Market Overview: Alcohol Based Disinfectant Market to Reach $5.6 Billion by 2034 as Healthcare Standards, Bio-Based Alcohols, and Regulatory Tightening Reshape Industry Structure

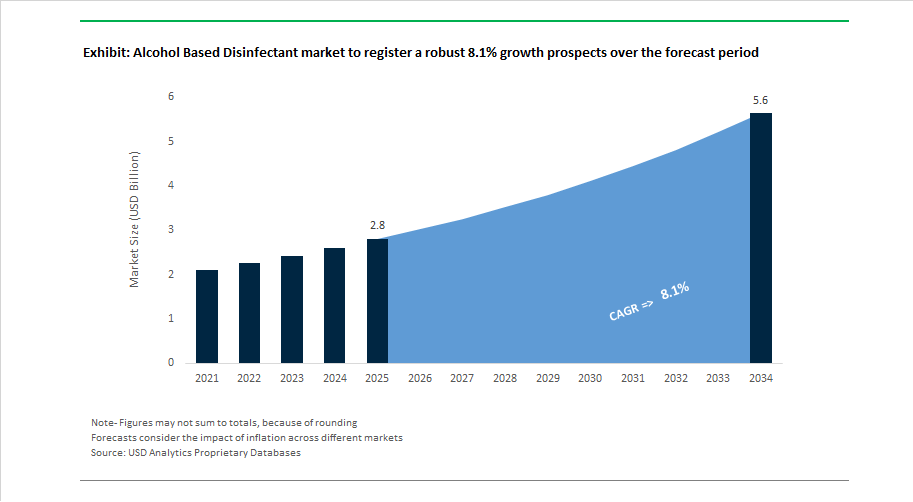

The global alcohol based disinfectant market is projected to grow from $2.8 billion in 2025 to $5.6 billion by 2034, registering a strong 8.1% CAGR driven by persistent demand for hospital-grade surface disinfectants, surgical skin antiseptics, hand sanitizers, and industrial IPA sterilization solutions. Alcohol-based formulations containing ethanol, isopropyl alcohol (IPA), and chlorhexidine blends remain essential due to rapid antimicrobial efficacy against bacteria, fungi, and enveloped viruses. Growth is linked to stricter healthcare hygiene protocols, expansion of outpatient surgical centers, semiconductor cleanroom sterilization needs, and rising awareness of infection prevention in commercial environments. Sustainability and safety considerations are shaping production, with manufacturers adopting low-carbon bio-based alcohols, water-efficient distillation systems, and dermal-safe emollient technologies to balance efficacy with environmental and occupational health standards.

Regulatory and product innovation momentum began building in April 2024 when 3M introduced SoluPrep S sterile antiseptic solution combining 70% IPA with chlorhexidine gluconate for presurgical skin preparation. In the same month, Neogen Corporation launched Farm Fluid MAX for agricultural biosecurity applications. Global harmonization advanced in late 2024 as ISO issued new safety and labeling standards for alcohol-based sanitizers. Market regulation tightened in early 2025 when the US FDA enforced new impurity testing requirements for industrial sanitizers, reducing participation of smaller producers. Sustainability initiatives strengthened in June 2025 as Procter & Gamble expanded bio-based alcohol production for its hygiene product lines. Mid-2025 saw major brands including GOJO and Ecolab introduce dermal-safe foaming alcohol sanitizers with advanced moisturizers to address skin irritation from frequent use.

Strategic consolidation and supply chain realignment accelerated in late 2025 as tariff adjustments on ethanol and IPA imports prompted regional production shifts. In December 2025, Reckitt divested its Essential Home portfolio to concentrate resources on Lysol and Dettol disinfectant lines, while Ecolab finalized acquisition of Ovivo’s electronics water business to integrate high-purity sterilization solutions for semiconductor manufacturing. The industry’s largest consolidation occurred in January 2026 when The Clorox Company agreed to acquire GOJO Industries, combining surface disinfection and hand hygiene leadership. Regional growth intensified in early 2026 as India and Southeast Asia expanded production capacity to serve private healthcare and electronics assembly sectors. Sustainability performance benchmarking advanced in January 2026 through Ecolab’s partnership with CDP to promote water efficiency across alcohol production operations, reinforcing the sector’s shift toward resource-optimized disinfectant manufacturing.

