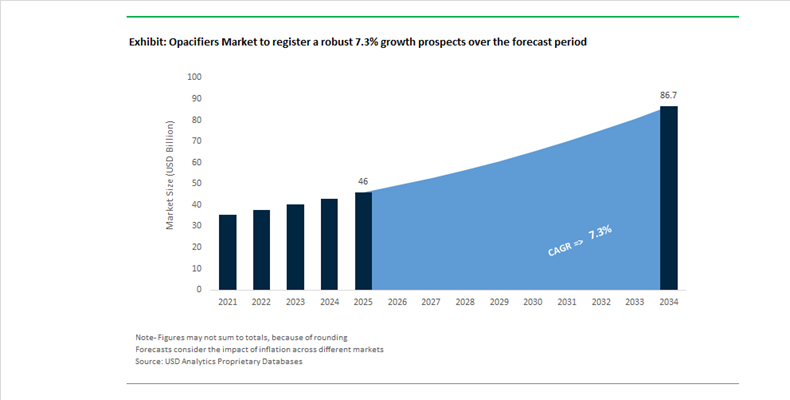

Opacifiers Market Valued at $46 Billion in 2025, Projected to Reach $86.7 Billion by 2034 at 7.3% CAGR Amid TiO₂ Rationalization and Sustainable Polymer Innovation

The Opacifiers Market is valued at $46 billion in 2025 and is forecast to reach $86.7 billion by 2034, expanding at a CAGR of 7.3%. Growth is anchored in strong demand across architectural coatings, plastics, packaging films, personal care formulations, and construction materials. Titanium dioxide (TiO₂) remains the dominant inorganic opacifier due to its high refractive index and brightness performance, yet the market is undergoing structural transformation driven by energy volatility in Europe, capacity rationalization in China, and regulatory pressure to reduce mineral intensity and PFAS-linked additives. Parallel innovation in opaque polymer dispersions and bio-based alternatives is reshaping the competitive landscape, particularly in paints and cosmetics.

In July 2024, Kronos Worldwide, Inc. completed the acquisition of Venator’s 50% stake in the Louisiana Pigment Company facility, securing full control of a strategic U.S. TiO₂ production asset. In June 2024, The Chemours Company resumed operations at its Altamira, Mexico TiO₂ plant after a climate-driven water disruption, prompting investment in water-resilient extraction technologies. September 2024 marked the launch of the CELLIGHT project by VTT Technical Research Centre of Finland, targeting cellulose-based opacifiers as sustainable alternatives to titanium dioxide in coatings and cosmetics. In October 2025, Venator Materials agreed to divest its UK TiO₂ facility to LB Group, followed in January 2026 by a definitive agreement to sell Venator Germany GmbH, including the Duisburg site, to International Chemical Investors Group. These moves reflect aggressive portfolio restructuring across Europe.

Capacity rationalization intensified in January 2026 when Tronox Holdings plc announced the permanent closure of its 46,000-metric-ton Fuzhou TiO₂ plant, citing sulfur feedstock cost escalation and persistent domestic oversupply. In contrast, Asia continues to attract strategic investments. In August 2025, Chemours formed a manufacturing alliance with SRF Limited to expand capacity in India, strengthening supply for architectural coatings and plastics without significant capital deployment. In February 2026, BASF SE added a new dispersion production line at its Mangalore site to support demand for polymer-based opacifiers in architectural paints and construction chemicals.

Sustainability-driven product innovation is accelerating. In April 2025, BASF launched Lamesoft® OP Plus, a wax-based, 95% renewable carbon opacifier engineered for rinse-off hair care products, offering biodegradability and conditioning benefits compared to acrylate-based systems. In September 2025, Dow Inc. introduced an alternative to fluoropolymer-based polymer processing aids, enabling PFAS-free opaque films for food and consumer packaging. In January 2026, Dow initiated its Transform to Outperform restructuring program to modernize specialty chemical operations, including opaque polymer technologies, leveraging AI-enabled supply optimization.

