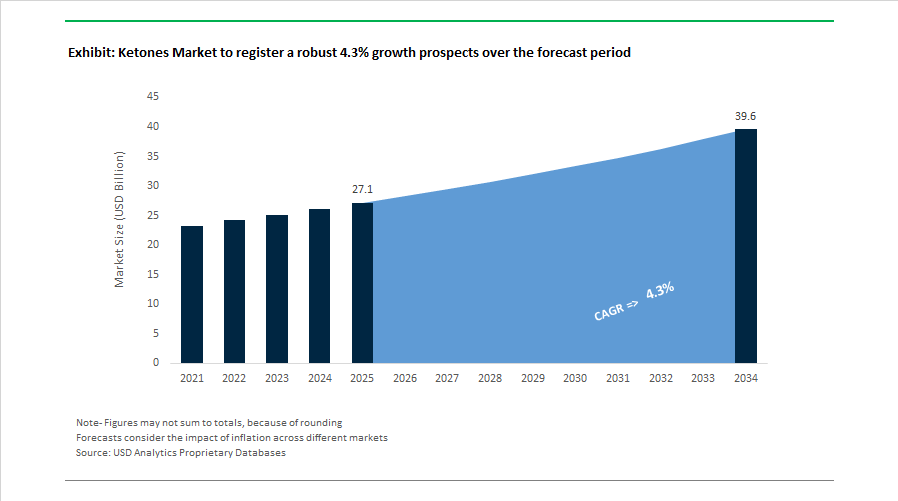

Ketones Market to Reach $39.6 Billion by 2034 as Feedstock Integration and Functional Nutrition Expand Demand

The Ketones Market is projected to grow from $27.1 billion in 2025 to $39.6 billion by 2034, registering a CAGR of 4.3%. Growth is being supported by recovery in industrial solvent demand, rising infrastructure investments across emerging economies, and the rapid commercialization of functional ketone esters in health and nutrition. At the same time, margin compression in 2025 and regulatory pressure on volatile organic compounds (VOCs) have triggered strategic restructuring across the global ketone value chain.

Feedstock integration remains central to competitiveness. In February 2026, LyondellBasell projected a stronger 2026 outlook following a difficult 2025, during which margins fell roughly 45% below historical averages. The company is advancing $2.9 billion in active projects, including major propylene unit additions at Channelview, Texas, capable of converting ethylene into approximately 882 million pounds of propylene annually. As propylene is a key precursor for acetone and downstream methyl ethyl ketone (MEK), this investment strengthens North American ketone supply resilience. Meanwhile, Prasol Chemicals announced in November 2025 a multi-year debottlenecking and expansion plan in Maharashtra, scaling diacetone alcohol and acetone-based chemistries to capture rising demand from coatings and lubricant additive manufacturers.

Pricing cycles have begun to stabilize after a 2025 downturn. MEK prices declined nearly 20% from 2024 highs, settling around $0.93/kg FOB China by late 2025. By January 2026, sentiment shifted toward gradual recovery as automotive refinishing and construction demand improved. Celanese implemented global price increases effective June 1, 2025, citing elevated logistics and regulatory costs, reinforcing tighter supply discipline across specialty ketone derivatives. Concurrently, new U.S. tariff adjustments in 2025 reshaped procurement strategies, prompting manufacturers to diversify sourcing and expand domestic output to reduce exposure to Chinese exports.

Regulatory developments are accelerating solvent substitution. In July 2024, California introduced stricter VOC controls extending into 2025, encouraging the transition toward bio-based ketones and low-VOC solvent systems. In parallel, Technip Energies and Shell partnered in June 2024 to commercialize Bio-2-Glycols technology, enabling production of bio-derived glycols and renewable ketone intermediates from glucose feedstocks. These developments reflect broader decarbonization pressures across coatings and adhesives markets.

Beyond industrial solvents, exogenous ketones are reshaping the demand profile. In April 2025, Herbalife completed its $44 million acquisition of Pruvit assets, marking a major entry of established nutrition brands into ketone esters and salts. HVMN introduced an enhanced ketone ester formula in early 2025, improving bioavailability and taste, historically key adoption barriers. By January 2026, AI-enabled metabolic tracking platforms began offering personalized ketone intake recommendations based on real-time biomarker monitoring, creating a tech-integrated wellness ecosystem. Pruvit’s expansion into keto-friendly protein powders and snacks in 2024 signaled the integration of ketones into broader functional food applications rather than niche supplements.