Strategic Market Trends and High-Value Opportunities Reshaping the Alcohol-Based Disinfectant Market

Market Trend: Portfolio Rationalization and Shift Toward Clinical and High-Level Disinfection SKUs

The post-COVID market has moved firmly into a consolidation cycle. Major brands are exiting low-differentiation sanitizer categories and instead investing in professional-grade alcohol disinfectants designed for hospitals, long-term care centers, clinics, and surgical settings. Reckitt Benckiser’s 2025 portfolio strategy is a strong example: manufacturing lines are being consolidated and capital is being redirected into high-margin Powerbrands such as Dettol and Lysol, where clinical-grade, multi-surface disinfectants command premium pricing and recurring purchasing contracts.

Ecolab is elevating differentiation through R&D, targeting high-level disinfection where kill time, pathogen coverage, and material compatibility determine procurement decisions. The company’s Disinfectant 1 Wipe enables one-minute kill performance against over 40 clinical pathogens, including C. auris and Norovirus—meeting emerging hospital audit benchmarks. Industry-wide divestitures are also signaling structural change. Multiple chemical manufacturers divested generic ethanol-based sanitizer operations in mid-2025, allowing them to reallocate R&D into proprietary isopropyl-alcohol (IPA) virucidal blends engineered for compatibility with high-value medical equipment such as CT and MRI surfaces.

Market Trend: Heightened Regulatory Oversight Driving Mandatory Reformulation and Compliance Investments

Regulation is now a primary force shaping product life cycles. The U.S. FDA’s 2025 Over-the-Counter Monograph update increased facility fees under OMUFA by 10 percent, raising fixed cost-of-participation and effectively reducing the number of low-scale entrants. The same year, enforcement of methanol-contamination requirements under the final FDA guidance forced producers to install Gas Chromatography (GC) purity testing capabilities or pivot to certified high-purity alcohol suppliers. This has become a competitive barrier, separating GMP-qualified players from opportunistic pandemic-era entrants.

In Europe, ECHA’s Biocidal Products Regulation (BPR) review for ethanol is changing participation economics. Formulation dossier submissions now cost €200,000 to €500,000 per SKU, limiting the field to manufacturers with strong regulatory and documentation infrastructure. Compliance is no longer a paperwork requirement; it has become a capital allocation strategy where firms that can sustain regulatory spending will own institutional-grade disinfectant contracts.

Market Opportunity: Healthcare Modernization and HAI Prevention Unlock Non-Cyclical, Procurement-Backed Growth

Global investments in hospital infrastructure are creating durable demand for alcohol-based disinfectants. NHS England’s National Standards of Healthcare Cleanliness 2025 introduced a new hospital “Star Rating” system tied to audit-verified disinfection protocols. These standards drive long-horizon product purchasing, tying disinfectant suppliers into multi-year procurement cycles.

India’s PM-ABHIM program, with a total outlay exceeding ₹64,000 crore (~USD 7.7 billion) through 2026, is expanding critical care capacity across district hospitals, where alcohol-based surgical rubs and clinical surface disinfectants are required for accreditation. Hospitals are additionally seeking residue-free IPA disinfectants suitable for digital diagnostic screens and EHR tablets, where surface damage risk previously limited the use of aggressive cleaners. This represents a distinguishing revenue channel for suppliers offering non-corrosive, medical-device-safe formulations.

Market Opportunity: Ultra-Pure Alcohol for Semiconductor and EV Battery Manufacturing Creates a Parallel Growth Engine

A major expansion front is emerging outside healthcare: high-purity alcohol demand in advanced manufacturing. Semiconductor fabs require 5N-grade (99.999% pure) IPA, used to clean wafers and sterilize cleanroom equipment, where microscopic contaminants can destroy production batches. Producers such as LCY Group are scaling to reach 50,000 tons of electronic-grade IPA capacity by 2028, signaling industrial-scale demand alignment.