The opacifiers market is increasingly defined by TiO₂ supply consolidation, energy-sensitive European restructuring, Asia-Pacific capacity migration, and rapid development of bio-based and PFAS-free alternatives. Structural shifts in coatings, plastics compounding, and personal care formulation are driving higher-value, compliance-ready opacifier technologies across global value chains.

Opacifiers Market Trends and Opportunities

Trend: Strategic Shift Toward TiO₂ Optimization and Opaque Polymer Substitution

Despite the August 2025 ruling by the Court of Justice of the European Union annulling the carcinogenic classification of titanium dioxide, architectural and industrial coatings manufacturers are continuing to structurally reduce TiO₂ dependency. This trend is no longer driven by regulatory fear alone but by supply chain resilience, lifecycle carbon accounting, and customer-driven ESG procurement criteria. TiO₂ remains one of the most energy-intensive pigments to mine and process, exposing formulators to volatility in energy pricing and logistics.

A key industry milestone was highlighted in October 2025 when Dow demonstrated that its ROPAQUE™ opaque polymer technology, when combined with EVOQUE™ pre-composite polymers, enables up to a 25% reduction in TiO₂ loading in flat and semi-gloss coatings without compromising hiding power. Lifecycle assessments indicate that such formulations can lower greenhouse gas emissions by approximately 12% over a 60-year building lifespan, a metric increasingly scrutinized by commercial real estate developers and public infrastructure buyers.

This optimization trend is being reinforced through cross-industry collaboration. In September 2025, AkzoNobel, Arkema, and BASF announced a strategic partnership to reduce the carbon footprint of architectural powder coatings. Central to this initiative is the expanded use of alternative opacifying systems that deliver consistent whiteness and opacity with lower TiO₂ intensity. Even after the September 2025 ECHA update removed the inhalation carcinogen labeling requirement for powdered TiO₂, leading formulators have maintained low-TiO₂ R&D pipelines as a hedge against future REACH revisions and to strengthen their positioning with ESG-focused institutional clients.

Trend: Rising Demand for High-Refractive-Index Opacifiers in Micro-Electronics

The rapid miniaturization of electronic components is creating a structurally new demand profile for opacifiers. In micro-LED displays, advanced sensors, and wearable electronics, opacity must be achieved within ultra-thin layers where conventional silica-based systems underperform. As a result, zirconium oxide and zinc oxide nanoparticle opacifiers are gaining strategic importance due to their higher refractive indices and superior thermal stability.

By mid-2025, zirconium oxide nanoparticles were increasingly specified in semiconductor polishing slurries and optical encapsulants because they maintain a refractive index of approximately 2.1 even at reduced film thicknesses. This characteristic is critical for maximizing light out-coupling efficiency in next-generation smartphone and wearable displays, where brightness and power efficiency are tightly coupled. Parallel innovation is occurring in zinc oxide-based systems. Electronics industry data from 2025 shows that ZnO nanoparticle opacifiers used in flexible electronics and UV sensors deliver response times of 6 to 8 seconds, outperforming legacy mineral opacifiers while offering superior mechanical flexibility.

Miniaturization is also driving material science innovation. The transition toward one-dimensional nanostructures such as ZnO nanowires and nanorods for display backplanes has created niche demand for doped ZnO opacifiers. These materials allow precise tuning of optical and electrical properties, enabling high-opacity barriers in micro-circuitry without increasing dielectric thickness. For opacifier suppliers, this represents a shift from volume-driven coatings markets toward high-margin, specification-driven electronics applications.

Opportunity: Commercialization of Non-TiO₂ Clean-Label Food and Pharma Coatings

The sustained ban on E171 titanium dioxide in food applications across the European Union, alongside its temporary exemption in pharmaceuticals, has created a bifurcated but highly attractive opportunity landscape. Food manufacturers are under immediate pressure to replace TiO₂ in confectionery, chewing gum, and decorative coatings, while pharmaceutical producers are cautiously evaluating long-term alternatives under strict performance constraints.

In late 2025, Sensient Food Colors expanded its Avalanche™ portfolio to more than 40 clean-label white solutions based on starch and mineral hybrids. These systems are engineered to replicate TiO₂ opacity in panned confections while maintaining stability under acidic conditions and thermal stress. Their scalability signals that non-TiO₂ whiteners are moving from niche compliance tools to mainstream formulation components.

