Market Overview: Bio-Ketones Market Acceleration Through Fermentation Platforms, Sustainable Aviation Fuel Pathways, and High-Performance Bio-Polymers (2025–2034)

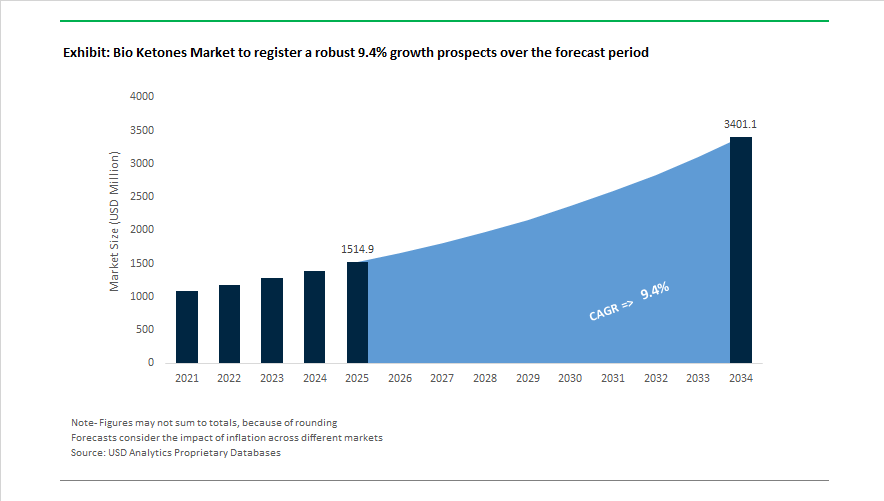

The bio ketones market is projected to expand from USD 1,514.9 Million in 2025 to USD 3,400.5 Million by 2034, reflecting a CAGR of 9.4% driven by rapid scale-up of bio-based chemical intermediates, sustainable polymers, green solvents, and next-generation fuels. Bio-ketones are emerging as critical building blocks derived from fermentation, biomass conversion, and renewable carbon feedstocks, replacing fossil-based ketone routes in performance materials, specialty chemicals, and energy applications. Industrial scale deployment accelerated in 2024 when Westlake Epoxy secured ISCC PLUS certification in Germany, enabling bio-attributed epoxy systems incorporating renewable ketone intermediates. In April 2024, nutraceutical startup KEY introduced a ketone-based energy drink following $4 million funding, highlighting expanding consumer applications for bio-derived metabolic compounds. Momentum intensified in October 2025 when Geno and Qore began operations at the world’s largest bio-BDO plant in Iowa, establishing fermentation infrastructure that underpins broader bio-ketone and bio-glycol value chains for sustainable textiles and packaging.

Advanced materials and fragrance sectors are accelerating bio-ketone adoption. In October 2025, Syensqo received the Bosch Global Supplier Award for its sustainable polymer portfolio. The company further gained recognition in November 2025 at the SPE Innovation Awards for bio-sourced MTM resins enabling 40% weight reduction in structural automotive parts. In January 2026, Syensqo introduced AvaSpire PAEK compounds in partnership with Uniwell Rohrsysteme for Grohe plumbing systems, demonstrating bio-ketone polymer penetration into durable infrastructure components. Fragrance applications are also scaling. In November 2025, Givaudan launched biodegradable PlanetCaps fragrance encapsulation and announced Singapore capacity expansion by Q1 2026, while committing $110 million in February 2026 to a Mexico facility focused on aroma chemicals including bio-derived ketones.

Energy transition pathways are creating new high-volume demand streams. In October 2025, India confirmed initial Sustainable Aviation Fuel production at Indian Oil’s Panipat refinery using alcohol-to-jet conversion routes involving bio-ketone intermediates. During 2025, Marubeni Corporation, Boeing Japan, and Obayashi advanced feasibility studies on forest-residue-based SAF and bio-naphtha production. Aerospace material innovation also progressed in December 2025 when Syensqo partnered with Vertical Aerospace to supply bio-based composites and high-performance polymers for electric aircraft structures. Market ecosystem coordination is increasing, highlighted by the November 2025 announcement of BIOKET 2026, a global platform dedicated to industrial deployment of bio-based chemical intermediates. These developments position bio-ketones as a strategic interface between green chemistry, advanced polymers, renewable fuels, and high-performance specialty materials manufacturing.

