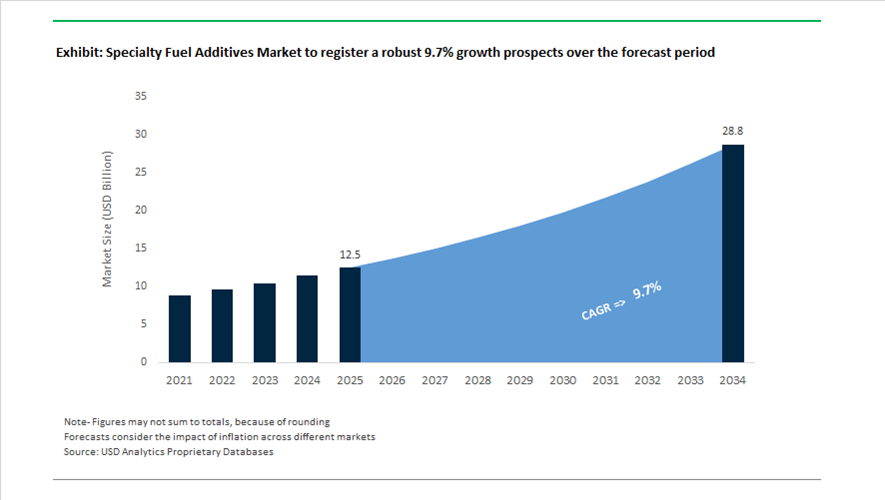

Specialty Fuel Additives Market Valuation 2025–2034: $12.5 Billion to $28.8 Billion at 9.7% CAGR Fueled by Hydrogen Engines, TOP TIER+ Standards, and Renewable Diesel Integration

The global specialty fuel additives market is valued at $12.5 billion in 2025 and is projected to reach $28.8 billion by 2034, expanding at a robust CAGR of 9.7%. Growth is being driven by tighter emission regulations, expansion of renewable diesel and biodiesel blends, hydrogen-powered internal combustion engines, advanced gasoline performance standards, and rising demand for deposit control additives, drag reducing agents (DRAs), cold-flow improvers, cetane enhancers, and corrosion inhibitors. Specialty fuel additives are increasingly engineered to address challenges in Gasoline Direct Injection (GDI), hybrid drivetrains, hydrogen combustion, and low-carbon fuels, while ensuring compliance with ILSAC, TOP TIER+™, and regional decarbonization mandates.

Regulatory-driven innovation accelerated in 2024. In July 2024, The Lubrizol Corporation introduced PV1710, developed to meet upcoming ILSAC GF-7 standards, targeting improved fuel economy, oxidation stability, and deposit control in passenger car engines. In late 2024, Clariant completed its transition to a fully PFAS-free additive portfolio, launching the AddWorks® PPA line as a sustainable processing aid for fuel-contact materials. In May 2024, Chevron Oronite made a Final Investment Decision to expand its Ningbo, China additive facility, with construction commencing in July 2024 and full integration expected in late 2026. Throughout 2024, Chevron completed the operational integration of Renewable Energy Group (REG), strengthening its ability to supply performance additives optimized for renewable diesel and biodiesel blends.

Product innovation intensified in 2025. In August 2025, Afton Chemical launched the HiTEC® 65522 gasoline performance additive series, approved for the new TOP TIER+™ category, engineered to mitigate stochastic pre-ignition (SPI) and injector fouling in GDI engines. In September 2025, Afton Chemical introduced HiTEC® 12582, the world’s first dedicated additive designed specifically for hydrogen-powered heavy-duty internal combustion engines (H2ICE), addressing corrosion, lubrication, and water management challenges unique to hydrogen combustion. In the same month, BASF unveiled its next-generation Keropur® AP 225-20 gasoline performance additive series designed to meet the stringent U.S. TOP TIER+™ standard, with first deliveries scheduled for the first half of 2026.