In contrast, the pharmaceutical supply chain remains highly sensitive. In August 2025, the European Medicines Agency reaffirmed that TiO₂ remains approved for medicinal products, citing the risk of shortages across more than 91,000 human medicines if it were removed. Existing alternatives often require significantly higher loadings, which can negatively affect tablet disintegration, dissolution, and coating integrity. This technical barrier creates a premium opportunity for chemical suppliers capable of delivering near one-to-one TiO₂ replacements that meet stringent pharmaceutical KPIs, where switching costs are high and supplier qualification cycles are long.

Opportunity: NIR-Reflective Opacifiers for Urban Heat Island Mitigation

Urban climate policy is unlocking a fast-growing application segment for opacifiers designed not only for visual whiteness but also for near-infrared reflectivity. Cool roof and cool façade mandates are being adopted globally as municipalities seek to reduce peak energy demand and mitigate urban heat island effects.

According to 2025 reports from the U.S. Environmental Protection Agency and the U.S. Department of Energy, roofs coated with IR-reflective opacifier systems can be up to 50°F cooler than conventional dark roofs. These coatings reflect roughly 50% of incoming infrared radiation, compared to around 5% for standard pigments, enabling reductions in building air-conditioning energy consumption of up to 25% .

Municipal programs such as NYC CoolRoofs and California Title 24 are accelerating adoption of white and reflective elastomeric coatings that rely on advanced opacifier chemistries. Beyond traditional white roofs, innovation is expanding into color-flexible systems. In May 2025, AkzoNobel introduced a new “sunscreen” coating platform using IR-reflective opacifiers that allow darker or more vibrant exterior colors without the traditional heat absorption penalty. This capability significantly broadens the addressable market by aligning architectural aesthetics with energy-efficiency mandates, positioning NIR-reflective opacifiers as a cornerstone technology in climate-resilient urban construction.

Opacifiers Market Share and Segmentation Insights

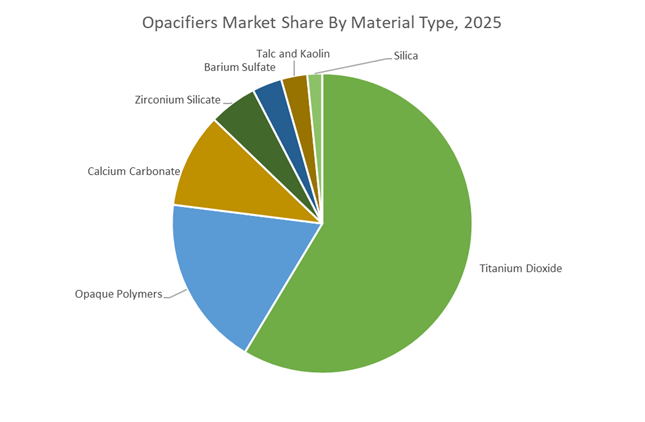

Titanium Dioxide Dominates Opacifier Material Demand Due to Superior Refractive Index and Light Scattering Performance

Titanium dioxide accounted for 58.60% of the Opacifiers Market by material type in 2025, maintaining its position as the most widely used white pigment across paints, plastics, and paper applications. The dominance of TiO₂ is attributed to its exceptionally high refractive index and superior light scattering capability, which deliver unmatched opacity, brightness, and whiteness in formulated products. These optical properties make titanium dioxide essential for achieving high hiding power in architectural coatings, industrial finishes, and polymer compounds. In 2025, market dynamics are shaped by TiO₂ optimization strategies, where formulators improve pigment dispersion, control particle size distribution, and integrate extender pigments or opaque polymers to reduce TiO₂ loading while preserving opacity performance in cost-sensitive formulations.