Trends and Opportunities Reshaping the Bio Ketones Market

Market Trend: Fermentation-Derived Cyclic Ketones Scaling into Engineering Plastics Supply Chains

A core structural transformation in the Bio Ketones Market is the industrialization of microbial and precision fermentation routes that unlock scalable production of cyclic ketones—cyclopentanone and cyclohexanone—used as critical intermediates for polyamide and polyurethane manufacture. This shift is strategically important because bio-derived ketones reduce dependency on fossil aromatics and support carbon footprint reduction across downstream engineering plastics.

In February 2025, International Process Plants (IPP) leased a 40-million-gallon-per-year precision fermentation facility in Minnesota to Nuol Green Chemistry, signaling a move to leverage existing agro-industrial infrastructure rather than build greenfield plants. For downstream pull, Mitsubishi Chemical Group’s September 2025 collaboration with Honda to incorporate recycled and bio-based acrylic resins into automotive exteriors demonstrates a clear market signal: OEMs are willing to adopt bio-ketone-based monomers that meet durability, optical, and mechanical specs required in automotive environments.

Market Trend: Bio-Acetone Positioned as the Strategic Enabler for Sustainable Acrylics and BPA Replacement

Bio-acetone is emerging as a “drop-in” substitute that enables polymer manufacturers to decarbonize Methyl Methacrylate (MMA) and PMMA acrylic glass without capex-heavy process redesign. Its commercial scale-up is being driven by regional industrial policy.

A key example is Celtic Renewables’ December 2025 Scottish Government-backed project in Grangemouth, which converts agricultural residues—including pot ale from whisky distilleries—into bio-acetone using ABE fermentation. This aligns with EU Green Deal Scope 3 compliance pressures, which are forcing polymer and specialty chemical manufacturers to adopt bio-feedstocks to counter exposure to volatile benzene prices (averaging $660/MT in Europe) and rising carbon-reporting requirements in electronics and medical packaging.

Market Opportunity: Bio-MEK for Lithium-Ion Battery Electrode Manufacturing

Gigafactory construction and scale-up is transforming solvent demand profiles. Bio-based Methyl Ethyl Ketone (MEK) presents a commercially viable, high-margin penetration path, given its compatibility with slurry casting and PVDF binder systems in lithium-ion battery electrodes.

Industry data from 2025 shows that switching from fossil MEK to bio-MEK can reduce operational CO₂ emissions of EV cell production by 2 to 5% due to solvent lifecycle improvements. Bio-MEK’s high evaporation rate (3.8 vs. butyl acetate) cuts energy draw from electrode drying ovens, improving line throughput and lowering per-kWh manufacturing cost—an immediate value proposition for players like PowerCo, LG Energy Solution, and North American gigafactory OEMs prioritizing IRA tax-credit eligible supply chains.

Market Opportunity: Levulinic-Derived Ketones Unlocking Non-Phthalate Plasticizers and Sustainable Aviation Fuel Pathways

Levulinic acid is emerging as a strategic platform molecule, enabling the synthesis of high-value ketones such as Gamma-Valerolactone (GVL), 2-MTHF, and MTHF. These molecules provide low-toxicity, low-VOC plasticizer performance required in C.A.S.E. applications (Coatings, Adhesives, Sealants, Elastomers) and offer a pathway into future Sustainable Aviation Fuel (SAF) formulations.

In February 2025, Biofine Technology was granted U.S. Patent No. 12,227,486 for a new biorefinery system that improves levulinic acid and furfural conversion efficiencies, paving the way to cost-competitive levulinic ketones. Technical trials published in 2025 indicate catalysts can now achieve an 87.6% yield converting biomass to 2-MTHF—an emerging SAF blending molecule delivering seal-swelling functionality similar to aromatics while reducing lifecycle jet-fuel carbon intensity by more than 70%.

