Coalescing Agents Market Outlook 2025–2034: $2 Billion to $3.2 Billion at 5.4% CAGR Driven by Low-VOC Coatings and Bio-Circular Feedstocks

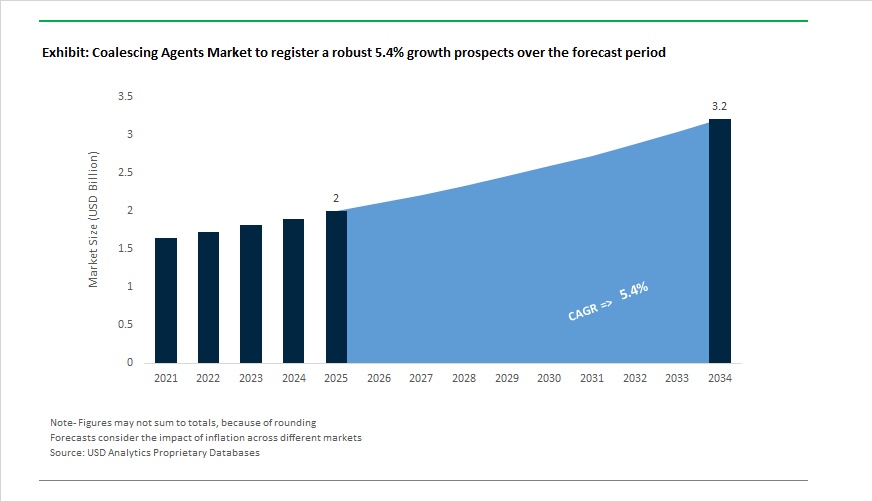

The global Coalescing Agents Market is projected to grow from $2 billion in 2025 to $3.2 billion by 2034, registering a CAGR of 5.4%. Demand is closely tied to the expansion of waterborne architectural coatings, low-VOC industrial paints, and sustainable packaging films. Coalescing agents remain critical in reducing minimum film-forming temperature (MFFT), improving film integrity, and ensuring crack-free performance in colder application environments. Regulatory pressure on volatile organic compounds (VOCs), semi-volatile organic compounds (SVOCs), and PFAS-based additives is accelerating reformulation across acrylic, vinyl acetate, and styrene-butadiene latex systems.

Innovation in low-emission and sustainable chemistry intensified in 2025–2026. In January 2025, Dow received the BIG Innovation Award for DALPAD™ A Plus, engineered to reduce SVOC emissions by more than 60% while maintaining high MFFT reduction efficiency. In September 2025, Dow introduced an alternative to fluoropolymer-based polymer processing aids, responding to global regulatory scrutiny of PFAS materials and supporting safer film-forming performance in packaging and coatings. Dow further strengthened its sustainability platform in October 2025 by expanding its ISCC PLUS-certified bio-circular portfolio at its Freeport, Texas facility, enabling certified sustainable intermediates for next-generation eco-friendly coalescing agents. In January 2026, Dow launched its Transform to Outperform strategy, emphasizing circular feedstock integration and accelerated sustainable product cycles for DALPAD™ and UCAR™ additive lines.

Portfolio restructuring and distribution realignment reshaped competitive positioning. In October 2025, BASF completed the sale of its decorative paints business to Sherwin-Williams, redirecting capital toward core Industrial Solutions and Chemicals segments that include high-performance coalescing technologies. Arkema announced in January 2026 that over 70% of its global coating facilities achieved ISCC PLUS certification, allowing bio-attributed coalescing agents with at least 20% lower product carbon footprint using mass-balance accounting. Evonik streamlined its North American distribution network in February 2026, appointing Dorset & Jackson, Palmer Holland, and Chem-Materials to improve market penetration and technical service support for waterborne and solvent-borne additives. In India, IMCD finalized the acquisition of business lines from CJ Shah and Company during November 2023–2024, strengthening specialty chemical distribution for the fast-growing paints and coatings sector.