Capacity expansion and infrastructure-oriented additives are shaping 2026 supply dynamics. In its February 2026 earnings update, Innospec confirmed that its major expansion in Drag Reducing Agents will ramp up in volume through 2026, supporting pipeline efficiency and reducing pumping energy consumption in fuel transport networks. In February 2026, Cabot Corporation completed its acquisition of Mexico Carbon Manufacturing, enhancing regional capabilities for conductive additives used in specialized fuel systems and advanced energy storage. These developments, combined with renewable fuel integration, hydrogen engine chemistry, stricter deposit control standards, and PFAS-free reformulation strategies, are positioning the specialty fuel additives market for sustained double-digit growth momentum toward 2034.

Key Trends and High-Value Opportunities in the Specialty Fuel Additives Market

Mandated Investment in Operability Additives for Renewable Diesel and Sustainable Aviation Fuel

The global scale-up of Renewable Diesel (HVO) and Sustainable Aviation Fuel is structurally redefining demand patterns in the specialty fuel additives market. Regulatory mandates such as the UK’s 2% SAF blending requirement effective January 1, 2025 and the EU’s ReFuelEU Aviation framework have accelerated the commercialization of paraffinic biofuels. However, these fuels inherently lack the aromatic compounds present in fossil fuels, resulting in inferior cold-flow properties, oxidation stability challenges, and material compatibility risks. As a result, additive loading is no longer optional but a prerequisite for regulatory compliance under ASTM and EN fuel specifications.

This shift is driving capital allocation toward downstream “fuel finishing” capabilities. In May 2025, Neste disclosed a €770 million investment across Singapore, Rotterdam, and Martinez, with a strategic emphasis on advanced additive injection and blending systems. These systems are essential to manage cold filter plugging point performance and long-term stability for 100% renewable fuel streams. The cost of compliance is material. According to the International Air Transport Association, SAF compliance costs in Europe reached approximately $1.2 billion in 2025 for one million tonnes of fuel. This economic pressure is pushing refiners toward yield-positive additives that enable the use of lower-quality, high-acidity waste feedstocks without accelerating corrosion or damaging refinery metallurgy. Operability additives have therefore evolved into margin-protection tools rather than simple performance enhancers.

OEM-Led Tightening of Gasoline Direct Injection Deposit Control Standards

The dominance of Gasoline Direct Injection engines has created a non-discretionary demand for advanced detergent and deposit control additives. Unlike port fuel injection systems, GDI architectures are prone to rapid injector and combustion chamber deposit formation, with performance degradation observed in as little as 20,000 miles. This has prompted OEMs and fuel marketers to move beyond minimum EPA requirements toward higher, standardized cleanliness benchmarks.

In 2025, the TOP TIER™ program introduced TOP TIER+™, marking the first major revision since 2005. The updated standard specifically targets GDI-related deposits, requiring fuel marketers to adopt additive packages that pass enhanced real-world performance tests for injector cleanliness and combustion chamber deposits. This development has elevated additive chemistry to a strategic lever for OEM warranty compliance and emissions durability.

Responding to this shift, BASF announced its Keropur Gasoline Performance Additive Series in September 2025. These formulations are engineered to exceed TOP TIER+™ requirements, supporting consistent emissions performance across vehicle lifecycles. The trend underscores how deposit control additives are increasingly specified by OEM-driven standards rather than discretionary fuel marketing claims, embedding long-term demand visibility for specialty additive suppliers.

Lubricity and Material-Protection Additives for Hydrogen Internal Combustion Engines

Hydrogen-fueled internal combustion engines are emerging as a transitional solution for heavy-duty transport decarbonization, particularly in applications where fuel cells remain cost-prohibitive. However, hydrogen introduces a fundamental lubrication and materials challenge. Gaseous hydrogen provides zero inherent lubricity and increases the risk of hydrogen embrittlement in conventional steel fuel system components.

