Dioctyl Terephthalate Market to Reach $4.7 Billion by 2034 at 6.9% CAGR Amid Bio-Based Plasticizer Adoption and Flexible PVC Dominance

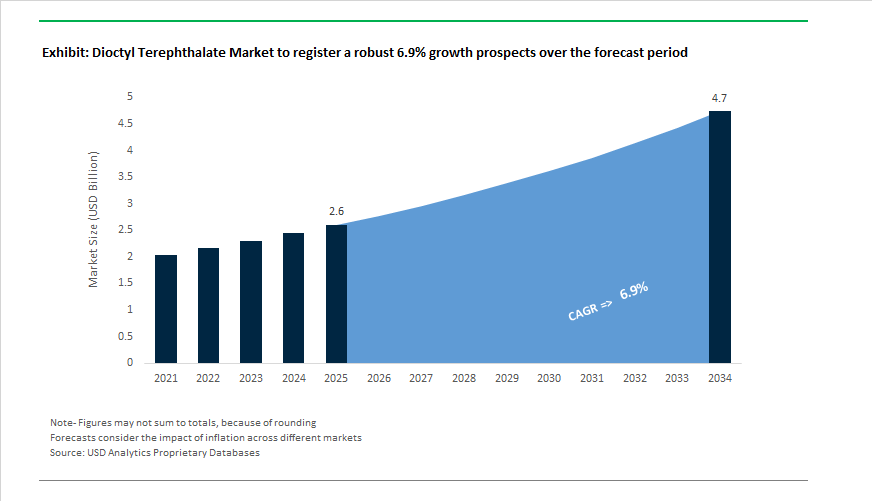

The Dioctyl Terephthalate (DOTP) Market is projected to grow from $2.6 billion in 2025 to $4.7 billion by 2034, registering a CAGR of 6.9%. Growth momentum is driven by the accelerated replacement of ortho-phthalates in flexible PVC applications, tightening EU and U.S. regulatory frameworks, and the rapid penetration of biomass-balanced plasticizers in automotive interiors, flooring, wire and cable, and medical-grade polymers. By the end of 2024, verified trade data confirmed that DOTP accounted for 38.7% of global flexible PVC demand, reflecting its structural displacement of legacy phthalate plasticizers. Automotive interiors represented 28.5% of total DOTP consumption, while construction and flooring accounted for 29.4%, underscoring the chemical’s integration into durability-driven, low-migration polymer systems.

Supply-side expansion and sustainability integration reshaped the competitive landscape through 2024 and 2025. In late 2024, new production capacity additions in China increased global DOTP supply by 11.7% year-over-year, intensifying price competition and accelerating the shift toward high-purity automotive and medical grades. In February 2025, BASF introduced biomass-balanced (BMB) and Ccycled® grades of DOTP at its Pasadena, Texas, and Cornwall, Ontario sites, enabling customers to reduce product carbon footprint through mass-balance feedstock substitution. In parallel, bio-based DOTP adoption in Europe expanded sharply during 2024–2025, with reported penetration reaching 17.9%, nearly triple the growth rate of conventional grades, supported by green public procurement mandates and automotive Scope 3 decarbonization targets. UPC Technology reinforced this transition in late 2024, reporting that its eco-friendly and hydrogenated plasticizer portfolio captured over 70% of Taiwan’s market share, signaling rapid displacement of conventional phthalates in high-sensitivity jurisdictions.

Operational volatility and strategic restructuring defined late 2025 and early 2026. In December 2025, Nan Ya Plastics reported a NT$1.75 billion revenue decline in its chemical division, citing weaker plasticizer pricing and softened demand sentiment. The pressure intensified in January 2026, when scheduled maintenance of Nan Ya’s 2-ethylhexanol (2-EH) unit constrained DOTP output during a critical pre-Lunar New Year stocking period. Meanwhile, Eastman Chemical’s Kingsport methanolysis facility exceeded its 2025 recycled-content targets, reaching full operational scale in January 2026 and producing 2.5 times more recycled feedstock than in 2024. The facility generated an incremental $60 million in earnings, reinforcing circular DMT/TPA supply for sustainable DOTP production. Grupa Azoty unveiled its Strategy 2030 in November 2025, allocating PLN 600 million for recapitalization and committing to a 9% carbon footprint reduction, while LG Chem’s January 2026 outlook emphasized high-purity, technology-driven DOTP to navigate structural oversupply. Evonik’s February 2026 Tailor Made efficiency program, involving workforce rationalization, reflects the sector’s transition toward high-margin specialty plasticizers and Asia-focused investment as global flexible PVC demand continues its structural realignment toward compliant, low-carbon formulations.

