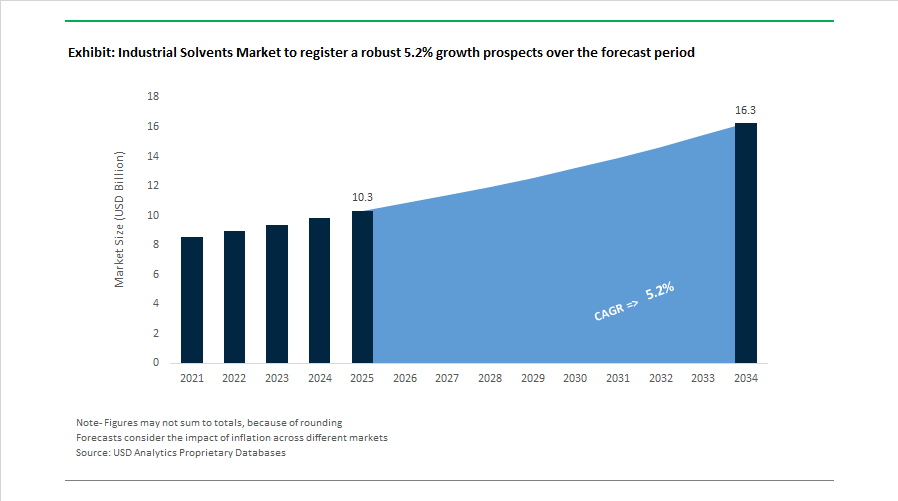

Industrial Solvents Market to Reach $16.3 Billion by 2034 at 5.2% CAGR Driven by EV Battery Electrolytes, Bio-Based Alternatives, and Capacity Realignment

The Industrial Solvents Market is projected to expand from $10.3 billion in 2025 to $16.3 billion by 2034, registering a CAGR of 5.2%. Growth is being shaped by structural shifts in electric vehicle battery manufacturing, semiconductor fabrication, specialty coatings, adhesives, and sustainable chemical formulations. Demand for high-purity carbonate solvents, glycol ethers, methyl glycols, glacial acetic acid, cyclopentanone, and bio-based solvent alternatives is increasing as manufacturers pursue supply chain security, carbon reduction targets, and performance optimization. Regional capacity investments and divestitures between 2024 and 2026 highlight a strategic transition toward specialty, high-margin solvent portfolios while rationalizing energy-intensive European production assets.

Major capital deployment began in March 2024 when Dow announced plans to construct a world-scale carbonate solvents facility on the U.S. Gulf Coast. Supported by the U.S. Department of Energy, the project aims to secure domestic electrolyte solvent supply for lithium-ion batteries used in electric vehicles and grid-scale energy storage. In the same month, BASF inaugurated its new 46,000 metric ton methyl glycols plant at its Zhanjiang Verbund site in China, targeting rising regional demand for high-performance brake fluids and industrial solvent applications within the automotive sector. In April 2024, Clariant opened its Industrial Applications Innovation Center in Charlotte, North Carolina, providing advanced laboratory capabilities to support customer transitions from solvent-based to water-based formulations. At the American Coatings Show 2024, Clariant also introduced its VITA portfolio of 100% bio-based solvents derived from bioethanol, offering chemically equivalent performance to fossil-based counterparts. In May 2024, Arkema finalized the acquisition of Dow’s flexible packaging laminating adhesives business, strengthening its position in solvent-based and solvent-less adhesive technologies aligned with sustainable packaging trends.

Strategic adjustments intensified through 2025. In the first half of 2025, BASF confirmed the shutdown of its cyclopentanone and adipic acid plants at Ludwigshafen, consolidating CPon production in South Korea and France to address elevated European energy costs. On July 1, 2025, Shell completed its acquisition of Raj Petro Specialities, expanding its specialty solvent and industrial fluids portfolio across India and South Asia. In late 2025, LyondellBasell commenced construction of a new propylene unit at its Channelview, Texas complex, expected to produce approximately 882 million pounds annually, reinforcing upstream feedstock supply for glycol-based solvents and propylene oxide derivatives. In December 2025, Solventum finalized its $850 million acquisition of Acera Surgical, underscoring increasing demand for high-purity solvents and polymers used in advanced medical material applications.