This challenge has catalyzed industry collaboration. In March 2025, Cummins Inc. became a founding member of the Hydrogen Engine Alliance of North America, a consortium focused on resolving material compatibility and durability barriers for H2-ICE platforms. Within this context, specialty fuel additives represent a high-margin opportunity. Additive formulators are developing vapor-phase corrosion inhibitors and mist-lubrication systems that can be introduced into hydrogen fuel streams to protect injectors, pumps, and high-pressure valves. These additive systems command a significant price premium relative to conventional diesel additives, reflecting their critical role in enabling commercial hydrogen combustion without premature equipment failure.

Multi-Functional Additive Systems for Extended Drain Intervals in LNG and Hybrid Marine Vessels

The maritime industry’s transition toward LNG and hybrid propulsion is fundamentally altering engine oil chemistry requirements. LNG combustion generates different acidic byproducts and wear mechanisms compared to heavy fuel oil, while hybrid operations introduce frequent stop-start cycles that accelerate oil degradation. This has created demand for multi-functional additive systems capable of maintaining oil performance under dual-fuel contamination scenarios.

In October 2025, Wärtsilä and TMS Cardiff Gas renewed a five-year lifecycle agreement for LNG carriers built around predictive maintenance and real-time oil condition monitoring. This data-driven maintenance model is increasing reliance on high base number detergents, advanced dispersants, and oxidation inhibitors that can extend oil drain intervals by up to 20% even in hybrid operating profiles.

Simultaneously, regulatory pressure to reduce methane slip under IMO decarbonization targets is elevating the role of fuel and lubricant additives that stabilize combustion and manage high-temperature oxidation. For vessel operators facing rising carbon costs in EU waters, these additive systems are becoming essential tools for compliance, asset protection, and operating cost control rather than optional performance upgrades.

Specialty Fuel Additives Market Share and Segmentation Insights

Deposit Control Additives Lead the Specialty Fuel Additives Market for Engine Performance and Emissions Control

Deposit control additives accounted for 28.40% of the specialty fuel additives market in 2025, reflecting their critical role in maintaining fuel system cleanliness and engine efficiency. These additives prevent the buildup of carbon deposits in fuel injectors, intake valves, and combustion chambers, helping maintain optimal engine performance, fuel economy, and emissions compliance. Deposit control chemistries are particularly important for modern high-pressure fuel injection systems used in both gasoline and diesel engines. A key 2025 technology driver is the increasing adoption of gasoline direct injection (GDI) engines and advanced common rail diesel systems, which require sophisticated detergent formulations such as polyetheramine (PEA) and polyisobutylene amine (PIBA) to manage deposit formation under demanding operating conditions.

Diesel Fuel Applications Drive Global Demand for Specialty Fuel Additives

Diesel represents the largest application segment in the specialty fuel additives market, accounting for 42.80% of global consumption in 2025 due to the widespread use of diesel engines in commercial transportation, heavy machinery, and industrial equipment. Modern diesel fuel systems require comprehensive additive packages that provide lubricity enhancement, cold flow improvement, oxidation stability, corrosion protection, and injector cleanliness. The scale of global diesel fuel consumption supports consistent demand for specialized additive technologies. A significant 2025 market challenge is the increasing adoption of biodiesel and renewable diesel blends, which introduce new formulation requirements related to oxidative stability, cold temperature performance, and deposit control, driving the development of multifunctional additive packages tailored for biodiesel-compatible diesel fuels.

Specialty Fuel Additives Market Competitive Landscape

The global specialty fuel additives market in 2026 is shaped by hydrogen-compatible additives, advanced detergency systems, and hybrid fuel optimization. Leading players are investing in sustainable fuel chemistries, regional blending hubs, and OEM-aligned formulations to support ICE efficiency, SAF adoption, and next-generation mobility solutions.

Afton Chemical Expands Hydrogen Engine Additives and GDI Performance Solutions with HiTEC® Portfolio Innovation

Afton Chemical Corporation is advancing its leadership in specialty fuel additives through targeted innovation for both hydrogen and gasoline engines. The launch of HiTEC® 12582 establishes the first dedicated additive for hydrogen heavy-duty engines, addressing corrosion resistance and water management challenges. Its HiTEC® 65522 series aligns with TOP TIER+™ standards, optimizing performance in GDI engines that dominate new vehicle production. Expansion of its Singapore facility enhances regional blending capabilities and reduces supply lead times in Asia-Pacific markets. Afton’s OEM partnerships and proprietary testing data enable development of region-specific fuel additive solutions. Its focus on bridging traditional and alternative fuels strengthens its competitive positioning.