Trends and Opportunities Shaping the Dioctyl Terephthalate (DOTP) Market

Regulatory Phase-Out of DEHP Creating Mandatory DOTP Substitution

- The accelerated removal of DEHP and DOP from sensitive applications remains the single most powerful demand driver for DOTP. Regulatory bodies across Europe and advanced healthcare markets are tightening controls on substances of concern, effectively forcing downstream converters to adopt terephthalate-based plasticizers.

- The EU Packaging and Packaging Waste Regulation, approved in late 2024 and implemented through 2025, mandates that all packaging be recyclable by 2030 while simultaneously increasing scrutiny of chemical additives used in food-contact materials. DOTP is increasingly specified in food-grade PVC films because it bypasses ECHA monitoring frameworks that continue to target ortho-phthalates for full phase-out by 2026. This regulatory alignment has elevated DOTP from a preferred option to a default specification in compliant flexible packaging.

- In parallel, medical device regulations are converging globally. In early 2025, healthcare regulators across Europe, Switzerland, and parts of Asia aligned their food-contact and medical polymer standards with EU 10/2011 principles. This alignment has triggered widespread replacement of DEHP in PVC tubing, IV bags, and blood-contact accessories with DOTP-based formulations, particularly Eastman 168™ grades. DOTP’s non-reprotoxic profile and long-term biostability are now baseline requirements rather than competitive advantages in medical polymer procurement.

Rising Competitive Pressure from High-Spec Plasticizer Alternatives

- Despite its strong regulatory positioning, DOTP faces increasing competition from both ends of the plasticizer spectrum. On one side, commodity plasticizers exert cost pressure in non-sensitive applications. On the other, specialty plasticizers such as DINCH and trimellitates are capturing high-margin niches.

- Trioctyl Trimellitate is increasingly favored in high-temperature wire and cable insulation, particularly in electric vehicle battery systems and industrial heat-resistant cables. Price adjustments announced in March 2025 highlighted the widening value gap between DOTP and high-performance trimellitates, reinforcing that DOTP is being optimized for volume-driven compliant applications rather than extreme performance environments.

- In sensitive hygiene and infant-care segments, DINCH remains a formidable competitor due to its long-standing toxicological acceptance. However, DOTP producers are countering this pressure by introducing ISCC PLUS mass-balanced grades and recycled-content compliant offerings. By December 2025, multiple Asian DOTP manufacturing hubs reported a 35% increase in exports to Europe, driven by formulators seeking cost-effective non-phthalate solutions that still satisfy Global Recycled Standard and sustainability disclosure requirements.

DOTP Demand Acceleration from Renewable Energy and Grid Modernization

- The global transition toward renewable energy and decentralized power systems is opening a structurally durable growth channel for DOTP. Outdoor electrical infrastructure increasingly requires plasticizers that deliver long-term flexibility, UV resistance, and environmental safety under extreme conditions.

- With global electricity grid investment projected to reach approximately 400 billion dollars across 2024 and 2025, demand for low-temperature, weather-resistant PVC cables has intensified. DOTP’s glass transition temperature near minus 50 degrees Celsius makes it particularly well-suited for solar DC cables, wind turbine wiring, and underground transmission lines that must maintain flexibility over service lifetimes exceeding 25 years.

- Solar infrastructure is emerging as a particularly strong demand center. By late 2025, leading cable manufacturers were actively promoting non-hazardous material portfolios aligned with ESG procurement mandates. DOTP is increasingly specified in PVC-based solar panel backsheets and cable jackets, where it delivers moisture resistance and mechanical durability without the risk of regulated phthalate migration into soil or groundwater.

Expansion Beyond PVC into Rubber and Engineering Polymer Processing

- DOTP’s application scope is expanding beyond traditional PVC as processors seek safer, higher-performance alternatives to mineral oils and low-cost plasticizers in elastomers and engineering polymers.