Portfolio realignment and regional optimization continued into 2026. In January 2026, Syensqo completed the divestiture of its Oil & Gas Business Unit to SNF Group, repositioning itself as a pure-play specialty company focused on high-growth sustainable solvent and performance material segments. Earlier, in September 2024, Syensqo had delayed its North American battery materials project, including solvent and PVDF production, by up to two years to recalibrate capital allocation amid macroeconomic uncertainty in the EV supply chain. In early 2026, LyondellBasell announced an expansion of glacial acetic acid production at its La Porte, Texas facility to capture market share as European competitors rationalize older assets. These developments reflect a market increasingly defined by battery-grade solvent investments, bio-based innovation, and strategic capacity rebalancing across North America, Europe, and Asia-Pacific.

Industrial Solvents Market Trends and Opportunities

Regulatory-Driven Phase-Out of High-VOC and Halogenated Industrial Solvents

The industrial solvents market is undergoing a compliance-led transformation as environmental regulations move from gradual tightening to enforceable substitution mandates. The U.S. Environmental Protection Agency’s January 2025 amendments to the National VOC Emission Standards for Aerosol Coatings have introduced product-weighted reactivity thresholds that materially disadvantage high-VOC and halogenated solvents. These limits are no longer technology neutral. They explicitly favor low-reactivity and low-VOC solvent systems to curb ground-level ozone formation, forcing coatings, adhesives, and sealants manufacturers to reformulate core product lines.

This regulatory pressure is being mirrored and amplified in Asia. China’s Comprehensive Management Plan for VOCs in Key Industries, issued in February 2025, mandates a 20-percentage-point reduction in solvent-based industrial coatings and a 20% reduction in solvent-based adhesives by the end of 2025 compared to 2020 baselines. The impact on market structure has been immediate. Environmentally compliant solvents, including water-based and bio-derived systems, reached a 35% market share in China during the first half of 2025. Forward-looking industry models indicate that this share is on track to exceed 40% by 2030 as enforcement intensity increases across provincial jurisdictions.

Manufacturers are responding by accelerating the adoption of exempt solvents such as acetone and PCBTF derivatives while scaling bio-based alternatives. In North America, bio-based industrial solvents reached functional price parity with conventional products in 2025, driven by improved agricultural feedstock logistics and long-term supply agreements from integrated coatings producers. This has effectively removed cost as a primary barrier, turning regulatory compliance into a decisive competitive differentiator rather than a constraint.

Geopolitical Supply Chain Realignment and European Capacity Rationalization

A second defining trend is the structural contraction of solvent production capacity in Europe, driven by persistently high energy prices, carbon compliance costs, and muted downstream demand. In 2025, EU chemical output declined 2.5% year on year, with deeper contractions in energy-intensive hubs such as the Netherlands and France. For solvent producers, this environment has rendered several assets structurally uncompetitive.

Mid-to-late 2025 saw a wave of permanent plant closures and consolidations. Facilities producing acetone, phenolics, and maleic anhydride were either shut down or relocated, as producers prioritized capital discipline over volume retention. The consequence has been a measurable rise in import dependency. During the first eight months of 2025 alone, the EU chemical trade deficit increased by nearly five million tons compared to the prior year.

Downstream users in electronics, pharmaceuticals, and specialty coatings are increasingly qualifying solvent suppliers in India and China to offset lost European capacity. While this shift improves cost positioning, it introduces new risks around supply consistency, batch-to-batch purity, and intellectual property exposure. As a result, procurement strategies are becoming more diversified and contract-driven, favoring suppliers capable of offering quality assurance, traceability, and long-term volume security rather than spot pricing alone.

