Solvents Market Valuation 2025–2034: $59.3 Billion to $111.8 Billion at 7.3% CAGR Fueled by High-Purity Pharma Grades, Circular Technologies, and Capacity Expansion

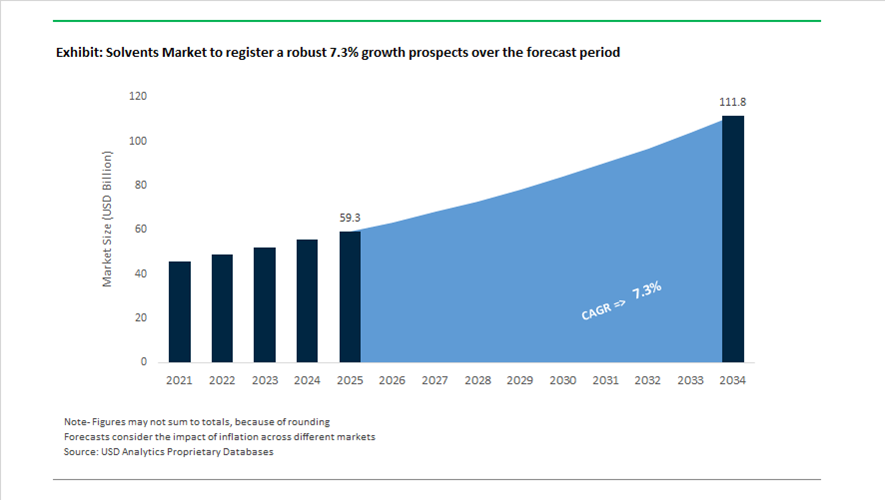

The global solvents market is valued at $59.3 billion in 2025 and is projected to reach $111.8 billion by 2034, expanding at a CAGR of 7.3%. Growth is driven by rising demand for hydrocarbon solvents, oxygenated solvents, glycol ethers, alcohols, ketones, esters, chlorinated solvents, and specialty high-purity grades across pharmaceuticals, agrochemicals, paints and coatings, electronics manufacturing, adhesives, and industrial cleaning. Increasing regulatory scrutiny on volatile organic compounds and carbon intensity is accelerating the shift toward bio-based solvents, ultra-high-purity formulations, and circular solvent recovery systems. Simultaneously, high-growth sectors such as electric vehicles, semiconductor fabrication, and advanced coatings are reshaping performance requirements for solvent purity, solvency power, and environmental compliance.

In January 2024, INEOS announced a 50% expansion of hydrocarbon solvent capacity at its Chocolate Bayou, Texas facility to meet surging pharmaceutical and agricultural demand. In March 2024, ExxonMobil Chemical and BASF entered a strategic collaboration to commercialize high-performance hydrocarbon solvents utilizing catalytic dehydrogenation technology to enhance sustainability in industrial cleaning applications. In May 2024, LyondellBasell divested its ethylene oxide and derivatives business to INEOS for approximately $700 million, strengthening INEOS’s integration in the ethylene value chain while allowing LyondellBasell to pivot toward polypropylene and circular solutions. In late 2024, LyondellBasell acquired APK AG’s solvent-based Newcycling® technology, enabling advanced separation of multilayer plastic waste into high-purity recycled polymers through solvent extraction processes.

Specialty solvent innovation expanded throughout 2024 and 2025. In mid-2024, Honeywell introduced Chromasolv™ Plus ultra-high-purity solvents designed for liquid chromatography-mass spectrometry applications in metabolomics and biomarker research, enhancing UV absorbance control and analytical precision. In October 2024, Clariant launched VitiPure™ LEX co-solvents optimized for low water-solubility active pharmaceutical ingredients. In November 2025, AkzoNobel and Axalta announced a merger of equals, creating a major coatings and solvent formulations entity focused on nanostructured solvent systems for aerospace and automotive OEM coatings. These developments illustrate a strong emphasis on pharmaceutical-grade purity, advanced coating chemistries, and solvent-enabled polymer recycling.