- In rubber compounding, DOTP is gaining traction as a processing aid in nitrile butadiene rubber and styrene butadiene rubber formulations. Technical evaluations conducted in mid-2025 show that DOTP reduces compound viscosity more efficiently than mineral oils while offering superior resistance to fuel extraction. This performance profile is particularly valuable in automotive fuel lines, seals, and gaskets, where long-term chemical stability is critical.

- In thermoplastic polyurethane systems, DOTP is increasingly adopted as a secondary plasticizer to enhance flexibility without compromising regulatory compliance. This trend is most pronounced in electronics, wearables, and consumer devices manufactured in North America and Asia-Pacific. DOTP allows TPU components to meet stringent consumer safety transparency standards while delivering the softness and durability required for next-generation flexible electronics.

Dioctyl Terephthalate (DOTP) Market Share and Segmentation Insights

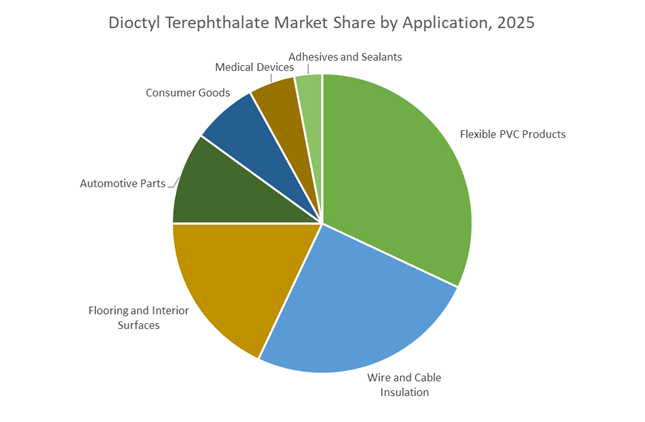

DOTP Market Share by Application : Flexible PVC Products Anchor Demand as Non-Phthalate Adoption Accelerates

Flexible PVC products lead the Dioctyl Terephthalate (DOTP) market in 2025 with 32% share, positioning DOTP as the preferred non-phthalate plasticizer for hoses, tubing, films, and profiles requiring long-term flexibility and durability. Wire and cable insulation follows as a major segment, leveraging DOTP’s excellent electrical properties, thermal stability, and low migration in building wire, automotive harnesses, and appliance cords. Flooring and interior surfaces, including luxury vinyl tiles (LVT) and sheet vinyl, represent a significant share as residential and commercial projects increasingly specify phthalate-free plasticizers. Automotive parts are a fast-growing application, driven by OEM sustainability commitments and global regulatory compliance. Consumer goods such as footwear and garden hoses maintain steady demand, while medical devices use DOTP in tubing and blood bags as a safer alternative to DEHP. Adhesives and sealants remain niche, adopting DOTP for flexible, compliant construction formulations.

DOTP Market Share by End-User Industry : Construction Dominates While Automotive and Healthcare Expand

Building and construction account for 38% of DOTP consumption, driven by widespread use in flooring, wall coverings, roofing membranes, and construction profiles aligned with green building standards and indoor air quality regulations. Electrical and electronics form a significant segment through wire and cable insulation and flexible conduits requiring permanent, low-migration plasticizers. Automotive and transportation are expanding rapidly as manufacturers transition to DOTP to meet REACH, Proposition 65, and global OEM material guidelines. Packaging and consumer goods also represent an important share, particularly in flexible packaging and closures where food-contact compliance favors terephthalate plasticizers. Healthcare and pharmaceuticals remain a smaller but strategic segment, utilizing DOTP in medical devices and pharmaceutical packaging where biocompatibility and regulatory approval are essential. Together, these industries reinforce DOTP’s position as a core growth driver in the global non-phthalate plasticizers market.

Competitive Landscape of the Dioctyl Terephthalate (DOTP) Market

The Dioctyl Terephthalate (DOTP) market in 2026 is shaped by rapid migration away from phthalates, strong demand from medical devices, wire & cable, flooring, automotive interiors, and EV infrastructure, and accelerating adoption of circular, biomass-balanced, and recycled-content plasticizers. Competitive leadership now hinges on non-phthalate innovation, vertical integration into PTA and 2-ethylhexanol (2-EH), global logistics scale, and regulatory-ready grades compliant with REACH and medical standards.