Pricing dynamics and performance-driven innovation continued to influence the coalescing agents market structure. In March 2026, Eastman implemented price increases for esters and non-phthalate plasticizers, reflecting ongoing raw material and energy cost pressures that impact benchmark coalescing chemistries. Clariant reported in October 2025 that its Adsorbents & Additives unit achieved modest growth and strong pricing performance despite weak European demand, supported by performance improvement programs and sustainability positioning. Clariant also reported a 12% reduction in Scope 1 and 2 greenhouse gas emissions in the 12 months leading to September 2025, strengthening its branding around sustainability-focused additives. Earlier, in May 2023–2024, AkzoNobel introduced bisphenol-free internal beverage can coatings requiring specialized coalescing protocols to ensure pinhole-free barrier formation without endocrine-disrupting chemistries. These developments underscore steady mid-single-digit growth prospects for coalescing agents through 2034, supported by regulatory reformulation, carbon footprint reduction, and expanding waterborne coating adoption across architectural and industrial applications.

Coalescing Agents Market Trends and Drivers

Rapid Market Shift Toward Zero-VOC and Low-Odor Coalescing Agents Driven by Air-Quality Regulations

The coalescing agents market is undergoing a structural pivot as regulatory pressure, indoor-air-quality concerns, and ESG-aligned procurement policies force formulators to transition away from traditional volatile ester-alcohol coalescents.

As of January 2025, the U.S. EPA’s updated VOC emission standards for aerosol and architectural coatings introduced new compliance metrics reflecting VOC reactivity—not only weight—pushing manufacturers to re-engineer chemistry for compliance. Simultaneously, California SCAQMD Rule 1113 continues to define the global benchmark with sub-50 g/L VOC caps—a threshold now being mirrored by multiple Ozone Transport Commission (OTC) states, signaling emerging regulatory alignment across the U.S. market.

Industry innovation is responding at scale. In late 2024, BASF launched Loxanol® CA 5336, a zero-VOC, odor-free coalescing agent optimized for silk and semi-gloss paints, enabling premium-quality interior finishes that support LEED v4.1 certification pathways. During its Q3 2025 earnings call, Eastman outlined an additive-portfolio expansion under its innovation-driven growth model, emphasizing low-VOC intermediates outperforming legacy solvents on performance, odor, and end-user experience — signaling a future industry environment where VOC content becomes a procurement-critical KPI, not optional marketing value.

Hydrophobic Coalescing Chemistries Delivering Exterior Weatherability and Infrastructure-Grade Durability

As waterborne architectural coatings become the global standard, industry focus is widening from film-formation efficiency to weatherability, surfactant-leaching prevention, and corrosion protection. At the European Coatings Show (ECS) 2025, technical sessions highlighted the transition to water-insoluble coalescents engineered to embed directly within the polymer matrix, improving Early Water Resistance (EWR) such that exterior paint systems withstand rainfall within two hours of application—a critical differentiator in humid and monsoon-prone geographies.

Industrial-grade exterior coatings—especially those applied on bridges, ports, and public buildings—are increasingly specified to utilize hydrophobic coalescing aids that reduce water-vapor transmission rate (WVTR) and extend coating life cycles. This is strategically important as governments increasingly link

Bio-Based Coalescing Agents Supporting Scope-3 Carbon Reduction and Mass-Balance Sustainability

A major commercial value pool is emerging in bio-based coalescing agents that support renewable carbon content targets, ISCC-PLUS certification, and Scope-3 decarbonization strategies. In May 2025, Perstorp’s 2024 Sustainability Report documented a 30% YoY increase in Pro-Environment portfolio sales, driven by adoption of Pevalen™ Pro 100, a non-phthalate plasticizer/coalescent featuring 100% renewable carbon content with an 80% product-carbon-footprint (PCF) reduction versus fossil-based equivalents.

This shift is being reinforced by bio-feedstock innovation: Cargill, at ECS 2025, unveiled Agri-Pure™ bio-solvents and modified vegetable-oil coalescents allowing formulators to raise bio-renewable composition without compromising scrub-resistance or block-resistance, enabling waterborne systems to meet professional painter performance benchmarks.

Coalescing Systems Enabling Low-Temperature-Cure Industrial Coatings for Energy and Productivity Optimization

A second major growth vector lies in next-generation coalescing agents engineered for low-temperature curing by addressing energy-cost inflation and sustainability mandates in industrial coating lines.

