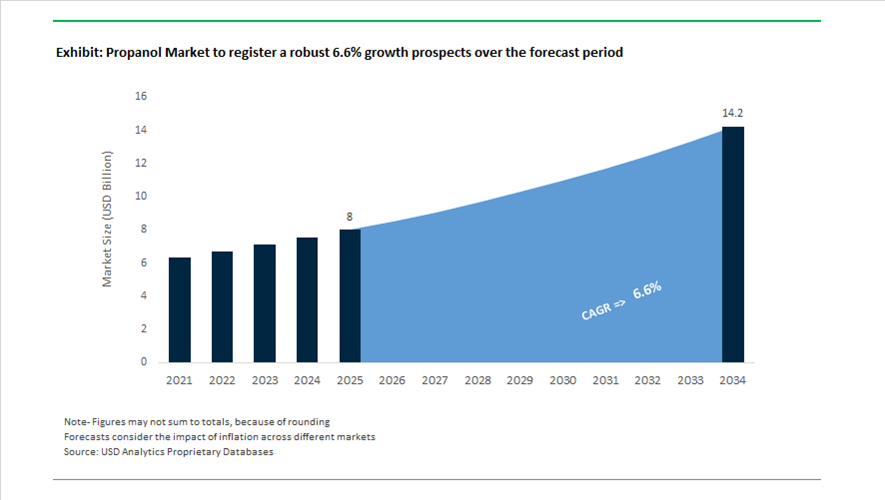

Propanol Market Valued at $8 Billion in 2025, Projected to Reach $14.2 Billion by 2034 at 6.6% CAGR

The global propanol market is valued at $8 billion in 2025 and is projected to reach $14.2 billion by 2034, expanding at a robust CAGR of 6.6%. Growth is supported by rising demand for n-propanol and isopropanol (IPA) in industrial coatings, pharmaceutical solvents, electronics cleaning fluids, agrochemical formulations, disinfectants, printing inks, and personal care products. Tightening purity standards for medical-grade and semiconductor-grade solvents, along with expanding propylene derivative capacity in the U.S. Gulf Coast and Asia-Pacific, are reshaping global supply dynamics. The market is also experiencing increasing volatility in feedstock pricing, particularly ethylene and propylene, influencing contract structures and price adjustments among leading oxo alcohol producers.

Structural portfolio shifts in 2025 altered competitive positioning. In July 2025, Shell completed the acquisition of Raj Petro Specialities, strengthening its distribution network for specialty solvents including high-purity isopropanol across India’s expanding manufacturing and pharmaceutical sectors. In October 2025, BASF divested its decorative paints business to Sherwin-Williams, sharpening its focus on core chemicals such as n-propanol used in industrial coatings and solvent systems. Throughout 2025, OQ Chemicals implemented multiple price adjustments for n-propanol and related oxo alcohols in response to feedstock volatility and elevated European energy costs. In Q3 2025, Dow started up new assets on the U.S. Gulf Coast, increasing availability of propylene-derived solvents for North American customers and improving regional supply resilience.

Purity-driven demand expansion has intensified across electronics and healthcare applications. During 2024 and 2025, manufacturers including LG Chem launched specialized high-purity isopropanol grades with sub-ppb metal impurity levels to support advanced semiconductor dry cleaning processes. In August 2025, Dow’s focus on pharmaceutical-grade PURAGUARD™ PG USP/EP glycols reflected a broader tightening of solvent specifications across medical disinfectants and injectable formulations, indirectly tightening high-purity alcohol markets. By late 2025, Asia-Pacific accounted for more than one-third of global propanol consumption, led by pharmaceutical, agrochemical, and electronics manufacturing expansion in China and India. In mid-2025, specialty producers began shipping biopropanol derived from agricultural waste streams, targeting premium cosmetics and fragrance applications aligned with 2030 sustainability goals.