High-Purity Solvents for Lithium-Ion Battery Manufacturing Ecosystems

The electrification of transport and stationary energy storage is creating one of the most attractive margin pools in the industrial solvents market. Lithium-ion battery manufacturing relies heavily on ultra-high-purity solvents for electrode slurry preparation, with N-Methyl-2-pyrrolidone remaining the dominant solvent for dissolving PVDF binders. However, regulatory scrutiny is reshaping how this demand is served.

The U.S. EPA’s proposed TSCA risk management rule for NMP, issued in June 2024, introduced mandatory Workplace Chemical Protection Programs that significantly raise compliance costs for gigafactories. As a result, battery manufacturers are rapidly investing in closed-loop solvent recovery systems. By late 2025, large-scale battery plants were deploying recovery units capable of reclaiming high-purity NMP suitable for direct reuse, reducing both solvent procurement costs and hazardous waste volumes.

This shift has catalyzed a fast-growing secondary market for recycled NMP, where purity assurance and recovery efficiency are becoming key value drivers. In parallel, innovation in NMP-free electrode technologies is accelerating. UV-curable and water-based binder systems are emerging that can reduce capital expenditure by up to 90% compared to conventional thermal drying lines. While these technologies are still in early commercialization, they represent a disruptive pathway for solvent minimization and solvent substitution strategies across next-generation battery platforms.

Tailored Solvents for Advanced Dissolution-Based Plastic Recycling

A second high-value opportunity lies in solvent systems designed for dissolution-based plastic recycling. Unlike mechanical recycling, dissolution processes use selective solvents to separate polymers from complex waste streams while preserving polymer chain integrity. This capability is particularly critical for multilayer and food-contact packaging where conventional recycling fails to meet purity thresholds.

Industrial dissolution recycling platforms are gaining strategic relevance in Europe as policymakers recognize their role in achieving high-quality recyclate targets. By late 2025, industry bodies had positioned dissolution recycling as a complementary pathway to mechanical recycling, especially for applications requiring virgin-like polymer performance. Commercial pilots demonstrate that dissolution processes can deliver output volume improvements of approximately 50% versus pyrolysis by eliminating downstream oil upgrading steps.

From a solvent market perspective, this creates demand for highly selective, recoverable solvents engineered for low toxicity, high recyclability, and stable performance across multiple cycles. As dissolution recycling scales from pilot to industrial capacity, solvent suppliers that can provide integrated solvent management, recovery, and reuse solutions are likely to secure long-term, high-margin supply contracts within the circular plastics value chain.

Industrial Solvents Market Share and Segmentation Insights

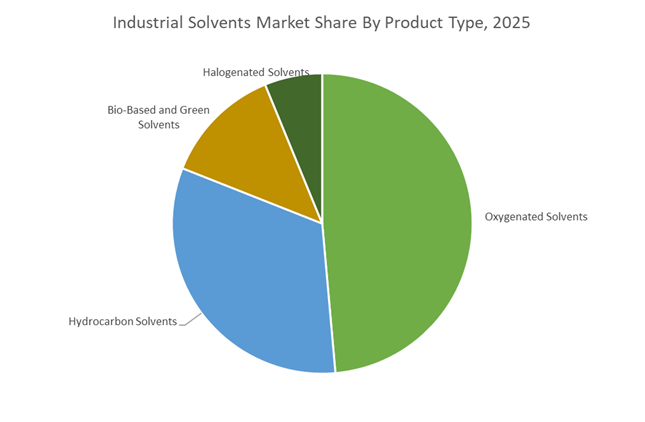

Oxygenated Solvents Lead the Industrial Solvents Market Through Regulatory-Compliant Performance