During the 2025 Coatings & Adhesives Webinar Series, Clariant emphasized measurable lifecycle cost savings linked to low-temperature-curing coalescents and shifted its R&D focus toward additives with reduced melting points, enabling film hardening at ambient or near-ambient temperatures.

The automotive refinish sector is a leading adopter. Coalescents optimized for 2K waterborne polyurethane systems are enabling up to 25% energy reduction in body-shop curing cycles—while still supporting gloss retention, scratch resistance, and rapid hardness development required for premium-finish vehicle repairs.

Coalescing Agents Market Share and Segmentation Insights

Type Distribution: Hydrophobic Coalescents Lead as Low-VOC Formulations Reshape Product Selection

Hydrophobic coalescing agents command 55% of market share in 2025, driven by their effectiveness in lowering minimum film formation temperature (MFFT) and enabling durable latex film formation in architectural coatings across varied climates. Ester alcohols, TXIB, and benzyl alcohol remain preferred choices for exterior and interior paints requiring consistent performance under ambient curing conditions. Hydrophilic coalescing agents, including glycol ethers such as EB and DPnB, maintain steady demand in formulations favoring water solubility and simplified incorporation without high-shear mixing. Partially water-soluble coalescents are gaining traction as formulators seek balanced partitioning between aqueous and polymer phases, improving film integrity while minimizing water sensitivity and adhesion loss. Across all categories, tightening VOC regulations are reshaping product portfolios, accelerating adoption of low-VOC and non-VOC coalescing technologies in paints, adhesives, and inks.

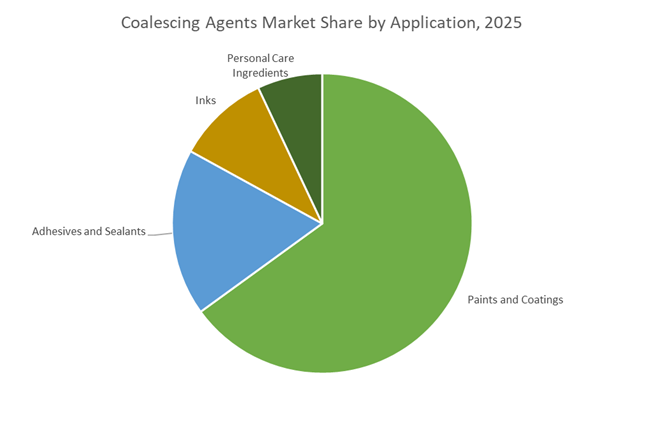

Application Breakdown: Paints and Coatings Anchor Consumption While Personal Care Emerges as a Growth Niche

Paints and coatings account for 65% of global coalescing agent demand, reflecting their essential role in forming continuous, washable films in decorative and protective latex coatings. In architectural applications, coalescents ensure proper particle fusion at room temperature, delivering durability, gloss, and stain resistance. Adhesives and sealants represent a significant secondary market, where coalescing agents enhance tack, peel strength, and cohesive bonding in products ranging from pressure-sensitive labels to construction adhesives. Printing inks, particularly flexographic and gravure systems, rely on coalescents to achieve uniform film formation, sharp image definition, and rub resistance on paper and flexible packaging substrates. Personal care is an emerging application area, with coalescing agents increasingly used in water-resistant sunscreens and long-wear cosmetics to improve film uniformity, adhesion, and performance longevity on skin and hair.

Competitive Landscape of the Coalescing Agents Market

The Coalescing Agents Market is led by specialty chemical majors and performance-additive innovators advancing low-VOC formulations, MFFT reduction technologies, and bio-based coalescents for architectural, industrial, and specialty coatings. Competitive differentiation centers on zero-VOC enhancers, AI-enabled formulation design, circular-economy additives, and regulatory-compliant solutions aligned with indoor air quality standards. Market leaders are expanding capacity in Asia and North America while accelerating Green Transformation initiatives, bio-based portfolios, and integrated dispersion systems to support high-durability, low-emission waterborne coatings across construction, infrastructure, and automotive applications.

