Paraffin Inhibitors Market Valued at $760.8 Million in 2025 with 6.1% CAGR Driven by Deepwater Flow Assurance and Digital Optimization

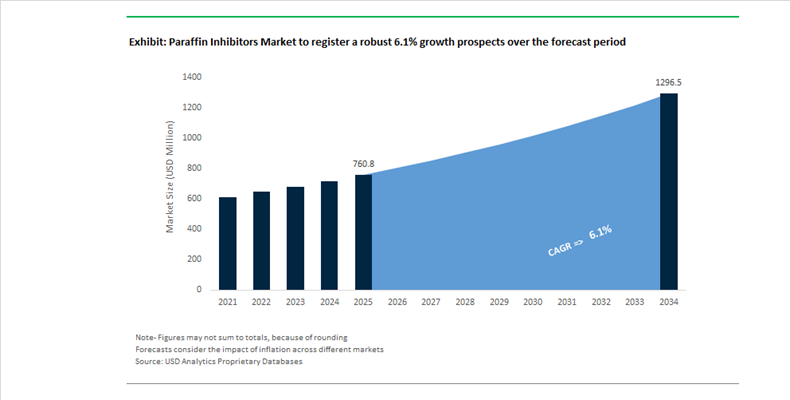

The Paraffin Inhibitors Market is valued at $760.8 Million in 2025 and is projected to reach $1,296.3 Million by 2034, expanding at a CAGR of 6.1%. Paraffin inhibitors, also referred to as wax inhibitors or crystal modifiers, are essential flow assurance chemicals used to prevent wax deposition in crude oil production, transportation pipelines, and subsea infrastructure. As global upstream operators increasingly exploit high-wax crude reserves in deepwater, Arctic, and mature fields, the technical complexity of wax control has intensified. Production from ultra-deepwater assets and tight oil formations has elevated the need for low-temperature performance, solvent reduction, and compatibility with digital injection systems. The market’s growth trajectory is therefore tied directly to offshore investments, shale recovery optimization, and decarbonization-linked efficiency mandates within oilfield operations.

A pivotal supply-side development occurred in May 2024 when BASF announced a multi-million euro expansion of its Basoflux® paraffin inhibitor production capacity at Tarragona, Spain. The facility upgrade prioritized aqueous dispersions and solvent-efficient formulations designed for colder operating conditions. Deliveries from the expanded site commenced in early 2025, introducing grades engineered to reduce solvent load and improve wax crystal dispersion at lower pour points. These innovations directly align with upstream operators’ efforts to cut chemical consumption and minimize environmental impact in offshore basins.

On the service-provider front, SLB expanded its biodegradable paraffin container systems through 2024 and 2025, integrating environmentally safer barrier materials into its digital oilfield platform. This initiative reflects a broader shift toward sustainability in offshore regions with heightened ecological sensitivity. Meanwhile, ChampionX strengthened its position in deepwater flow assurance through advanced paraffin crystal modifiers tested in ultra-deep subsea networks. These technologies address wax precipitation challenges in long tiebacks where temperatures fall below wax appearance thresholds.

Operational digitization is accelerating adoption of predictive wax management systems. By early 2026, companies including Baker Hughes and Halliburton reported that more than half of new Permian Basin service contracts incorporated AI-driven dosage optimization. These systems use real-time pipeline temperature, pressure, and flow data to dynamically adjust inhibitor injection rates, reducing both over-treatment and blockage risk.

Feedstock volatility also influenced the market in 2024 when Evonik declared force majeure on its VESTANAT® IPDI products, temporarily tightening availability of specialty isocyanate-based additive precursors. In parallel, bio-based alternatives are emerging. February 2026 industry reports highlighted palm-derived Methyl Ester Sulfonate (MES) as a viable sustainable surfactant for paraffin dispersion, reflecting the sector’s gradual pivot toward renewable oilfield chemistry. The paraffin inhibitors market is therefore evolving at the intersection of offshore expansion, digital flow assurance, solvent optimization, and ESG-driven reformulation.

