Surface Disinfectants Market 2025–2034: $6.2 Billion to $11.8 Billion at 7.4% CAGR Driven by Hospital-Grade Formulations, Smart IoT Hygiene Systems, and Plastic-Free Delivery Platforms

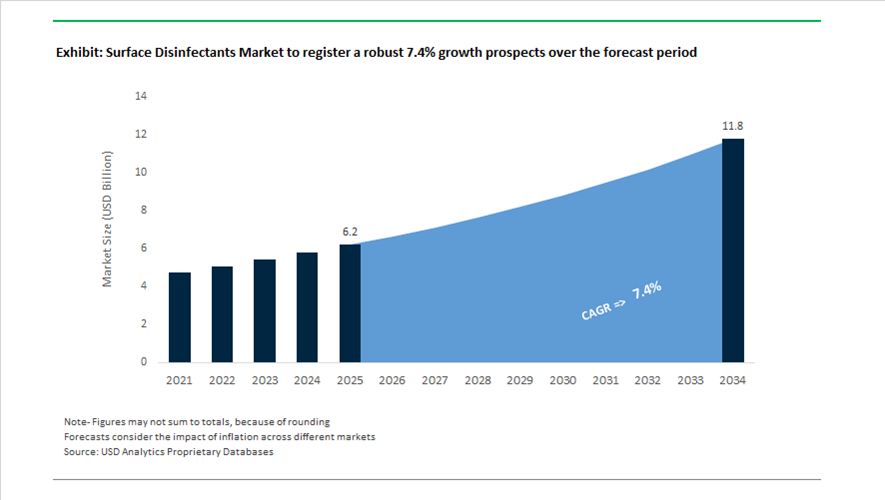

The global surface disinfectants market is valued at $6.2 billion in 2025 and is projected to reach $11.8 billion by 2034, expanding at a CAGR of 7.4%. Growth is supported by sustained institutional demand for hospital-grade disinfectants, EPA-registered surface sanitizers, quaternary ammonium compounds, hydrogen peroxide-based cleaners, and alcohol-based surface sprays across healthcare, education, transportation, hospitality, and residential segments. Increasing infection control compliance, antimicrobial resistance management, allergen-neutralizing formulations, and digital cleaning validation systems are redefining product development in the B2B hygiene chemicals landscape. Manufacturers are prioritizing low-residue chemistry, electronics-safe disinfectant wipes, smart-home compatible sanitation products, and sustainable concentrate systems to meet evolving regulatory and ESG requirements.

Technology integration and sustainability transformation accelerated in 2024 and 2025. In March 2024, Diversey partnered with Microsoft to deploy Azure IoT-enabled cleaning systems that monitor disinfectant “kill times” through sensor-driven validation, ensuring EPA-mandated dwell times are consistently achieved in healthcare and commercial facilities. In June 2024, Solenis acquired Aqua ChemPacs, adding dissolvable cleaning pod technology to its disinfectant portfolio, significantly reducing plastic packaging and freight emissions associated with liquid concentrates. Finalized in late 2024, BASF divested its industrial cleaning and hygiene ingredient assets to Louis Dreyfus Company, enabling LDC to enter the specialty disinfectant intermediates segment while BASF sharpened its focus on high-purity medical-grade chemical production. In March 2025, TABBSZ introduced water-soluble disinfectant tablets formulated with plant-based surfactants, enabling point-of-use dilution and eliminating single-use plastic bottles. In May 2025, CloroxPro secured a nationwide supply agreement with Vizient, reinforcing distribution of hospital-grade surface disinfectants across major U.S. healthcare networks. In September 2025, CloroxPro launched Screen+ sanitizing wipes engineered for sensitive medical electronics, delivering non-corrosive pathogen control without damaging touchscreen coatings. During the same month, GOJO Industries introduced Purell Clean & Go hybrid wipes designed for dual skin and surface disinfection in mobile environments.

