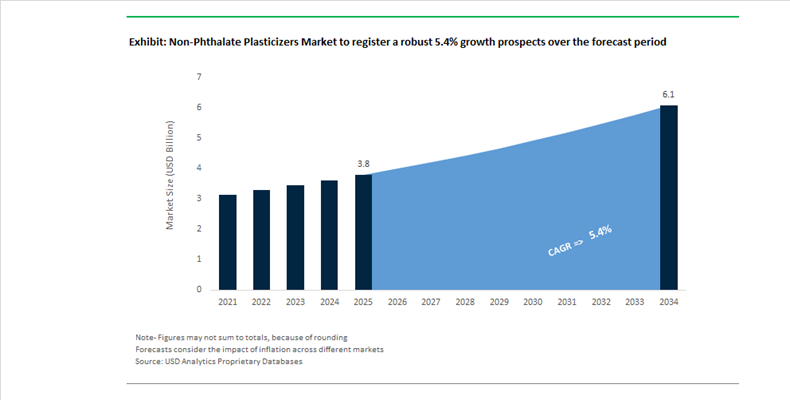

Non-Phthalate Plasticizers Market Valued at $3.8 Billion in 2025, Projected to Reach $6.1 Billion by 2034 at 5.4% CAGR Amid Regulatory Phase-Out of DEHP

The Non Phthalate Plasticizers Market is valued at $3.8 billion in 2025 and is forecast to reach $6.1 billion by 2034, registering a CAGR of 5.4%. Market acceleration is directly linked to global regulatory restrictions on phthalates such as DEHP, DINP, and DBP across medical devices, food-contact materials, toys, flooring, and flexible PVC applications. Demand is concentrated in high-purity DOTP (dioctyl terephthalate), DINCH (diisononyl cyclohexane-1,2-dicarboxylate), bio-based plasticizers, and biomass-balanced formulations that meet REACH, FDA, and California Proposition 65 compliance standards. Medical-grade tubing, IV bags, automotive interiors, coated fabrics, and wire & cable insulation are transitioning rapidly toward phthalate-free alternatives to mitigate reproductive toxicity and endocrine disruption risks.

In January 2024, Perstorp launched Pevalen™ Pro 100, the first plasticizer made entirely from 100% renewable carbon using a mass-balance approach, delivering an 80% lower carbon footprint for PVC flooring and coated fabrics. In September 2024, California passed Assembly Bill 2300 banning DEHP in IV bags by 2030 and tubing by 2035, triggering immediate validation programs for DINCH and DOTP in North America. In October 2024, Evonik Industries expanded production of ELATUR® CH (DINCH) and ELATUR® DINCD at its Marl facility to address procurement security in medical and toy sectors. During the second half of 2024, Eastman Chemical Company announced a $100 million expansion to increase output of Eastman 168™ (DOTP), reinforcing its leadership in general-purpose PVC replacement chemistry.

Capacity expansion and sustainability positioning intensified through 2025. BASF SE completed the doubling of Hexamoll® DINCH capacity at Ludwigshafen, increasing output from 100,000 to 200,000 metric tons annually to meet global medical and food-contact demand. In February 2025, BASF introduced ISCC PLUS-certified Ccycled® and biomass-balanced grades of Palatinol® DOTP Advantage 50 in North America, produced at Pasadena, Texas and Cornwall, Ontario, enabling certified recycled and renewable feedstock integration without process modification. In May 2025, BASF launched Pluriol® A 2400 I in Europe, an isoprenol-PEG intermediate supporting third-generation phthalate-free superplasticizers in construction chemicals. In October 2025, Bhageria Industries commenced commercial production of new plasticizers and ethoxylates in Maharashtra to capture India’s rising domestic demand for phthalate-free PVC additives.

Regulatory momentum solidified long-term structural demand. In early 2025, the European Union extended the REACH deadline for DEHP phase-out in medical devices to July 2030, reinforcing irreversible migration toward non-phthalate solutions while providing transition flexibility. During 2024 and 2025, Lanxess AG transitioned Mesamoll® to carbon-reduced raw materials, achieving a 20% lower product carbon footprint while maintaining high saponification resistance for sealants and waterbeds. In late 2024, ExxonMobil committed over $200 million to advanced recycling capacity in Texas, targeting 1 billion pounds annually by 2026 to supply certified circular feedstocks for next-generation plasticizers.