Strategic Trends and High-Impact Opportunities Transforming the Paraffin Inhibitors Market

Mandated Paraffin Inhibitor Deployment in Shale and Deepwater Oil Production

The paraffin inhibitors market is increasingly shaped by the economics of high-cost oil production, where flow assurance failures translate directly into asset write-downs. In unconventional shale and deepwater environments, paraffin inhibition is no longer treated as a remedial chemical response but as a core element of well design and early-life production strategy. Operators are moving decisively toward first-oil and continuous injection models to prevent irreversible wax deposition that can permanently restrict wellbore and pipeline capacity.

Deepwater developments illustrate the scale of risk. Independent flow assurance studies published in 2025 indicate that paraffin-induced pipeline blockages in subsea systems can trigger decommissioning costs exceeding USD 100 million per incident. As a result, operators in the Gulf of Mexico and Brazil’s pre-salt basins are standardizing subsea umbilical injection systems capable of delivering inhibitors that remain stable at seabed temperatures near 4°C and operating pressures above 10,000 psi. These specifications have narrowed the supplier landscape toward high-performance chemistries with proven subsea reliability.

In shale plays, lifecycle economics are driving similar behavior. In the Permian Basin, major operators such as Chevron and ExxonMobil have adopted automated chemical injection at the wellhead during initial production. This approach has materially reduced the frequency of costly workovers and extended the productive life of unconventional wells, where rapid pressure decline accelerates wax precipitation. Supply-side investments reflect this demand shift. In May 2024, BASF expanded production of its Basoflux paraffin inhibitor portfolio in Tarragona, Spain, targeting complex crude systems where legacy formulations struggle to maintain flow consistency.

Reformulation Toward Environmentally Acceptable and Non-Polymer Inhibitors

Environmental regulation has become a defining constraint for paraffin inhibitor selection, particularly in offshore regions governed by stringent discharge rules. Compliance is now a prerequisite for market access rather than a differentiation factor, forcing a broad reformulation away from persistent polymers and hazardous surfactants toward biodegradable and low-toxicity alternatives.

Under the OSPAR Strategy 2030 for the North-East Atlantic, chemical components that fail biodegradability and substitution criteria are flagged for phase-out. This has accelerated the removal of alkylphenol ethoxylates and other persistent additives, replacing them with formulations that meet OECD 306 biodegradability thresholds of more than 60% within 28 days. The shift is not incremental but structural, with chemical suppliers redesigning core inhibitor platforms rather than modifying legacy blends.

Innovation momentum supports this transition. In 2023, SLB announced the development of a next-generation biodegradable paraffin inhibitor engineered for use in environmentally sensitive offshore zones. These formulations rely on vegetable-derived fatty acids and amino acid-based chemistries to disrupt wax crystal growth while avoiding bioaccumulation risks associated with traditional ethylene-vinyl acetate copolymers. Regulatory pressure is also globalizing. Amendments to Singapore’s Environmental Protection and Management Act implemented in January 2025 effectively ban medium-chain chlorinated paraffins by August 2025, aligning with the Stockholm Convention and signaling a broader international sunset for chlorinated components in inhibitor formulations.

Digital Twin and Predictive Flow Assurance Services

One of the most attractive growth opportunities in the paraffin inhibitors market lies in the transition from product sales to outcome-based service models. The Chemicals-as-a-Service approach is gaining traction as operators seek predictable uptime rather than reactive chemical consumption. By integrating inhibitors with digital twins and real-time analytics, suppliers are embedding themselves deeper into production operations.

Industry analysis in early 2025 highlighted that digital twins capable of simulating fluid behavior can dynamically predict wax appearance temperature as reservoir conditions evolve. This enables real-time adjustment of inhibitor dosage, reducing chemical overuse by an estimated 15% to 25% while maintaining flow assurance. Cloud-based platforms are accelerating adoption. In August 2024, ChampionX expanded its XSPOC optimization software, linking downhole sensors directly to surface injection systems. This creates autonomous dosing loops that respond instantly to changes in water cut or temperature.