Bio-Ketones Market Share and Segmentation Insights

Market Share by Source Feedstock: Lignocellulosic Biomass Anchors Supply While Waste Valorization Accelerates

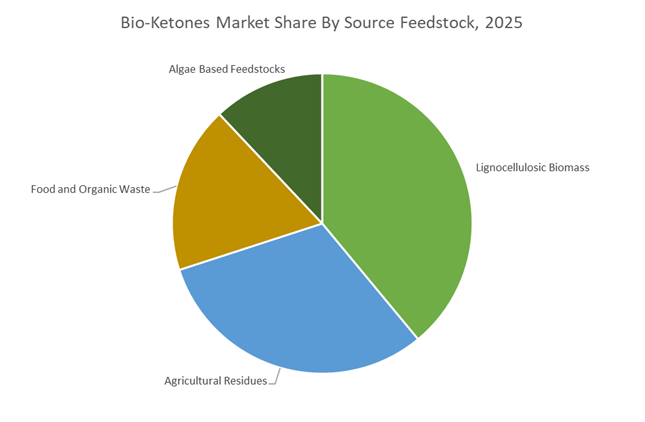

Lignocellulosic biomass leads the Bio-Ketones Market with a 39% share in 2025, supported by abundant availability of wood chips, forestry residues, and energy crops that provide non-food cellulosic sugars for fermentation and thermochemical conversion into bio-acetone and bio-MEK. Government mandates promoting advanced biofuels and low-carbon chemicals continue to reinforce this segment’s dominance. Agricultural residues, including corn stover, wheat straw, and rice husks, hold the second-largest share, benefiting from established collection networks and cost competitiveness across North America and Europe. Food and organic waste is emerging rapidly as a circular economy feedstock, converting municipal solid waste and industrial by-products into renewable ketones via anaerobic digestion and catalytic pathways, accelerated by waste valorization policies. Algae-based feedstocks remain the smallest but most technologically progressive segment, offering high lipid productivity and non-arable land utilization, although elevated production costs currently constrain large-scale commercialization.

Market Share by End User Industry: Automotive Applications Lead While Healthcare and Green Construction Gain Momentum

Automotive and mobility represent the largest end-use segment, accounting for 38% of bio-ketone demand in 2025, driven by rising adoption of bio-acetone and bio-MEK as sustainable solvents in vehicle coatings, adhesives, and lightweight composite manufacturing. Renewable ketones are also being evaluated as blend components for drop-in biofuels, while the EV transition is increasing demand for bio-based interior materials. Food and beverage applications utilize bio-ketones as natural flavoring agents and extraction solvents, with acetoin and bio-based MEK gaining traction in clean-label formulations that command regulatory price premiums. Healthcare and pharmaceuticals are expanding use in API synthesis, drug formulation, and high-purity cleaning, supported by sustainability mandates and supply chain transparency requirements. Construction and infrastructure consume bio-ketones in low-VOC architectural coatings and sealants, reinforced by green building certifications, while aerospace and defense remain niche but high-value adopters for specialty composites, cleaners, and de-icing systems.

Competitive Landscape Analysis of the Bio Ketones Market

The bio ketones market is transitioning from niche green solvents to a strategic pillar of sustainable chemicals, driven by demand from batteries, electronics, pharmaceuticals, coatings, and personal care. Competition is centered on renewable feedstock integration, solvent performance parity with fossil counterparts, closed-loop recovery systems, and regulatory alignment with EU sustainability frameworks. Leading players are differentiating through proprietary bio-ketone platforms, mass balance production models, metabolic-grade APIs, and circular chemistry initiatives. As OEMs and formulators seek low-toxicity, high-solvency alternatives, the market is consolidating around innovators capable of delivering scalable volumes, predictable purity, and application-specific bio-ketone solutions across energy storage, life sciences, and specialty materials.

Circa Group pioneers levoglucosenone-based ketone solvents with Cyrene

Circa Group is the technology originator of the levoglucosenone platform, effectively creating the high-performance bio ketone solvent segment. Its flagship Cyrene solvent, derived from waste cellulose, has emerged in 2026 as a leading bio-alternative to NMP, outperforming fossil solvents in graphene dispersion and battery electrode coating. Circa launched its ReGeN closed-loop recovery system in early 2026, enabling up to 95% solvent recycling and materially lowering total ownership costs. The company’s Reuven Plant in France is scaling toward 1,200 tpa capacity, with long-term expansion targets of 80,000 tpa via regional hubs. Strategically, Circa is advancing second-generation LGO derivatives through its Renewable Chemistry Institute partnership.