Non-Phthalate Plasticizers Market Trends and Opportunities

Trend: Mandatory Phase-Out of Legacy Phthalates in Consumer Goods and Food-Contact Applications

The non-phthalate plasticizers market has entered a non-discretionary growth phase as global regulators tighten enforcement against legacy phthalates such as DEHP and DINP. Compliance pressure is no longer limited to Europe but is rapidly converging across North America and Asia, forcing consumer goods manufacturers to execute large-scale reformulations. In the United States, the enforcement landscape shifted materially with California’s updated Proposition 65 framework. Effective January 1, 2025, the revised short-form warning rules require manufacturers to explicitly name at least one chemical of concern. In 2024 alone, phthalates accounted for nearly 19% of all 60-day Prop 65 violation notices, significantly elevating litigation exposure for vinyl toys, childcare articles, and household products. As a result, achieving “phthalate-free” status below 0.1% by weight has become a strategic necessity rather than a marketing choice.

In Europe, regulatory scrutiny has escalated further with the publication of the EU Toy Safety Regulation 2025/2509 in December 2025. The regulation introduces a mandatory Digital Product Passport, requiring importers and manufacturers to maintain a digital audit trail proving the absence of endocrine-disrupting phthalates. This effectively blocks non-compliant products at EU borders, reshaping global supply chains and accelerating the substitution of phthalates with non-phthalate esters such as DOTP, DINCH, and trimellitates. Parallel momentum is emerging in Asia. In October 2025, the Food Safety and Standards Authority of India issued a draft notification targeting both Bisphenol A elimination and stricter phthalate migration limits in food-contact materials. This alignment with European migration standards transforms India into a major demand center for non-phthalate plasticizers, creating a structural volume shift across packaging, consumer goods, and flexible PVC applications.

Trend: High-Performance Trimellitates and Polymeric Plasticizers for the EV Ecosystem

Electrification is redefining performance requirements for plasticizers, positioning high-molecular-weight non-phthalate chemistries as essential materials for the automotive value chain. Electric vehicles operate under significantly higher thermal and electrical stress compared to internal combustion platforms, particularly with the adoption of 800-volt architectures and densely packed battery modules. This has driven rapid adoption of Trioctyl Trimellitate and polymeric plasticizers, which offer superior heat stability, ultra-low volatility, and exceptional migration resistance. Industry data indicates that TOTM consumption in automotive wiring harnesses and sealing systems grew by 17% year-on-year in 2024, reflecting its ability to withstand continuous operating temperatures of up to 150°C while maintaining a migration rate as low as 0.1 percent over 24 hours.

Interior air quality has become an equally critical specification. Automotive OEMs are increasingly mandating high-purity TOTM grades exceeding 99.5% purity for dashboards, door panels, and interior trims to mitigate windshield fogging caused by plasticizer volatilization. This requirement has shifted demand toward premium-grade trimellitates, particularly among high-end and electric vehicle manufacturers. To support this structural demand, Asian producers have expanded capacity aggressively. Between 2023 and 2024, South Korea alone added approximately 12,000 metric tons of trimellitate capacity, strategically positioned to supply battery-electric vehicle manufacturing hubs across China and Northeast Asia. These investments signal a long-term repositioning of non-phthalate plasticizers from compliance-driven substitutes to performance-critical automotive materials.

Opportunity: Bio-Based Plasticizers and Renewable Feedstock Integration

Bio-based plasticizers represent one of the most attractive growth avenues within the non-phthalate plasticizers market, particularly as consumer-facing brands commit to fossil-carbon reduction targets. Epoxidized Soybean Oil has already transitioned from a secondary stabilizer to a primary plasticizer in food-contact PVC applications. ESBO is now widely used in gasket linings for glass jar closures, supported by regulatory clearances from both the FDA and EFSA. Its ability to deliver phthalate-free flexibility while maintaining seal integrity has positioned ESBO as the default solution for condiments, baby food, and infant nutrition packaging.