The operational impact is material. Data published in 2025 shows that predictive modeling can reduce unplanned downtime in subsea tiebacks by up to 40%, delivering a compelling return on investment for operators facing the high cost and logistical complexity of subsea interventions. As digital integration deepens, paraffin inhibitors are increasingly sold as part of integrated flow assurance solutions rather than standalone chemicals.

High-Performance Inhibitors for Arctic and Long-Distance Subsea Tiebacks

As oil and gas development pushes into colder and more remote regions, demand is rising for paraffin inhibitors that perform under extreme thermal and logistical constraints. Arctic projects and long-distance subsea tiebacks present environments where conventional thermal management is insufficient, and chemical performance becomes the primary safeguard against wax deposition.

In Arctic exploration, operators in Russia and Norway are actively seeking inhibitors that remain pumpable at temperatures as low as minus 40°C. Responding to this need, Sanyo Chemical Industries launched a cold-flow improver in late 2024 specifically designed for ultra-low-temperature applications. These formulations ensure reliable injection during transport and storage, a critical requirement in remote Arctic logistics chains.

Subsea tiebacks exceeding 50 kilometers present a parallel challenge. As fluids cool during transit to host platforms, wax precipitation becomes a persistent threat. Industry reviews published in 2025 describe wax deposition in these systems as a billion-dollar economic liability over project lifecycles. This is driving strong demand for crystal modifiers and dispersants that keep paraffin particles suspended over long distances. Regulatory considerations add another layer. Updates to MARPOL Annex II in 2025 have tightened rules around noxious liquid substances, creating a niche for inhibitors that simplify tanker cleaning and discharge compliance in polar and cold-water shipping routes. Together, these dynamics position extreme-environment formulations as a premium, high-margin segment within the paraffin inhibitors market.

Paraffin Inhibitors Market Share and Segmentation Insights

Crystal Modifier Chemistries Lead Paraffin Inhibitor Demand in Oilfield Flow Assurance Programs

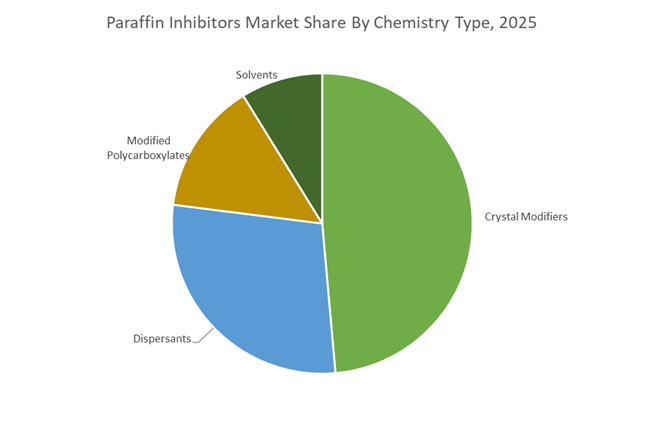

Crystal modifiers accounted for 48.60% of the Paraffin Inhibitors Market by chemistry type in 2025, reflecting their effectiveness in controlling wax deposition in crude oil production and transportation systems. Polymer chemistries such as ethylene vinyl acetate copolymers, maleic ester polymers, and polymeric acrylates modify wax crystal growth, preventing agglomeration and reducing the pour point of waxy crude oils. These inhibitors are widely used in upstream production systems and pipeline networks where paraffin deposition can restrict flow and increase maintenance costs. In 2025, tailored polymer design for field specific crude compositions is shaping product development, with manufacturers engineering crystal modifier polymers optimized for particular wax carbon chain distributions and operating temperatures to improve inhibition efficiency at lower treatment dosages.