The EV battery sector presents a complementary growth engine. Residue-free IPA is increasingly relied upon to clean electrodes and foil layers, ensuring proper formation of the Solid Electrolyte Interphase (SEI). Contamination at this phase can trigger early cell aging or thermal failures, making high-purity IPA a mission-critical consumable. With the U.S. and European Chips Acts unlocking USD 200 billion in semiconductor project announcements, every new fabrication plant requires thousands of gallons of IPA annually for cleanroom maintenance—positioning alcohol-based disinfectants and solvents as essential feedstock for next-generation energy and electronics supply chains.

Alcohol-based disinfectants are evolving into two parallel product classes: clinical-grade medical disinfection products that rely on regulatory qualification and recurring hospital procurement, and ultra-pure industrial alcohols used as consumable components within semiconductor and EV manufacturing ecosystems. Companies that control pharmaceutical-grade IPA supply, maintain regulatory compliance readiness, and continue innovating in residue-free disinfection chemistry are expected to lead the market’s high-margin growth trajectory through 2030.

Alcohol Based Disinfectant Market Share and Segmentation Insights

Market Share by Product Type: Ethanol Leads as IPA Retains Industrial Stronghold

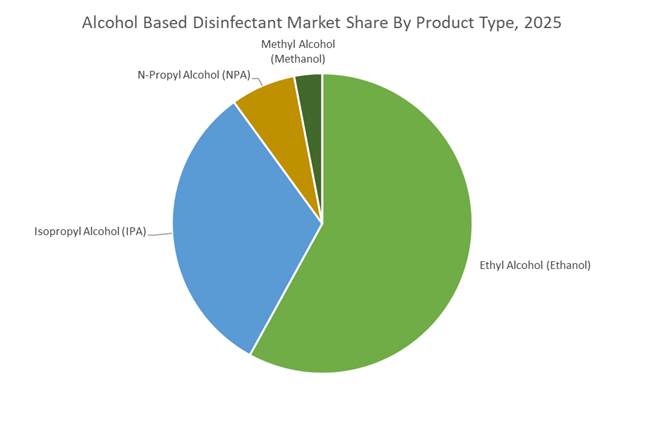

Ethyl alcohol (ethanol) represents approximately 58% of the global alcohol based disinfectant market in 2025, maintaining clear dominance due to its favorable safety profile, low dermal toxicity, and endorsement by WHO and FDA guidelines requiring minimum 60% concentration for effective hand sanitization. Denatured ethanol formulations remain standard for hand sanitizers and skin antiseptics. Following pandemic-driven oversupply and inventory destocking in 2023 to 2024, demand has stabilized at structurally elevated levels versus 2019. Isopropyl alcohol (IPA) ranks second, widely used for surface disinfection, medical prep pads, pharmaceutical cleanrooms, and electronics manufacturing due to rapid evaporation and minimal residue. N-propyl alcohol holds a small, specialized share, constrained by toxicity concerns and EU cosmetic restrictions. Methanol accounts for the smallest legitimate share, restricted to industrial applications or denaturant use, with regulatory crackdowns significantly limiting improper sanitizer use.

Market Share by End User: Healthcare Facilities Anchor Demand in the Post-Pandemic Era

Healthcare facilities account for roughly 44% of alcohol based disinfectant consumption in 2025, forming the most stable and premium segment. Hospitals, clinics, dental offices, and long-term care institutions rely on alcohol-based hand rubs, surgical scrubs, and disinfectant wipes under permanent compliance frameworks from WHO, CDC, and accreditation bodies. Commercial establishments rank second, reflecting normalized dispenser usage across offices, retail, hospitality, and food service, with refill-driven purchasing replacing prior panic buying patterns. Residential consumers experienced the sharpest correction after pandemic stockpiling, with per-household volumes normalizing though baseline penetration remains higher than pre-2020 levels. Industrial users represent the smallest but highly specification-driven segment, encompassing pharmaceutical cleanrooms, electronics assembly, and food processing sanitation. Demand here is non-discretionary and closely linked to industrial output indices, ensuring stable procurement regardless of consumer sentiment.