Beyond agricultural feedstocks, innovation is accelerating toward non-food renewable sources. In 2025, algae-derived plasticizers such as AlgX entered early commercial deployment, offering bio-content exceeding 80% without competing with edible oil supply chains. These materials provide a compelling sustainability profile for brands pursuing circular economy narratives. The healthcare sector is also emerging as a key adopter. Hospitals are rapidly transitioning away from DEHP-containing medical devices, particularly in neonatal and critical care. Manufacturers such as B. Braun Medical have commercialized DEHP-free intravenous systems utilizing bio-based plasticizers like acetyl tributyl citrate, which deliver improved biocompatibility and reduced patient exposure risk. This convergence of food safety, healthcare standards, and sustainability commitments is elevating bio-based plasticizers into core formulation components.

Opportunity: Ultra-Low Migration Plasticizers for Medical and Food-Grade PVC

The highest-value segment of the non-phthalate plasticizers market lies in ultra-low migration solutions engineered for medical and food-contact applications. In these environments, chemical leaching is not only a regulatory issue but a direct patient and consumer safety concern. Superior-grade TOTM has emerged as a benchmark material in this segment, with global usage in medical devices surpassing 14,000 metric tons in 2024. These grades are defined by residual phthalate levels below 0.05 percent and are increasingly specified for dialysis tubing, blood bags, and intravenous lines.

Scientific validation is reinforcing this opportunity. Migration modeling studies published in late 2025 demonstrated that advanced non-phthalate systems such as DINCH and ATBC can achieve migration levels well below established Specific Migration Limits, even under high-temperature sterilization conditions. This performance is critical for food-grade cling films and medical disposables subjected to repeated thermal cycles. A further layer of innovation is emerging through functional plasticizers. In 2025, research teams demonstrated zinc-based adipate plasticizers capable of delivering both mechanical flexibility and intrinsic biocidal activity. These materials inhibit bacterial growth on PVC surfaces, opening a premium niche for hospital interiors and food processing environments where hygiene and material longevity are equally critical.

Non-Phthalate Plasticizers Market Share and Segmentation Insights

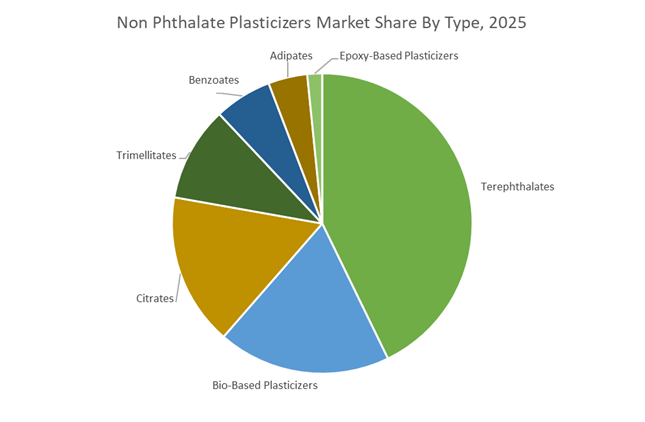

Terephthalates Lead Non-Phthalate Plasticizer Market with DOTP Dominance in PVC Applications

Terephthalates accounted for 42.80% of the Non-Phthalate Plasticizers Market by type in 2025, driven by strong adoption of DEHT or DOTP as the primary replacement for traditional phthalate plasticizers in flexible PVC applications. These plasticizers offer high compatibility, low volatility, and strong low-temperature performance, making them suitable for flooring, wall coverings, films, and coated fabrics. Their regulatory acceptance and cost effectiveness support large scale industrial use. Terephthalates are widely used across construction materials and consumer products requiring flexible PVC formulations. In 2025, DOTP capacity expansions are supporting global demand growth, with manufacturers scaling production to meet regulatory driven substitution trends across major markets.