Capacity rationalization and efficiency programs continued into 2026. In early 2026, PPG finalized the divestment of its silica business to Qemetica, indirectly affecting the coatings and solvent ecosystem where n-propanol remains a key intermediate. In February 2026, BASF announced a new dispersions production line at its Mangalore site in India, increasing downstream demand for n-propanol as a co-solvent in architectural coatings. In January 2026, ExxonMobil reported achieving $15.1 billion in structural cost savings, optimizing its U.S. Gulf Coast chemical plants to enhance competitiveness in propylene-derived isopropanol production against Asian imports.

The propanol market is increasingly defined by pharmaceutical-grade and semiconductor-grade isopropanol, propylene-based solvent expansion in the Gulf Coast, bio-based propanol integration, oxo alcohol price volatility, high-purity cleaning solvents for chip fabrication, and Asia-Pacific consumption dominance. Feedstock optimization, sustainability mandates, and purity-driven application growth continue to drive structural expansion across global propanol supply chains.

Strategic Trends and Monetizable Opportunities in the Propanol (IPA & NPA) Market

Non-Discretionary Demand for Ultra-High-Purity IPA in Semiconductor Manufacturing

Ultra-high-purity isopropanol has transitioned from a specialty solvent into a mission-critical process chemical for advanced semiconductor fabrication. Demand for electronic-grade IPA with purity levels of 99.99% and above is now structurally insulated from broader industrial cycles, as it is directly linked to wafer yield, defect control, and process reliability in sub-5nm logic and memory nodes. As of December 2025, IPA is indispensable for wafer cleaning, photoresist stripping, and precision drying steps where even trace ionic or organic contamination can compromise device performance.

Consumption data from Asia underscores the inelastic nature of this demand. Taiwan’s semiconductor ecosystem recorded a 12% year-over-year increase in IPA usage during 2024–2025, reaching more than 310,000 metric tons, while South Korea consumed approximately 210,000 metric tons to support advanced memory and logic fabs. These volumes are tied to cleanroom expansion rather than end-market electronics demand, making IPA consumption structurally resilient even during cyclical slowdowns in consumer devices.

This demand profile is reshaping global capacity planning. With more than USD 140 billion committed to new fab construction across the United States, Germany, and India by late 2024, chemical suppliers are prioritizing purification upgrades over commodity volume additions. By 2025, close to 40% of all announced global IPA capacity expansions were dedicated specifically to electronic-grade output, reflecting the premium margins and long-term offtake security associated with UHP IPA supply contracts.

Strategic Capacity Pivot of Normal Propanol for Feedstock Security

Normal propanol is increasingly being treated as a strategic intermediate rather than a standalone solvent, particularly in Asia and the Middle East where downstream integration is accelerating. Over 45% of global NPA demand is now concentrated in the Asia-Pacific region, driven by the expansion of propylene oxide and derivative value chains, including glycol ethers and polyols. China’s rapid rollout of HPPO technology, favored for its lower environmental footprint and water-only byproduct, has intensified the pull for stable NPA supply.

Feedstock volatility has further reinforced this trend. In the third quarter of 2025, propanol prices in the United States climbed to USD 1,393 per metric ton following propylene shortages along the Gulf Coast. This episode highlighted the vulnerability of merchant propanol supply models and accelerated investment in integrated production hubs. In response, manufacturers in China and the Middle East are scaling propane dehydrogenation facilities to secure captive propylene, reducing exposure to global supply disruptions and stabilizing cost structures for propanol-based derivatives.

As a result, capacity decisions are increasingly driven by feedstock integration and geographic proximity to downstream consumers rather than export-led solvent trade, marking a structural shift in the global NPA supply landscape.

Commercialization of Bio-Based Propanol through Fermentation Routes

Sustainability-driven procurement policies are opening a high-value niche for bio-based propanol, particularly in personal care, coatings, and specialty cleaning applications where Scope 3 emissions are under scrutiny. Unlike bio-ethanol, bio-propanol offers higher energy density and superior solvency, positioning it as a premium green alternative rather than a direct commodity substitute.