KetoLipix Therapeutics advances pharmaceutical-grade bio ketones through proprietary ester platforms

KetoLipix Therapeutics leads the medical bio-ketone segment, transforming ketone esters into regulated pharmaceutical APIs. Backed by IOI Oleo heritage, the company controls the world’s largest ketone ester library with fourteen patent families. Its 2026 portfolio focuses on sustained-release ketone esters designed for epilepsy and cardiometabolic health, using core-shell delivery to mask taste while ensuring predictable PK/PD profiles. Unlike consumer nutrition brands, KetoLipix targets metabolic state induction via standardized medical formulations. In early 2026, the company launched an advanced drug discovery pipeline to industrialize non-toxic bio-based building blocks, positioning itself at the intersection of oleochemistry and clinical pharmacology.

BASF scales mass-balance bio ketones through Verbund and digital optimization

BASF integrates bio-based feedstocks into its oxygenated solvents portfolio using its Verbund infrastructure and mass balance production model. In 2026, BASF expanded bio-certified acetone and MEK by co-processing bio-naphtha in existing steam crackers. The company introduced its Scope 3.1 Supplier Management Program to enforce verified product carbon footprint standards across bio-ketone precursors, aligned with EU Battery Passport requirements. High-purity bio-acetone is increasingly supplied to electronics and semiconductor cleaning applications. Through its Global Digital Hub in Hyderabad, BASF applies AI to dynamically optimize renewable versus fossil feedstock blends, enabling customer-specific green premia and reinforcing leadership in digitally enabled sustainable solvents.

Solvay expands green chemistry ketones for batteries and personal care

Solvay is strengthening its position in green chemistry solvents, extending its Augeo portfolio into bio-based ketone intermediates for fragrance, cleaning, and advanced materials. In early 2026, Solvay transitioned its Bad Wimpfen site into a center for automotive and battery chemicals, emphasizing bio-derived electrolyte additives and ketone-based binders. The company’s bio ketones are gaining traction in high-voltage environments, supporting stable SEI layer formation in sodium-ion and lithium-metal batteries. Solvay’s 2026 roadmap prioritizes circular performance, launching fully biodegradable bio-ketone formulations compliant with Safe and Sustainable by Design principles, reinforcing its leadership in low-toxicity, high-solvency alternatives.

Neste supplies renewable feedstocks enabling drop-in bio ketone production

Neste is leveraging its global leadership in renewable fuels to become a critical upstream supplier of bio-based chemical feedstocks. Its Neste RE platform provides fully renewable raw materials used by partners to manufacture bio-acetone and bio-MIBK in 2026. The company established the world’s first global renewable plastics supply chain with Sony, delivering bio intermediates for consumer electronics. Neste’s Singapore refinery expansion reached full capacity in 2026, increasing availability of renewable propane and butane for oxygenated chemicals. With unmatched feedstock flexibility, Neste converts low-quality waste into cracker-ready inputs, enabling competitively priced drop-in bio ketone solutions for global chemical producers.

Shell Chemicals integrates cellulosic pathways for performance-grade bio ketones

Shell Chemicals has pivoted toward performance chemicals with strong emphasis on bio-based and circular feedstocks. During late 2025 and early 2026, Shell integrated cellulosic ethanol conversion into its oxygenates value chain, generating bio-based ketone precursors from non-food biomass. Its primary 2026 focus is personal care and cosmetics, supplying bio ketones that mirror conventional physical properties, enabling seamless adoption by multinational brands. Under its Horizon Scenario strategy, Shell is developing modular bio-energy systems with CCS, targeting carbon-negative bio ketone solvents by 2030. Organizational restructuring in early 2026 further accelerated commercialization of new bio-based intermediate grades.