Strategic consolidation and product diversification intensified in 2026. In January 2026, The Clorox Company announced a $2.25 billion agreement to acquire GOJO Industries, combining Clorox’s surface disinfectant leadership with the Purell brand’s dominance in skin hygiene to create an integrated B2B and retail infection prevention platform. In January 2026, Clorox launched PURE Allergen Neutralizer, expanding the disinfectant category into chemical neutralization of pet dander and dust mite allergens on both hard and soft surfaces. In January 2025, Reckitt initiated development of a major R&D and Innovation Centre in Shanghai, expected to reach full operational capacity by 2026, focused on adapting Lysol disinfectant chemistries for high-density Asian urban settings and smart-home sanitation ecosystems. In January 2026, Ecolab partnered with CDP to introduce new “Water Performance” benchmarks for chemical manufacturers, addressing the water intensity of disinfectant formulation and dilution processes. These mergers, IoT-enabled compliance systems, allergen-neutralizing chemistries, and plastic-free concentration technologies are structurally strengthening the global surface disinfectants market through 2034.

Structural Trends and High-ROI Opportunities in the Surface Disinfectants Market

Healthcare Consolidation on EPA-Registered One-Step Disinfectants

Healthcare systems across North America and Europe are accelerating procurement consolidation toward EPA-registered one-step cleaner disinfectants as part of broader “Standardization of Care” initiatives. These products eliminate the need for separate cleaning and disinfection steps, directly addressing one of the most persistent operational risks in infection control: incorrect dwell time. In high-acuity environments where environmental services teams manage hundreds of rooms per shift, reducing procedural complexity has become a frontline defense against Healthcare-Associated Infections.

Updated guidance released in November 2025 by bodies such as the Provincial Infectious Diseases Advisory Committee and aligned U.S. advisory groups highlighted that EPA List N and List Q one-step disinfectants can cut total surface cleaning time by up to 30%. This efficiency gain is strategically significant given that approximately one in 31 hospitalized patients acquires at least one HAI on any given day, translating infection prevention directly into cost avoidance and patient outcome metrics.

Procurement data from tertiary care hospitals in late 2024 further reinforces this shift. Facilities that standardized on hydrogen peroxide-based one-step disinfectants reported a 32% reduction in MRSA surface contamination within the first year of implementation. These outcomes are now driving multi-year, multi-million dollar supply contracts that bundle chemistry with closed-loop dilution and dispensing systems, reducing human error, chemical waste, and compliance risk. As hospital networks continue to consolidate, preferred vendor status in one-step disinfectants is becoming a decisive competitive advantage.

De-Risking Formulations as Regulators Move Away from Quats

Quaternary Ammonium Compounds have long been the backbone of surface disinfection, but regulatory and scientific scrutiny is rapidly eroding their default status. Concerns around antimicrobial resistance, occupational asthma, and chronic respiratory exposure are prompting regulators to reassess the long-term safety profile of Quats, particularly in high-frequency use environments such as healthcare, schools, and public facilities.

In January 2025, California’s Department of Toxic Substances Control convened a public workshop under the Safer Consumer Products Program to evaluate Quats as potential Priority Products. A Technical Document expected in Fall 2025 is widely anticipated to mandate alternatives analysis for selected Quat chemistries, setting a regulatory precedent that often cascades into national and international markets. Parallel pressure is emerging in the EU through occupational safety frameworks and eco-label procurement criteria.

This regulatory trajectory is accelerating the adoption of safer chemistries, most notably hydrogen peroxide, citric acid, and lactic acid-based disinfectants. The bio-based and low-toxicity segment is now growing materially faster than legacy formulations, particularly in North America, where over one quarter of surface disinfectant revenues are already tied to non-toxic or Safer Choice-aligned products. Strategic partnerships announced in late 2024 to scale sustainable hydrogen peroxide production underscore that formulators are repositioning portfolios well ahead of formal bans, treating de-risking as a growth strategy rather than a compliance cost.

