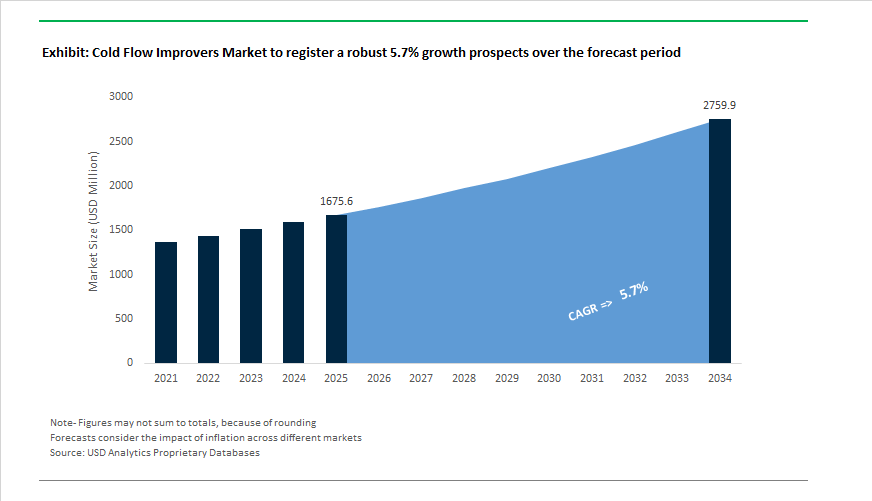

Cold Flow Improvers Market Outlook 2025–2034: $1,675.6 Million to $2,759.6 Million at 5.7% CAGR Driven by Biodiesel Blends and Winter Fuel Compliance

The global Cold Flow Improvers (CFI) Market is projected to expand from $1,675.6 Million in 2025 to $2,759.6 Million by 2034, registering a CAGR of 5.7%. Growth is primarily supported by rising biodiesel blending mandates, tightening Cold Filter Plugging Point (CFPP) specifications, and the increasing operational complexity of diesel engines in sub-zero and high-altitude environments. Cold flow improvers, wax anti-settling agents, pour point depressants, and crystal modifiers are essential in maintaining fuel operability during winter conditions by preventing paraffin wax crystallization and gelling. The shift toward renewable diesel, B100 biodiesel, and hydrogenated vegetable oil (HVO) has introduced new crystallization behaviors that require advanced additive chemistries beyond conventional fossil diesel solutions.

Supply chain localization and capacity expansion intensified in 2024–2026. In November 2024, Infineum announced the expansion of its India operations with a new blending facility, scheduled for trial production in mid-2025 and full-scale output by Q3 2025, strengthening South Asian fuel additive supply chains. Afton Chemical initiated execution of its Ningbo expansion project in July 2024, with completion targeted for late 2026 to support growing Asia-Pacific diesel additive demand. In January 2026, Chevron Oronite partnered with Azelis South Africa to expand distribution of fuel and lubricant additives across Sub-Saharan Africa, targeting transport and power generation markets where seasonal cold performance is increasingly critical. New United States tariffs introduced in 2025 on copolymers and maleic acid derivatives disrupted precursor sourcing, prompting additive producers to adopt localized blending strategies to ensure uninterrupted winter fuel supply in North America.

Product innovation reflects the transition toward renewable fuels and alternative propulsion systems. In 2025, Clariant expanded its DODIFLOW™ and DODILUBE™ portfolio, specifically optimized for B100 biodiesel and HVO applications, addressing the crystallization patterns of saturated fatty acid methyl esters. Evonik confirmed in February 2026 that its VISCOPLEX® cold flow improvers delivered resilient performance across canola, soy, and palm-based biodiesel blends, supporting compliance with strict EU CFPP standards. In March 2025, Innospec launched the LaZuli™ product line certified for deepwater subsea production, leveraging wax modification expertise to prevent gelling and hydrate formation in extreme environments. Afton Chemical introduced HiTEC® 12582 in September 2025, the first commercially available additive designed for hydrogen heavy-duty internal combustion engines, signaling strategic diversification of traditional CFI manufacturers into hydrogen propulsion technologies.

