Methyl Isobutyl Ketone Market 2025–2034: Capacity Rationalization, Acetone One-Step Dominance, and Semiconductor-Grade Demand Driving $1,760 Million Outlook at 4.7% CAGR

The Methyl Isobutyl Ketone (MIBK) Market is projected to grow from $1,164.1 Million in 2025 to $1,760 Million by 2034, registering a CAGR of 4.7%. Market dynamics are being shaped by structural oversupply in Asia, technology shifts in production pathways, and evolving downstream demand from agrochemicals, coatings, pharmaceuticals, and semiconductor manufacturing. MIBK remains a critical solvent for extraction processes, surface coatings, adhesives, rubber chemicals, and electronic-grade applications due to its strong solvency power, low miscibility with water, and chemical stability. However, price volatility and feedstock cost pressures continue to influence producer margins and global trade flows.

In 2024, China commissioned approximately 130,000 metric tons of new MIBK capacity, raising its domestic production capability to nearly 250,000 tons and transitioning the region from deficit to surplus. This aggressive expansion triggered significant downward pressure on global spot prices, culminating in a notable correction in Q1 2025 when prices in key Asian hubs declined by more than 15% following a late-2024 peak. In parallel, India strengthened its position as a major consumer of high-purity MIBK extraction grades during 2024 and 2025, driven by expanded agrochemical and pharmaceutical manufacturing under the “Make in India” initiative. Throughout 2025, semiconductor facility expansions in India and the United States contributed to a reported 19% increase in MIBK usage for advanced electronic coatings and photoresist carrier systems.

Supply rationalization intensified in 2025 and early 2026. In April 2025, Shell shut down its 90,000 mt/year MEK unit in Pernis, signaling broader ketone portfolio optimization across Europe. North American MIBK producers curtailed operating rates to near or below 70% during 2025 to manage inventory amid soft coatings demand and rising Chinese exports. In May 2025, Mitsui Chemicals announced the split-off of its Basic & Green Materials business, including MIBK operations, to enhance competitiveness. In early 2026, KH Neochem confirmed discontinuation of MIBK production at its Yokkaichi Plant by December 2025, reflecting competitive pressure from low-cost Asian supply. Concurrently, Celanese implemented price increases citing feedstock and logistics costs, while industry leaders accelerated adoption of the acetone one-step production process, which by early 2026 had become the dominant technology due to superior conversion efficiency and lower capital intensity compared to legacy isopropanol routes.

Market Size Outlook, 2021-2035.png)

Methyl Isobutyl Ketone (MIBK) Market Trends and Opportunities

Trend: Structural Capacity Rationalization Creating a Western Supply Cliff

The global MIBK market is undergoing a structural rebalancing as Western production hubs face sustained cost pressures and regulatory constraints. Escalating energy prices in Europe, coupled with the capital intensity required to retrofit aging chemical assets to meet modern environmental standards, have accelerated permanent capacity rationalization. Between 2022 and 2027, close to 90 chemical plants across Europe are expected to shut down or have already ceased operations, removing nearly 25 million tonnes of installed capacity from the market. Energy-intensive solvents such as MIBK are disproportionately exposed, as European natural gas prices remain roughly four times higher than those in the United States, eroding the competitiveness of regional producers.

This contraction is reshaping global trade flows. By mid-2025, Asia had emerged as the dominant production center, with mainland China accounting for more than one-third of global MIBK capacity. Europe has consequently shifted into a structurally import-dependent position, with operating rates for petrochemical intermediates stabilizing at only 70–75%, well below the historical 85% threshold required for sustainable margins. Strategic portfolio reviews by diversified chemical majors are reinforcing this trend. Dow, for example, has been reassessing high-cost assets following upstream rationalization moves in North America, signaling that further exits from uneconomic regions remain likely. Collectively, these dynamics are tightening the merchant MIBK market and increasing price sensitivity to logistics disruptions and Asian export policies.