Emerging markets remain important consumption engines. India increased capital expenditure by 11.1% to $133 billion for FY 2024–25, driving demand for ketone-based solvents in infrastructure coatings. As infrastructure expansion continues, India has become one of the fastest-growing importers of MEK and acetone derivatives.

Trends and Opportunities in the Global Ketones Market

Strategic Capacity Realignment and Acetone Supply Decoupling from Phenol Economics

The global ketones market is undergoing a structural reset as the traditional cumene route for acetone production becomes increasingly misaligned with market realities. The cumene process inherently links acetone output to phenol demand, yielding roughly 0.6 metric tons of acetone per ton of phenol. In Western markets, this coupling has become a strategic liability due to weak phenol demand, elevated energy costs, and aggressive carbon pricing frameworks. As a result, producers are accelerating the transition toward “on-purpose” acetone production via isopropanol dehydrogenation, allowing capacity decisions to be driven by acetone end-markets rather than phenol consumption cycles.

This shift is most visible in Europe. In June 2025, INEOS Phenol announced the permanent shutdown of its Gladbeck, Germany site, historically the world’s second-largest phenol plant. The closure removes approximately 400,000 metric tons per year of acetone capacity from the European supply base and underscores the region’s deteriorating energy competitiveness under CO₂ taxation regimes. The resulting supply gap is accelerating investment into alternative production routes. Mid-2025 techno-economic assessments show that optimized IPA-to-acetone conversion, combined with biomass-based utilities and improved reactor temperature control, can lift producer revenues by about 5.2% while delivering ultra-high-purity acetone at 99.99%. This grade is increasingly demanded in downstream methyl methacrylate, electronics resins, and specialty coatings.

While Europe rationalizes capacity, Asia-Pacific is consolidating its role as the global acetone and ketone supply anchor. New investments in Indonesia and Vietnam added roughly 0.6 million metric tons of capacity in 2024 alone, strengthening the region’s ability to serve BPA, polycarbonate, and engineered resin value chains. For decision-makers, this divergence signals a long-term geographic rebalancing of ketone production, with Asia emerging as the marginal supplier and Europe transitioning toward structural import dependence.

Expansion of High-Purity Specialty Ketones in Life Sciences and Advanced Materials

Parallel to base acetone realignment, demand growth is accelerating in high-purity specialty ketones such as methyl isobutyl ketone and cyclohexanone. These molecules play a critical role as solvents and chiral building blocks in pharmaceutical synthesis and next-generation agrochemical formulations. By late 2025, pharmaceutical applications accounted for approximately 19% of global MIBK demand, equivalent to nearly 98 kilotons annually. More importantly, regulatory tightening and quality requirements have pushed over 1,200 pharmaceutical manufacturers worldwide to mandate purity levels exceeding 99%, improving crystallization yields by an estimated 9% during active ingredient synthesis.

Compliance costs are rising but unavoidable. Roughly 39% of global MIBK producers are investing in advanced VOC-abatement systems to meet sub-500 mg/m³ emission thresholds enforced across the EU and North America. These upgrades have increased operating costs by about 16%, yet they are now a prerequisite for Tier-1 pharmaceutical and medical supply contracts. At the same time, process innovation is offsetting some of this pressure. Integrated acetone-isopropanol process improvements introduced through 2024–2025 have enhanced ketone conversion efficiency by around 15%, directly supporting the synthesis of high-performance intermediates such as 6PPD antiozonants used in premium tire and rubber compounds.

Bio-Based Ketones as Scalable Sustainable Platform Chemicals

The transition from fossil-based to renewable carbon feedstocks is opening a new growth chapter for ketones. Acetone-Butanol-Ethanol fermentation, once considered obsolete, is being revived through precision fermentation technologies that dramatically improve yield and process control. In February 2025, International Process Plants leased a 40-million-gallon-per-year fermentation facility in Little Falls, Minnesota, to Nuol Green Chemistry. The facility is purpose-built for bio-acetone and bio-butanol production using engineered enzymes, targeting cosmetics, food-grade solvents, and specialty coatings markets.