Onshore Oil Production Drives Paraffin Inhibitor Consumption in Global Flowline Networks

Onshore operations represented 62.80% of the Paraffin Inhibitors Market by area of application in 2025, reflecting the large number of wells, flowlines, and gathering pipelines used in land based oil production systems. Paraffin deposition is a persistent operational challenge in onshore oilfields across diverse climates where temperature fluctuations cause wax precipitation in production tubing and pipelines. Continuous chemical treatment programs using paraffin inhibitors help maintain flow assurance and prevent equipment fouling in these production networks. In 2025, the expansion of unconventional oil production from shale and tight formations is increasing the complexity of wax management programs, with operators adopting formation specific paraffin inhibition strategies based on detailed crude oil composition and wax crystallization characteristics.

Paraffin Inhibitors Market Competitive Landscape

The Paraffin Inhibitors Market is evolving toward AI-driven flow assurance, multifunctional chemical formulations, and sustainable aqueous dispersions. Leading players are integrating digital monitoring, customized inhibitor systems, and low-toxicity chemistries to address wax deposition challenges in deepwater, unconventional, and high-paraffinic crude production environments.

Baker Hughes integrates digital flow assurance with multifunctional inhibitor deployment

Baker Hughes is strengthening its leadership in paraffin inhibitors through integrated digital flow assurance and long-term refinery partnerships. The multiyear agreement with Marathon Petroleum enables deployment of advanced chemical solutions such as XERIC™ demulsifiers and TOPGUARD™ inhibitors across multiple refining assets. With a record $35.9 billion RPO and strong IET segment orders, the company demonstrates robust demand for integrated chemical and digital solutions. Its BIOQUEST™ renewable additives support environmental compliance while maintaining high-performance paraffin inhibition. Baker Hughes’ digital monitoring platforms provide real-time insights into chemical efficacy, reducing non-productive time and optimizing dosing. This combination of digitalization, sustainability, and large-scale contracts strengthens its competitive positioning.

BASF expands aqueous paraffin inhibitor capacity with sustainable dispersion technology

BASF SE is advancing its position in the paraffin inhibitors market through sustainable aqueous-based dispersions and large-scale production expansion. The expansion of Basoflux® capacity at its Tarragona site enhances supply for high-paraffinic crude production across EMEA and North America. These formulations reduce solvent usage and improve efficiency at lower operating temperatures, aligning with sustainability goals. BASF’s integration of the Zhanjiang Verbund site supports localized supply of high-purity intermediates for Asia-Pacific markets. With a projected EBITDA of €6.2–€7.0 billion and €2.3 billion cost optimization target, the company is reinforcing operational efficiency. This integration of scale, sustainability, and regional production strengthens BASF’s market leadership.

SLB delivers customized deepwater paraffin management with data-driven chemical solutions

SLB is redefining paraffin inhibition through a data-driven, customized approach tailored for deepwater and unconventional reservoirs. Its advanced polymer-based inhibitors are designed to modify wax crystallization at the nucleation stage, preventing deposition in subsea environments. The company combines laboratory simulation with field data to select optimal dispersants and pour-point depressants based on crude characteristics such as API gravity and wax appearance temperature. Integration of flow assurance software enables precise chemical injection and deposit remediation using environmentally aligned solvents. SLB’s focus on biodegradable and low-toxicity formulations supports compliance with offshore discharge regulations. This combination of customization, digital integration, and sustainability positions SLB as a technology leader.

ChampionX scales mobile and solar-powered paraffin inhibition systems for upstream optimization

ChampionX is enhancing its competitive position through innovative delivery systems and data-driven paraffin inhibition technologies. Its ParaClear™ system provides kinematic-based diagnostics to develop customized solutions, achieving up to 39% production improvement in field applications. Expansion of this technology across multiple U.S. basins and into midstream pipelines demonstrates scalability. The integration of solar-powered chemical injection systems reduces reliance on hot oil treatments and minimizes operational downtime. Its ESP Digital Ecosystem further enables real-time monitoring of paraffin-related performance issues. This combination of mobility, digitalization, and efficiency strengthens ChampionX’s role in upstream flow assurance.