Trend: Captured Demand Growth from the Lithium-Ion Battery Ecosystem

Parallel to supply contraction, demand visibility for MIBK is strengthening through its growing role in lithium-ion battery manufacturing. MIBK has become a non-discretionary solvent for polyvinylidene fluoride binders, which are essential for cathode adhesion and mechanical stability in high-nickel battery chemistries. This has shifted a meaningful share of MIBK demand away from spot transactions toward multi-year, captive offtake agreements with battery material producers.

Investment patterns underscore this structural shift. In February 2025, Arkema announced a 15% capacity expansion at its Calvert City, Kentucky facility, representing an investment of approximately $20 million. The expansion is explicitly aligned with North American gigafactory ramp-ups and the localization requirements embedded in Inflation Reduction Act incentives. With global EV sales projected to exceed 17 million units in the 2024–2025 period, demand for PVDF binders is estimated to reach roughly $950 million in 2025. Given that MIBK is the preferred solvent for achieving optimal slurry rheology and adhesion in advanced cathodes, producers capable of delivering 99.9% purity with minimal metallic traces are commanding premium pricing under both the EU Battery Regulation and U.S. Department of Energy-supported supply chain programs.

Opportunity: MIBK Recovery and Circularity in Semiconductor Lithography

The semiconductor industry’s transition toward extreme ultraviolet lithography is intensifying solvent consumption per wafer, elevating MIBK usage in photoresist thinning and development. This has created a compelling opportunity for closed-loop solvent recovery systems that reduce hazardous waste volumes while materially lowering operating costs. Performance data from 2025 indicate that on-site recovery can cut solvent procurement and disposal expenses by up to 50%, with recovery efficiencies approaching 95% using IoT-enabled monitoring and control systems. Typical payback periods of 12 to 24 months are making these installations economically attractive for high-throughput fabs.

Technology requirements are becoming more stringent as well. Reclaimed MIBK used in semiconductor processes often must exceed 99% purity to maintain electronic-grade performance. In response, fabs are adopting microwave-assisted distillation and advanced membrane separation technologies capable of removing trace contaminants without degrading solvent quality. Regulatory pressure is accelerating adoption. Updates to VOC emission controls under the UNECE Gothenburg Protocol, now monitored by more than 50 countries, are effectively making solvent recovery a permitting prerequisite for large fabrication plants in the United States, China, and India. This convergence of economics and compliance is positioning MIBK recycling solutions as a structurally embedded growth segment rather than a discretionary sustainability add-on.

Opportunity: Strategic Formulation for High-Solids, Low-VOC Infrastructure Coatings

Tightening VOC regulations are opening a second high-value growth avenue for MIBK in advanced coatings. Jurisdictions such as California, under Rule 1113, and the broader EU Green Deal framework are forcing formulators to move away from traditional aromatic solvents while maintaining performance standards for heavy-duty applications. MIBK’s strong solvency profile allows it to function as a critical bridging solvent, enabling higher resin loading and reducing total solvent volumes by an estimated 20–30% while staying within VOC limits as low as 50 g/L.

Infrastructure investment cycles are amplifying this opportunity. India’s paints and coatings market alone is projected to reach $16.5 billion by FY25, supported by sustained public spending on bridges, ports, offshore structures, and industrial assets. These applications demand coatings with long service life, corrosion resistance, and predictable curing behavior, areas where MIBK-based formulations retain a clear performance advantage. At the same time, formulators are increasingly deploying hybrid systems that blend bio-based solvents with conventional chemistries, using MIBK as a performance anchor. This approach allows manufacturers to progress toward Scope 3 emission reduction targets without sacrificing drying speed, leveling, or film integrity, positioning MIBK as a critical enabler of compliant yet high-performance infrastructure coatings in the next regulatory cycle.