Eastman Chemical Company dominates premium DOTP with medical-grade and circular plasticizer innovation

Eastman Chemical Company is the global benchmark in the DOTP market, having pioneered high-performance non-phthalate plasticizers. Its flagship Eastman 168™ DOTP remains the industry gold standard, prized for low migration, excellent permanence, and superior compatibility in sensitive PVC applications. In early 2026, Eastman expanded its Eastman 168™ SG (Sensitive Grade) portfolio for blood bags and medical tubing, accelerating replacement of DEHP in healthcare. Under its Molecular Recycling Integration strategy, Eastman is deploying carbon renewal technology to deliver DOTP with up to 50% recycled content, meeting circular-material mandates. Backed by large-scale capacity in Kingsport and Texas City, Eastman combines global logistics with deep R&D to serve medical, flooring, and high-end consumer markets.

BASF SE leverages Verbund integration and Ccycled DOTP for REACH-compliant applications

BASF SE maintains a cost-competitive edge through its fully integrated Verbund production network, anchoring its leadership in sustainable DOTP plasticizers. The company’s Palatinol® DOTP is widely adopted across European automotive interiors and resilient flooring, meeting strict REACH compliance requirements. During 2025–2026, BASF expanded its biomass-balanced and Ccycled DOTP portfolio, utilizing chemically recycled plastic waste as feedstock. Production optimization at its Zhanjiang Verbund site in China now supports South China’s growing demand for eco-friendly wire and cable insulation. With backward integration into 2-ethylhexanol and purified terephthalic acid (PTA), BASF shields customers from feedstock volatility while advancing low-carbon plasticizer adoption.

Aekyung Chemical emerges as Asia-Pacific’s largest DOTP capacity hub

Aekyung Chemical has rapidly become the dominant DOTP supplier in Asia-Pacific, reaching 660,000 tons per year capacity by 2026 following its acquisition of a 50% stake in VPCHEM Vietnam. In 2026, Aekyung repositioned its Vietnam facility to focus exclusively on high-purity DOTP exports to North America and Europe, capitalizing on ASEAN cost advantages. As the only plasticizer producer in Vietnam, Aekyung commands unmatched regional logistics efficiency. Its strategic roadmap targets conversion of 40% of general-purpose lines to eco-friendly non-phthalate grades by 2027, reinforcing leadership in sustainable PVC plasticizers for construction, automotive, and consumer goods.

UPC Technology Corporation supplies high-purity DOTP to global flooring and construction markets

UPC Technology Corporation operates as one of the world’s largest independent DOTP manufacturers, serving as a critical merchant supplier to global PVC processors. Its Uni-Plasticizer DOTP, known for >99.5% purity and consistent batch quality, is widely used in automated extrusion lines for flooring and wallpapers. UPC dominates the global decorative surfaces segment, where DOTP’s low volatile emissions and stability are essential. A late-2024 MoU with BASF secured long-term 2-ethylhexanol supply, stabilizing operations through 2026. With expanded production across Eastern China and Southeast Asia, UPC is well positioned to support regional infrastructure growth and high-volume construction demand.

Nan Ya Plastics capitalizes on extreme vertical integration for EV and wire & cable DOTP

Nan Ya Plastics, part of the Formosa Plastics Group, delivers world-scale DOTP through complete backward integration into PTA and 2-EH, enabling highly competitive factory-direct pricing. In 2026, Nan Ya ramped production of specialty low-fogging DOTP blends for premium automotive interiors, particularly electric vehicles. The company is also a leading supplier for wire and cable insulation, where DOTP’s electrical resistivity supports global 5G rollout and renewable grid expansion. With large manufacturing bases in both Texas and Taiwan, Nan Ya executes a Global Manufacturing Resilience strategy, navigating tariffs while ensuring uninterrupted supply to North American and Asian PVC markets.

China: World-Scale Capacity, Policy-Backed Self-Sufficiency, and NEV Pull

China has emerged as the most structurally important geography in the dioctyl terephthalate market, driven by capacity scale, policy alignment, and downstream substitution away from regulated ortho-phthalates. In July 2025, BASF operationalized its expanded DOTP line at the Nanjing Verbund site, lifting annual capacity to 80,000 metric tons. This expansion is strategically aligned with East Asia’s surging demand for non-phthalate plasticizers in flooring, synthetic leather, and consumer goods. At the policy level, the final phase of the Made in China 2025 framework has pushed chemical parks to achieve 70% self-sufficiency in purified terephthalic acid and 2-ethylhexanol feedstocks, directly lowering production costs and insulating DOTP supply chains from import volatility.