Quality certification, sustainability positioning, and portfolio realignment continue to shape competitive dynamics. Innospec’s Oklahoma City manufacturing center achieved ISO 9001:2015 certification in Q4 2024, reinforcing quality assurance for its fuel and oilfield additive technologies. BASF received EcoVadis Gold status in June 2024, placing it among the top 5% of chemical producers for sustainability performance, strengthening demand for mass-balance certified additives. Clariant reported a 12% reduction in greenhouse gas emissions in October 2025, enhancing the marketability of its Green CFI solutions. In October 2025, BASF completed the sale of its decorative paints business to refocus capital on industrial additives, including refinery chemicals and fuel performance improvers. These developments indicate sustained mid-single-digit growth through 2034, supported by biodiesel mandates, renewable fuel complexity, localized manufacturing strategies, and decarbonization-aligned additive innovation across global refining markets.

Cold Flow Improvers (CFI) Market Trends and Drivers

Tailored Cold Flow Improvers for High-Content Biodiesel Blends (B20+) Driving Feedstock-Specific Formulation Demand

The rapid expansion of bio-diesel adoption under U.S. EPA Renewable Fuel Standard (RFS) and EU RED III mandates is now forcing a structural transition away from generic CFIs toward chemically tailored packages optimized for various fatty-acid profiles. Biodiesel’s crystallization behavior varies sharply across FAME-based fuels, making additive precision a competitive differentiator rather than a formulation afterthought.

According to August 2025 bio-fuel crystallization studies, most commercial CFIs can reduce the pour point (PP) of B20 to ≤ −36°C at a 200% loading rate; however, performance diverges strongly by ester type—with mustard ethyl esters showing a 19.4°C PP reduction versus only 7.2°C for methyl esters. This underscores a market shift toward feedstock-specific polymer chemistry, where additive design increasingly dictates fleet operability in winter conditions.

Industry players are scaling capacity to meet new formulation needs. Evonik’s PAMA production expansion (2023–2024) signals aggressive investment in polymethacrylate-based CFIs, which provide superior wax-crystal modification in heterogeneous B20+ blends—positioning polymeric CFIs as a strategic input for fuel distributors seeking SBTi-aligned decarbonization while maintaining cold-weather operability.

Arctic-Grade CFIs Enabling Energy Security and Cold-Region Logistics Expansion

As global supply chains extend into sub-polar shipping lanes, and energy security strategies expand military readiness in extreme-temperature territories, demand is rising for Arctic-grade CFIs engineered for performance far below conventional winter-diesel standards.

Producers such as Clariant are commercializing Wax Anti-Settling Flow Improvers (WAFIs)—leveraging co-crystallization and electrostatic repulsion mechanisms—designed to prevent wax-cake accumulation in fuel filters at −40°C to −50°C. These developments are crucial for Northern Sea Route maritime fleets, remote mining fleets, and off-grid power systems in polar regions, where engine stalling equates to operational and safety risk.

By December 2025, energy intelligence reports indicate a second-wave adoption of 3rd-generation multifunctional CFIs, combining cold-flow improvement + cetane-boosting functionality—ensuring instant ignition response in sub-zero military, marine, and emergency-response vehicles. Strategically, CFIs are evolving from operability enhancers into mission-critical fuel reliability technologies.

Aviation-Grade CFIs to Support Global SAF Blending Mandates and Fuel Freeze-Point Compliance

The aviation sector represents a high-margin frontier for CFIs due to rising SAF (Sustainable Aviation Fuel) obligations. Under the EU ReFuelEU Aviation mandate (January 2025), 2% SAF blending is required, scaling to 6% by 2030, fundamentally altering jet-fuel thermal-flow requirements.

SAF—particularly HEFA-based fuels—carries a modified hydrocarbon distribution compared to Jet-A1, demanding specialized CFIs that keep freeze-point < −47°C to protect high-altitude fuel lines where temperatures plummet during transcontinental operations.

Strong supply-chain signals validate scaling opportunity: as of November 2025, Neste’s Singapore SAF refinery is supplying commercial volumes to APAC airports, while Singapore and Japan have SAF roadmaps entering enforcement in 2026–2027—implying a measurable procurement pathway for ASTM-approved aviation-grade CFIs.