Feedstock innovation further strengthens the business case. Celtic Renewables and similar players are commercializing routes that utilize low-value residues and spent materials instead of food crops, eliminating a major cost and sustainability barrier. These residue-to-chemical pathways enable circular production of bio-based ketones with significantly lower lifecycle emissions. Government policy is reinforcing this shift. Under National Bio-Energy Mission 2025 frameworks, countries such as India are offering capital financial assistance for biomass-to-chemical projects, explicitly aiming to replace imported petrochemical solvents with domestically produced second-generation bio-ketones.

Fluorinated Ketones for High-Voltage and High-Safety Battery Electrolytes

One of the most strategic emerging opportunities for ketones lies in advanced energy storage. High-nickel lithium-ion batteries and next-generation chemistries require electrolytes that remain stable above 4.5 volts while mitigating thermal runaway risk. Fluorinated ketones are gaining traction as enabling materials due to their oxidative stability and ability to form robust solid-electrolyte interphase layers.

Academic and applied research is rapidly validating this opportunity. Studies published in 2024–2025 by University of Tokyo and AIST demonstrated that fluorinated mesogen-based electrolytes remain stable above 4.0 V versus Li/Li+, delivering higher coulombic efficiency and improved discharge capacity relative to conventional systems. Subsequent testing of fluorinated ketone and ester local high-concentration electrolytes showed reliable performance at sub-zero temperatures down to –20 °C and during fast-charging at 4C rates. These attributes are critical for electric vehicle thermal management and grid-scale storage applications.

Beyond performance, safety is the defining value proposition. Fluorinated ketones contribute directly to non-flammable electrolyte formulations, addressing one of the most pressing constraints in stationary energy storage and aerospace battery systems. For stakeholders across the ketones value chain, this positions fluorinated ketones not as niche additives but as strategic enablers of next-generation electrification and energy security.

Ketones Market Share and Segmentation Insights

Acetone Leads the Ketones Market Through Large-Scale Production and Multi-Industry Solvent Applications

Acetone represented 48.60% of the Ketones Market share in 2025, establishing it as the dominant ketone product across global chemical and industrial applications. Acetone is one of the most widely produced ketones due to its large-scale manufacturing through the cumene process, where it is generated as a co-product during the production of phenol from cumene oxidation. The chemical’s high solvency, fast evaporation rate, and compatibility with numerous polymer systems make it a key solvent in paints, coatings, adhesives, printing inks, and industrial cleaning formulations. Beyond solvent applications, acetone also serves as a critical chemical intermediate in the production of methyl methacrylate (MMA) and bisphenol A (BPA), which are used in manufacturing acrylic plastics, polycarbonate resins, and epoxy materials. In 2025, the global acetone market remains closely linked to phenol production capacity and bisphenol A demand, meaning acetone availability and pricing dynamics are often influenced by phenol market conditions rather than standalone acetone consumption patterns.

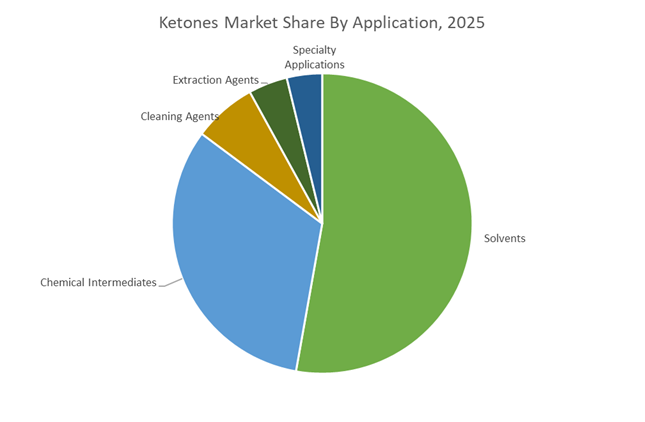

Solvent Applications Drive the Largest Consumption of Ketones Across Industrial Formulations

Solvent applications accounted for 52.80% of the Ketones Market share in 2025, making them the largest application segment for ketone-based chemicals. Ketones such as acetone, methyl ethyl ketone (MEK), methyl isobutyl ketone (MIBK), and cyclohexanone are widely used as high-performance solvents in paints, coatings, adhesives, sealants, printing inks, and resin processing operations. Their molecular structure provides strong solvency for numerous resins including acrylics, vinyl polymers, epoxies, and nitrocellulose, enabling efficient dissolution, viscosity control, and film formation in coating and adhesive formulations. Ketones also offer controlled evaporation rates and compatibility with multi-component solvent systems, making them valuable in high-speed industrial coating and printing operations. In 2025, tightening global volatile organic compound emission regulations have reshaped solvent formulation strategies, encouraging the use of high-solids coatings and optimized solvent blends. Within these systems, ketones remain essential because they enable effective polymer dissolution and rapid drying performance, maintaining their importance in industrial solvent markets despite evolving environmental regulations.