United States Bio Ketones Market: Incentivized Bio-Refining and Advanced Materials Pull

The United States bio ketones industry is benefiting from a convergence of federal incentives, precision fermentation infrastructure, and downstream reformulation mandates. As part of the 2024–2025 effort to localize chemical supply chains, the federal government expanded tax credits for facilities using renewable feedstocks such as agricultural residues and food waste to produce bio-based acetone and methyl ethyl ketone. This policy shift is accelerating capital deployment into bio-refining assets that can displace fossil-derived solvents without compromising performance in coatings, adhesives, and industrial cleaning.

Infrastructure scale-up is already visible. In February 2025, International Process Plants finalized the lease of a 40-million-gallon-per-year precision fermentation facility in Little Falls, Minnesota, to Nuol Green Chemistry. The plant is optimized for high-purity bio-acetone and isobutanol, signaling a shift from pilot-scale fermentation to industrial throughput. Regulatory drivers are reinforcing demand. The United States Environmental Protection Agency updated its VOC standards in 2025, compelling industrial paint and coatings manufacturers to reformulate toward non-toxic solvents, with Bio MEK emerging as a preferred substitute. At the technology frontier, U.S. biotechnology firms are deploying enzymatic pathways to generate ketone intermediates for Bio-PEEK, targeting aerospace and medical implant applications. Complementing this, the United States Department of Energy announced USD 120 million in late 2025 for AI-enabled biofoundries capable of one-step synthesis of long-chain bio-ketones, strengthening the country’s leadership in high-value bio-based materials.

India Bio Ketones Market: Policy-Backed Transition from Petrochemicals to Bio-Based Ketones

India’s bio ketones industry is being shaped by an explicit national pivot toward circular biomanufacturing under the BioE3 framework. Approved in August 2024, the BioE3 policy positions biotechnology as a core economic pillar, prioritizing the replacement of conventional petrochemical routes with bio-based industrial models by 2026. This has elevated bio-acetone and related ketones as strategic intermediates for pharmaceuticals, specialty chemicals, and export-oriented manufacturing.

Capital commitments are aligning with this vision. In April 2025, Deepak Chem Tech Limited, a subsidiary of Deepak Nitrite, allocated ₹3,500 crore for a greenfield complex. While initially centered on phenol and acetone, the site is being built with transition-ready infrastructure to integrate bio-based feedstocks and fermentation-derived ketones over time. Ecosystem development is accelerating through institutional support. The Office of the Principal Scientific Adviser announced plans to expand the S&T Clusters initiative from 8 to 25 clusters by 2028, with Gujarat and Maharashtra designated as hubs for specialty bio-aromatics and bio-ketones. Import substitution policies under the Atmanirbhar Bharat program are adding further momentum, with quality control orders and incentives directly targeting domestic production of bio-based solvents for pharmaceutical manufacturing. In parallel, the Department of Biotechnology is co-funding USD 250 million, alongside the World Bank, across 101 projects to strengthen industry–academia collaboration on bio-based intermediates, anchoring long-term capacity creation.

European Union Bio Ketones Market: Regulatory Substitution and Low-Carbon Specialty Chemistry

The European Union bio ketones market is being driven primarily by regulatory pressure and carbon accounting requirements rather than cost arbitrage. In 2025, the European Chemicals Agency imposed a high burden of proof for continued use of traditional petroleum solvents under REACH, sharply increasing compliance costs and accelerating substitution toward bio-ketones with improved toxicological profiles. This has created immediate demand across coatings, inks, and specialty resins.

Policy incentives are reinforcing adoption. The EU Green Deal’s Circular Economy Action Plan, updated for 2026, introduced preferential procurement guidelines for products utilizing ISCC PLUS–certified bio-acetone, particularly in plastics and coatings. Innovation is extending into fragrances and specialty ingredients. In 2025, players within the Symrise and Givaudan-Firmenich ecosystem commercialized a fermentation-derived beta-methyl naphthyl ketone, delivering a 40% lower carbon footprint than synthetic alternatives. France-based Arkema has also expanded its bio-based portfolio, focusing on bio-sourced ketones for high-performance resins used in 3D printing and automotive lightweighting. These developments position Europe as a demand-led market for premium, low-carbon bio ketones.