Cold-Stability Solutions for Bio-Based and Synthetic Paraffinic Fuels (HVO) in Heavy-Duty and Backup Power Systems

The rise of HVO Renewable Diesel, a paraffinic fuel with 100% sulfur elimination and an 85% reduction in particulate matter, represents a forecastable surge in additive demand due to HVO’s unique crystallization pattern.

In 2025, the global HVO market reached US$18.12 billion, projected at 12.8% CAGR through 2027, driven by decarbonization mandates and OEM fleet conversion. However, in cold or static storage environments—such as mining vehicles, agricultural equipment, hospitals, and data-center emergency generators—paraffinic wax precipitation presents a failure risk.

Cold Flow Improvers Market Share and Segmentation Insights

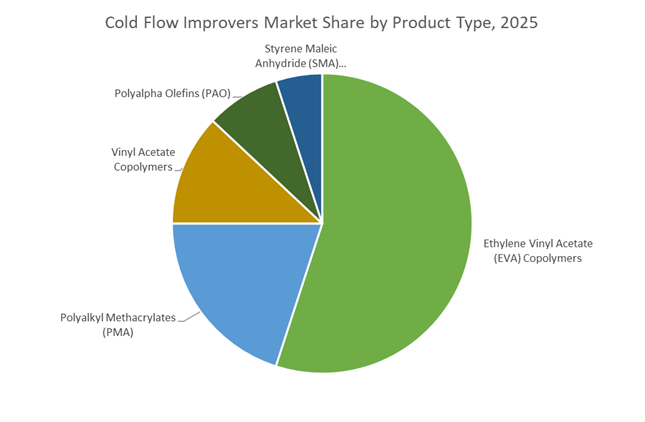

Product Type Dynamics: EVA Copolymers Dominate as Biodiesel Compatibility Drives Additive Innovation

Ethylene Vinyl Acetate (EVA) copolymers lead the Cold Flow Improvers Market with 55% share in 2025, serving as the industry benchmark for modifying wax crystal morphology in middle distillate fuels. Their proven ability to improve cold filter plugging point (CFPP) and pour point across diesel and biodiesel blends makes EVA the preferred choice for refinery-scale fuel conditioning. Polyalkyl methacrylates (PMA) represent the second-largest segment, valued for dual functionality, delivering both cold flow performance and lubricity enhancement that protects fuel injection systems during winter operation. Vinyl acetate copolymers are gaining traction alongside rising FAME blending mandates, as they effectively manage complex wax structures in biodiesel-rich fuels. Styrene maleic anhydride (SMA) copolymers and polyalpha olefins (PAO) occupy niche positions, primarily used in premium additive packages and extreme cold formulations such as arctic-grade diesel and aviation turbine fuels requiring ultra-low temperature operability.

End-User Industry Distribution: Refineries Anchor Demand While Transportation Drives Seasonal Consumption

Oil refineries and fuel terminals account for 48% of cold flow improver consumption, as additives are typically introduced at distribution points to ensure compliance with regional winter fuel specifications before retail delivery. Automotive and transportation fleets form a major secondary market, particularly in cold climates, where logistics operators and trucking companies rely on supplemental cold flow improvers to prevent fuel gelling, filter blockage, and vehicle downtime. Industrial and power generation users depend on these additives to maintain reliability of backup generators and burners during cold snaps, safeguarding manufacturing continuity and data center operations. Aerospace and defense represent a specialized segment, requiring tailored cold flow technologies for jet fuels and military vehicles operating in sub-zero environments, where conventional diesel formulations would otherwise fail, reinforcing demand for high-performance specialty additive systems.

Competitive Landscape of the Cold Flow Improvers Market

The Cold Flow Improvers Market is led by fuel additive specialists and integrated chemical majors advancing paraffin inhibition, pour point depressants, and biodiesel-compatible CFI technologies. Competitive differentiation centers on MDFI performance, renewable fuel compatibility, digital refinery services, and ZeroPCF-aligned formulations. Market leaders are expanding capacity in cold-climate logistics corridors, deploying IoT-enabled dosing systems, and launching hybrid additive packages that combine cold flow, lubricity, and cetane enhancement. Strategic priorities increasingly focus on Arctic fuel reliability, HVO and FAME optimization, and next-generation solutions for sustainable aviation fuel and hydrogen-powered fleets.