Methyl Isobutyl Ketone Market Share and Segmentation Insights

Acetone-Based Production Technology Leads Methyl Isobutyl Ketone Market Due to Feedstock Integration and Process Efficiency

The acetone-based process accounted for 78.60% of the Methyl Isobutyl Ketone (MIBK) Market share in 2025, making it the dominant industrial route for large-scale MIBK production. This manufacturing pathway involves a three-stage process consisting of acetone condensation, catalytic hydrogenation, and dehydration, producing MIBK with high yield and process efficiency. The method benefits from the widespread availability of acetone as a co-product of the phenol production process, which provides a stable and cost-effective feedstock supply for chemical manufacturers. The well-established process infrastructure and mature catalytic technologies have enabled global producers to operate large integrated chemical plants that link acetone, phenol, and MIBK production systems. This integration significantly improves feedstock utilization and reduces production costs compared with alternative synthesis routes such as isopropanol-based methods. In 2025, MIBK production economics remain closely linked to global acetone supply dynamics, meaning fluctuations in phenol market demand can influence acetone availability and pricing, which in turn affects MIBK manufacturing costs and global solvent market pricing trends.

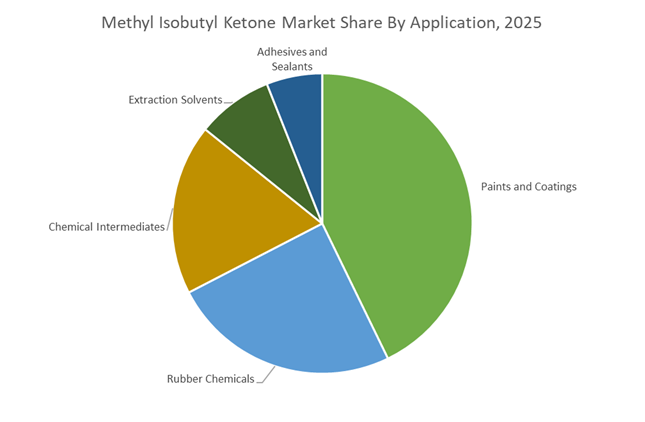

Paints and Coatings Sector Drives the Largest Demand for Methyl Isobutyl Ketone Solvents

Paints and coatings accounted for 42.80% of the Methyl Isobutyl Ketone Market share in 2025, establishing the coatings industry as the largest consumer of MIBK solvents. MIBK is widely used in automotive coatings, industrial protective coatings, wood finishes, and architectural paints, where it functions as an effective solvent for a wide range of resins including acrylics, nitrocellulose, vinyl resins, and epoxy systems. The solvent offers an advantageous combination of strong solvency power, moderate evaporation rate, and compatibility with numerous coating formulations, enabling improved film formation, surface leveling, and coating performance. These characteristics make MIBK particularly valuable in coatings that require controlled drying properties and consistent finish quality. In 2025, evolving environmental regulations targeting volatile organic compound (VOC) emissions have influenced coating formulation strategies, with manufacturers increasingly adopting high-solids coating systems that reduce solvent content while maintaining performance. MIBK remains an important formulation solvent in these systems because its solvency and evaporation characteristics help maintain proper coating viscosity, flow, and application properties even as total solvent volumes are reduced.

Methyl Isobutyl Ketone Market Competitive Landscape

The methyl isobutyl ketone (MIBK) market in 2026 is driven by high-purity electronic-grade solvents, semiconductor expansion, and regulatory-compliant production. Competition spans isopropanol-based green synthesis and large-scale acetone routes, with demand anchored in photoresist processing, rubber chemicals (6PPD), and high-solids coatings.

Shell optimizes isopropanol-based MIBK production for high-purity coatings and industrial applications

Shell Chemicals is strengthening its MIBK leadership through its integrated Energy and Chemicals Park model, ensuring resilient supply and feedstock optimization. Its isopropanol-to-MIBK production route delivers superior purity, critical for pharmaceutical extraction and agrochemical applications. Shell maintains stable utilization rates of 75–79%, supported by its Trading & Optimisation division managing acetone and hydrogen volatility. The company is prioritizing high-margin outputs, including technical-grade MIBK for coatings and marine paints. Its solvent portfolio is widely used in high-performance protective coatings requiring controlled evaporation kinetics. Shell’s global integration and purity-focused production strategy reinforce its dominance in specialty solvent markets.