Material-Compatible Disinfectants for Public High-Touch Electronics

The proliferation of interactive displays, self-service kiosks, and touch-enabled appliances in retail, transit, and healthcare has exposed a critical gap in the surface disinfectants market. Conventional chemistries often damage oleophobic coatings, cause stress cracking in polycarbonate housings, or leave residues that degrade optical clarity. This has created a premium opportunity for OEM-validated, material-compatible disinfectants engineered specifically for sensitive electronics.

Research published in 2025 emphasizes that public touchscreen hygiene requires kill times under 60 seconds to be operationally viable, ruling out many mild formulations. At the same time, electronics manufacturers are increasingly issuing Approved Vendor Lists for disinfectants that do not compromise device longevity or warranties. Alcohol-free, residue-free wipes based on accelerated hydrogen peroxide or pH-neutral organic acids are emerging as preferred solutions because they deliver rapid efficacy without corrosivity or streaking.

For disinfectant manufacturers, qualification by appliance, display, and medical device OEMs represents a defensible growth lever. Once validated, these formulations are often embedded into service contracts, facilities management tenders, and aftermarket consumables programs, creating recurring revenue streams with higher margins than commoditized hard-surface cleaners.

Durable Residual Antimicrobial Coatings for High-Traffic Infrastructure

While conventional disinfectants provide point-in-time sanitation, high-traffic environments increasingly demand continuous protection. Residual Antimicrobial Coatings are gaining strategic relevance in transit systems, airports, hospitality, and large venues where frequent reapplication of liquid disinfectants is impractical. These coatings aim to suppress microbial load over extended periods, fundamentally shifting the infection control paradigm from reactive to preventative.

As of April 2025, the EPA’s residual efficacy guidance formally distinguishes between 24-hour residual disinfectants and longer-lasting supplemental residual products that must withstand rigorous abrasion and wear testing. Only a limited set of copper-based surfaces and specialized silane systems currently meet these standards, underscoring the technical barriers to entry.

Real-world deployments in public transportation systems reported in September 2025 demonstrated sustained viral load reductions following copper-film installation. However, the most scalable opportunity lies in transparent, spray-applied coatings capable of surviving more than 50 industrial wash cycles, a requirement in hospitality and healthcare. Studies indicate that such durable coatings can reduce infection rates by up to 80% in high-occupancy settings, positioning residual antimicrobial technologies as a cornerstone opportunity for surface disinfectant manufacturers seeking differentiation beyond traditional liquid formulations.

Surface Disinfectants Market Share and Segmentation Insights

Chemical-Based Disinfectants Dominate with Broad-Spectrum Efficacy and Regulatory Compliance Demand

Chemical-based disinfectants accounted for 72.80% of the surface disinfectants market in 2025, supported by their proven broad-spectrum antimicrobial efficacy, rapid kill times, and regulatory approvals across critical sectors. Products such as quaternary ammonium compounds, sodium hypochlorite, hydrogen peroxide, and alcohol-based disinfectants remain industry standards for infection control in healthcare, commercial, and industrial environments. Their compatibility with EPA-registered disinfection protocols and pathogen-specific claims reinforces adoption across high-risk settings. The 2025 market dynamic reflects permanently elevated hygiene standards, with sustained demand across hospitals, educational institutions, offices, and households, as organizations maintain stringent sanitation practices and compliance-driven disinfection programs.

Healthcare Facilities Lead Surface Disinfectant Demand with Strict Infection Control Protocols

Healthcare facilities accounted for 38.60% of surface disinfectants market demand in 2025, driven by the need for rigorous infection prevention and control (IPC) protocols across hospitals, clinics, and long-term care centers. High-frequency disinfection of patient rooms, surgical areas, medical equipment, and high-touch surfaces sustains consistent product consumption. Disinfectants must meet hospital-grade standards with proven efficacy against pathogens such as C. diff, MRSA, VRE, and norovirus, reinforcing reliance on high-performance chemical formulations. The 2025 trend highlights standardized infection control protocols, where healthcare providers continue elevated disinfection practices, ensuring compliance with regulatory guidelines and prioritizing patient safety through validated, high-efficacy disinfectant solutions.