Competitive Landscape in Ketones Market

Shell Chemicals Strengthens Global Oxygenated Solvent Supply

Shell Chemicals remains a dominant player in the global ketones market, particularly in the acetone and methyl ethyl ketone segments. Through its integrated refinery-to-chemicals network, the company maintains strong supply capabilities for high-purity oxygenated solvents used in industrial coatings, adhesives, and specialty chemical synthesis. In a strategic operational shift during 2025–2026, Shell announced the closure of its MEK production facility in Pernis, Netherlands while forming new partnerships along the U.S. Gulf Coast to optimize a more efficient chemical asset base. The company specializes in high-purity acetone and MEK grades designed for low-viscosity coatings and high-performance adhesives. Shell is transitioning toward asset-light chemical operations in Europe while prioritizing expansion in Asia and North America, where feedstock economics are more favorable. In 2025, the company also successfully piloted bio-based feedstock integration into ketone production to support the sustainability goals of personal care and coatings customers.

Dow Inc. Advances Digital Manufacturing and Solvent Innovation

Dow Inc. maintains a leading position in the ketones market through its diversified oxygenated solvents portfolio used in infrastructure, packaging, and electronics applications. In January 2026, the company launched its Transform to Outperform program, targeting approximately $2 billion in near-term operating EBITDA improvement through digital manufacturing and operational simplification. As of early 2026, Dow is deploying artificial intelligence and advanced automation to improve productivity across its oxygenated solvents operations. The company also opened its first Cooling Science Studio in Shanghai during late 2025, focusing on next-generation thermal management solutions for data centers, where specialty ketones and esters serve as advanced cooling fluids. Dow currently operates manufacturing facilities across 29 countries, supporting supply to high-growth industries including semiconductor packaging, infrastructure coatings, and electronic materials.

BASF SE Expands Sustainable Ketone Production Through Verbund Integration

BASF SE leverages its globally integrated Verbund system to produce ketones as high-value intermediates across fragrance chemicals, vitamin synthesis, and specialty fuel additives. In February 2026, BASF projected EBITDA before special items between €6.2 billion and €7.0 billion, with the Chemicals and Nutrition & Care divisions contributing significantly to profitability. The company’s Zhanjiang Verbund site in China is ramping up operations during 2026 and represents a major milestone in sustainable chemical manufacturing. The facility includes the first steam cracker globally powered by renewable energy compressors, significantly lowering the carbon footprint of downstream ketone intermediates. Under its Winning Ways roadmap, BASF aims to achieve €2.3 billion in cumulative annual cost savings by the end of 2026 through organizational simplification and AI-enabled process optimization. BASF’s ketone portfolio includes specialized aliphatic and aromatic intermediates used across flavors, fragrances, and high-performance chemical additives.

Celanese Corporation Strengthens Acetyl Chain Integration

Celanese Corporation holds a strategic role in the ketones market through its global acetyl chain platform, supplying acetic acid and derivatives that serve as key feedstocks for industrial solvent and ketone production. In February 2026, Celanese opened the expanded Michigan Technology Center, designed to accelerate product development and engineering innovation across its engineered materials portfolio. The company also completed the divestiture of its Micromax business in early 2026, enabling stronger capital allocation toward high-margin specialty materials and core chemical intermediates. During the same period, Celanese implemented price increases for acetic acid and related derivatives across the Western Hemisphere to offset rising logistics and raw material costs. The company reported fourth-quarter 2025 operating EBITDA of $435 million with margins of approximately 20%, positioning Celanese for continued footprint optimization and refinancing initiatives in 2026.