Dow advances electronic-grade MIBK with green solvent innovation and feedstock stability

Dow Inc. is positioning itself at the forefront of electronic-grade MIBK through its Performance Solvents strategy and advanced material science capabilities. The company’s Shanghai Cooling Science center is accelerating the development of ultra-high-purity MIBK for semiconductor cleaning and photoresist stripping. Its “Transform to Outperform” initiative enhances asset efficiency while maintaining cost competitiveness across oxygenated solvent lines. Dow is aligning with sustainability mandates, with 15% of R&D focused on low-VOC and green solvent technologies. Long-term feedstock agreements ensure cost stability amid acetone market volatility. Its integrated approach supports growing demand across electronics, adhesives, and automotive coatings.

Mitsui Chemicals shifts to specialty MIBK with biomass integration and feedstock optimization

Mitsui Chemicals is transforming into a high-value specialty chemical player, positioning MIBK as a critical intermediate in mobility, ICT, and healthcare applications. The strategic split of its Basic & Green Materials segment enables sharper focus on advanced materials and specialty solvents. Integration of the Chiba Ethylene Complex with Idemitsu Kosan enhances feedstock efficiency for ketone production. Through ISCC PLUS-certified facilities, Mitsui offers biomass-attributed MIBK using mass balance methods, aligning with sustainability targets of global OEMs. Expansion of MDI capacity via Kumho Mitsui drives internal solvent demand for polyurethane processing. This vertically integrated model strengthens its presence in high-performance polymer and electronics markets.

Celanese integrates AI-driven formulation tools with MIBK applications in coatings and elastomers

Celanese Corporation is redefining MIBK utilization through digitalization and advanced engineered materials integration. Its Chemille® AI platform enables predictive modeling of solvent-resin interactions, optimizing coating flow, leveling, and performance. Expansion of the Michigan Technology Center enhances application development for automotive materials like Hytrel® and Santoprene®, which rely on MIBK-derived intermediates. The company achieved $120 million in cost reductions, prioritizing low-cost Gulf Coast production to maintain margins. Celanese’s MIBK is essential for manufacturing rubber anti-ozonants such as 6PPD, improving tire durability and weather resistance. Its focus on digital tools and specialty applications strengthens its competitive positioning.

Sasol scales low-carbon MIBK production to meet CBAM-driven demand in Europe

Sasol Limited is advancing its MIBK portfolio through its International Chemicals Reset strategy, emphasizing cost discipline and sustainability. The company has secured 1,200 MW of renewable energy, enabling the production of lower-carbon MIBK aligned with EU Carbon Border Adjustment Mechanism (CBAM) requirements. Improved reliability at Secunda operations increased production volumes by 10%, ensuring consistent global supply. Sasol’s MIBK is widely used in pharmaceutical extraction processes, where high solvency and purity are critical. Its integrated production model supports applications across industrial solvents, aviation materials, and specialty chemicals. Sasol’s decarbonization strategy positions it as a key supplier in sustainability-driven markets.

China: Capacity Consolidation and Transition to Export-Oriented Leadership

China has entered a structurally different phase in the methyl isobutyl ketone market, marked by scale consolidation and a decisive pivot toward export orientation. By January 2026, the country had established itself as the world’s largest MIBK producer, with total installed capacity reaching approximately 600,000 metric tons annually. This shift reflects a transition from historical import dependence to net-exporter status, with 2025 export volumes surpassing 80,000 tons and shipments increasingly directed toward Southeast Asia and the Middle East. Environmental compliance reforms introduced in late 2025 have accelerated this consolidation, as several small, high-emission units in Shandong and Jiangsu were phased out. As a result, Tier-1 producers are entering the 2026 cycle with materially higher utilization rates, estimated at 75–80%, strengthening pricing discipline and operational efficiency.