Surface Disinfectants Market Competitive Landscape

The surface disinfectants market in 2026 is defined by residual antimicrobial protection, non-corrosive formulations, and IoT-enabled hygiene compliance. Competition is shifting toward 24-hour efficacy, sustainable biocides, and data-integrated disinfection systems across healthcare, hospitality, and high-traffic public environments.

Ecolab Scales AI-Integrated Hygiene and Water Circularity Solutions for High-Purity Disinfection

Ecolab is strengthening its leadership in surface disinfectants through AI-driven hygiene systems and integrated water management solutions. The company reported strong 2025 performance with projected 2026 EPS of $8.43–$8.63, driven by Life Sciences and Food & Beverage growth. Its acquisition of Ovivo Electronics expands capabilities in ultrapure water and cleanroom disinfection for semiconductor environments. The “One Ecolab” initiative is targeting $325 million in savings, reinvested into automated hygiene monitoring and chemical optimization platforms. Its Watermark™ data-driven framework supports industrial clients in managing water and sanitation demands. Ecolab’s global service infrastructure enables end-to-end infection prevention across critical industries.

Reckitt Expands Lysol Pro Solutions with Multi-Modal Disinfection for High-Traffic Environments

Reckitt is advancing its professional disinfectant portfolio by scaling Lysol Pro Solutions across institutional hygiene markets. The company reported double-digit growth in laundry and air sanitizer segments in 2026, driven by demand in healthcare and hospitality. Its Germ Protection division is strengthening market share through high-performance wipes and surface disinfectants. Reckitt is investing in antimicrobial polymers that provide extended residual protection on surfaces. The company targets high-traffic public spaces with integrated hygiene programs that combine disinfection protocols and brand-driven reassurance. Strategic capital restructuring supports reinvestment in premium disinfection technologies and product innovation.

Clorox Accelerates Digital Transformation and Residual Disinfection for Healthcare and Electronics

Clorox is enhancing its competitive position through digital transformation and rapid innovation in professional disinfectants. Its ERP rollout in 2026 enables 65% faster product development cycles and improved supply chain responsiveness. CloroxPro expanded its Screen+ wipes portfolio, targeting high-touch electronic devices in healthcare environments. The IGNITE strategy focuses on EcoClean formulations using plant-based actives aligned with ESG procurement requirements. The company maintains leadership in bleach and accelerated hydrogen peroxide technologies, delivering rapid kill times against resistant pathogens. Its residual disinfection capabilities and Safe Choice-certified solutions strengthen its presence in healthcare and education sectors.

BASF Enables Green Disinfectant Formulations with Bio-Based Surfactants and Regulatory Expertise

BASF plays a critical upstream role in the surface disinfectants market by supplying bio-based surfactants and biodegradable intermediates. The company divested its Aseptrol® chlorine dioxide business in 2026 to focus on high-growth sustainable cleaning ingredients. Its innovations include biodegradable polymers and opacifiers that enhance formulation aesthetics without compromising antimicrobial performance. BASF is scaling biomass balance (BMB) intermediates, enabling formulators to develop renewable-origin disinfectants. With North American sales of $18.1 billion in 2025, the company continues to expand its Care Chemicals footprint. Its regulatory expertise accelerates product approvals under ECHA and EPA frameworks.

STERIS Advances Automated Sterilization and Low-Water Disinfection Technologies for Healthcare Systems

STERIS is leading innovation in high-end healthcare disinfection through automated and water-efficient sterilization systems. Its STERI-Green PLUS technology reduces water consumption by 99%, addressing sustainability mandates in hospital operations. The ConnectAssure platform enables paperless sterile processing by digitally logging disinfection cycles for compliance. The Prolystica® product line emphasizes environmentally safe formulations free from phosphates and harmful surfactants. STERIS is expanding its global Applied Sterilization Technologies network, focusing on E-beam and X-ray sterilization alternatives. Its integrated hardware-software approach enhances infection control efficiency and traceability in critical healthcare environments.