BASF Strengthens Fuel Additive Portfolio with Keropur® Innovation and Vertical Integration in Antioxidants Production

BASF SE is reinforcing its specialty fuel additives portfolio through high-performance detergents and antioxidant technologies. The Keropur® AP 225-20 formulation exceeds EPA requirements and supports cleaner combustion ahead of regulatory mandates. Expansion of aminic antioxidant capacity in Mexico addresses demand for fuel stability and long-life lubricants in North America. BASF’s Verbund integration ensures efficient production of polyisobutene-based additives, mitigating feedstock volatility. Its Surface Technologies segment continues to deliver resilience through high-margin specialty solutions. The company’s focus on sustainable fuel additives and vertical integration strengthens its role in advanced fuel chemistries.

Innospec Enhances High-Margin Fuel Specialties Segment with Strong Profitability and Strategic Market Expansion

Innospec Inc. is strengthening its position in specialty fuel additives through its Fuel Specialties segment, which reported a 7% increase in operating income and strong cash reserves. The company’s margin-focused strategy has driven gross margins to 34.7%, supported by a shift toward high-value additive formulations. Strategic initiatives include expansion of its technology pipeline across oilfield services and performance chemicals. Its partnership with the Africa Gifted Foundation aligns growth with emerging fuel infrastructure markets in Africa. Innospec’s agility in niche markets and strong financial position enhance its competitiveness. Its focus on premium additives supports sustained profitability.

Lubrizol Advances Hybrid and NEV Additive Technologies with Regional Innovation Centers and Advanced ATF Solutions

Lubrizol Corporation is expanding its footprint in hybrid and new energy vehicle (NEV) markets through specialized additive technologies. Its Lubrizol® PV1710 platform supports hybrid engine oils with enhanced emulsion stability under ILSAC GF-7 standards. The Lubrizol® AT9311 additive enables multi-vehicle transmission fluid compatibility, improving efficiency and reducing inventory complexity. The Shanghai Innovation Center strengthens localized R&D for the rapidly growing Chinese NEV market. Strategic partnerships in sustainable mining and industrial fluids support diversification into energy transition sectors. Lubrizol’s focus on advanced mobility solutions strengthens its position in evolving fuel additive markets.

Infineum Strengthens Regional Supply Chains and Low-Viscosity Additive Innovation for Modern Engine Requirements

Infineum is reinforcing its leadership in specialty fuel additives through supply chain localization and advanced formulation technologies. Its partnership with Rianlon enables a self-sufficient additive production ecosystem in Asia-Pacific. The launch of Infineum P6188 addresses ultra-low viscosity requirements for modern European engines, improving fuel efficiency and emissions performance. Expansion of blending operations in India supports growing mobility demand in emerging markets. Investments in renewable energy infrastructure enhance sustainability of manufacturing operations. Infineum’s focus on high-spec additive solutions and regional resilience strengthens its competitive advantage.

Chevron Oronite Expands Global Additive Distribution and Heavy-Duty Engine Solutions Through Strategic Partnerships and Research Leadership

Chevron Oronite is strengthening its global presence in specialty fuel additives through strategic distribution partnerships and product integration. Its collaboration with ICONIC Base Oil Solutions enhances market penetration in Brazil, while partnerships in South Africa support growth in emerging regions. The company’s OGA® and OLOA® product lines provide integrated solutions for gasoline and lubricant applications. Ongoing research into gas engine oil formulations focuses on reducing carbon intensity and meeting future performance standards. Its global manufacturing network ensures consistent supply of dispersants and detergents. Chevron Oronite’s integration with its parent energy infrastructure supports large-scale production and innovation.