Oxygenated solvents accounted for 48.6% of the Industrial Solvents Market share in 2025, making them the dominant solvent category across multiple industrial chemical applications. Oxygenated solvents including alcohols, ketones, esters, and glycol ethers provide strong solvency, controlled volatility, and compatibility with modern environmental regulations, enabling their widespread use in coatings formulations, pharmaceutical processing, adhesives manufacturing, and industrial cleaning applications. Compared with hydrocarbon and halogenated solvents, oxygenated solvents offer lower toxicity profiles, improved biodegradability, and reduced environmental impact, making them attractive to manufacturers facing stricter chemical safety standards. In 2025, regulatory pressure on volatile organic compound (VOC) emissions continues to reshape solvent demand patterns globally. To address evolving regulations, producers have developed low-VOC and regulatory-exempt oxygenated solvent formulations that allow manufacturers to maintain high solvency performance while meeting regional air quality requirements. These innovations have accelerated the substitution of traditional hydrocarbon and halogenated solvents in several industrial formulations.

Paints and Coatings Sector Drives the Largest Demand for Industrial Solvents

Paints and Coatings represented 38.6% of the Industrial Solvents Market share in 2025, establishing the sector as the largest end-use segment for industrial solvent consumption. Solvents play a critical role in coatings formulations by dissolving resins, controlling viscosity, enabling pigment dispersion, and supporting film formation during drying, making them essential components of both solvent-borne and waterborne coatings systems. The global scale of architectural coatings, industrial coatings, automotive paints, and protective coatings drives substantial demand for solvents used during formulation, application, and curing processes. In 2025, the coatings industry continues shifting toward waterborne coatings technologies, driven by regulatory pressure to reduce VOC emissions and improve environmental performance. This transition has increased demand for coalescing solvents and specialty oxygenated solvents that support film formation and surface leveling in water-based coatings systems. Ester alcohols and glycol ethers are particularly important in these formulations, enabling coatings to achieve improved drying performance, enhanced film integrity, and consistent application at lower ambient temperatures, supporting the growing adoption of environmentally compliant coatings technologies across the global construction and manufacturing sectors.

Competitive Landscape in Industrial Solvents Market

BASF SE Strengthens Feedstock Integration and Expands in High-Growth Regions

BASF SE remains a dominant force in the industrial solvents market, leveraging its proprietary Verbund production model to optimize raw material utilization and energy efficiency across interconnected plants. The company extends strong position in acrylates, alcohols, esters, and specialty solvent intermediates. In March 2026, BASF announced price increases of up to $100 per metric ton for butyl acrylate and 2-ethylhexyl acrylate in the Asia-Pacific region to counter rising logistics and energy costs. The February 2026 expansion of dispersions capacity at its Mangalore, India site reinforces its strategic push into high-growth emerging markets with rising coatings and construction demand. The divestiture of its optical brightening agent business to Catexel sharpens focus within the Care Chemicals division on core industrial solvent applications. With 2025 group sales of approximately €60 billion and a 2026 EBITDA target between €6.2 billion and €7.0 billion, BASF continues to anchor its competitive edge through operational scale and financial resilience.

Dow Inc. Accelerates Digital Transformation to Improve Specialty Solvent Margins

Dow Inc. is executing a large-scale structural transformation aimed at reinforcing its leadership in specialty chemicals and industrial solvent derivatives. In January 2026, the company launched its Transform to Outperform program, targeting at least $2 billion in near-term operating EBITDA gains through AI-driven automation, operational simplification, and digital integration. Dow operates manufacturing facilities in 29 countries with approximately 34,600 employees and has set a $500 million in-year EBITDA improvement goal for 2026. The restructuring includes a projected reduction of roughly 4,500 roles globally, reflecting cost-reset initiatives to navigate cyclical demand softness in coatings, construction chemicals, and packaging. By modernizing customer service systems and deploying advanced process analytics, Dow aims to enhance margin performance across solvent-based formulations and industrial intermediates. The transformation reinforces its competitiveness in oxygenated solvents, glycols, and performance chemicals amid structural industry headwinds.