Clariant optimizes low-dosage paraffin control with multifunctional oilfield chemical systems

Clariant is focusing on high-efficiency paraffin inhibitors designed to reduce operating costs through lower dosage and multifunctional performance. Its Paraffin Control Technologies are engineered for extreme subsea and high-temperature environments, maintaining effectiveness under high shear conditions. The company’s Phasetreat™ Nan portfolio integrates wax inhibition with enhanced oil-water separation, delivering dual functionality for complex production systems. Successful implementation of squeeze treatments in high-temperature fields demonstrates its capability in challenging conditions. Clariant’s rapid customization and deployment capabilities provide a competitive advantage in dynamic production environments. This focus on efficiency, multifunctionality, and adaptability strengthens its market positioning.

United States – Digital Flow Assurance and Shale-Centric Chemical Optimization

The United States paraffin inhibitors market is being reshaped by the convergence of shale productivity optimization, digital oilfield tools, and tightening environmental compliance. In March 2025, ChampionX, following its integration into SLB, deployed the ParaClear system across rod-lift wells in the Denver–Julesburg Basin. The deployment combined continuous chemical injection with solar-powered paraffin trailers, delivering a documented 39% uplift in production. This outcome has accelerated adoption of automated paraffin inhibition programs across mature shale assets, where marginal gains translate directly into improved well economics.

Offshore, the Gulf of Mexico is driving a parallel shift in chemistry requirements. By late 2025, operators increasingly favored subsea injection of high-purity modified polycarboxylates to mitigate wax deposition in ultra-deepwater tie-backs, where mechanical remediation is economically unviable. R&D capability is expanding in tandem. In July 2025, Nouryon inaugurated its Oilfield Innovation Center in Houston, equipped for advanced wax rheology and asphaltene–paraffin interaction testing. Regulatory pressure is reinforcing formulation change. New 2025 U.S. Environmental Protection Agency guidelines are accelerating the phase-out of aromatic solvents, driving demand toward aqueous-based paraffin dispersions and solvent-minimized chemistries.

Spain – European Export Platform for Sustainable Paraffin Control

Spain has emerged as a strategic European production and export hub for next-generation paraffin inhibitors. In May 2024, BASF announced a major expansion of its Basoflux® production at the Tarragona site, adding dedicated assets for both sustainable aqueous-based and optimized solvent-based paraffin inhibitors. The facility commenced first customer deliveries in January 2025, positioning Spain as a central supply node for European, African, and Middle Eastern offshore and onshore markets.

The strategic importance of Tarragona lies not only in capacity, but in formulation direction. Basoflux dispersions produced in Spain are engineered to function effectively at lower temperatures with reduced solvent loadings, directly aligning with forthcoming EU 2026 resource-efficiency and emissions mandates. This capability is particularly relevant for mature North Sea and Mediterranean assets, where operators face rising compliance costs alongside declining production profiles.

China – Offshore Expansion and Feedstock Localization

China’s paraffin inhibitors market is being driven by offshore expansion and deliberate localization of key polymer feedstocks. In late 2025, China National Offshore Oil Corporation intensified Deep Sea One Phase II development in the South China Sea. These projects mandate paraffin inhibitors with high thermal stability and long residence times, suitable for subsea pipelines operating under high-pressure, high-temperature conditions.

On the supply side, domestic chemical producers in Zhejiang increased synthesis of Ethylene Vinyl Acetate copolymers in 2025. EVA remains a core feedstock for paraffin crystal modifiers, and localization reduces exposure to imported specialty intermediates. Regulatory tightening is reinforcing this shift. Regional authorities enforced stricter Quality Control Orders for EVA copolymers in 2025, ensuring that both imported and domestic materials meet high-purity industrial specifications. This has raised baseline quality expectations for paraffin inhibitor formulations supplied to offshore and onshore operators.

