sustainability, and regional investment enhances its competitive advantage.

ExxonMobil expands high-purity solvent portfolio with pricing power and energy transition applications

ExxonMobil Product Solutions is maintaining a strong position in oxygenated and specialty solvents through high-performance product portfolios and strategic pricing adjustments. The 2026 price increase across Exxsol™ and Isopar™ lines reflects tightening supply conditions and strong demand for low-aromatic, regulatory-compliant solvents. Its Solvesso™ and Exxsol™ D grades are increasingly aligned with ultra-low naphthalene requirements, reducing environmental labeling constraints. ExxonMobil’s Escaid™ fluids are gaining traction in lithium-ion battery recycling and metal extraction, highlighting the integration of solvents into green energy value chains. The company also supplies high-purity IPA and MEK for disinfection and industrial adhesive applications. This focus on performance, compliance, and emerging applications strengthens ExxonMobil’s market presence.

Eastman scales molecular recycling to produce low-carbon specialty oxygenated solvents

Eastman Chemical Company is differentiating itself through molecular recycling technologies that enable production of oxygenated solvents with high recycled content and reduced environmental impact. Its Kingsport methanolysis facility generated $60 million in incremental earnings in 2025 while significantly increasing recycled feedstock utilization. Plans for a second facility in Longview, Texas will further expand capacity for sustainable solvent production. The company is targeting $125–$150 million in cost reductions in 2026 to maintain margins amid market volatility. Despite a 7% decline in revenue, Eastman generated nearly $1 billion in operating cash flow, reflecting strong portfolio resilience. This focus on circularity and cost discipline positions Eastman as a leader in sustainable solvent innovation.

LyondellBasell optimizes portfolio and expands circular solvent feedstock capabilities

LyondellBasell (LYB) is strengthening its position in oxygenated solvents through portfolio optimization and strategic investments in intermediates and recycling technologies. The planned divestment of four European assets by mid-2026 reflects a shift toward high-margin oxyfuels and intermediate chemicals. The company exceeded its 2025 cash generation target, reaching $800 million, and is aiming for $1.3 billion by 2026 to support growth initiatives. Investments of $1.2 billion in capital expenditure include the Flex-2 propylene expansion and MoReTec-2 recycling facility, both critical for sustainable solvent feedstock production. Improved profitability in intermediate chemicals highlights strong demand for styrene and oxyfuel derivatives. This combination of financial strength, portfolio focus, and circular innovation enhances LYB’s competitive positioning.

China – Circular Chemistry Scale-Up and Semiconductor-Grade Purity

China’s oxygenated solvents industry is transitioning from volume-driven production toward circular chemistry and ultra-high-purity applications. In early 2025, BASF SE inaugurated its first commercial loopamid® facility at Caojing, Shanghai, a milestone that embeds oxygenated intermediates into fully circular polyamide value chains and enables textile-to-textile recycling at industrial scale. This development is complemented by the November 2025 commissioning of a CFRP-enabled dispersant production line at Nanjing Jiangbei, strengthening regional supply of advanced oxygenated additives for coatings and industrial formulations. Policy backing under the 14th Five-Year Plan is accelerating the industrialization of bio-based succinic acid and 1,4-butanediol, reinforcing China’s ambition to dominate biodegradable plastics and downstream solvent derivatives.

At the same time, purity and efficiency standards are tightening. Domestic producers in Zhejiang have finalized 2026 expansion plans for semiconductor-grade isopropyl alcohol to support 7nm and 5nm fabrication nodes, positioning oxygenated solvents as strategic enablers of China’s electronics self-sufficiency. The Ministry of Industry and Information Technology of China has enforced new Efficiency Top Runner standards for methanol and ethanol plants, mandating a 12% energy-intensity reduction by late 2026. Export policy realignment in 2025, including renewed purchases of U.S. bio-feedstocks, is stabilizing domestic production of oxygenated esters and alcohols while insulating supply chains from agricultural volatility.

United States – Bio-Solvent Incentives and Carbon-Managed Production

The U.S. oxygenated solvents market is being reshaped by biofuel policy clarity, carbon management, and tightening purity standards. In November 2025, guidance from the U.S. Environmental Protection Agency on Renewable Fuel Standard volumes signaled higher blending mandates for 2026, directly incentivizing ADM and Cargill to expand bio-ethanol and bio-butanol capacities targeted at solvent applications. Pricing discipline has also tightened, with Eastman Chemical Company implementing North American price increases for n-butyl acetate and n-propyl acetate in May 2025 to offset feedstock and logistics inflation.

Strategic repositioning is evident among integrated energy and chemical players. ExxonMobil allocated a portion of its expanded lower-emission investment plan toward CCS-enabled low-carbon oxygenated intermediates, signaling convergence between solvents and decarbonized petrochemicals. Technical standards are also rising, with ASTM D770 updates in 2025 imposing stricter limits on non-volatile residues in isopropyl alcohol, driven by ultra-clean requirements from the U.S. electronics sector. Export momentum remains strong, as near-record ethanol shipments in Q3 2025 to India and Brazil reinforced the U.S. role as a global supplier of fuel-grade and industrial oxygenated solvents.