Technological progress has moved fermentation-based propanol closer to commercial viability. Research published in November 2025 shows that optimized microbial strains, including Clostridium beijerinckii, are achieving glucose-to-propanol conversion rates of 70 to 80 grams per liter, a level that supports pilot-to-industrial scale transitions. While production costs remain higher than petrochemical routes, early adopters are willing to absorb premiums for certified low-carbon solvents in regulated and brand-sensitive applications.

Beyond solvents, bio-propanol is being evaluated as a next-generation biofuel component. With global liquid biofuel production reaching 175.2 billion liters in 2024, propanol’s higher volumetric energy content compared to ethanol makes it a candidate for sustainable aviation fuel blending and advanced industrial fuel formulations, extending its opportunity horizon beyond traditional chemical markets.

Integration into the Lithium-Ion Battery Gigafactory Ecosystem

A fast-emerging growth avenue for isopropanol lies in lithium-ion battery manufacturing, where moisture control is a critical determinant of cell safety and performance. As gigafactories scale globally, battery-grade IPA is increasingly used as a precision drying and processing aid during electrode manufacturing.

A 2025 industry study on aqueous electrode processing demonstrated that IPA addition lowers surface tension during slurry drying, preventing mud cracking and enabling the production of thicker electrodes with higher energy density. This capability is essential for long-range electric vehicle batteries, where incremental gains in electrode thickness translate directly into extended driving range.

While dry-electrode technologies promise cost reductions of up to 15%, they remain limited to pilot-scale deployments. The vast majority of global battery production continues to rely on wet-slurry processes, where ultra-pure IPA plays a vital role during calendering and post-drying stages. Maintaining residual moisture at parts-per-million levels is critical to preventing lithium degradation and thermal runaway, positioning battery-grade IPA as a non-negotiable input for current-generation gigafactories.

Propanol Market Share and Segmentation Insights

Isopropanol Leads Global Propanol Market Due to Broad Industrial and Healthcare Applications

Isopropanol accounted for 72.80% of the Propanol Market by type in 2025, reflecting its widespread use across solvents, disinfectants, pharmaceutical manufacturing, and industrial cleaning applications. Isopropyl alcohol offers excellent solvency, rapid evaporation, and strong antimicrobial activity, making it a preferred ingredient in hand sanitizers, surface disinfectants, cosmetics, and industrial cleaning formulations. Global production of isopropanol continues to support large scale demand from healthcare, electronics manufacturing, and chemical processing sectors. In 2025, post pandemic hygiene awareness continues to support elevated isopropanol consumption, with sustained demand for disinfectants and sanitation products across healthcare facilities, institutional environments, and consumer hygiene markets.

Solvent Applications Drive Propanol Demand Across Industrial Manufacturing Processes

Solvent applications represented 38.60% of the Propanol Market by application in 2025, reflecting the compound’s role as a versatile solvent used in coatings, inks, adhesives, pharmaceutical formulations, and industrial cleaning processes. Isopropanol provides effective dissolution of resins, oils, and organic compounds while offering rapid evaporation and compatibility with water based systems. Manufacturing industries rely heavily on solvent grade IPA for product formulation and equipment cleaning processes. In 2025, increasing demand for electronics grade isopropanol is shaping market growth, as semiconductor and electronics manufacturers require ultra high purity solvents for wafer cleaning, surface preparation, and precision electronic component manufacturing.

Propanol Market Competitive Landscape

The global propanol market in 2026 is defined by high-purity pharmaceutical-grade demand, bio-circular n-propanol adoption, and Verbund-integrated production. Industry leaders are optimizing decarbonized supply chains, AI-enabled processing, and feedstock efficiency to address REACH compliance and volatility in ethylene and propylene markets.