Capacity expansion by leading state-linked and private players is reinforcing China’s long-term supply dominance. Wanhua Chemical and Sinopec NanHua are finalizing new MIBK units with incremental capacities of 30,000 tons and 45,000 tons respectively, scheduled for full ramp-up by mid-2026. Beyond volume, product mix is evolving. Electronic-grade MIBK with purity above 99.9% recorded double-digit growth in 2025, driven by domestic semiconductor fabrication, PCB cleaning, and display panel manufacturing. Government-led consumer trade-in policies during 2025–2026 have also indirectly supported demand from rubber antioxidants and automotive coatings, as vehicle and appliance replacement cycles accelerate.

United States: Inventory Discipline and Specialty Solvent Resilience

The United States MIBK market is entering 2026 after a period of correction and rebalancing. During late Q3 2025, prices declined by just over 3%, largely due to elevated inventories and a concurrent softening in acetone feedstock costs. By Q4 2025, producers and distributors had shifted toward inventory rationalization, with companies such as Celanese targeting significant inventory reductions to improve cash flow and tighten spot availability of specialty solvent grades. This strategic drawdown is stabilizing the domestic supply-demand balance as the market moves into 2026.

End-use demand remains uneven but resilient in high-value applications. While architectural coatings linked to residential construction have been subdued, MIBK consumption in pharmaceutical extraction, chemical synthesis, and performance adhesives has remained steady. Automotive manufacturing continues to be a structural support, with MIBK playing a critical role in high-performance adhesives and bumper retainer systems used in next-generation vehicle platforms. Recognition of lightweighting and assembly innovations at the 2025 SPE Automotive Innovation Gala underscores the solvent’s continued relevance in advanced mobility applications, even as broader solvent markets face cyclical pressure.

India: Regulatory Push and Downstream Reformulation

India’s methyl isobutyl ketone market is being reshaped by regulatory reform and downstream manufacturing upgrades. The End-of-Life Vehicles Rules notified by the Ministry of Environment, Forest and Climate Change in January 2025 established a nationwide vehicle scrappage framework effective from April 2025. This policy is materially increasing demand for rubber antioxidants and automotive coatings, both of which rely on MIBK as a key solvent during production of replacement vehicles and components. Parallel regulatory pressure from plastic waste management amendments requiring higher recycled content in packaging is pushing ink and adhesive manufacturers to adopt high-purity solvents that are compatible with recycled resins, further supporting MIBK usage.

Strategic corporate activity is strengthening domestic integration. In July 2025, Shell Lubricants completed the acquisition of Raj Petro Specialities, enhancing access to specialized chemistries and MIBK-derived intermediates for industrial fluids and process applications. On the production side, India remains a key hub for the isopropanol-based MIBK route, supporting localized supply to agrochemical and pharmaceutical manufacturers. This route’s importance reflects India’s broader positioning as a formulation and downstream processing center rather than a bulk export base.

Germany: Sustainable Solvent Use in Advanced Manufacturing

Germany maintains a structurally important role in the global MIBK landscape through its leadership in the acetone production route and its focus on sustainable industrial chemistry. Domestic producers continue to emphasize high-performance applications, particularly in polymer synthesis chains where MIBK is used as a process solvent under stringent quality and traceability requirements. Major production sites around Frankfurt have achieved ISCC carbon footprint certification, reinforcing Germany’s alignment with low-carbon manufacturing frameworks and circular feedstock sourcing.

Industrial coatings remain a central demand pillar. German machinery and aerospace manufacturers continue to specify MIBK for its strong solvency and controlled evaporation characteristics, which are critical for precision coatings and surface treatments. This focus on technically demanding end uses positions Germany as a reference market for performance-grade MIBK, even as lower-margin commodity demand migrates toward higher-capacity regions.