United States Surface Disinfectants Market Shaped by Residual Protection and Healthcare Sustainability

The United States surface disinfectants market is undergoing a structural shift as the Environmental Protection Agency expanded List N in 2025–2026 to recognize Supplemental Residual Antimicrobial Products. This regulatory evolution moves the industry beyond kill-on-contact chemistry toward long-lasting surface protection, with certified formulations capable of maintaining antimicrobial activity for weeks or longer after a single application. The change has accelerated innovation in polymer-bound actives, stabilized oxidizers, and surface-bonding technologies, particularly for healthcare, transportation, and critical infrastructure settings. Parallel public health guidance from the Centers for Disease Control and Prevention has intensified surface testing protocols in long-term care facilities, driving a measurable transition from traditional quaternary ammonium compounds toward stabilized hydrogen peroxide systems that address antimicrobial resistance concerns while maintaining broad-spectrum efficacy.

Product innovation and supply-chain resilience are equally prominent. In September 2025, The Clorox Company expanded its professional portfolio with electronic-safe disinfectant wipes engineered to protect sensitive touchscreen substrates without delamination risk. At the enterprise level, the company completed a major ERP rollout at the start of fiscal 2026, enhancing real-time visibility across professional disinfectant supply chains and enabling rapid regional response to outbreak spikes. Sustainability has become a competitive differentiator, exemplified by Ecolab commercializing the first EPA-registered plastic-free hospital disinfectant wipe in early 2025. Derived from wood pulp fibers, this solution directly addresses clinical plastic waste while meeting stringent antimicrobial performance benchmarks.

China Surface Disinfectants Market Driven by Automation, Purity, and Biocompatibility

China’s surface disinfectants industry is being reshaped by state-led public health automation and tighter occupational safety oversight. Under the Healthy China 2030 framework, subsidies accelerated in 2025 for UV-C sterilization systems and electrostatic sprayers across public transit hubs, with Tier-1 cities targeting near-universal automated disinfection coverage. This policy push has expanded demand for complementary chemical disinfectants optimized for rapid-cycle application and compatibility with automated delivery systems. Simultaneously, the State Administration for Market Regulation introduced stricter registration requirements, mandating advanced biocompatibility testing to mitigate respiratory exposure risks for cleaning personnel, particularly in high-frequency commercial environments.

Capacity expansion is increasingly concentrated in eco-friendly and ultra-high-purity segments. Industrial park data from Zhejiang indicates a substantial scale-up in bio-based disinfectants formulated with plant-derived enzymes to meet rising consumer and institutional demand for low-toxicity solutions. At the high end, domestic chemical producers expanded ultra-high-purity peracetic acid production in 2025 to support cleanroom disinfection for semiconductor lithography and advanced chip packaging. This convergence of public health, electronics manufacturing, and green chemistry is positioning China as both a volume producer and a technical supplier of application-specific surface disinfectants.

United Kingdom and European Union Market Defined by Regulatory Uncertainty and Portfolio Repositioning

The surface disinfectants market across the United Kingdom and European Union is navigating a complex regulatory transition under the Biocidal Products Regulation. The European Chemicals Agency scheduled approvals for several active substances in October 2026, compelling manufacturers to reformulate extensive product portfolios well in advance to avoid market disruption. Compounding this, the Biocidal Products Committee postponed its final opinion on ethanol in late 2025, creating interim uncertainty that has favored isopropanol- and hydrogen peroxide-based alternatives across healthcare and institutional corridors. These dynamics have elevated regulatory intelligence and reformulation agility as core competitive capabilities.

Strategic portfolio realignment is reshaping the competitive landscape. In July 2025, Reckitt Benckiser announced the divestment of its Essential Home business to concentrate investment on Powerbrands such as Lysol and Dettol, a move designed to accelerate clinical-grade germ protection R&D. Complementing this focus, the company inaugurated a Global Science and Innovation facility in Shanghai in mid-2025 to develop region-specific hygiene solutions, underscoring a globalized innovation model where regulatory compliance and performance differentiation are developed in parallel.