Pricing behavior in late 2025 reflects this structural maturity. Domestic DOTP prices stabilized in the $2,150–$2,210 per metric ton range after the volatility of 2024, supported by an estimated 12% improvement in manufacturing efficiency through smart-factory pilots in Zhejiang and Jiangsu. Environmental regulation is now the dominant demand driver. The 2025 Action Plan for Green Development mandates a 20% reduction in VOC emissions from flexible PVC lines, accelerating the phase-out of DEHP in favor of DOTP formulations. This regulatory push is reinforced by automotive trends. Under 2026 New Energy Vehicle cabin air-quality mandates, OEMs such as BYD and Geely have transitioned to high-purity DOTP to eliminate odor and fogging issues associated with low-molecular-weight plasticizers. As a result, China’s DOTP demand is increasingly anchored in compliance-critical applications rather than discretionary consumption.

United States: Feedstock Integration, Medical Adoption, and Decarbonization Pathways

The United States DOTP market is shaped by feedstock security, regulatory validation, and sustainability investments rather than pure capacity expansion. In late 2025, ExxonMobil confirmed the tripling of production in the Permian Basin, ensuring a stable and cost-competitive supply of ethane and propene for U.S. Gulf Coast chemical operations. This vertical integration provides domestic DOTP producers with a structural advantage over imports, particularly in periods of global feedstock volatility. Regulatory clarity has further strengthened DOTP’s position. Following the January 2025 TSCA risk evaluation by the U.S. Environmental Protection Agency, DOTP was formally recognized as a preferred substitute for ortho-phthalates in sensitive uses, driving a reported 15% increase in procurement by U.S. medical device manufacturers for blood bags and IV tubing.

Trade policy has also influenced sourcing behavior. The reduction of reciprocal tariffs on East Asian petrochemical products from 25% to 15% in 2025 eased landed costs for specialized DOTP grades used in high-performance wire and cable insulation, particularly for telecommunications infrastructure. At the same time, sustainability considerations are becoming more prominent. In November 2025, BASF and ExxonMobil announced collaboration on methane pyrolysis at the Baytown Complex to produce low-emission hydrogen. This initiative could reduce the carbon footprint of DOTP manufactured at integrated U.S. sites by up to 10%, signaling that future competitiveness will increasingly be linked to decarbonized production pathways rather than cost alone.

South Korea: Export-Led Resilience and Specialty Grade Differentiation

South Korea’s DOTP market is export-oriented and increasingly differentiated through performance innovation. In 2025, the country recorded total exports of $709.7 billion, with the Ministry of Trade, Industry and Energy highlighting specialty plasticizers as a resilient export category. DOTP shipments to ASEAN markets grew by 7.4%, reflecting tightening safety regulations in importing countries and the preference for non-phthalate formulations. Corporate R&D has played a central role in maintaining this competitiveness. LG Chem commercialized an ultra-low-temperature DOTP grade in mid-2025 that maintains PVC flexibility at temperatures as low as −40°C, targeting cold-chain logistics and aerospace wiring applications expected to expand in 2026.

This focus on high-performance niches has insulated DOTP from the broader petrochemical downturn. While South Korea’s overall petrochemical export value contracted by 11.4% in 2025 due to global oversupply, non-phthalate plasticizers demonstrated relative resilience. The reason is structural rather than cyclical. DOTP demand is increasingly driven by regulatory compliance in EU and U.S. markets, where safety and material performance standards act as non-negotiable entry requirements.

India: Infrastructure-Led Demand and Import Substitution

India’s dioctyl terephthalate market is transitioning from import dependence toward localized production, supported by infrastructure expansion and industrial policy. By September 2025, Production Linked Incentive schemes had attracted over ₹2 lakh crore in investments, with specialty chemicals and plasticizer intermediates identified as priority segments. These incentives are designed to reduce reliance on DOTP imports from South Korea and China, particularly for applications where supply continuity is critical. Demand growth is being driven by urban infrastructure rather than consumer goods alone. The Ministry of Housing and Urban Affairs reported a 30% year-on-year increase in 5G-ready fiber optic cable installations in 2025, directly boosting consumption of DOTP-plasticized jacketing materials across 100 designated Smart Cities.