Eastman sets the global benchmark with Texanol and zero-VOC Optifilm performance enhancers

Eastman Chemical Company dominates the global coalescing agents market through its industry-standard Texanol™ ester alcohol and the high-performance Optifilm™ range. Optifilm™ Enhancer 400, a zero-VOC and very low-odor coalescent, is increasingly used in premium architectural coatings and hypoallergenic paint systems addressing indoor air quality demand. Eastman’s strategic focus extends beyond traditional solvents, leveraging Oxo-technology licensing to deliver high-purity derivatives compliant with Green Label certifications in China and Europe. Its core strength lies in advanced Minimum Film-Forming Temperature reduction, enabling formulators to deploy high-glass-transition resins while maintaining low emissions and superior film integrity.

BASF accelerates low-VOC coatings growth through AI-driven ZeroPCF dispersion systems

BASF integrates coalescing agents within its Dispersions and Resins platform, supplying specialized additives for high-performance architectural and industrial coatings. In February 2026, BASF expanded its Mangalore, India facility with a new dispersions line to meet surging South Asian demand for low-VOC paints. With 2024 sales of €65.3 billion, BASF’s Surface Technologies segment anchors its Green Transformation strategy for 2026 to 2030. Under Winning Ways, the company is embedding AI into formulation workflows while advancing ZeroPCF chemicals. BASF also delivers one-stop solutions, pre-matching coalescents with Acronal® and Basonal® dispersions to enhance scuff and stain resistance.

Dow advances low-odor DALPAD systems for waterborne coatings and infrastructure demand

Dow is a major force in waterborne coatings, led by its DALPAD™ platform, including DALPAD™ A PLUS, a flagship low-odor, non-VOC coalescent meeting strict A+ French emission standards. In January 2026, Dow launched its Transform to Outperform initiative targeting a USD 2 billion EBITDA uplift by 2028 through simplification and AI-driven customer engagement. Recent innovations include coalescents that improve water-whitening resistance in acrylic emulsions for exterior durability. Dow is also expanding production of performance glycol ethers in North America to support infrastructure-driven coatings demand tied to the USD 1 trillion US physical upgrade program.

Evonik pivots to specialty coalescents with biosurfactants and circular coatings solutions

Evonik is shifting decisively toward high-margin specialty additives, supporting advanced coating systems with complementary wetting agents and biosurfactants. In 2026, Evonik streamlined its US and Canada distribution model, appointing exclusive partners to strengthen regional technical support. The company showcased TEGO® Wet 288 and sophorolipid-based TEGO® XP 32156 to enhance substrate wetting alongside its coalescent portfolio. Guided by its Leading Beyond Chemistry strategy, Evonik prioritizes circular economy additives that improve recyclability of coated substrates. It also dominates specialty inks and radiation-curable coatings, where rapid film formation and surface tension reduction are mission-critical.

Synthomer expands bio-based coalescing agents for high-growth Asian construction markets

Synthomer supplies aqueous polymer solutions and specialized coalescing agents for functional coatings and adhesives. In February 2026, the company released its Global Strategic Business Report highlighting growth opportunities across Asian construction and automotive sectors. Synthomer offers tailored hydrophilic and hydrophobic coalescents that replace solvent-heavy systems, supported by Enhanced Performance Products designed to improve scrub resistance and early hardness development. Strategically, Synthomer is scaling its bio-based coalescing portfolio, projected to grow at a 7.82% CAGR through 2032, driven by rising demand for sustainable interior wall paints and low-emission industrial finishes.

Elementis advances levulinic-acid coalescents for premium architectural and marine coatings

Elementis is a leader in rheology modifiers and bio-based additives, strengthening its coalescing portfolio through an exclusive partnership with NXTLEVVEL Biochem to commercialize levulinic-acid-derived coalescents. Founded in 1844, Elementis leverages high-purity hectorite-based additives that work synergistically with coalescents to optimize coating stability. Recent innovations include specialized marine coalescents maintaining film integrity under high salinity and temperature variability. Elementis focuses on high-end architectural coatings and personal care applications, where natural origin, safety profiles, and performance consistency are primary purchasing criteria.