Building and Construction Sector Drives Demand for Non-Phthalate Plasticizers in PVC Materials

Building and construction accounted for 42.80% of the Non-Phthalate Plasticizers Market by end-use industry in 2025, reflecting the extensive use of plasticized PVC in flooring, wall coverings, roofing membranes, pipes, and insulation materials. Regulatory restrictions on phthalates and increasing adoption of green building standards are accelerating the shift toward safer plasticizer alternatives. Construction materials require durable, flexible, and compliant formulations that meet environmental and safety standards. In 2025, evolving global building codes are reinforcing non-phthalate adoption, with manufacturers reformulating PVC products to comply with stricter indoor air quality and material safety regulations across residential and commercial infrastructure projects.

Non-Phthalate Plasticizers Market Competitive Landscape

The non-phthalate plasticizers market in 2026 is driven by regulatory substitution, renewable feedstock adoption, and performance parity in high-temperature and medical-grade PVC applications. Competitive advantage centers on bio-based plasticizers, carbon footprint reduction, and localized production to address pricing volatility and supply chain resilience.

BASF advances biomass-balanced plasticizers with carbon transparency and infrastructure-grade stabilizer integration

BASF is strengthening its leadership through its VALERAS® platform, focusing on sustainable non-phthalate plasticizers with verified carbon reduction. Its BMBcert™ solutions enable replacement of fossil feedstocks with renewable inputs, reducing product carbon footprint by up to 60% without reformulation. The company implemented a global price increase of up to 20% in 2026 to offset raw material and logistics costs. Expansion of Irgastab® Cable KV 10 supports high-voltage cable applications requiring thermal stability and insulation performance. BASF’s Tinuvin® NOR® 211 AR enhances durability in agricultural films, extending lifecycle performance. Its integrated approach combines sustainability, regulatory compliance, and high-performance additives.

Eastman scales circular plasticizers with Renew technology and strong DOTP market positioning

Eastman Chemical is a key innovator in non-phthalate plasticizers through its molecular recycling-based Renew platform. Its Eastman 168™ Renew 20 incorporates 20% certified recycled content, providing a drop-in solution for medical, flooring, and wall covering applications. The company implemented a USD 0.05/lb price increase in 2026, reflecting strong demand and cost pressures. With US$8.8 billion in 2025 revenue, Eastman continues to expand DOTP production at its Kingsport facility to serve North American construction markets. Its DOA Renew series offers superior low-temperature flexibility for food-contact applications. This circular economy-driven strategy reinforces Eastman’s leadership in sustainable plasticizers.

Evonik expands ELATUR® portfolio with specialty non-phthalate plasticizers for sensitive consumer applications

Evonik is focusing on high-performance, specialty non-phthalate plasticizers under its Advanced Technologies strategy. Its ELATUR® DINCD offers low volatility, excellent migration resistance, and superior processing characteristics for vinyl flooring, toys, and consumer goods. The company targets €1.7–2.0 billion EBITDA in 2026, supported by strong performance in its Custom Solutions segment. Distribution optimization in North America enhances technical service and market penetration. Evonik is integrating surfactant and additive expertise to improve compatibility of plasticizers in complex rubber formulations. This system-based approach strengthens its presence in high-margin specialty applications.

LANXESS optimizes specialty additives portfolio with low-VOC plasticizers and cost-efficiency initiatives

LANXESS is strengthening its non-phthalate plasticizer portfolio through its FORWARD! restructuring program, targeting €250 million in total cost savings by 2026. Its Mesamoll® product line is being enhanced with Klarix XIT technology to enable biocide-free, ultra-clean formulations. The company is focusing on adhesives, sealants, and coatings requiring low-VOC performance for indoor applications. Despite market pressures, its Specialty Additives segment generated €505 million in Q3 2025 sales. LANXESS is optimizing production networks to improve efficiency and competitiveness against low-cost imports. This focus on sustainability and cost control supports long-term market positioning.