Japan Surface Disinfectants Market Anchored in Supply Security and Material Compatibility

Japan’s surface disinfectants industry is distinguished by its emphasis on supply stability and advanced material compatibility. Amendments to the Pharmaceuticals and Medical Devices Act enacted in May 2025 introduced the Supply System Manager requirement, obligating manufacturers to notify authorities of shipment disruptions and ensuring continuity of hospital-grade disinfectant supply during public health emergencies. This framework elevates operational transparency and favors producers with resilient domestic manufacturing and inventory management systems.

Chemical safety and application specificity are advancing in tandem. The Ministry of Health, Labour and Welfare expanded the Existing and New Chemical Substances inventory in December 2025, adding numerous high-performance surfactants that enable low-toxicity disinfectant formulations. Japanese manufacturers have leveraged these approvals to launch neutral pH disinfectants tailored for robotics and automation environments, ensuring corrosion-free performance on sensitive joints and components of disinfection-assistant robots. This alignment between chemical formulation and advanced manufacturing infrastructure reinforces Japan’s role as a precision-driven market for next-generation surface hygiene solutions.

Comparative Snapshot: Surface Disinfectants Industry by Country

Surface Disinfectants Market County Level Snapshot

|

Region

|

Primary Regulatory Driver

|

Innovation Focus

|

Market Differentiator

|

|

United States

|

EPA List N residual standards

|

Long-lasting antimicrobials and plastic-free formats

|

Supply-chain digitalization and AMR-aligned chemistry

|

|

China

|

Healthy China 2030 and SAMR reforms

|

Automated disinfection and ultra-high-purity actives

|

Scale in automation and semiconductor-grade purity

|

|

UK / EU

|

BPR approvals and ethanol review

|

Reformulation and portfolio consolidation

|

Regulatory agility and clinical-grade brand focus

|

|

Japan

|

PMD Act supply security

|

Material-compatible, low-toxicity formulations

|

Reliability and advanced equipment compatibility

|

Surface Disinfectants Market Report Scope

Surface Disinfectants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.2 Billion

|

|

Market Size (2034)

|

$11.8 Billion

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Composition (Chemical-Based Disinfectants, Bio-Based and Natural Disinfectants, Alternative Disinfection Technologies), By Form (Liquid Disinfectants, Disinfectant Wipes, Sprays, Gels and Foams), By End-Use Sector (Healthcare Facilities, Commercial and Institutional, Industrial and Manufacturing, Residential and Household)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Clorox Company, Reckitt Benckiser Group plc, Ecolab Inc., Procter & Gamble Company, Diversey Holdings, Ltd., S. C. Johnson & Son, Inc., Metrex Research, LLC, Cantel Medical Corporation, CarrollCLEAN, Whiteley Corporation, Gojo Industries, Inc., Saraya Co., Ltd., Henkel AG & Co. KGaA, 3M Company, Schülke & Mayr GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Surface Disinfectants Market Segmentation

By Composition

- Chemical-Based Disinfectants

- Bio-Based and Natural Disinfectants

- Alternative Disinfection Technologies

By Form

- Liquid Disinfectants

- Disinfectant Wipes

- Sprays

- Gels and Foams

By End-Use Sector

- Healthcare Facilities

- Commercial and Institutional

- Industrial and Manufacturing

- Residential and Household

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Surface Disinfectants Industry

- The Clorox Company

- Reckitt Benckiser Group plc

- Ecolab Inc.

- Procter & Gamble Company

- Diversey Holdings, Ltd.

- S. C. Johnson & Son, Inc.

- Metrex Research, LLC

- Cantel Medical Corporation

- CarrollCLEAN

- Whiteley Corporation

- Gojo Industries, Inc.

- Saraya Co., Ltd.

- Henkel AG & Co. KGaA

- 3M Company

- Schülke & Mayr GmbH

*- List not Exhaustive