Medical applications represent a parallel growth vector. In August 2025, the Department of Pharmaceuticals confirmed that 21 PLI-backed medical device projects had entered production, including diagnostic equipment requiring flexible, biocompatible components. DOTP is increasingly specified in these applications due to its regulatory acceptance and performance stability, reinforcing India’s role as a demand growth market where infrastructure and healthcare investments converge.

Germany: Regulatory Substitution and Sustainable Distribution Leadership

Germany occupies a pivotal position in the European DOTP market as regulatory substitution accelerates. The adoption of Regulation (EU) 2025/1731 in August 2025 expanded REACH Annex XVII to include 16 additional CMR substances, effectively making DOTP the default plasticizer for PVC products sold in the EU from September 1, 2025. This regulatory shift has rapidly displaced legacy phthalates across flooring, cables, and coated fabrics. At the same time, sustainability considerations are reshaping procurement. European manufacturers reported a 17.9% adoption rate of bio-based DOTP grades in 2025, driven by EU Green Deal objectives and corporate decarbonization targets.

German distributors have played a central role in scaling these alternatives. Companies such as OQEMA have expanded distribution of sustainable plasticizer variants across the DACH region, positioning Germany as both a compliance and sustainability reference market. As a result, DOTP demand in Germany is less sensitive to price fluctuations and more closely tied to regulatory timelines and certified material specifications.

Dioctyl Terephthalate Market: Country-Level Strategic Snapshot

Dioctyl Terephthalate Market County Level Snapshot

|

Country

|

Strategic Focus

|

Primary Demand Drivers

|

Market Positioning

|

|

China

|

Capacity scale and VOC compliance

|

Flooring, wallpapers, NEV interiors

|

Global production and substitution hub

|

|

United States

|

Feedstock security and medical adoption

|

Medical devices, cables, sustainability

|

Regulatory-validated growth market

|

|

South Korea

|

Export resilience and specialty grades

|

Cold-chain, aerospace, ASEAN exports

|

Performance-driven supplier

|

|

India

|

Infrastructure and import substitution

|

Telecom cables, medical devices

|

High-growth demand market

|

|

Germany

|

REACH-driven substitution and bio-based uptake

|

PVC products, green materials

|

EU regulatory benchmark

|

Dioctyl Terephthalate Market Report Scope

Dioctyl Terephthalate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$4.7 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Purity Grade (High Purity Grade, Ultra-High Purity Grade, Industrial Grade), By Application (Wire and Cable Insulation, Flexible PVC Products, Flooring and Interior Surfaces, Automotive Parts, Medical Devices, Consumer Goods, Adhesives and Sealants), By End-User Industry (Building and Construction, Automotive and Transportation, Electrical and Electronics, Healthcare and Pharmaceuticals, Packaging and Consumer Goods)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Eastman Chemical Company, Exxon Mobil Corporation, LG Chem Ltd., Aekyung Chemical Co., Ltd., Nan Ya Plastics Corporation, Evonik Industries AG, Oxea GmbH, UPC Technology Corporation, Hanwha Solutions Corporation, China Petroleum & Chemical Corporation, Wanhua Chemical Group Co., Ltd., Grupa Azoty S.A., Valtris Specialty Chemicals, KLJ Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Dioctyl Terephthalate Market Segmentation

By Purity Grade

- High Purity Grade

- Ultra-High Purity Grade

- Industrial Grade

By Application

- Wire and Cable Insulation

- Flexible PVC Products

- Flooring and Interior Surfaces

- Automotive Parts

- Medical Devices

- Consumer Goods

- Adhesives and Sealants

By End-User Industry

- Building and Construction

- Automotive and Transportation

- Electrical and Electronics

- Healthcare and Pharmaceuticals

- Packaging and Consumer Goods

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Dioctyl Terephthalate Industry

- BASF SE

- Eastman Chemical Company

- Exxon Mobil Corporation

- LG Chem Ltd.

- Aekyung Chemical Co., Ltd.

- Nan Ya Plastics Corporation

- Evonik Industries AG

- Oxea GmbH

- UPC Technology Corporation

- Hanwha Solutions Corporation

- China Petroleum & Chemical Corporation

- Wanhua Chemical Group Co., Ltd.

- Grupa Azoty S.A.

- Valtris Specialty Chemicals

- KLJ Group

*- List not Exhaustive