India – Portfolio Expansion and Green Chemistry Incentives

India’s paraffin inhibitors market is transitioning from formulation dependence to integrated specialty chemistry capability. In May 2024, Dorf Ketal Chemicals acquired Impact Fluid Solutions, materially expanding its portfolio across paraffin inhibition, wellbore stability, and flow assurance. This acquisition strengthened India’s position as a technology supplier rather than a contract blender for oilfield chemicals.

Policy support is reinforcing domestic innovation. Under the 2025 NITI Aayog Chemical Clusters initiative, subsidies have been directed toward R&D centers focused on biodegradable and low-toxicity paraffin dispersants, particularly for mature fields operated by ONGC and Oil India Limited. Regulatory alignment is tightening raw material quality. Amendments issued in October 2025 to the Ethylene Vinyl Acetate Copolymers Quality Control Order are standardizing EVA inputs used in pour point depressants, improving consistency across domestically formulated paraffin inhibitors.

United Arab Emirates – Regional Technical Hub and EOR Integration

The UAE is positioning itself as a regional innovation and application hub for paraffin inhibition under extreme reservoir conditions. In late 2025, Nouryon designated its Dubai innovation center as the primary technical support base for the Middle East and Southeast Asia. The facility focuses on localized troubleshooting for high-paraffin crudes, which are common across Gulf reservoirs.

Operational integration is advancing at the national oil company level. Abu Dhabi National Oil Company reported in 2025 that embedding paraffin inhibitors directly into CO₂-based Enhanced Oil Recovery injection streams reduced wellbore plugging incidents by 22%. This integration underscores a broader trend in the UAE toward multifunctional chemical programs that address flow assurance, recovery efficiency, and operational reliability simultaneously.

Comparative Snapshot – Paraffin Inhibitors Industry by Country

Paraffin Inhibitors Market County Level Snapshot

|

Country

|

Primary Driver

|

Technology Focus

|

Structural Implication

|

|

United States

|

Shale productivity and digital dosing

|

Aqueous dispersions, automated injection

|

High-value, data-driven chemical programs

|

|

Spain

|

European sustainability mandates

|

Low-solvent Basoflux® dispersions

|

Export-oriented, regulation-aligned supply

|

|

China

|

Offshore expansion and localization

|

High-thermal-stability EVA modifiers

|

Improved feedstock security and quality

|

|

India

|

Portfolio integration and policy incentives

|

Biodegradable PPDs, specialty formulations

|

Transition toward innovation-led supply

|

|

UAE

|

EOR-linked flow assurance

|

Integrated inhibitor injection streams

|

Regional hub for extreme crude profiles

|

Paraffin Inhibitors Market Report Scope

Paraffin Inhibitors Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$760.8 Million

|

|

Market Size (2034)

|

$1296.3 Million

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Chemistry Type (Crystal Modifiers, Dispersants, Solvents, Modified Polycarboxylates), By Functionality (Paraffin Inhibitors, Paraffin Dispersants, Pour Point Depressants), By Operation Segment (Upstream, Midstream, Downstream), By Area of Application (Onshore, Offshore and Subsea)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SLB, Baker Hughes, Halliburton, BASF, Nouryon, Clariant, Evonik Industries, Innospec, Dorf Ketal Chemicals, Croda International, Dow, Ecolab, Kemira, Solenis, ZFA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Paraffin Inhibitors Market Segmentation

By Chemistry Type

- Crystal Modifiers

- Dispersants

- Solvents

- Modified Polycarboxylates

By Functionality

- Paraffin Inhibitors

- Paraffin Dispersants

- Pour Point Depressants

By Operation Segment

- Upstream

- Midstream

- Downstream

By Area of Application

- Onshore

- Offshore and Subsea

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Paraffin Inhibitors Industry

- SLB

- Baker Hughes

- Halliburton

- BASF

- Nouryon

- Clariant

- Evonik Industries

- Innospec

- Dorf Ketal Chemicals

- Croda International

- Dow

- Ecolab

- Kemira

- Solenis

- ZFA

*- List not Exhaustive