BASF Expands Verbund Capacity and Decarbonized Propanol Production for Asia-Pacific Growth

BASF is reinforcing its Verbund integration strategy to maintain cost leadership while advancing green transformation in industrial alcohols. The company projects 2026 EBITDA between €6.2 billion and €7.0 billion, driven by Chemicals and Nutrition & Care segments. The Zhanjiang Verbund site significantly increases localized propanol and intermediates supply for Asia-Pacific pharmaceutical and coatings markets. BASF targets CO2 emissions between 17.2 and 18.2 million metric tons while increasing renewable electricity usage. It secured $75 million DOE funding to accelerate decarbonized production technologies. This positions BASF as a leader in low-carbon, high-purity n-propanol and isopropanol supply chains.

Dow Drives AI-Led Restructuring and Bio-Circular Propanol Portfolio Expansion

Dow is executing its Transform to Outperform strategy to modernize operations and enhance specialty solvent production. The company targets $2 billion EBITDA improvement in 2026, with growth from high-value segments like electronics-grade chemicals. It is shutting down its Freeport propylene oxide facility, shifting supply chains toward more efficient global assets. Dow reported $40 billion in 2025 sales and aims for $500 million in incremental EBITDA gains through AI-driven productivity. Its ISCC PLUS certified bio-circular propanol solutions are targeting sustainable beauty and personal care markets. This strengthens Dow’s positioning in sustainable and high-performance solvent applications.

Eastman Strengthens Circular Solvent Leadership with Molecular Recycling and Cost Optimization

Eastman is leveraging circular economy technologies to sustain competitiveness in high-purity solvent markets. The company generated nearly $1 billion in operating cash flow in 2025 and forecasts stable EPS growth entering 2026. Its Kingsport methanolysis facility delivered $60 million incremental earnings, enabling production of recycled-content chemicals. Eastman increased its cost-reduction target to $125–$150 million to counter global competition. The company focuses on pharmaceutical-grade propanol with strong regulatory compliance under 21 CFR standards. This positions Eastman as a leader in circular, high-purity solvent supply chains.

Sasol Enhances Integrated Alcohol Production with Renewable Energy and Operational Efficiency

Sasol is executing its Grow and Transform strategy with a focus on operational reliability and energy transition. The Secunda Operations achieved a 10% production increase supported by improved coal quality. The company generated positive free cash flow of R0.8 billion in 2026, reflecting disciplined capital management. Sasol secured over 1,200 MW of renewable energy capacity to reduce carbon intensity in n-propanol production. The restart of its Louisiana Integrated Polyethylene cracker strengthens global ethylene derivative supply. This enhances Sasol’s competitiveness in integrated specialty alcohol production.

LOTTE Chemical Accelerates Portfolio Shift Toward High-Performance Materials and Green Solvent Integration

LOTTE Chemical is transitioning from commodity petrochemicals to high-performance materials and eco-friendly solutions. The company reported KRW 18,483 billion in revenue in 2025 and targets profitability recovery in 2026. Its Yulchon compounding plant will expand engineering plastics using propanol-based intermediates. LOTTE is investing in a 60MW hydrogen fuel cell plant to support green material production. The company is aligning with semiconductor and pharmaceutical demand for high-purity solvents. This positions LOTTE as a key Asian player in sustainable and specialty propanol applications.

United States: Semiconductor Purity, VOC Compliance, and Post-Pandemic Capacity Rebalancing

The United States propanol industry is increasingly shaped by semiconductor-grade purity requirements, environmental regulation, and the strategic repurposing of pandemic-era capacity. In April 2025, ExxonMobil announced a $100 million upgrade of its Baton Rouge facility to enable the production of 99.999% ultra-pure isopropanol. This investment is directly aligned with the U.S. semiconductor reshoring agenda, as domestic chipmakers targeting 2-nanometer logic nodes require extremely low metal and moisture contamination in cleaning solvents. Parallel capacity upgrades are underway at smaller specialty producers. In early 2024, Nova Molecular Technologies initiated a $23.75 million expansion in Sumter County, focusing on high-purity propanol grades for pharmaceutical synthesis and electronics cleaning, reinforcing a two-tier market structure that separates commodity IPA from electronic and pharma-grade material.