Shell Chemicals Leverages Vertical Integration to Maintain Cost Leadership

Shell Chemicals market growth is supported by deep integration with upstream oil and gas operations. Its vertical integration model ensures stable hydrocarbon feedstock supply, enabling cost leadership in hydrocarbon and oxygenated solvent segments. Shell’s extensive refining and petrochemical infrastructure provides resilience against crude price volatility and supply chain disruptions. In early 2026, the company released its Energy Security Scenarios, highlighting how AI-driven industrial transitions and lower-carbon chemical pathways will reshape solvent manufacturing. Strategic investments in India and other high-growth Asian markets are strengthening its LNG and downstream chemical footprint to capture rising demand in paints, adhesives, and industrial cleaning solvents. Aligned with its net-zero emissions target by 2050, Shell is progressively redirecting capital toward lower-carbon intermediates and specialty solvent applications.

ExxonMobil Product Solutions Focuses on High-Purity Hydrocarbon Solvents

ExxonMobil Product Solutions specializes in ultra-high-purity hydrocarbon fluids marketed under the Exxsol™ and Isopar™ brands. Its refining circuit, reportedly twice the size of other major international oil companies, provides strong reliability in solvent consistency and specification control. The company’s Exxtend™ advanced recycling technology processed 40,000 metric tons of plastic waste in 2025 and targets 500,000 metric tons annually by 2027, reinforcing its position in solvent-mediated recycling and circular polymer solutions. Ongoing investments across the U.S. Gulf Coast, Singapore, and China are aimed at expanding value-accretive, non-combusted product lines. ExxonMobil holds a 9.1 out of 10 reliability rating in analyst surveys, particularly for Odorsolv technologies used in indoor industrial cleaning and sensitive applications requiring low odor and high purity.

Celanese Corporation Enhances Cash Discipline and Specialty Acetyl Leadership

Celanese Corporation is a leading producer in the acetyl chain, supplying acetic acid, vinyl acetate monomer, and ester solvents for coatings, adhesives, and chemical intermediates. In February 2026, Celanese completed the $500 million sale of its Micromax business to Element Solutions Inc., directing proceeds toward deleveraging initiatives. Shortly after, the company announced regional price increases of up to $100 per metric ton for acetic acid, VAM, and ester derivatives due to feedstock and energy cost escalation in the Western Hemisphere. Reporting 2024 net sales of $10.3 billion and employing over 11,000 personnel globally, Celanese is reinforcing its balance sheet while expanding its sustainable product portfolio. The strategic focus on cash generation, disciplined capital allocation, and eco-conscious solvent technologies enhances its competitiveness in specialty industrial solvent applications.

Arkema S.A. Advances Specialty Solvent Innovation and Circular Materials

Arkema S.A. has repositioned itself as a pure-play specialty materials company, concentrating on advanced solvent-based solutions for electronics, coatings, and automotive industries. The company reported a resilient 2025 EBITDA of €1,251 million with a 13.8% margin, and it targets slight EBITDA growth in 2026 despite subdued demand in Europe and the United States. Three major capacity expansions initiated in late 2025, including Rilsan Clear production in Asia, are expected to contribute approximately €50 million in additional EBITDA in 2026. Arkema plans a 3% annual headcount reduction over three years while maintaining capital expenditure at around €600 million in 2026 to enhance organizational efficiency. Its Elium resins play a central role in industrial-scale recycling of thermoplastic composites, strengthening its sustainability credentials within the industrial solvents and specialty chemicals ecosystem.