BASF scales Basoflux and Keroflux capacity to dominate Arctic-grade diesel performance

BASF remains a dominant force in cold flow improvers through its Basoflux® and Keroflux® product families, widely regarded as industry benchmarks for middle distillate flow improvement. During late 2024 and throughout 2025, BASF announced major capacity expansions for paraffin inhibitors to support oil and gas logistics in Arctic and sub-Arctic regions. The company also introduced bio-based paraffin inhibitors aligned with its ZeroPCF roadmap and EU Green Deal requirements for 2026. Strategically, BASF is integrating digital twins into refinery services, enabling predictive modeling of additive response by fuel batch before shipment, strengthening winter-grade diesel reliability and operational efficiency.

Innospec strengthens renewable fuel compatibility with B100-specific pour point solutions

Innospec operates as a pure-play fuel performance specialist, delivering highly tailored cold flow packages for biodiesel and HVO applications. Its core strength lies in addressing crystallization challenges associated with FAME and renewable diesel blends. The company recently expanded blending facilities across Asia-Pacific to capture rising winter-grade diesel demand from logistics hubs. In 2026, Innospec launched the PPD-Bio Series, engineered specifically for B100 biodiesel fuels. With manufacturing and R&D operations spanning more than 20 countries, Innospec supports ASTM D975 and EN 590 compliance, positioning itself as a preferred partner for low-temperature operability in next-generation fuel systems.

Clariant advances terpolymer CFIs with IoT-driven refinery dosing platforms

Clariant is recognized for its technically advanced DODIFLOW™ and DODILUBE™ brands, offering over 100 tailored DODIFLOW grades matched to specific crude slates and distillate ranges. The company holds strong differentiation in Wax Anti-Settling Additives, preventing wax sedimentation in storage tanks, a critical requirement for standby generators and data centers. In 2025, Clariant expanded its Refinery Services model with automated IoT-based dosing systems that dynamically adjust CFI levels using ambient temperature forecasts. Recent innovation includes DODIFLOW™ 5603, designed to handle high-saturation methyl esters in 2026-grade biofuels.

Infineum delivers integrated hybrid additives for premium winter diesel compliance

Infineum, backed by the combined refining expertise of Shell and ExxonMobil, commands a significant share of the concentrated diesel CFI segment. Deep vertical integration with major refineries enables real-world validation of cold flow performance under commercial operating conditions. Its Sustainability in Motion strategy focuses on enabling lower-grade, high-wax feedstocks while maintaining premium winter specifications. In 2026, Infineum expanded its hybrid additive portfolio, introducing one-pack solutions that combine cold flow improvement with lubricity and cetane enhancement. This integrated approach supports cost optimization while improving low-temperature operability across global diesel supply chains.

Afton Chemical targets trucking and hydrogen fleets with HiTEC cold flow technologies

Afton Chemical, operating under the HiTEC® brand, specializes in performance fuel additives for on-road and off-road markets. Its HiTEC® 4500 series delivers strong Cold Filter Plugging Point performance in ultra-low-sulfur diesel, supporting North America’s trucking sector where temperature volatility is extreme. In September 2025, Afton launched a dedicated CFI solution for hydrogen internal combustion engines, addressing lubrication and flow challenges in emerging H2-powered heavy-duty fleets. The company’s patented GreenClean™ 3 detergent technology is frequently bundled with CFIs to prevent injector deposits while maintaining fuel fluidity in sub-zero environments.

Evonik expands PAMA production to support SAF and high-altitude fuel reliability

Evonik leads Polyalkyl Methacrylate technology through its VISCOBASE® and VISCOPLEX® platforms, delivering dual viscosity index improvement and cold flow enhancement. In late 2025, Evonik commissioned a new PAMA production line in Singapore to serve Southeast Asia’s accelerating industrial fuel demand. Effective May 2026, the company streamlined distribution to focus on specialty niches such as aviation jet fuel CFIs, where extreme cold reliability is mandatory. Under its Leading Beyond Chemistry strategy, Evonik is advancing bio-based monomers to develop fully renewable cold flow improvers for sustainable aviation fuel markets.