Regulatory and trade forces are further reshaping demand. Escalating trade tensions in spring 2025 raised tariffs on IPA imports from South Korea and China, increasing domestic solvent and disinfectant production costs and improving the relative competitiveness of U.S.-based producers. At the same time, stricter EPA enforcement of VOC emission limits has accelerated reformulation in downstream sectors. By late 2025, adoption of bio-based propanol formulations in paints and coatings had risen by 14%, while demand for n-propanol in low-VOC adhesives and industrial finishes grew 13% year on year. Importantly, the United States continues to carry record-high IPA capacity built during 2020–2022. This surplus is now being redirected from hand sanitizers toward industrial cleaning, pharmaceutical API synthesis, and electronics manufacturing, supporting utilization without relying on consumer disinfectant demand.

China: Feedstock Economics, Energy Efficiency Mandates, and Electronics Compliance

China’s propanol market dynamics in 2025 reflect a complex interaction between industrial modernization policy, feedstock price volatility, and downstream electronics standards. In September 2025, the Ministry of Industry and Information Technology implemented a nationwide Equipment Renewal action plan, mandating a 20% improvement in energy efficiency across propanol synthesis facilities. This has pushed producers to retrofit reactors, improve heat integration, and optimize hydrogenation steps, favoring large, capitalized players with access to process optimization technologies. However, market conditions have remained mixed. In mid-2025, declining upstream ethylene prices and a subdued real estate sector weighed on construction-related solvent demand, shifting producer focus toward higher-value chemical and electronics applications.

Feedstock economics have provided partial relief. By November 2025, propylene prices fell to their lowest level since 2024, significantly expanding margins for domestic propanol producers even as downstream polypropylene demand remained weak. State-owned refiners such as Sinopec highlighted yield optimization and feedstock diversification strategies in their 3Q 2025 disclosures, positioning propanol as a resilient outlet amid declining refined fuel consumption. Regulatory compliance is also elevating quality standards. The introduction of a new China RoHS Conformity Assessment System in November 2025 has increased purity requirements for solvents used in PCB assembly, reinforcing demand for low-residue, electronics-grade propanol in China’s export-oriented electronics manufacturing base.

India: Infrastructure Pull and Healthcare-Linked Solvent Demand

India’s propanol industry in 2025 has been characterized by steady, infrastructure-driven demand and cautious inventory management. During the first half of the year, n-propanol consumption remained resilient due to sustained offtake from the paints and coatings sector, supported by government-led urban housing schemes and national highway expansion. These projects favor solvent systems that balance drying performance with regulatory compliance, maintaining baseline demand even amid global price volatility.

Short-term supply dynamics also influenced pricing behavior. In early 2025, excess inventories at major ports led to temporary price stabilization, prompting chemical distributors and large consumers to shift toward just-in-time procurement strategies rather than bulk stocking. Beyond construction, public health initiatives are providing incremental support. Expansion of rural healthcare sanitation programs under the Ministry of Jal Shakti in 2025 increased the use of propanol as a disinfectant carrier, reinforcing its role as a multifunctional solvent bridging industrial and institutional applications in the Indian market.

European Union: Supply Security, REACH Signals, and Premium Purity Standards

Within the European Union, the propanol market is increasingly framed by supply chain security and regulatory signaling rather than volume expansion. In Q4 2025, the European Commission established the Critical Chemicals Alliance to monitor capacity closures and dependency risks for essential chemical building blocks, including propanol. This initiative reflects concerns over regional self-sufficiency following years of margin pressure and plant rationalization in basic chemicals. Regulatory developments are also shaping substitution patterns. In November 2025, the European Chemicals Agency recommended restrictions on specific phosphorodithioate derivatives, indirectly stimulating demand for propanol-based alternatives in lubricant and fuel additive formulations.