Eastman Chemical Company Expands Specialty Ketone Applications

Eastman Chemical Company is a major supplier of specialty ketones, esters, and acid intermediates used across transportation, packaging, and construction materials markets. In March 2026, Eastman announced off-list price increases for glacial acetic acid and acetic anhydride, key upstream intermediates influencing ketone production economics across North America and Latin America. The company continues to execute an innovation-driven growth strategy focused on differentiated application development in automotive coatings, architectural finishes, and industrial adhesives. Eastman has also expanded its sustainable product portfolio by integrating molecular recycling technology, enabling production of chemical intermediates with lower environmental impact. Despite macroeconomic softness in late 2025, Eastman maintained a stable dividend policy announced in February 2026, reflecting strong confidence in its specialty chemical and solvent portfolio.

Sasol Limited Expands Gas-Based Ketone Production Capabilities

Sasol Limited plays a distinctive role in the ketones market through its proprietary coal-to-liquids and gas-to-liquids technologies, which generate high-quality oxygenated solvent co-products. As of February 2026, Sasol reported that its chemicals segment accounted for approximately 62% of total fiscal year-to-date volumes, reflecting the growing strategic importance of specialty chemicals in its portfolio. The company is executing its Future Sasol transformation plan, designed to streamline operations and enhance customer-centric chemical product offerings. In 2026, Sasol commissioned the third low-carbon boiler at its Natref facility to improve operational efficiency and support corporate decarbonization goals. The company is also evaluating methane rich gas supply options to secure long-term feedstock availability for its gas-based chemical production operations in South Africa.

United States Ketone Industry: Ultra-Pure Solvent Leadership and Digitalized Cost Control

The United States ketone industry is consolidating its leadership in ultra-high-purity solvent production, closely aligned with semiconductor and advanced materials supply chains. In early 2025, ExxonMobil confirmed upgrades at its Baton Rouge facility, enabling production of 99.999% ultra-pure isopropanol. This feedstock is critical for downstream ketone synthesis used in 2 nm semiconductor node drying and wafer cleaning processes, positioning the U.S. as a preferred source for electronic-grade ketones. Parallel investments in digital manufacturing are reinforcing competitiveness, with ExxonMobil deploying an app-based industrial control architecture at the same site to cut operating costs by an estimated 10–15% across chemical synthesis units.

Decarbonization and portfolio optimization are shaping medium-term strategy. Celanese Corporation achieved ISCC carbon footprint certification in December 2025 following carbon capture and utilization integration at its Clear Lake complex, converting captured CO₂ into methanol for downstream ketone chains. At the same time, Celanese’s divestiture of its Micromax® portfolio is freeing capital for higher-margin specialty materials. Regulatory shifts effective February 2026 under new Consumer Product Safety Commission rules are also influencing formulation strategies, favoring efficient ketones such as MEK in low-VOC compliant adhesive and coating systems. Softer crude price expectations for 2025–2026 further support stable ketone production economics by easing propylene and aromatics feedstock costs.

China Ketone Industry: Policy-Led Upgrading and Carbon-Accountable Growth

China’s ketone industry is evolving under a clear policy mandate to prioritize value-added, high-end oxygenated solvents. The Ministry of Industry and Information Technology’s 2025–2026 work plan sets a 5% annual growth target for chemical sector added value, explicitly steering producers toward automotive and electronics-grade ketones. Within this framework, BASF announced that its Nanjing site has transitioned its entire intermediate portfolio to 100% renewable electricity, delivering measurable reductions in product carbon footprint and strengthening supplier credentials for multinational customers.

Operational sophistication is increasing alongside environmental oversight. BASF’s commissioning of a Controlled Free Radical Polymerization dispersant line in Nanjing supports high-performance industrial coatings that rely on advanced ketone solvent systems. Simultaneously, the expansion of China’s national carbon market to petrochemicals in 2025 requires ketone producers to implement absolute emissions monitoring by 2026, accelerating investment in cleaner distillation and energy management. Strategic acquisitions, such as Sumitomo Chemical securing a Taiwanese semiconductor process chemicals business, further underscore China’s role as a central node in Asia’s ketone-based electronics materials ecosystem.

South Africa Ketone Industry: Coal-to-Chemicals Stability and Emission Reduction Pilots

South Africa’s ketone industry remains anchored in coal-to-chemicals integration, with operational reliability improving after recent infrastructure upgrades. Sasol Limited reported stable FY2025 production at its Secunda Operations following the ramp-up of a new destoning plant that improved coal feedstock quality. Enhanced steam availability at Natref, supported by a second low-carbon boiler, lifted production by 17% year-on-year and stabilized supplies of heavy ketones and related co-products.