United States: Regulatory Recalibration Driving Low-SVOC and Bio-Attributed Coalescents

The United States coalescing agents industry is undergoing a decisive transition shaped by regulatory tightening, green chemistry investments, and application-specific performance demands. A key inflection point emerged in January 2025 when Dow received a BIG Innovation Award for its DALPAD A Plus coalescing agent. This next-generation additive delivers a greater than 60% reduction in semi-volatile organic compound emissions in waterborne coatings, directly addressing indoor air quality concerns while maintaining film formation efficiency. The launch coincided with a critical regulatory shift. On January 17, 2025, the U.S. Environmental Protection Agency finalized amendments to the National Volatile Organic Compound Emission Standards, introducing updated product-weighted reactivity limits for coatings. These revisions are reshaping formulation strategies by prioritizing high-efficiency coalescents that minimize ozone formation potential rather than relying solely on traditional VOC metrics.

Manufacturing resilience and sustainability credentials are reinforcing this transition. Eastman Chemical Company implemented strategic pricing adjustments in April 2025 for its Optifilm Enhancer portfolio to offset raw material volatility while sustaining domestic production capacity for high-performance architectural coatings. In parallel, Dow’s acrylate facility in Deer Park, Texas, achieved ISCC PLUS certification in 2025, enabling mass-balance production of bio-attributed feedstocks for sustainable coalescing agent formulations. Capital investment trends further underscore the shift. Publicly listed specialty chemical firms in the United States reported a combined $240 million in 2025 capital expenditure dedicated to green chemistry pilot plants, with waterborne coating additives identified as a priority focus area. Demand-side dynamics are also evolving. Rising electric vehicle production is driving the use of specialized coalescents that ensure film integrity in thin-layer, high-durability automotive primers, expanding the role of advanced coalescing agents beyond architectural coatings.

China: Mandatory Standards Accelerating Zero-VOC and Localized Supply Chains

China’s coalescing agents market is being transformed by mandatory national standards, localized production mandates, and accelerated adoption of zero-VOC technologies. On May 30, 2025, the State Administration for Market Regulation released GB 30981.1-2025 and GB 30981.2-2025, introducing more granular limits on hazardous substances in architectural and industrial coatings, with enforcement scheduled for June 2026. These standards are compelling domestic paint manufacturers to reformulate aggressively, driving a measurable shift toward high-performance coalescing agents with reduced environmental and health impacts.

Technology investment is supporting compliance at scale. In November 2025, BASF commissioned a high-performance dispersant and additive production line in Nanjing, leveraging Controlled Free Radical Polymerization to manufacture advanced coalescents with lower product carbon footprints. The strategic location within the Jiangbei New Material Technology Park, designated in late 2025 as a core Asia-Pacific specialty additives hub, is strengthening regional supply reliability and accelerating the green transformation of China’s industrial coatings sector. Regulatory enforcement under the Made in China 2025 framework has intensified. The Ministry of Ecology and Environment reported a marked increase in VOC inspections across provinces in 2025, contributing to a year-on-year rise in the adoption of zero-VOC coalescing agents by domestic manufacturers. These developments are particularly significant for automotive coatings, where localized production from the Nanjing facility is reducing dependence on imported high-end film-forming aids.

Germany: Circular Chemistry and Compliance-Driven Formulation Innovation

Germany’s coalescing agents industry is evolving within a highly regulated environment that prioritizes circularity, substance safety, and formulation simplification. At the K Show 2025 in Düsseldorf, German chemical leaders highlighted bio-based UV-oligomers and biodegradable opacifier dispersions designed to replace persistent acrylate-based components in industrial coatings. These innovations reflect a broader shift toward circular economy-aligned additive systems that reduce long-term environmental persistence.

Material integration strategies are also changing. LANXESS expanded its Scopeblue label in March 2025, introducing iron oxide pigments with a substantially lower carbon footprint for use in premium coatings formulated alongside eco-compatible coalescing agents. At the European Coatings Show 2025, LANXESS launched Klarix XIT, a non-biocidal additive enabling the production of biocide-free coatings, thereby reducing formulation complexity in film formation systems. Regulatory compliance remains a powerful driver. German formulators transitioned to bisphenol-free internal can coatings in 2025 in response to EU REACH requirements. This shift has increased reliance on high-purity coalescents capable of maintaining flexibility and adhesion without restricted endocrine-active substances, reinforcing Germany’s role as a testbed for compliance-driven additive innovation.