United States Industrial Solvents Market: Onshoring, EV-Driven Formulation Shifts, and Digitalized Production

The United States industrial solvents market is being reshaped by supply chain localization, electrification-led formulation changes, and regulatory-backed modernization of manufacturing assets. Under the 2025 Federal Supply Chain Task Force directives, Eastman Chemical Company and Univar Solutions have prioritized onshoring high-purity and ultra-high-purity solvents to secure domestic supply for sub-2nm semiconductor fabrication. This strategic pivot reduces exposure to cross-border logistics risks while aligning solvent purity with advanced photolithography and wafer-cleaning requirements. Pricing discipline has also emerged as a structural lever. In March 2025, Eastman implemented targeted price increases for key solvent grades such as Eastman DB and EB, reflecting sustained pressure from feedstock volatility and higher operating costs across the North American corridor.

At the formulation and operations layer, sustainability and performance are converging. Afton Chemical launched HiTEC 35701 in late 2025, a specialized solvent-additive package for eAxle systems that delivers enhanced copper protection in both liquid and vapor phases for electric vehicles. Capacity investments support these shifts. BASF finalized a significant expansion supplying the North American market to increase aminic antioxidant output and specialty solvent intermediates, with full operations expected by late 2026 to meet stability requirements of modern industrial lubricants. In parallel, EPA-issued onshoring grants exceeding $150 million through 2025 are accelerating Smart Factory upgrades that integrate AI-driven monitoring to reduce solvent losses and fugitive emissions. Bio-based feedstocks are gaining traction as Vertec and Tedia expanded portfolios in 2025 with corn, soybean, and citrus-derived solvents for pharmaceutical and agricultural applications.

China Industrial Solvents Market: Policy-Led Upgrading, VOC Controls, and Traceable Supply Chains

China’s industrial solvents industry is advancing through a coordinated policy framework that prioritizes value-added upgrading, emissions control, and lifecycle traceability. In September 2025, the Ministry of Industry and Information Technology issued a petrochemical growth blueprint targeting a sustained increase in sector value while mandating the transition from bulk solvent sales to integrated, high-end chemical solutions. This directive is reinforced by regulatory enforcement. From June 1, 2026, the State Administration for Market Regulation will enforce GB 30981.1-2025, imposing stricter VOC and hazardous substance limits on coatings and related solvent systems, accelerating adoption of water-based and high-solid formulations across industrial users.

Environmental substitution timelines are also firm. Effective July 1, 2026, the Ministry of Ecology and Environment will prohibit hydrochlorofluorocarbons as cleaning agents, catalyzing a shift toward hydrofluoroethers and fluorinated olefins in electronics manufacturing. Capacity investments underpin compliance and growth. BASF is progressing its Zhanjiang Verbund site, with methyl glycols production slated to begin by late 2025 to supply brake fluids and industrial intermediates across Asia-Pacific. Governance mechanisms are tightening as Shanghai and other hubs implement the One Enterprise One QR Code policy, enabling real-time tracking of hazardous solvents from production through disposal, elevating compliance and audit readiness.

European Union Industrial Solvents Market: REACH Restrictions, Circularity, and Data Center Fluids

Across Germany and the Netherlands, the industrial solvents market is aligning with tighter occupational exposure limits, circular economy objectives, and emerging digital infrastructure needs. Regulation (EU) 2025/1090 updates REACH Annex XVII to restrict DMAC and NEP, effective December 23, 2026, requiring products containing at or above 0.3% to meet legally binding DNEL thresholds. This has accelerated reformulation programs and substitution screening across industrial solvent portfolios.

Circularity is moving from pilot to scale. BASF and EU partners signed a 2025 memorandum to advance high-purity regeneration of spent solvents, supporting the EU’s 2030 zero-pollution ambition while reducing reliance on virgin feedstocks. Product innovation reflects adjacent demand growth. Shell introduced Direct Liquid Cooling Fluid S3 in June 2025 in Houston and London, a dielectric solvent designed for immersion cooling of AI and high-performance computing data centers. At the same time, Evonik and Clariant expanded ISCC PLUS certified capacity in Germany to produce rhamnolipid-based biosurfactants as drop-in replacements for petroleum-derived solvents.