The focus is now shifting toward emissions performance and output flexibility. Sasol’s FY2026 roadmap targets a 20% reduction in absolute greenhouse gas emissions by 2030, with 2025–2026 serving as a pilot phase for carbon-efficient distillation technologies. In parallel, the ORYX GTL plant’s successful ramp-up in early FY2025 is expected to materially increase liquid fuel and chemical co-product output, reinforcing South Africa’s position as a strategic supplier of ketone intermediates derived from gas-to-liquids and coal-based pathways.

France Ketone Industry: Specialty Materials Pivot and Green Finance Alignment

France’s ketone industry is increasingly shaped by specialty materials positioning and disciplined cost management. Arkema projects resilient EBITDA margins through 2026 despite macroeconomic volatility, supported by a strategic pivot toward specialty materials that utilize high-performance ketones as solvents and intermediates. Cost optimization initiatives launched in late 2025 aim to offset fixed-cost inflation through streamlined processing and energy efficiency gains, targeting €100 million in cumulative savings.

Innovation and sustainable finance are reinforcing this transition. At the K 2025 trade show, Arkema showcased ketone-derived organic peroxides and advanced polyimides designed for 5G and AI hardware cooling, highlighting the role of specialty ketones in next-generation electronics. The issuance of a €500 million green bond in 2025 further underlines Arkema’s commitment to funding R&D in sustainable intermediates and bio-based ketone derivatives, aligning capital markets strategy with regulatory and customer sustainability expectations.

Ketone Industry: Country-Level Strategic Snapshot

Ketones Market County Level Snapshot

|

Region

|

Primary Strategic Driver

|

Core Industry Focus

|

Structural Outcome

|

|

United States

|

Ultra-pure solvents and digitalization

|

Semiconductors, low-VOC adhesives

|

Cost-efficient, high-spec supply

|

|

China

|

MIIT policy and carbon accountability

|

Automotive and electronics ketones

|

Value-added upgrading

|

|

South Africa

|

Coal-to-chemicals integration

|

Heavy ketones and GTL co-products

|

Stable output with lower emissions

|

|

France

|

Specialty materials and green finance

|

High-performance and bio-based ketones

|

Margin resilience and innovation

|

Ketones Market Report Scope

Ketones Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.1 Billion

|

|

Market Size (2034)

|

$39.6 Billion

|

|

Market Growth Rate

|

4.3%

|

|

Segments

|

By Product Type (Acetone, Methyl Ethyl Ketone, Methyl Isobutyl Ketone, Cyclohexanone, Other Ketones), By Application (Solvents, Chemical Intermediates, Extraction Agents, Cleaning Agents, Specialty Applications), By End-Use Industry (Automotive and Transportation, Construction and Infrastructure, Electronics and Semiconductors, Pharmaceuticals and Healthcare, Packaging and Printing, Agriculture)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Exxon Mobil Corporation, Shell plc, Dow Inc., Celanese Corporation, BASF SE, Sasol Limited, Arkema S.A., Mitsui Chemicals, Inc., Sumitomo Chemical Co., Ltd., Lotte Chemical Corporation, INEOS Phenol, Kumho P&B Chemicals, Zhejiang Xinhua Chemical Co., Ltd., PetroChina Company Limited, Hexion Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ketones Market Segmentation

By Product Type

- Acetone

- Methyl Ethyl Ketone

- Methyl Isobutyl Ketone

- Cyclohexanone

- Other Ketones

By Application

- Solvents

- Chemical Intermediates

- Extraction Agents

- Cleaning Agents

- Specialty Applications

By End-Use Industry

- Automotive and Transportation

- Construction and Infrastructure

- Electronics and Semiconductors

- Pharmaceuticals and Healthcare

- Packaging and Printing

- Agriculture

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ketones Industry

- Exxon Mobil Corporation

- Shell plc

- Dow Inc.

- Celanese Corporation

- BASF SE

- Sasol Limited

- Arkema S.A.

- Mitsui Chemicals, Inc.

- Sumitomo Chemical Co., Ltd.

- Lotte Chemical Corporation

- INEOS Phenol

- Kumho P&B Chemicals

- Zhejiang Xinhua Chemical Co., Ltd.

- PetroChina Company Limited

- Hexion Inc.

*- List not Exhaustive