United States Specialty Fuel Additives Market Anchored by TOP TIER+™ and Alternative Fuels

The United States specialty fuel additives market is undergoing a structural upgrade driven by the transition to the TOP TIER+™ detergent gasoline standard between 2025 and 2026. This shift has elevated baseline performance requirements for detergent treat rates, injector cleanliness, and combustion stability in gasoline direct injection engines. In response, Afton Chemical and BASF introduced the HiTEC 65522 and Keropur AP 225-20 series respectively, both engineered to mitigate stochastic pre-ignition and advanced injector fouling. These formulations reflect a broader U.S. trend toward higher-chroma additive performance to protect downsized, turbocharged powertrains operating under elevated thermal and pressure loads.

Beyond conventional fuels, the U.S. market is emerging as a global testbed for next-generation propulsion additives. In September 2025, Afton Chemical commercialized the world’s first dedicated additive for hydrogen-fueled heavy-duty internal combustion engines, addressing lubrication loss, valve seat recession, and abnormal combustion risks unique to hydrogen. Parallel innovation is unfolding in sustainable aviation fuel, where University of Illinois researchers demonstrated a renewable ethylbenzene additive derived from recycled polystyrene in early 2025, restoring aromatic functionality critical for seal swelling and system lubrication. Strategic alignment with regulators is evident as new additive packages entering the market in 2026 are designed to exceed EPA Lowest Additive Concentration thresholds, reinforcing the United States’ role as a formulation and certification benchmark.

China Specialty Fuel Additives Market Shaped by Scale, Digitalization, and Alternative Blends

China’s specialty fuel additives industry is expanding through a combination of capacity scale-up, digital supply chain controls, and policy-backed alternative fuel adoption. Chevron Oronite is executing a major expansion at its Ningbo facility, scheduled for completion in late 2026, to increase regional supply of high-performance detergents and carboxylate dispersants. This investment reflects sustained demand from China’s vast passenger vehicle fleet and tightening emission norms for heavy-duty diesel applications.

At the formulation level, Ministry of Industry and Information Technology guidance issued during 2024–2025 emphasizes nanotechnology-enabled fuel additives to improve thermal stability and particulate matter reduction in domestic diesel fleets. Supply chain integrity has also become a priority. BASF introduced digitally authenticated Keropur bottles using QR-based verification to counteract counterfeit additives in the aftermarket. Simultaneously, China’s 2025 industrial roadmap prioritizes additives tailored for methanol-gasoline blends and high-concentration biodiesel, accelerating demand for cold flow improvers and oxidative stabilizers capable of operating across diverse provincial fuel standards.

India Specialty Fuel Additives Market Driven by E20 and B20 Blending Targets

India’s specialty fuel additives market is being reshaped by aggressive biofuel blending mandates under the National Policy on Biofuels. The advancement of the E20 ethanol blending target to the 2025–2026 supply year has materially increased demand for corrosion inhibitors, phase separation suppressants, and oxidation stability improvers to address the hygroscopic and solvent characteristics of high-ethanol gasoline. These requirements are pushing additive suppliers to redesign treat packages specifically for BS-VI engine platforms operating on variable ethanol content.

Manufacturing localization is accelerating in parallel. Lubrizol is investing $200 million in a new manufacturing hub in Aurangabad, positioning India as a “Local for Local” supply base for performance additives serving South Asia and the Middle East. Policy support is reinforcing this shift through the Production Linked Incentive scheme for advanced biofuels, which encourages the development of additives compatible with E20 to E100 flex-fuel engines. On the diesel side, India’s pursuit of B20 biodiesel blending by late 2026 is driving demand for high-performance lubricity improvers, particularly for fuels derived from used cooking oil that must meet the wear protection requirements of modern common-rail systems.

Germany Specialty Fuel Additives Market Focused on Climate-Neutral Fuels and Premium Detergency

Germany’s specialty fuel additives sector is closely aligned with Europe’s climate-neutral fuel ambitions and high-performance engine protection requirements. Clariant expanded its collaboration with KBR during 2024–2025 to scale green ammonia as a maritime fuel, including the development of catalysts and additives that improve combustion stability and usable energy density in ammonia-fueled engines. This positions Germany at the forefront of additive chemistry for non-carbon fuels.