Germany (EU Hub) – Bioeconomy Alignment and Regulatory Substitution

Germany is positioning oxygenated solvents at the core of the EU bioeconomy transition. The European Commission’s November 2025 bioeconomy strategy explicitly prioritizes bio-based alcohols, glycols, and esters as substitutes for fossil-derived materials, creating regulatory tailwinds for German producers. Evonik Industries and BASF SE have transitioned key oxygenated solvent lines to Product Carbon Footprint-certified tracks, enabling customers to quantify Scope 3 emission reductions and strengthening supplier differentiation in regulated markets.

Operationally, Germany is also adapting to energy volatility. Elevated natural gas price swings in 2025 accelerated electrification of methanol reforming processes, reducing exposure to fossil fuel shocks. Regulatory leadership under REACH has been decisive, with Germany spearheading restrictions on certain glyme solvents in 2025, forcing rapid substitution toward safer oxygenated alternatives such as bio-derived esters. Circular fashion integration has further elevated demand, as loopamid® technology embedded oxygenated solvents into nylon recycling supply chains serving global apparel brands, reinforcing Germany’s role as a premium compliance and innovation hub.

India – Domestic Capacity Build-Out and Methanol Economy Momentum

India’s oxygenated solvents industry is gaining structural depth through policy-driven capacity expansion and end-use diversification. A 2025 NITI Aayog report outlined ambitions to raise India’s share of the global chemicals value chain to 6% by 2030, with targeted incentives for domestic production of oxygenated intermediates such as ethylbenzene and cumene. Market pricing in mid-2025 followed a U-shaped recovery as pharmaceutical and textile demand rebounded under new Production Linked Incentive approvals, restoring utilization across solvent plants.

Fuel applications are an additional growth vector. The Methanol Institute of India confirmed achievement of 15% blending targets in 2025, structurally increasing demand for fuel-grade oxygenated alcohols. Infrastructure support is material, with USD 4.5 billion in federal investment directed toward specialized chemical parks in Gujarat during July 2025, explicitly designed to host high-purity solvent manufacturing. Together, these developments position India as both a consumption-driven market and an emerging regional production base.

South Africa – Value Chain Consolidation and Low-Carbon Reforming

South Africa’s oxygenated solvents landscape is being reshaped by strategic consolidation and emissions reduction. At its May 2025 Capital Markets Day, Sasol announced a reset of its International Chemicals business, prioritizing reinforcement of the Southern Africa value chain for oxygenated alcohols and ketones. This strategy is aligned with operational decarbonization, as Sasol confirmed commissioning of energy-efficient reformers aimed at cutting greenhouse gas emissions by 30% by 2030.

Looking ahead, feedstock innovation is central. Sasol is piloting green hydrogen integration into its Fischer–Tropsch process to produce low-carbon oxygenated waxes and solvents, a move that could reposition South Africa as a supplier of differentiated, lower-carbon oxygenated chemicals to global markets seeking emissions-aligned sourcing.

Comparative Snapshot – Oxygenated Solvents Industry by Country

Oxygenated Solvents Market County Level Snapshot

|

Country

|

Core Strategic Focus

|

Key Policy or Industry Lever

|

Competitive Position

|

|

China

|

Circular intermediates and ultra-pure IPA

|

Five-Year Plan and efficiency mandates

|

Scale plus technology upgrading

|

|

United States

|

Bio-solvents and CCS integration

|

RFS clarity and ASTM purity standards

|

Export-driven, carbon-managed supply

|

|

Germany

|

Bioeconomy and regulatory substitution

|

EU bioeconomy and REACH updates

|

Premium compliant solutions

|

|

India

|

Domestic capacity and methanol blending

|

PLI incentives and infrastructure spend

|

Emerging production and demand hub

|

|

South Africa

|

Value chain reset and green hydrogen

|

Corporate decarbonization roadmap

|

Niche low-carbon supplier

|

Oxygenated Solvents Market Report Scope

Oxygenated Solvents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$894.7 Million

|

|

Market Size (2034)

|

$1577 Million

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Product Type (Alcohols, Ketones, Esters, Glycols and Glycol Ethers, Bio-Based and Green Solvents), By Application (Paints and Coatings, Pharmaceuticals, Cleaning and Degreasing, Printing Inks, Adhesives and Sealants, Agrochemicals, Personal Care and Cosmetics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Dow, Exxon Mobil, Shell, Eastman Chemical, LyondellBasell Industries, Solvay, Sasol, Archer Daniels Midland, Arkema, OQ Chemicals, PETRONAS Chemicals Group, Mitsubishi Chemical Group, INEOS, Sinopec

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Oxygenated Solvents Market Segmentation

By Product Type

- Alcohols

- Ketones

- Esters

- Glycols and Glycol Ethers

- Bio-Based and Green Solvents

By Application

- Paints and Coatings

- Pharmaceuticals

- Cleaning and Degreasing

- Printing Inks

- Adhesives and Sealants

- Agrochemicals

- Personal Care and Cosmetics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Oxygenated Solvents Industry

- BASF

- Dow

- Exxon Mobil

- Shell

- Eastman Chemical

- LyondellBasell Industries

- Solvay

- Sasol

- Archer Daniels Midland

- Arkema

- OQ Chemicals

- PETRONAS Chemicals Group

- Mitsubishi Chemical Group

- INEOS

- Sinopec

*- List not Exhaustive