Competitive Landscape: Digital Hygiene Platforms and Skin-Safe Formulations Transforming the Alcohol Based Disinfectant Market

The Alcohol Based Disinfectant Market is shifting from commodity sanitizers toward integrated infection-prevention ecosystems combining smart dispensing, skin-barrier protection, and sustainability-led packaging. Growth is increasingly driven by healthcare digitization, cleanroom expansion for semiconductor manufacturing, and institutional demand across education, hospitality, and travel. Leading players are differentiating through data-enabled compliance monitoring, surgical-grade formulations, and brand-led consumer trust, while expanding alcohol-based portfolios into emerging applications such as air sanitation and AI hardware facilities.

Ecolab Inc. integrates smart hygiene analytics with clinical-grade alcohol disinfectants

Ecolab Inc. leads professional infection prevention by embedding alcohol-based disinfectants into its Total Plant hygiene architecture. Through platforms such as DishIQ™, Ecolab delivers real-time compliance and usage data to hospitals and food processors, reducing outbreak risk via predictive hygiene management. In late 2025, the company introduced next-generation Surgical Hand Rubs with enhanced emollients, supporting 15+ daily applications without skin barrier damage. Its portfolio includes Skinman Soft Protect and Manusept® via BODE Chemie. Strategically, Ecolab is expanding into semiconductor and data center cleanrooms, positioning alcohol-based disinfection as foundational to AI-era manufacturing hygiene.

The Clorox Company consolidates surface and skin hygiene leadership through Purell integration

The Clorox Company cemented category dominance with its January 2026 acquisition of GOJO Industries for $2.25 billion, bringing the Purell brand into its CloroxPro professional and retail ecosystems. This move created a unified platform spanning surface disinfectants and hand sanitizers for schools, healthcare, and workplaces. Clorox is leveraging its global retail reach to accelerate Purell penetration into big-box and international markets. Product innovation includes the EcoClean line with plant-based actives, reinforcing Clorox’s positioning as a one-stop hygiene provider for eco-conscious institutional buyers.

3M Company advances surgical disinfection with precision antiseptic systems

3M applies its “Science of Safety” platform to medical-grade alcohol disinfectants optimized for operating rooms and critical care. Its flagship SoluPrep™ S surgical prep delivers visible coverage and antimicrobial persistence up to 96 hours. In 2025, 3M deployed AI-driven supply chain analytics to forecast regional demand spikes, preventing hospital stock-outs. Beyond healthcare, its alcohol-based chemistries are increasingly adopted in aerospace cabin systems to mitigate pathogen transmission. Strategically, 3M is transitioning toward monodisperse formulation technologies, enabling faster evaporation and more uniform antimicrobial coverage on sensitive medical devices.

Reckitt Benckiser Group PLC expands alcohol disinfection into air sanitation and lifestyle hygiene

Reckitt Benckiser Group PLC commands global consumer trust through Lysol and Dettol, extending alcohol-based disinfection beyond surfaces into ambient environments. The launch of Lysol Air Sanitizer created a new category using alcohol mists to neutralize airborne pathogens. Reckitt is rapidly scaling Dettol across India and Southeast Asia, capturing demand from emerging middle-class households transitioning to branded hygiene. Sustainability is embedded via its Sustainable Innovation Calculator, targeting a 50% reduction in virgin plastic by 2030. The company is also repositioning alcohol wipes and sprays as everyday wellness tools for travelers and families.

SC Johnson Professional dominates institutional sanitation with virucidal foam systems

SC Johnson Professional specializes in the Away-from-Home segment, delivering high-volume alcohol disinfectants through tamper-proof dispensing infrastructure. Its InstantFOAM™ Complete range is the world’s first alcohol-based foam proven fully virucidal, bactericidal, and yeasticidal, making it a standard across education and hospitality. In 2025, SC Johnson upgraded European production to prioritize bio-ethanol sourcing, lowering carbon intensity. Its Targeted Hygiene methodology maps high-touch surfaces such as elevators and door handles, enabling facility managers to optimize sanitizer placement and maximize infection control efficiency.