Capacity additions and decarbonization initiatives intensified in 2026. In February 2026, BASF announced plans to increase 1,4-Butanediol production at Ludwigshafen, reinforcing supply of a critical solvent and intermediate for plastics and electronic chemicals. The same month, LyondellBasell confirmed progress on a glacial acetic acid unit at its La Porte, Texas complex to serve paints, adhesives, and coatings markets. BASF also introduced AdBlue® GE produced entirely with renewable electricity, highlighting broader decarbonization of nitrogen-based chemical production processes that intersect with solvent manufacturing. These strategic expansions, sustainability collaborations, and solvent-based circular technologies are shaping competitive positioning in the global solvents market toward $111.8 billion by 2034.

Strategic Trends and High-Value Opportunities in the Global Solvents Market

Petrochemical Majors Scaling Ultra-High-Purity Solvent Lines for Advanced Semiconductor Nodes

The global solvents market is experiencing a structural upgrade as semiconductor manufacturing transitions toward sub-5nm logic, 3nm nodes, and advanced packaging architectures. At these technology nodes, tolerance for metallic and organic impurities has tightened to parts-per-trillion levels, fundamentally redefining solvent production economics. Electronic-grade isopropyl alcohol, acetone, and N-Methyl-2-pyrrolidone are no longer commoditized inputs but precision-engineered materials that directly influence wafer yield and device reliability.

During 2024 and 2025, advanced packaging emerged as a disproportionate driver of solvent demand. The shift toward 300mm wafer processing has increased per-unit consumption of ultra-high-purity solvents by roughly 30% compared to legacy 200mm platforms. This is linked to more complex cleaning, surface preparation, and hybrid bonding steps required in 2.5D and 3D integration. To secure long-term supply continuity, petrochemical majors are deploying closed-loop purification systems, multi-stage distillation, and real-time contamination monitoring tailored to semiconductor fabs. Within this context, BASF maintained a leading position in 2024 with an estimated 18% share of the electronic wet chemicals segment, supported by strategic co-development agreements with foundries. These partnerships focus on solvent systems optimized for photolithography, EUV cleaning, and hybrid bonding, reinforcing solvents as a critical enabler of advanced semiconductor scaling rather than a secondary consumable.

EPA NESHAP Regulations Accelerating Substitution of Hazardous Industrial Solvents

A second defining trend is the regulatory-driven substitution of hazardous air pollutant solvents across industrial manufacturing in the United States. Final rules issued by the U.S. Environmental Protection Agency during 2024 and 2025 under the Clean Air Act have intensified restrictions on legacy solvents such as methyl ethyl ketone and toluene. These updates to the National Emission Standards for Hazardous Air Pollutants are not incremental adjustments but enforceable thresholds that compel immediate reformulation.

The EPA estimates that the revised standards will reduce hazardous air pollutant emissions by approximately 158 tons per year. For aerospace and automotive coatings, this has triggered a rapid pivot toward compliant alternatives including dimethyl carbonate and selected acetate esters that deliver comparable solvency without triggering HAP classifications. Regulatory pressure is further amplified by new fenceline monitoring requirements finalized in April 2024. Chemical plants must now publicly report emissions data on a quarterly basis, increasing legal and reputational exposure. As a result, solvent reformulation is increasingly viewed as a risk management strategy, accelerating adoption of low-VOC, non-HAP solvent systems across North American industrial value chains.

Bio-Derived Drop-In Solvents Supporting Circularity in Consumer Goods

Consumer packaged goods manufacturers are emerging as a major opportunity segment for solvent suppliers capable of delivering bio-derived drop-in alternatives at scale. Driven by Scope 3 carbon reduction commitments and consumer preference for sustainable products, CPG companies are integrating solvents derived from agricultural and biomass feedstocks into inks, coatings, and adhesive formulations. Ethyl lactate and bio-ethanol have moved beyond niche positioning to become mainstream ingredients in packaging and printing applications.