Sustainability-linked finance is emerging as a structural differentiator. From January 2026, EU labeling rules for green chemicals have simplified access to sustainable finance for producers able to demonstrate low-carbon propanol production pathways. At the national level, Germany has moved ahead of broader EU timelines. Draft updates to German Cosmetics Ordinances in November 2025 introduced stricter purity thresholds for propanol used in personal care and skincare products, reinforcing Europe’s premium positioning in high-specification consumer and specialty applications rather than commodity solvent volumes.

South Korea: Export Adaptation and High-Purity Positioning

South Korea’s propanol market showed signs of stabilization by mid-2025 as manufacturing sentiment improved across electronics and automotive supply chains. This recovery supported steady demand for propanol in precision cleaning of electronic components and automotive coatings. However, exporters have had to adapt rapidly to global trade frictions. Rather than competing on volume, Korean producers have increasingly shifted toward high-purity grades and specialty applications, or relocated portions of production to tariff-neutral jurisdictions to mitigate exposure to escalating trade disputes. This strategic repositioning underscores South Korea’s focus on value retention through quality differentiation rather than scale expansion in the global propanol industry.

Summary Snapshot: Propanol Industry Country Dynamics

Propanol Market County Level Snapshot

|

Region

|

Primary Market Driver

|

Propanol Industry Impact

|

|

United States

|

Semiconductor reshoring, VOC regulation

|

Growth in ultra-pure IPA and low-VOC n-propanol

|

|

China

|

Energy efficiency mandates, feedstock economics

|

Margin support from low propylene prices, higher purity demand

|

|

India

|

Infrastructure spending, sanitation programs

|

Stable coatings demand and disinfectant carrier usage

|

|

European Union

|

Supply security, REACH signaling

|

Shift toward premium, compliant propanol applications

|

|

South Korea

|

Trade adaptation, electronics recovery

|

Emphasis on high-purity grades and export resilience

|

Propanol Market Report Scope

Propanol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8 Billion

|

|

Market Size (2034)

|

$14.2 Billion

|

|

Market Growth Rate

|

6.6%

|

|

Segments

|

By Type (Isopropanol, n-Propanol), By Production Process (Indirect Hydration, Direct Hydration, Ethylene Hydrogenation, Bio-Based Fermentation), By Application (Solvents, Chemical Intermediates, Disinfectants & Sanitizers, Electronics Cleaning, Extraction & Laboratory Use)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ExxonMobil Corporation, Shell Chemicals, Dow Chemical Company, BASF SE, Sinopec Group, Sasol Limited, LyondellBasell Industries NV, INEOS Group, Mitsui Chemicals Inc., Lotte Chemical Corporation, LG Chem Ltd., Deepak Fertilisers and Petrochemicals Corporation Limited, Tokuyama Corporation, Nippon Refine Co. Ltd., Nova Molecular Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Propanol Market Segmentation

By Type

By Production Process

- Indirect Hydration

- Direct Hydration

- Ethylene Hydrogenation

- Bio-Based Fermentation

By Application

- Solvents

- Chemical Intermediates

- Disinfectants & Sanitizers

- Electronics Cleaning

- Extraction & Laboratory Use

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Propanol Industry

- ExxonMobil Corporation

- Shell Chemicals

- Dow Chemical Company

- BASF SE

- Sinopec Group

- Sasol Limited

- LyondellBasell Industries NV

- INEOS Group

- Mitsui Chemicals Inc.

- Lotte Chemical Corporation

- LG Chem Ltd.

- Deepak Fertilisers and Petrochemicals Corporation Limited

- Tokuyama Corporation

- Nippon Refine Co. Ltd.

- Nova Molecular Technologies

*- List not Exhaustive