Hartmann Group sets European benchmarks in surgical-grade alcohol disinfection

Hartmann Group, through its BODE Chemie division, remains Europe’s technical authority in clinical hand hygiene. Sterillium®, marking over 50 years in 2025, continues to define skin-friendly alcohol disinfection standards in hospitals worldwide. The company launched Mission: Infection Prevention in 2026, offering digitized consulting services to reduce healthcare-associated infections through protocol optimization. Complementary Bacillol® surface wipes are engineered for compatibility with sensitive medical electronics. Strategically, Hartmann is transitioning to PFAS-free and microplastic-free wipe substrates, aligning with stringent EU environmental mandates effective 2026.

United States Alcohol Based Disinfectant Market: Regulatory Tightening and High-Purity Demand Leadership

The United States continues to anchor global standards for alcohol-based disinfectants through regulatory modernization and high-purity manufacturing leadership. In 2025, the U.S. Food and Drug Administration implemented updated industrial production guidelines for alcohol-based hand sanitizers, introducing more stringent testing protocols for methanol and 1-propanol contamination. This shift has raised compliance thresholds and accelerated consolidation toward well-capitalized manufacturers with advanced analytical and quality control capabilities.

Beyond consumer hygiene, industrial demand is reshaping the U.S. market. By late 2025, domestic investment of approximately $0.64 billion positioned the country as the global leader in electronic-grade isopropyl alcohol, supporting semiconductor fabrication, precision optics, and cleanroom maintenance. Industry governance also strengthened when the American Cleaning Institute released a comprehensive framework in May 2025 for the selection and disposal of high-level disinfectants in commercial environments. On the supply side, producers such as ExxonMobil and Dow expanded sustainable chemistry platforms to develop bio-based IPA. Adoption is being reinforced by contactless innovation, with AI-enabled automated dispensers deployed across transport hubs, while the Centers for Disease Control and Prevention reaffirmed in 2025 that 60 to 95% alcohol concentration remains the benchmark for preventing healthcare-associated infections.

European Union Alcohol Based Disinfectant Market: Ethanol Classification Debate and Supply Localization Strategy

The European alcohol-based disinfectant market is entering a critical regulatory inflection point. In late 2025, the European Chemicals Agency convened a decisive session under the Biocidal Products Regulation to evaluate whether ethanol should be reclassified as a CMR Category 1A substance. Such a move would significantly alter authorization pathways for consumer and professional disinfectants, prompting manufacturers to prepare extensive dossiers ahead of the anticipated 2026 review cycle.

Industry response has been highly coordinated. The International Association for Soaps, Detergents and Maintenance Products launched the “Hands Up For Ethanol” campaign in 2025, positioning ethanol as the gold standard for medical disinfection and warning against unintended public health consequences of restrictive classification. At the national level, German specialists such as BODE Chemie expanded residue-free alcohol formulations for food processing and pharmaceutical facilities, where non-tainting performance is mandatory. From a resilience standpoint, the European Commission introduced a 2025 roadmap to localize biocidal-grade ethanol production using agricultural waste, reducing import dependency and strengthening pandemic preparedness across France and Germany.

India Alcohol Based Disinfectant Market: Export-Led Growth and Ethanol Ecosystem Integration

India is rapidly emerging as a competitive exporter in the alcohol-based disinfectant industry, supported by policy incentives and integration with the national biofuel ecosystem. In late 2025, the government launched the Market Access Support Intervention to enhance the global footprint of Indian-made disinfectants and specialty alcohol formulations, particularly across Africa, the Middle East, and Southeast Asia.

Domestic manufacturers are scaling pharma-grade offerings. Companies such as Himalaya Wellness and CavinKare expanded portable gel and spray sanitizer lines in 2025 to address on-the-go hygiene demand. Supply stabilization is being reinforced through biofuel synergies, as Praj Industries confirmed late-2025 trials for dual-use alcohol streams that serve both disinfectant and clean fuel markets under the Ethanol Blending Program. Quality governance also advanced when the Bureau of Indian Standards updated IS 15171 to align hand sanitizer efficacy metrics with global ISO benchmarks. Complementing this, Export Promotion Mission guidelines are enabling MSMEs to adopt high-precision distillation technologies for medical-grade isopropyl alcohol.