In 2024, global sales of natural and organic consumer products reached approximately $209 billion, reflecting year-on-year growth of 4.8%. This demand signal is directly influencing solvent selection, as bio-based solvents offer up to 50% lower toxicity and as much as 12% reduction in manufacturing energy consumption compared with petroleum-derived counterparts. Supply-side capacity is aligning with this shift. Global bio-based methanol production is projected to reach 21.3 million tons by 2026, creating a strong integration opportunity for the adhesives and sealants sector. This segment is expected to be among the fastest adopters of green solvents, particularly in North America and Asia Pacific, where regulatory scrutiny of packaging sustainability is intensifying.

Custom Solvent Blends Enabling Solid-State Battery Manufacturing

The commercialization of lithium-metal and all-solid-state batteries is opening a high-value niche for advanced solvent formulations. Unlike conventional lithium-ion systems, solid-state battery processing requires extremely precise control over slurry rheology, evaporation rates, and dielectric behavior to enable defect-free electrolyte layers. This has driven demand for custom ternary and quaternary solvent blends designed specifically for solid-state processing workflows.

The market for battery electrolyte solvents is projected to reach $11.64 billion in 2025, with growth increasingly tied to next-generation battery architectures rather than conventional liquid electrolytes. Manufacturers are leveraging AI-driven molecular simulations to accelerate solvent design, ensuring compatibility with high-voltage cathode materials and supporting the industry’s push toward the 500 Wh per kilogram energy density threshold. Scale-up innovation is already visible. In 2025, Samsung Electro-Mechanics began sampling sub-50 micron all-solid-state battery cells using solvent-assisted doctor blade casting techniques. These processes rely on high-dielectric, low-viscosity solvent systems to achieve uniform ceramic electrolyte layers at industrial throughput, positioning advanced solvent blends as a foundational input for the next phase of battery manufacturing evolution.

Solvents Market Share and Segmentation Insights

Oxygenated Solvents Lead the Solvents Market Due to Strong Regulatory Compliance and Performance

Oxygenated solvents accounted for 42.8% of the solvents market in 2025, establishing them as the most widely used solvent category across industrial and specialty chemical applications. This group includes alcohols, ketones, esters, and glycol ethers, which offer strong solvency, controlled volatility, and relatively lower toxicity compared with hydrocarbon and halogenated alternatives. Oxygenated solvents are widely used in paints and coatings, pharmaceuticals, printing inks, and industrial cleaning formulations. A major 2025 market driver is the regulatory-driven shift toward lower VOC solvent systems, where manufacturers increasingly develop high-performance oxygenated solvents with reduced emission profiles and regulatory-exempt status in certain jurisdictions, enabling compliance with tightening global environmental regulations.

Paints & Coatings Segment Drives Global Solvent Consumption Across Coating Formulations

Paints and coatings represent the largest application segment in the solvents market, accounting for 38.60% of total demand in 2025 due to the critical role solvents play in coating formulation and application performance. Solvents are used to dissolve resins, control coating viscosity, and support uniform film formation during application and drying. They are essential in both solvent-borne coatings and as coalescing agents in waterborne systems. The scale of global coatings production across architectural, industrial, automotive, and protective coatings continues to support strong solvent consumption. A key 2025 industry transition is the growing adoption of high-solids and waterborne coating technologies, which reduce solvent content per unit of coating while still requiring specialty solvents for film formation and performance in high-performance coating systems.

Solvents Market Competitive Landscape

The global solvents market in 2026 is shaped by a transition toward oxygenated and bio-based solvents, AI-driven cost optimization, and regionalized production strategies. Industry leaders are prioritizing low-VOC formulations, PFAS-free alternatives, and integrated chemical production systems to address regulatory pressures and evolving demand across coatings, EV batteries, and electronics.