India: Infrastructure-Led Paint Demand and Bio-Content Adoption

India’s coalescing agents market is expanding through a combination of infrastructure stimulus, distribution consolidation, and export-oriented specialty chemical manufacturing. In late 2024, IMCD India acquired the specialty chemical business lines of CJ Shah and Company, strengthening nationwide distribution of advanced coalescing agents to serve the rapidly growing construction and architectural coatings segments. This consolidation has improved access to global-grade additives across regional paint manufacturing hubs.

Production and export capabilities are scaling in parallel. hubergroup Chemicals inaugurated expanded facilities in India in 2025, focusing on customized manufacturing of UV-curable oligomers and specialty additives for global markets. Demand fundamentals are being reinforced by public infrastructure programs. The Indian government’s Smart Cities mission contributed to a notable rise in water-based architectural paint consumption during 2025, increasing the requirement for hydrophilic coalescing agents that perform reliably under diverse climatic conditions. Sustainability considerations are also gaining traction. hubergroup Chemicals reported strong market interest in sugar alcohol-based UV-oligomers with bio-based content approaching 70 %, particularly for sustainable packaging applications. These trends position India as both a high-growth consumption market and an emerging export hub for next-generation coalescing agents.

Comparative Summary: Country-Level Strategic Direction in the Coalescing Agents Industry

Coalescing Agents Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Key Application Focus

|

Direction of Coalescing Agent Innovation

|

|

United States

|

VOC reactivity limits and green chemistry CAPEX

|

Architectural and automotive coatings

|

Low-SVOC, bio-attributed, high-efficiency coalescents

|

|

China

|

Mandatory hazardous substance standards

|

Industrial and automotive coatings

|

Zero-VOC, locally produced advanced coalescents

|

|

Germany

|

EU REACH compliance and circular economy

|

Industrial and packaging coatings

|

Biocide-free, biodegradable, high-purity additives

|

|

India

|

Infrastructure expansion and export manufacturing

|

Architectural paints and packaging

|

Hydrophilic, high bio-content coalescing agents

|

Coalescing Agents Market Report Scope

Coalescing Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2034)

|

$3.2 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Type (Hydrophilic Coalescing Agents, Hydrophobic Coalescing Agents, Partially Water-Soluble Coalescing Agents), By Chemistry (Esters, Glycol Ethers, Alcohols and Diols, Ketones and Others), By Application (Paints and Coatings, Adhesives and Sealants, Inks, Personal Care Ingredients), By Functionality (Low-VOC and Zero-VOC Agents, Low-Odor Agents, Bio-based and Renewable Coalescents)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Eastman Chemical Company, Arkema S.A., Evonik Industries AG, Elementis Plc, Celanese Corporation, Synthomer Plc, Croda International Plc, Clariant AG, LANXESS AG, Syensqo SA, Akzo Nobel N.V., Stepan Company, Hubergroup Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coalescing Agents Market Segmentation

By Type

- Hydrophilic Coalescing Agents

- Hydrophobic Coalescing Agents

- Partially Water-Soluble Coalescing Agents

By Chemistry

- Esters

- Glycol Ethers

- Alcohols and Diols

- Ketones and Others

By Application

- Paints and Coatings

- Adhesives and Sealants

- Inks

- Personal Care Ingredients

By Functionality

- Low-VOC and Zero-VOC Agents

- Low-Odor Agents

- Bio-based and Renewable Coalescents

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Coalescing Agents Industry

- BASF SE

- Dow Inc.

- Eastman Chemical Company

- Arkema S.A.

- Evonik Industries AG

- Elementis Plc

- Celanese Corporation

- Synthomer Plc

- Croda International Plc

- Clariant AG

- LANXESS AG

- Syensqo SA

- Akzo Nobel N.V.

- Stepan Company

- Hubergroup Chemicals

*- List not Exhaustive