India Industrial Solvents Market: Investment-Led Capacity and Digital Formulation Development

India’s industrial solvents landscape is strengthening through large-scale investments and digital innovation platforms that support lower-carbon chemistries. Lubrizol announced a $200 million investment in an Aurangabad facility, with completion targeted across 2025–2026, to manufacture high-performance additives and solvents serving domestic and Middle Eastern industrial markets. The site is designed to integrate advanced quality control and export-oriented logistics, improving regional supply resilience.

Innovation capabilities are being reinforced by ecosystem investments. Chevron established its $1 billion Engineering and Innovation Excellence Center in Bengaluru in 2025. The center focuses on developing lower-carbon solvent formulations and digitalizing chemical supply chain workflows, including predictive analytics for solvent efficiency and emissions reduction. Together, these moves position India as a formulation and engineering hub for next-generation industrial solvents.

Industrial Solvents Industry: Country-Level Strategic Summary

Industrial Solvents Market County Level Snapshot

|

Region

|

Primary Policy or Demand Driver

|

Key Industrial Response

|

Structural Direction

|

|

United States

|

Semiconductor onshoring, EV electrification

|

High-purity solvent localization, bio-based expansion, Smart Factory upgrades

|

Supply security with performance-led reformulation

|

|

China

|

Value-added upgrading, VOC and HCFC controls

|

Water-based systems, HFEs, traceable solvent lifecycles

|

Policy-driven modernization at scale

|

|

European Union

|

REACH restrictions, circular economy

|

Solvent regeneration, biosurfactants, data center fluids

|

Low-toxicity, circular solvent systems

|

|

India

|

Investment-led capacity, digital innovation

|

New manufacturing hubs, lower-carbon formulations

|

Export-ready growth with engineering focus

|

Industrial Solvents Market Report Scope

Industrial Solvents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.3 Billion

|

|

Market Size (2034)

|

$16.3 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Product Type (Oxygenated Solvents, Hydrocarbon Solvents, Halogenated Solvents, Bio-Based and Green Solvents), By Function (Dissolution and Dispersion, Cleaning and Degreasing, Chemical Intermediates, Surface Preparation, Cooling and Heat Transfer), By End-Use Sector (Paints and Coatings, Pharmaceuticals and Healthcare, Electronics and Semiconductors, Adhesives and Sealants, Printing Inks, Agrochemicals)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Exxon Mobil Corporation, Shell plc, Dow Inc., Eastman Chemical Company, LyondellBasell Industries N.V., Chevron Phillips Chemical Company, Solvay S.A., Arkema S.A., Univar Solutions, Lubrizol Corporation, Huntsman Corporation, Clariant AG, Shin-Etsu Chemical Co., Ltd., Sinopec

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Solvents Market Segmentation

By Product Type

- Oxygenated Solvents

- Alcohols

- Ketones

- Esters

- Glycols and Glycol Ethers

- Hydrocarbon Solvents

- Halogenated Solvents

- Bio-Based and Green Solvents

By Function

- Dissolution and Dispersion

- Cleaning and Degreasing

- Chemical Intermediates

- Surface Preparation

- Cooling and Heat Transfer

By End-Use Sector

- Paints and Coatings

- Pharmaceuticals and Healthcare

- Electronics and Semiconductors

- Adhesives and Sealants

- Printing Inks

- Agrochemicals

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Industrial Solvents Industry

- BASF SE

- Exxon Mobil Corporation

- Shell plc

- Dow Inc.

- Eastman Chemical Company

- LyondellBasell Industries N.V.

- Chevron Phillips Chemical Company

- Solvay S.A.

- Arkema S.A.

- Univar Solutions

- Lubrizol Corporation

- Huntsman Corporation

- Clariant AG

- Shin-Etsu Chemical Co., Ltd.

- Sinopec

*- List not Exhaustive