BASF Strengthens Verbund Integration and Cost Leadership Through Zhanjiang Expansion and €2.3 Billion Savings Program

BASF SE leads the global solvents market with strong financial performance, reporting €6.6 billion EBITDA in 2025 and projecting €6.2–€7.0 billion for 2026. The Zhanjiang Verbund site in China is a cornerstone of its regionalized production strategy, enabling efficient, localized solvent manufacturing for Asia-Pacific demand. BASF’s cost optimization program has achieved €1.7 billion in savings, with a 2026 target of €2.3 billion, enhancing margin resilience amid feedstock volatility. Its focus on Chemicals and Nutrition & Care segments supports growth in high-value oxygenated solvents. Integration of renewable energy into production aligns with global decarbonization goals and low-VOC solvent demand. BASF’s scale, efficiency, and sustainability focus reinforce its leadership in integrated solvent production.

Dow Accelerates AI-Driven Productivity and Oxygenated Solvent Pricing Strategy Under Transform to Outperform Initiative

Dow Inc. is advancing its solvents portfolio through the “Transform to Outperform” initiative, targeting $2 billion in EBITDA improvement via automation and AI-driven productivity. With approximately $40 billion in 2025 sales, the company maintains strong financial resilience and shareholder returns. Strategic closure of high-cost European assets reallocates capital toward more competitive regions, enhancing global supply chain efficiency. Dow’s pricing adjustments across oxygenated solvents, including propanol and n-butyl acetate, reflect efforts to manage raw material volatility and sustain R&D investment. Its focus on lean operations and digital transformation strengthens its competitive positioning. The company’s emphasis on high-performance coatings and sustainable solvent systems aligns with regulatory and market trends.

ExxonMobil Expands Specialty Hydrocarbon Solvent Portfolio with Integrated Refining and Advantaged Project Growth

ExxonMobil Product Solutions maintains leadership in hydrocarbon solvents through its integrated refining network and strong financial performance, reporting $28.8 billion in 2025 earnings. Its specialty solvent portfolio, including Exxsol™, Isopar™, and Varsol™ fluids, addresses demand for high-purity industrial cleaning and ink applications. Strategic investments such as the Singapore Resid Upgrade enhance feedstock efficiency by converting lower-value inputs into high-value chemical outputs. The company achieved $3.0 billion in cost savings in 2025, reinforcing its competitive cost structure. Price adjustments across solvent lines reflect strong demand and evolving market dynamics. ExxonMobil’s focus on methane intensity reduction aligns its hydrocarbon solvent production with ESG compliance requirements.

LyondellBasell Expands Propylene and Acetic Acid Capacity to Strengthen Oxygenated Solvent Supply Chain

LyondellBasell is strengthening its position in oxygenated solvents through strategic capacity expansions in the U.S. Gulf Coast. Its Channelview project will produce 882 million pounds per year of propylene, supporting downstream solvent intermediates such as propylene oxide. Increased production of glacial acetic acid at its La Porte facility enhances supply for coatings, adhesives, and industrial solvent applications. The company is implementing capacity rationalization across the U.S. and Europe to stabilize margins and optimize asset utilization. Access to low-cost natural gas liquids provides a structural cost advantage over naphtha-based competitors. LyondellBasell’s feedstock integration and production expansion support its competitiveness in high-demand solvent segments.

Solvay Advances Bio-Based Oxygenated Solvents and Decarbonization Through Coatis Platform and Portfolio Optimization

Solvay S.A. is reinforcing its leadership in sustainable solvents through its Coatis oxygenated solvents platform, supported by €4.3 billion in 2025 net sales and a 20.7% EBITDA margin. The company’s portfolio optimization strategy includes site rationalization to focus on high-growth solvent markets. Its 29% reduction in Scope 1 and 2 emissions enhances the environmental profile of its bio-based solvent offerings. Solvay’s Coatis line provides low-carbon alternatives increasingly adopted in coatings, pharmaceuticals, and specialty applications. Strategic investments are directed toward high-purity and sustainable solvent solutions aligned with regulatory requirements. Its focus on decarbonization and specialty chemistry strengthens its position in the evolving solvents market.