ExxonMobil integrates advanced recycling and feedstock control to deliver high-purity non-phthalate plasticizer solutions

ExxonMobil is leveraging its large-scale refining and recycling infrastructure to strengthen its position in non-phthalate plasticizers. Its Baytown facility has processed over 80 million pounds of plastic waste, converting 90% into reusable feedstock for oxo-alcohol and plasticizer production. The company is advancing R&D in non-phthalate alternatives such as Jayflex™ L11P for wire and cable applications. Its Vistamaxx™ polymers enhance compatibility in recycled PVC systems, maintaining mechanical performance. Vertical integration across 2-EH and isononyl alcohol ensures stable supply amid global disruptions. ExxonMobil’s scale and circular feedstock strategy provide a strong competitive advantage in industrial-grade plasticizers.

United States: Certified Circularity and EV-Linked Formulation Depth

The United States non-phthalate plasticizers landscape is being reshaped by certified circular inputs and downstream demand from regulated applications. In February 2025, BASF expanded its ISCC PLUS portfolio from Pasadena, Texas, launching biomass-balanced and Ccycled® versions of Palatinol® DOTP Advantage 50. This move enables North American converters to adopt drop-in DOTP solutions with materially lower carbon footprints while preserving processing parity with legacy plasticizers. Regulatory stability further supports adoption. The U.S. FDA reinforced food-contact clearances for DOTP through 2025, accelerating substitution away from ortho-phthalates in food packaging films and medical tubing where compliance certainty is decisive for long qualification cycles.

Cost and performance dynamics are also tightening supplier discipline. In March 2025, Eastman Chemical Company implemented price adjustments for Eastman 168™ and DOA to offset volatility in 2-ethylhexanol feedstocks, signaling a shift toward value-based pricing for specialty esters. By December 2025, Eastman extended non-phthalate plasticizer utility into advanced EV interlayers, improving acoustic damping and glass integrity in lightweight automotive glazing. Looking ahead, BASF’s 2026 start-up of 3D-printed catalyst production in Ludwigshafen is set to raise esterification efficiency and purity for non-phthalate grades serving U.S. markets, reinforcing supply reliability and quality consistency.

China: DOTP Scale Leadership and Feedstock Integration

China has consolidated its role as the global manufacturing center for non-phthalate plasticizers, with Dioctyl Terephthalate entrenched as the default export-oriented alternative. By late 2025, domestic DOTP capacity leadership was reinforced by flexible operating-rate management across DOP, DOTP, and DINP to track swings in 2-ethylhexanol costs. This operating model prioritizes margin protection and inventory discipline while sustaining export commitments to consumer goods and wire and tellurium cable applications.

Structural integration is deepening. BASF commenced commercial operations at its loopamid facility in Caojing in early 2025. Although targeted at PA6, the site’s chemical recycling infrastructure establishes a template for circular recovery of plasticizer-rich textile waste, informing future non-phthalate loops. In parallel, SABIC’s Fujian petrochemical complex is progressing toward 2026 milestones with integrated ethylene oxide capacity, securing upstream feedstocks for non-phthalate derivatives used in high-end industrial coatings and specialty PVC formulations.

Germany: Circular Plastics and Reactive Alternatives

Germany’s non-phthalate plasticizers trajectory is anchored in circularity and migration-resistant chemistries. At K 2025 in Düsseldorf, Evonik advanced its Next Markets Program, emphasizing impurity removal from pyrolysis oil to enable production of high-quality non-phthalate plasticizers derived from plastic waste. This capability directly addresses EU sustainability thresholds while maintaining performance requirements for demanding polymer systems.

Complementing circular feedstocks, LANXESS highlighted Levagard® 2100, a low-viscosity reactive phosphonate that integrates into PUR and PIR matrices, delivering non-migrating plasticization without phthalates. LANXESS also expanded its Scopeblue™ labeling in 2025, designating products with at least 50% sustainable raw materials or a 50 percent lower carbon footprint. Process reliability was further improved with the March 2025 introduction of Preventol® OX, a chlorine-free disinfectant that reduces interference risks in sensitive non-phthalate esterification units.