Paints and Coatings Segment Leads Global Opacifier Consumption Driven by High-Volume Architectural Coating Production

Paints and coatings represented 48.60% of the Opacifiers Market by application in 2025, making it the largest demand segment supported by the extensive global production of architectural paints, automotive coatings, and industrial protective finishes. Opacifiers play a critical role in coatings by providing hiding power, color development, and brightness required for both decorative and protective performance. Titanium dioxide remains the primary pigment used in these formulations due to its efficiency in light scattering and coverage. A major 2025 industry development is the emphasis on hiding power efficiency, where coating manufacturers optimize pigment volume concentration and incorporate opaque polymers that generate microvoid light scattering structures, enabling reduced titanium dioxide usage while maintaining coating durability and visual quality.

Opacifiers Market Competitive Landscape

The opacifiers market in 2026 is driven by polymer-based alternatives to titanium dioxide, emphasizing high hiding power, digital color calibration, and bio-based formulations. Competitive differentiation centers on cost-efficient opaque polymers, regulatory compliance, and biodegradable opacifiers for personal care, coatings, and high-performance packaging applications.

Ashland accelerates biodegradable polymer opacifiers through network optimization and specialty portfolio focus

Ashland is strengthening its position in high-performance opacifiers by aligning its “Execute and Globalize” strategy with manufacturing consolidation and specialty chemical focus. The $60 million network optimization program, including the Parlin facility closure, enhances production efficiency across global hubs. Its partnership with IMCD improves distribution reach for personal care opacifiers in the U.S. With Q1 FY2026 sales at $386 million, Ashland is reinvesting into high-purity excipients and functional additives. The agrimer™ eco-coat platform introduces biodegradable polymer opacifiers addressing clean-label and microplastic-free demand. This transition positions Ashland as a key innovator in sustainable, high-opacity polymer systems.

Dow scales opaque polymer innovation with circular materials and bio-based opacity solutions

Dow is leveraging its global scale and material science leadership to advance polymer-based opacifiers as cost-stable alternatives to TiO₂. Its DEXCARE™ CD-2 polymer enhances opacity and sensory performance in premium personal care formulations, supporting bio-based product demand. Innovation recognition through multiple BIG Awards highlights Dow’s leadership in sustainable opacity solutions, including TRITON™ FCX surfactants. Circular economy initiatives such as REVOLOOP™ resins enable high-opacity packaging with recycled content while maintaining UV resistance. With $43 billion in sales and operations across 31 countries, Dow drives cost optimization and supply stability. This integration strengthens its dominance in high-performance opacifier technologies.

Arkema expands specialty materials capacity to deliver advanced opacified polyamide solutions

Arkema is capitalizing on specialty materials growth by expanding high-performance polymer capacity, including its Singapore facility that supports both transparent and opacified grades. With €1,251 million EBITDA in 2025 and a 15.7% margin in Specialty Materials, the company demonstrates strong financial resilience. Its Rilsan® platform enables advanced applications in electronics, AR/VR devices, and healthcare, where optical control and durability are critical. Strategic segmentation enhances visibility into performance-driven product lines. Arkema’s €600 million CAPEX plan for 2026 supports low-carbon, high-value polymer innovation. This positions the company as a leader in next-generation opacifier materials.

Croda strengthens premium opacifier portfolio through NPP innovation and regional application expansion

Croda is advancing its opacifiers portfolio through its “Smart Science” model, focusing on high-margin, bio-based and high-purity ingredients. NPP sales growth of 5% and a 10% increase in new ingredients reflect strong innovation momentum. Expansion of application labs in Asia and the U.S. accelerates regional product customization and specification wins. Pharmaceutical lipid capacity expansion supports advanced formulations requiring controlled opacity and light sensitivity. With £28 million in transformation benefits and rising operating margins, Croda is enhancing profitability. This innovation-driven approach positions Croda strongly in premium personal care and pharma opacifier markets.

Intertek enables regulatory compliance and digital traceability for next-generation opacifier formulations

Intertek plays a critical role in the opacifiers market by providing advanced testing, certification, and regulatory compliance services. With record 2025 revenue of £3,431.6 million, the company supports global manufacturers navigating EPA and EU chemical safety regulations. Its Digital Product Passport service enhances transparency in chemical composition and environmental impact, aligning with sustainability mandates. Strategic acquisitions, including QTEST and AePVI, expand its global certification capabilities. The Melbourn facility strengthens pharmaceutical testing for opacity stability in complex formulations. Intertek’s Total Quality Assurance model ensures compliance, performance validation, and market access for advanced opacifier technologies.