United States Solvents Market Shaped by Semiconductor Localization and Toxicity Phase-Out

The United States solvents industry is undergoing a decisive shift driven by semiconductor supply chain localization, federal chemical risk management, and large-scale petrochemical investments. In August 2024, Eastman launched a domestic production line for electronic-grade EastaPure™ Isopropyl Alcohol, directly supporting U.S.-based semiconductor fabrication plants seeking resilient, contamination-controlled solvent supply. This move aligns with broader efforts to onshore electronic chemicals critical for advanced node manufacturing. At the feedstock level, LyondellBasell operationalized the world’s largest Propylene Oxide and Tertiary Butyl Alcohol complex in Texas in early 2024, adding 470,000 metric tons per year of propylene oxide capacity and strengthening availability of glycol ether solvents used across coatings, electronics, and industrial cleaning.

Regulatory developments are equally transformative. In December 2024, the Environmental Protection Agency finalized new TSCA risk management rules for perchloroethylene and trichloroethylene, effectively phasing out their use in most solvent applications by 2026. This has accelerated substitution toward lower-toxicity oxygenated and bio-derived solvents. Trade policy has also entered the equation. In February 2025, the MDI Fair Trade Coalition, led by BASF and Dow, filed anti-dumping petitions alleging extreme pricing distortions on Chinese imports, impacting isocyanate-linked solvent systems. Complementing these shifts, the U.S. Department of Energy announced USD 38 million in January 2025 for bio-innovation projects aimed at reducing synthetic nitrogen in feedstock production, indirectly strengthening the sustainability profile of bio-ethanol solvents. Specialty applications are also advancing, with Clariant introducing its Vitipure LEX series of highly purified PEG co-solvents for sensitive pharmaceutical formulations.

China Solvents Market Driven by High-Purity Localization and Green Manufacturing Mandates

China’s solvents industry is scaling rapidly under a dual mandate of self-sufficiency in electronic chemicals and stricter environmental compliance. In March 2024, BASF SE commissioned a new methyl glycols plant at its Zhanjiang Verbund site, adding 46,000 metric tons per year of capacity aimed at high-performance brake fluid and specialty solvent demand across Asia-Pacific. Parallel investments in Nanjing and Shanghai have enabled domestic production of 5N purity solvents, supporting China’s target of achieving 70% self-sufficiency in electronic chemicals by 2026, particularly for semiconductor-grade applications.

Policy frameworks are reinforcing this trajectory. Implementation of GB 4806.16-2025 has imposed strict limits on volatile residues in solvents used for food-contact materials, driving reformulation across packaging value chains. The Ministry of Industry and Information Technology has prioritized grants for photocatalytic sol-gel solvent systems used in self-cleaning architectural coatings under Smart City programs, reducing long-term chemical waste. Feedstock diversification is also underway, with advanced coal-to-methanol conversion technologies stabilizing solvent supply against petroleum price volatility and strengthening domestic resilience.

Germany and European Union Solvents Market Defined by REACH Tightening and Circular Recycling

Germany anchors the European solvents landscape through regulatory leadership, circular economy integration, and climate-neutral production. The European Commission’s Chemicals Industry Package announced for late 2025 introduces a targeted REACH revision, simplifying authorization for essential-use solvents while restricting hazardous variants. This regulatory clarity follows decisive action in June 2025, when Regulation (EU) 2025/1090 added DMAC and NEP to the REACH restricted list, mandating phase-out from most mixtures by December 2026 and accelerating substitution toward safer solvent chemistries.