European Union: Regulation-Driven Substitution Momentum

At the regional level, EU policy is accelerating structural substitution toward non-phthalate systems. New rules effective December 16, 2025 to prevent microplastic pollution from plastic pellets impose risk-management obligations across the supply chain for entities handling more than five tonnes annually. This elevates compliance costs for legacy additives and favors standardized, traceable non-phthalate plasticizers. Concurrently, the European Commission initiated consultations in November 2025 for a proposed ban on Medium-Chain Chlorinated Paraffins under the POP Regulation, with adoption targeted for Q2 2026. The prospective restriction is catalyzing demand for trimellitates and adipates as functional replacements in cables, sealants, and flexible PVC.

Distribution strategies are adapting to fragmented demand. BASF renewed its partnership with Häffner GmbH in 2025 to efficiently serve sub-20-tonne orders across SMEs, ensuring regulatory-compliant access to non-phthalate grades in decentralized European markets.

India: Infrastructure Pull and Domestic Capacity Utilization

India is emerging as a priority growth node for non-phthalate plasticizers, driven by flooring, wall coverings, and medical device demand linked to the 2025–2026 National Infrastructure Pipeline. Non-phthalate PVC systems are increasingly specified in public projects and commercial real estate where durability and health considerations are paramount. The KLJ Group has maintained high utilization across integrated assets to meet rising domestic requirements for phthalate-free consumer electronics and healthcare applications, positioning India to reduce import reliance while scaling compliant formulations.

Summary Table: Non-Phthalate Plasticizers – Country-Level Strategic Positioning

Non-Phthalate Plasticizers Market County Level Snapshot

|

Geography

|

Strategic Focus

|

Key Developments

|

Structural Impact

|

|

United States

|

Certified circular inputs and EV applications

|

ISCC PLUS DOTP, FDA clearances, EV interlayers

|

Faster substitution and premiumization

|

|

China

|

DOTP scale and feedstock integration

|

Operating-rate flexibility, EO integration

|

Cost leadership and export reliability

|

|

Germany

|

Circular plastics and reactive alternatives

|

Pyrolysis purification, Levagard® 2100

|

Low migration and EU compliance

|

|

European Union

|

Regulation-driven substitution

|

Microplastic rules, MCCP consultations

|

Accelerated demand for non-phthalates

|

|

India

|

Infrastructure-led demand

|

High utilization by domestic leaders

|

Import substitution and domestic scale

|

Non-Phthalate Plasticizers Market Report Scope

Non-Phthalate Plasticizers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.8 Billion

|

|

Market Size (2034)

|

$6.1 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Type (Terephthalates, Adipates, Trimellitates, Benzoates, Epoxy-Based Plasticizers, Citrates, Bio-Based Plasticizers), By Application (Flooring and Wall Coverings, Wires and Cables, Films and Sheets, Coated Fabrics, Consumer Goods, Medical Devices), By End-Use Industry (Building and Construction, Automotive and Transportation, Healthcare and Pharmaceuticals, Food and Beverage Packaging, Electrical and Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Eastman Chemical, ExxonMobil, Evonik Industries, LANXESS, Perstorp, KLJ Group, LG Chem, Nan Ya Plastics, DIC, Mitsubishi Chemical, UPC Technology, Polynt, Valtris Specialty Chemicals, Aekyung Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Non-Phthalate Plasticizers Market Segmentation

By Type

- Terephthalates

- Adipates

- Trimellitates

- Benzoates

- Epoxy-Based Plasticizers

- Citrates

- Bio-Based Plasticizers

By Application

- Flooring and Wall Coverings

- Wires and Cables

- Films and Sheets

- Coated Fabrics

- Consumer Goods

- Medical Devices

By End-Use Industry

- Building and Construction

- Automotive and Transportation

- Healthcare and Pharmaceuticals

- Food and Beverage Packaging

- Electrical and Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Non Phthalate Plasticizers Market

- BASF

- Eastman Chemical

- ExxonMobil

- Evonik Industries

- LANXESS

- Perstorp

- KLJ Group

- LG Chem

- Nan Ya Plastics

- DIC

- Mitsubishi Chemical

- UPC Technology

- Polynt

- Valtris Specialty Chemicals

- Aekyung Chemical

*- List not Exhaustive