South Africa: Integrated Production and Cost Discipline

South Africa’s relevance in the methyl isobutyl ketone market is anchored in integrated coal-to-chemicals production. Sasol reported progress in 2025 on phased shutdowns and operational upgrades at its Secunda Operations, aimed at improving long-term efficiency. Although coal quality challenges led to a modest year-on-year production decline, Secunda remains a strategically important global source of oxygenated solvents, including MIBK and related alcohols.

Cost management is a defining competitive lever. Sasol’s 2026 strategy targets mining costs within a controlled range to preserve export competitiveness for downstream chemical products. These efforts, combined with ongoing operational optimization, are positioning South African MIBK supply as a reliable option for global mining, coatings, and chemical synthesis customers seeking diversification beyond Asia-centric supply chains.

Country-Level Strategic Positioning in the Methyl Isobutyl Ketone Market

Methyl Isobutyl Ketone (MIBK) Market County Level Snapshot

|

Country / Region

|

Strategic Emphasis

|

Primary Demand Drivers

|

Policy or Industry Catalyst

|

Competitive Positioning

|

|

China

|

Scale consolidation and exports

|

Non-ferrous processing, electronics

|

MIIT reforms, trade-in policies

|

Global capacity and cost leadership

|

|

United States

|

Inventory discipline and specialties

|

Automotive adhesives, pharma

|

Inventory rationalization, innovation awards

|

Stable high-value consumption

|

|

India

|

Regulatory-driven reformulation

|

Automotive, inks, adhesives

|

ELV rules, plastic waste mandates

|

Downstream manufacturing hub

|

|

Germany

|

Sustainable high-performance use

|

Industrial coatings, polymers

|

ISCC certification, energy transition

|

Premium process-grade supplier

|

|

South Africa

|

Integrated production efficiency

|

Mining and export solvents

|

Operational upgrades, cost control

|

Diversified global supply source

|

Methyl Isobutyl Ketone (MIBK) Market Report Scope

Methyl Isobutyl Ketone (MIBK) Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1164.1 Million

|

|

Market Size (2034)

|

$1760 Million

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Production Method (Acetone-Based Process, Isopropanol-Based Process), By Grade (Solvent Grade, Chemical Intermediate Grade, Electronic Grade), By Application (Paints and Coatings, Rubber Chemicals, Chemical Intermediates, Extraction Solvents, Adhesives and Sealants), By End-User Industry (Automotive and Transportation, Building and Construction, Pharmaceuticals and Healthcare, Agrochemicals, Electronics and Electrical)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shell Chemicals, Dow, Mitsui Chemicals, Sasol, Arkema, Celanese, Eastman Chemical, Wanhua Chemical, Ningbo Zhenyang Chemical, Shandong Jinling Group, INEOS, KH Neochem, Kumho P&B Chemicals, Lotte Chemical, Sinopec

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Methyl Isobutyl Ketone Market Segmentation

By Production Method

- Acetone-Based Process

- Isopropanol-Based Process

By Grade

- Solvent Grade

- Chemical Intermediate Grade

- Electronic Grade

By Application

- Paints and Coatings

- Rubber Chemicals

- Chemical Intermediates

- Extraction Solvents

- Adhesives and Sealants

By End-User Industry

- Automotive and Transportation

- Building and Construction

- Pharmaceuticals and Healthcare

- Agrochemicals

- Electronics and Electrical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Methyl Isobutyl Ketone Market

- Shell Chemicals

- Dow

- Mitsui Chemicals

- Sasol

- Arkema

- Celanese

- Eastman Chemical

- Wanhua Chemical

- Ningbo Zhenyang Chemical

- Shandong Jinling Group

- INEOS

- KH Neochem

- Kumho P&B Chemicals

- Lotte Chemical

- Sinopec

*- List not Exhaustive