Industrial innovation is reinforcing competitiveness. In October 2024, LyondellBasell acquired full ownership of APK AG in Merseburg, deploying solvent-based recycling technology to separate polymers from multi-layer packaging and produce high-purity recycled LDPE. In coatings, BASF launched Efka PX 4360, a solvent-based dispersing agent developed using Controlled Free Radical Polymerization to enhance color performance in sustainable formulations. At a system level, German chemical parks have integrated Renewable Energy Verbund models, cutting an estimated 6.1 million metric tons of CO2 emissions from solvent production in 2024 compared with fossil-only baselines.

India Solvents Market Expanding Through Bio-Foundries and Trade Defense

India’s solvents industry is expanding under a combination of biotechnology-led feedstock strategies and intensified trade protection. The BioE3 policy approved in late 2024 has created financial incentives for bio-foundries producing bio-ethanol and other fermented solvents from agricultural waste, supporting both rural value chains and domestic solvent availability. This policy framework is accelerating the transition from petroleum-derived solvents toward renewable alternatives across pharmaceuticals, agrochemicals, and coatings.

Trade defense mechanisms are reinforcing domestic producers. In 2025, the Directorate General of Trade Remedies initiated multiple anti-dumping investigations into acetone and isopropyl alcohol imports from Southeast Asia, aiming to curb price undercutting and protect local capacity. Strategic corporate moves complement policy support. In December 2025, BASF, through its Indian operations, announced plans to acquire Noble Seeds, signaling deeper integration of chemical solutions with solvent-intensive agricultural and crop protection segments.

Comparative Snapshot: Country-Level Solvents Industry Dynamics

Solvents Market County Level Snapshot

|

Country / Region

|

Core Strategic Drivers

|

Key Solvent Focus Areas

|

Regulatory and Structural Impact

|

|

United States

|

Semiconductor localization, toxicity controls

|

Electronic-grade IPA, glycol ethers, bio-ethanol

|

TSCA phase-outs, onshoring, ESG disclosure

|

|

China

|

Self-sufficiency, green manufacturing

|

High-purity solvents, methyl glycols

|

GB 4806.16-2025, MIIT grants

|

|

Germany / EU

|

REACH tightening, circular economy

|

Solvent recycling, CFRP dispersants

|

Hazard restrictions, climate-neutral parks

|

|

India

|

BioE3 policy, trade protection

|

Bio-ethanol, acetone, IPA

|

Subsidies, anti-dumping investigations

|

Solvents Market Report Scope

Solvents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$59.3 Billion

|

|

Market Size (2034)

|

$111.8 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Product Type (Oxygenated Solvents, Hydrocarbon Solvents, Halogenated Solvents, Green & Bio-Based Solvents, High-Purity Solvents), By Application (Paints & Coatings, Pharmaceuticals, Industrial Cleaning, Printing Inks, Agricultural Chemicals, Adhesives & Sealants, Cosmetics & Personal Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Exxon Mobil Corporation, Shell plc, LyondellBasell Industries N.V., Eastman Chemical Company, SABIC, INEOS Group, Huntsman Corporation, Celanese Corporation, Chevron Phillips Chemical Company LLC, Ashland Inc., Mitsubishi Chemical Group, Solvay S.A., Shin-Etsu Chemical Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Solvents Market Segmentation

By Product Type

Alcohols

Ketones

Esters

Glycols

Glycol Ethers

Aliphatic

Aromatic

- Halogenated Solvents

- Green & Bio-Based Solvents

- High-Purity Solvents

By Application

- Paints & Coatings

- Pharmaceuticals

- Industrial Cleaning

- Printing Inks

- Agricultural Chemicals

- Adhesives & Sealants

- Cosmetics & Personal Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Solvents Industry

- BASF SE

- Dow Inc.

- Exxon Mobil Corporation

- Shell plc

- LyondellBasell Industries N.V.

- Eastman Chemical Company

- SABIC

- INEOS Group

- Huntsman Corporation

- Celanese Corporation

- Chevron Phillips Chemical Company LLC

- Ashland Inc.

- Mitsubishi Chemical Group

- Solvay S.A.

- Shin-Etsu Chemical Co. Ltd.

*- List not Exhaustive