China Alcohol Based Disinfectant Market: Volume Scale, Semiconductor Demand, and Green Certification

China continues to dominate global supply by volume in alcohol-based disinfectants and industrial alcohols, while simultaneously tightening safety and environmental oversight. In late 2025, the State Administration for Market Regulation issued mandatory standards for disinfectant purity and safety, specifically targeting reductions in heavy metal residues across industrial alcohol production.

Capacity expansion remains a defining feature. China achieved record output levels for methyl and ethyl alcohol in 2025, reinforcing its role as a primary exporter to industrial cleaning, pharmaceutical, and surface disinfection markets. Demand composition is also evolving. Rapid expansion of domestic wafer fabrication facilities drove a 15% increase in demand for ultra-high-purity IPA used in semiconductor tool cleaning and precision electronics maintenance. Sustainability signaling is strengthening through policy, as the Ministry of Industry and Information Technology introduced a Green Disinfectant certification in 2025 to promote bio-fermented ethanol and lower-emission production routes.

Country-Level Positioning in the Alcohol-Based Disinfectant Industry

Alcohol-Based Disinfectant market County Level Snapshot

|

Country / Region

|

Strategic Focus Area

|

Market Implication

|

|

United States

|

Regulatory tightening, electronic-grade IPA

|

Premium compliance and industrial demand leadership

|

|

European Union

|

Ethanol classification debate, supply localization

|

High regulatory risk with resilience-driven restructuring

|

|

India

|

Export promotion, ethanol blending integration

|

Fast-growing low-cost manufacturing and export base

|

|

China

|

High-volume output, semiconductor pull, eco-labeling

|

Scale dominance with rising quality thresholds

|

Alcohol-Based Disinfectant Market Report Scope

Alcohol Based Disinfectant market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.8 Billion

|

|

Market Size (2034)

|

$5.6 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Product Type (Ethyl Alcohol, Isopropyl Alcohol, N Propyl Alcohol, Methyl Alcohol), By Usage Form (Liquid Formulations, Gels and Lotions, Aerosol and Trigger Sprays, Pre Moistened Wipes), By Application (Hand and Skin Sanitizers, Clinical Device Disinfection, Clinical Surface Disinfection, Industrial Surface Cleaning), By End User (Healthcare Facilities, Commercial Establishments, Industrial Users, Residential Consumers), By Distribution Channel (Business to Business Sales, Supermarkets and Hypermarkets, Pharmacy and Drug Stores, Online Retail)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Reckitt Benckiser Group, 3M Company, Ecolab, Procter and Gamble, Gojo Industries, Unilever, The Clorox Company, Paul Hartmann, Henkel, Himalaya Wellness Company, Steris, LyondellBasell Industries, ExxonMobil Chemical, Dow, Kimberly Clark Professional

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Alcohol Based Disinfectant Market Segmentation

By Product Type

- Ethyl Alcohol

- Isopropyl Alcohol

- N Propyl Alcohol

- Methyl Alcohol

By Usage Form

- Liquid Formulations

- Gels and Lotions

- Aerosol and Trigger Sprays

- Pre Moistened Wipes

By Application

- Hand and Skin Sanitizers

- Clinical Device Disinfection

- Clinical Surface Disinfection

- Industrial Surface Cleaning

By End User

- Healthcare Facilities

- Commercial Establishments

- Industrial Users

- Residential Consumers

By Distribution Channel

- Business to Business Sales

- Supermarkets and Hypermarkets

- Pharmacy and Drug Stores

- Online Retail

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Alcohol Based Disinfectant Industry

- Reckitt Benckiser Group

- 3M Company

- Ecolab

- Procter and Gamble

- Gojo Industries

- Unilever

- The Clorox Company

- Paul Hartmann

- Henkel

- Himalaya Wellness Company

- Steris

- LyondellBasell Industries

- ExxonMobil Chemical

- Dow

- Kimberly Clark Professional

*- List not Exhaustive