China Bio Ketones Market: State-Led Bio-Economy Expansion and Electronic-Grade Purity

China’s bio ketones industry is scaling rapidly under centralized bio-economy planning and aggressive digitalization of bioprocesses. The National Plan for the Development of the Bio-economy (2025–2026) explicitly prioritizes green manufacturing routes, leading to fast-tracked capacity additions for fermentation-based acetone in Shandong and Jiangsu. These regions are emerging as large-scale hubs capable of serving domestic solvents demand while lowering lifecycle emissions.

Operational efficiency is a key differentiator. Chinese producers are integrating artificial intelligence into bioreactor management to optimize microbial performance, increase yields, and reduce energy intensity at scale. Downstream demand is shaping product specifications. China is aggressively expanding ultra-high-purity bio-acetone at 99.9% and above for semiconductor cleaning and electronics manufacturing, aligning decarbonization goals with supply chain self-sufficiency. By embedding bio-ketones into electronic-grade chemical supply, China is positioning these materials not as niche green alternatives but as core inputs in strategic industries.

Country-Level Strategic Snapshot: Bio Ketones Industry

Bio-Ketones Market County Level Snapshot

|

Country / Region

|

Strategic Focus

|

Key Developments

|

|

United States

|

Incentives and advanced materials

|

Bio-refining tax credits, precision fermentation scale-up, VOC-driven Bio MEK adoption

|

|

India

|

Policy-led biomanufacturing

|

BioE3 rollout, greenfield transition-ready assets, S&T clusters, import substitution

|

|

EU (Germany/France)

|

Regulatory substitution and low carbon

|

REACH pressure, ISCC PLUS procurement, low-carbon fragrance ketones

|

|

China

|

State-led scale and digitalization

|

Bio-economy plan, AI-driven fermentation, electronic-grade bio-acetone

|

Bio-Ketones Market Report Scope

Bio Ketones Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1514.9 Million

|

|

Market Size (2034)

|

$3400.5 Million

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Product Type (Bio Acetone, Bio Methyl Ethyl Ketone, Bio Polyether Ether Ketone, Bio Methyl Isobutyl Ketone, Specialty Bio Ketones), By Source Feedstock (Agricultural Residues, Food and Organic Waste, Algae Based Feedstocks, Lignocellulosic Biomass), By Purity Grade (Industrial Grade, Pharmaceutical Grade, Electronic Grade), By Application (Sustainable Solvents, Chemical Intermediates, Nutraceuticals and Dietary Supplements, Personal Care and Cosmetics, Pharmaceuticals, Bio Fuels), By End User Industry (Automotive and Mobility, Construction and Infrastructure, Healthcare and Pharmaceuticals, Food and Beverage, Aerospace and Defense)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Genomatica, LANXESS, Eastman Chemical Company, BASF, Nuol Green Chemistry, LG Chem, Mitsui Chemicals, Symrise, Givaudan, Deepak Nitrite, Anupam Rasayan, Celanese Corporation, Solvay, Wuhan Youji Industries, Circa Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bio Ketones Market Segmentation

By Product Type

- Bio Acetone

- Bio Methyl Ethyl Ketone

- Bio Polyether Ether Ketone

- Bio Methyl Isobutyl Ketone

- Specialty Bio Ketones

By Source Feedstock

- Agricultural Residues

- Food and Organic Waste

- Algae Based Feedstocks

- Lignocellulosic Biomass

By Purity Grade

- Industrial Grade

- Pharmaceutical Grade

- Electronic Grade

By Application

- Sustainable Solvents

- Chemical Intermediates

- Nutraceuticals and Dietary Supplements

- Personal Care and Cosmetics

- Pharmaceuticals

- Bio Fuels

By End User Industry

- Automotive and Mobility

- Construction and Infrastructure

- Healthcare and Pharmaceuticals

- Food and Beverage

- Aerospace and Defense

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bio Ketones Industry

- Genomatica

- LANXESS

- Eastman Chemical Company

- BASF

- Nuol Green Chemistry

- LG Chem

- Mitsui Chemicals

- Symrise

- Givaudan

- Deepak Nitrite

- Anupam Rasayan

- Celanese Corporation

- Solvay

- Wuhan Youji Industries

- Circa Group

*- List not Exhaustive