United States: Renewable Diesel Acceleration Reshaping Winter Fuel Additive Demand

The United States cold flow improvers industry is undergoing rapid structural change as renewable diesel and biodiesel penetration reshapes winter operability requirements across regions. In August 2025, BASF commissioned a multi-million-dollar expansion at its Texas facility, dedicating new capacity to advanced cold flow improvers and wax anti-settling additives. This expansion directly supports the accelerating rollout of renewable diesel across California, Texas, and the Midwest, where paraffinic fuel profiles demand more precise wax crystallization control. Industry data from late 2025 confirms that more than 9.5 billion liters of biodiesel were treated with high-performance CFIs in the U.S., particularly for B20 blends operating in cold Midwestern climates where cloud point and filterability compliance is critical.

Technology convergence is further differentiating the U.S. market. Afton Chemical launched its Greenclean 3 platform in 2025, combining cold flow improvement with high-efficiency detergency to address both low-temperature operability and injector cleanliness for heavy-duty fleets. Feedstock evolution is also influencing formulation design. Increased utilization of used cooking oil under the U.S. Environmental Protection Agency 2025 food waste reduction strategy has driven demand for UCO-specific crystallizers capable of managing higher saturated fat content. In September 2025, Chevron Phillips Chemical introduced a next-generation CFI engineered for extreme winter conditions, demonstrating CFPP reductions exceeding 10°C in high-paraffin crude blends. Complementing product innovation, the U.S. Department of Energy announced a $120 million grant pool in late 2025 to modernize refinery blending infrastructure, prioritizing high-precision additive injection systems for winter diesel and renewable fuels.

Germany: Regulatory Stringency and AI-Optimized Treat Rate Efficiency

Germany’s cold flow improvers market is being shaped by strict seasonal diesel standards, sustainability mandates, and advanced formulation intelligence. Enforcement of DIN EN 590 winter specifications in 2025 requires all diesel sold between November and February to achieve a CFPP of at least −20°C. This regulation has driven a double-digit increase in additive treat rates as refiners optimize fuels for colder operating windows. At the same time, compliance pressure from updated EU REACH Annex XVII restrictions has accelerated the phase-out of legacy polymer blends containing trace persistent substances, pushing German manufacturers toward fully biodegradable polyalkyl methacrylate chemistries.

Digital formulation capabilities are emerging as a competitive differentiator. In July 2025, Evonik Industries introduced an AI-assisted platform that enables refiners to predict additive performance across more than 200 diesel and biodiesel blend ratios, significantly reducing formulation uncertainty. Efficiency gains are also being realized through chemistry innovation. Clariant showcased its DODIFLOW 5603 terpolymer technology in early 2025, achieving target cold flow performance at materially lower treat rates than conventional EVA-based solutions. Sustainability requirements under the EU Renewable Energy Directive III are further reshaping demand. German refiners are increasingly deploying specialized CFIs tailored for hydrotreated vegetable oil, which exhibits distinct wax behavior due to its high isoparaffin content.

India: Biodiesel Localization and Aviation-Linked Additive Expansion

India’s cold flow improvers industry is transitioning from import reliance to localized innovation, driven by biodiesel policy support, refining investments, and aviation infrastructure growth. In December 2024, Sanyo Chemical introduced Neoprover HBF-101 in India, a cold flow improver specifically designed for indigenous biodiesel feedstocks such as palm and jatropha. This product reflects a broader shift toward tailoring additive chemistry to region-specific fatty acid profiles, which differ markedly from soybean-based biodiesel used in Western markets.

Demand diversification is also evident in aviation fuels. With India’s aviation sector receiving large-scale investment through 2026, requirements for fuel system icing inhibitors and aviation-grade CFIs capable of performing under sub-zero, high-altitude conditions have reached new highs. Refining capacity expansion is reinforcing domestic additive availability. HPCL‑Mittal Energy Limited announced a major downstream fine chemicals project in 2025 that includes dedicated units for polyalphaolefin-based fuel additives. Quality assurance frameworks are improving in parallel. The 2025 expansion of the SATHI Portal introduced traceability for fuel additives, aligning domestic CFI production with international ASTM D975 standards and strengthening India’s export readiness.