Conventional fuel additives remain strategically important. Evonik expanded production of polyisobutene intermediates in 2025, securing supply of critical raw materials for high-molecular-weight dispersants used in premium detergent packages. Regulatory economics are also shifting, as German producers adopt EU Carbon Border Adjustment Mechanism protocols ahead of 2026. The introduction of low-carbon additive labeling and green surcharges tied to renewable electricity usage is reshaping procurement decisions across European fuel marketers.

Mexico Specialty Fuel Additives Market Emerging as a Strategic Antioxidant Hub

Mexico is strengthening its role in the global specialty fuel additives supply chain through targeted capacity investments. In March 2025, BASF announced a major expansion at its Puebla site to increase production of aminic antioxidants, with completion expected in 2026. These additives are critical for extending the service life of lubricants and fuels exposed to higher temperatures and extended drain intervals.

The Puebla investment addresses a global shortage of long-life stabilizers and positions Mexico as a cost-competitive manufacturing base serving North America and export markets. As fuel formulations worldwide incorporate higher bio-content and operate under stricter emission and durability requirements, antioxidant availability has become a strategic constraint, elevating Mexico’s importance within multinational additive supply networks.

Comparative Snapshot: Specialty Fuel Additives Industry by Country

Specialty Fuel Additives Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Drivers

|

Structural Outcome

|

|

United States

|

Engine protection and alternative fuels

|

TOP TIER+™, hydrogen ICE, SAF

|

Global formulation benchmark

|

|

China

|

Scale and fuel diversity

|

Capacity expansion, methanol blends

|

Regional volume leadership

|

|

India

|

Biofuel compatibility

|

E20, B20 mandates, localization

|

Rapid demand expansion

|

|

Germany

|

Climate-neutral fuels

|

Ammonia engines, premium detergents

|

Technology-led differentiation

|

|

Mexico

|

Antioxidant supply

|

Stabilizer shortages, exports

|

Strategic manufacturing hub

|

Specialty Fuel Additives Market Report Scope

Specialty Fuel Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.5 Billion

|

|

Market Size (2034)

|

$28.8 Billion

|

|

Market Growth Rate

|

9.7%

|

|

Segments

|

By Product Type (Deposit Control Additives, Cetane Improvers, Octane Improvers, Lubricity Improvers, Cold Flow Improvers, Antioxidants & Stability Improvers, Corrosion Inhibitors, Anti-Icing Additives, Dyes & Markers), By Application (Gasoline, Diesel, Aviation Fuel, Marine Fuel, Biofuels)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Afton Chemical Corporation, Innospec Inc., BASF SE, Lubrizol Corporation, Infineum International Limited, Chevron Oronite Company LLC, Clariant AG, Evonik Industries AG, Baker Hughes Company, Dorf Ketal Chemicals, TotalEnergies Additives & Special Fuels, LANXESS AG, Dow Inc., Eurenco, Nalco Water

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Fuel Additives Market Segmentation

By Product Type

- Deposit Control Additives

- Cetane Improvers

- Octane Improvers

- Lubricity Improvers

- Cold Flow Improvers

- Antioxidants & Stability Improvers

- Corrosion Inhibitors

- Anti-Icing Additives

- Dyes & Markers

By Application

- Gasoline

- Diesel

- Aviation Fuel

- Marine Fuel

- Biofuels

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Fuel Additives Industry

- Afton Chemical Corporation

- Innospec Inc.

- BASF SE

- Lubrizol Corporation

- Infineum International Limited

- Chevron Oronite Company LLC

- Clariant AG

- Evonik Industries AG

- Baker Hughes Company

- Dorf Ketal Chemicals

- TotalEnergies Additives & Special Fuels

- LANXESS AG

- Dow Inc.

- Eurenco

- Nalco Water

*- List not Exhaustive