China: Bio-Blending Mandates and Marine Fuel Transitions Driving Additive Complexity

China’s cold flow improvers market is expanding in scope and sophistication as refinery modernization, mandatory bio-blending, and marine fuel transitions converge. In November 2025, BASF inaugurated a high-performance dispersant line in Nanjing utilizing Controlled Free Radical Polymerization, enabling the production of additives that enhance low-temperature fluidity in heavy-duty transport fuels. This investment aligns with China’s broader push to upgrade refinery additive technology for cleaner and more resilient fuel systems.

Policy mandates are intensifying demand. New requirements introduced in mid-2025 across several coastal provinces mandate B5 to B10 biodiesel blending, prompting state-owned enterprises to scale procurement of ethylene vinyl acetate copolymers and advanced CFIs. The marine fuel segment is also undergoing rapid change. In response to global sulfur caps, bunkering hubs in Shanghai and Ningbo have transitioned toward very low sulfur fuel oil, which exhibits higher wax crystallization risks during storage. Advanced paraffin inhibitors are therefore becoming essential for operational stability. Supporting long-term innovation, the Ministry of Industry and Information Technology allocated significant funding in 2025 to develop zero-residue CFIs that prevent injector fouling in next-generation high-pressure common rail engines.

Comparative Summary: Country-Level Strategic Direction in the Cold Flow Improvers Industry

Cold Flow Improvers (CFI) Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Key Fuel Segment

|

Direction of CFI Innovation

|

|

United States

|

Renewable diesel expansion and winter operability

|

Biodiesel and renewable diesel

|

UCO-specific, extreme-cold CFIs

|

|

Germany

|

DIN EN 590 and RED III compliance

|

Winter diesel and HVO

|

Biodegradable, low-treat-rate polymers

|

|

India

|

Biodiesel localization and aviation growth

|

Indigenous biodiesel and jet fuel

|

Feedstock-specific and aviation-grade CFIs

|

|

China

|

Bio-blending mandates and marine fuel shift

|

B5–B10 diesel and VLSFO

|

CFRP-based, zero-residue additives

|

Cold Flow Improvers (CFI) Market Report Scope

Cold Flow Improvers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1675.6 Million

|

|

Market Size (2034)

|

$2759.6 Million

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Product Type (Ethylene Vinyl Acetate Copolymers, Polyalkyl Methacrylates, Polyalpha Olefins, Styrene Maleic Anhydride Copolymers, Vinyl Acetate Copolymers), By Application (Diesel Fuel, Biofuels, Aviation Fuel, Marine Fuel, Lubricating Oils), By Functionality (Cloud Point Depressants, Pour Point Depressants, Cold Filter Plugging Point Improvers, Wax Anti-Settling Additives), By End-User Industry (Oil Refineries and Terminals, Automotive and Transportation, Aerospace and Defense, Industrial and Power Generation)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Innospec Inc., Evonik Industries AG, Clariant AG, Afton Chemical Corporation, Infineum International Limited, Chevron Oronite Company LLC, The Lubrizol Corporation, Baker Hughes Company, Dorf Ketal Chemicals, Sanyo Chemical Industries Co., Ltd., Ecolab Inc., Ingevity Corporation, Mitsubishi Chemical Group Corporation, Bell Performance Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Cold Flow Improvers Market Segmentation

By Product Type

- Ethylene Vinyl Acetate Copolymers

- Polyalkyl Methacrylates

- Polyalpha Olefins

- Styrene Maleic Anhydride Copolymers

- Vinyl Acetate Copolymers

By Application

- Diesel Fuel

- Biofuels

- Aviation Fuel

- Marine Fuel

- Lubricating Oils

By Functionality

- Cloud Point Depressants

- Pour Point Depressants

- Cold Filter Plugging Point Improvers

- Wax Anti-Settling Additives

By End-User Industry

- Oil Refineries and Terminals

- Automotive and Transportation

- Aerospace and Defense

- Industrial and Power Generation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Cold Flow Improvers Industry

- BASF SE

- Innospec Inc.

- Evonik Industries AG

- Clariant AG

- Afton Chemical Corporation

- Infineum International Limited

- Chevron Oronite Company LLC

- The Lubrizol Corporation

- Baker Hughes Company

- Dorf Ketal Chemicals

- Sanyo Chemical Industries Co., Ltd.

- Ecolab Inc.

- Ingevity Corporation

- Mitsubishi Chemical Group Corporation

- Bell Performance Inc.

*- List not Exhaustive