China – Capacity Scale, Pricing Discipline, and Structural Consolidation

China remains the undisputed anchor of the global opacifiers industry, underpinned by unmatched titanium dioxide production capacity and active policy intervention. During 2024–2025, China’s TiO2 capacity reached approximately 5.96 million tons, accounting for more than half of global installed capacity, reinforcing its role as the primary source of opacifiers for paints, coatings, plastics, and paper applications worldwide. Pricing strategy has become increasingly coordinated. In October 2025, leading producers such as Lomon Billions, CNNC HuaYuan, and Bluestar Chemical initiated a synchronized export price increase to offset sustained inflation in sulfuric acid and titanium concentrate costs. This pricing offensive signaled stronger discipline across the Chinese opacifier supply base.

Technological restructuring is accelerating in parallel. Central government mandates for 2025–2026 are actively pushing the industry away from sulfate-process production toward chloride-process technology, improving pigment quality while reducing emissions intensity. Environmental enforcement remains stringent. In late 2025, the Ministry of Ecology and Environment imposed temporary production halts in high-density TiO2 regions such as Panzhihua, affecting nearly one-fifth of domestic output and tightening short-term supply. Despite trade headwinds, export resilience has been notable. The removal of Indian anti-dumping duties and seasonal overseas stocking enabled Chinese exports to surge in late 2024, even as EU trade barriers persisted. Structurally, Beijing is encouraging mergers and reorganizations among smaller producers to enhance global pricing power, resource efficiency, and long-term competitiveness.

European Union (Germany & France) – Regulatory Reset and Capacity Rationalization

The European opacifiers market entered a pivotal phase in 2025 following a decisive regulatory reversal. On September 11, 2025, the European Chemicals Agency formally removed the inhalation carcinogen classification for titanium dioxide, following a final ruling by the Court of Justice of the European Union. This outcome eliminated mandatory hazard labeling requirements across safety data sheets and export packaging, materially reducing compliance friction for opacifier suppliers operating in Germany and France. The ruling restored confidence among downstream users in paints, plastics, and paper, particularly for export-oriented formulations.

However, regulatory relief has coincided with capacity contraction. Venator Materials permanently suspended its 60,000-ton-per-year Asia Sdn. Bhd. unit in September 2025, following liquidity-driven shutdowns in Germany. Energy cost volatility remains a structural constraint. Earlier in 2025, Venator implemented a substantial EMEA-wide price increase to counter escalating natural gas prices and carbon certificate costs. At the policy level, Germany’s phased corporate tax reduction program, lowering rates annually through 2032, is reshaping deferred tax positions for producers such as Kronos Worldwide. Strategically, EU manufacturers are redirecting R&D toward opaque polymers and bio-based opacifiers, aligning with European Green Deal targets and reducing long-term dependence on traditional mineral pigments.

United States – Supply Security and Downstream Application Diversification

The U.S. opacifiers industry is increasingly characterized by upstream integration and downstream diversification. In December 2024, The Chemours Company announced a strategic partnership with PCC Group to develop a chlor-alkali facility at its DeLisle site, securing chlorine feedstock for its large-scale titanium dioxide operations. This move directly addresses raw material risk and enhances long-term production stability. Market consolidation has further strengthened domestic supply. Kronos Worldwide completed full ownership of the Louisiana Pigment Company in mid-2024, expanding its North American capacity base.

Pricing actions reflect tight supply-demand balances. Chemours implemented global price increases effective December 2025, with differentiated hikes across plastics and coatings grades, signaling firm demand fundamentals. Beyond traditional opacification, U.S. players are leveraging chemical expertise into adjacent applications. Chemours’ successful qualification of advanced immersion cooling fluids with Samsung Electronics in late 2025 highlights cross-sector innovation potential. On the policy front, selective tariff exemptions introduced in 2025 stabilized domestic paints and coatings supply chains, mitigating volatility stemming from global pigment pricing disruptions.

India – Demand Expansion and Raw Material Leverage

India’s opacifiers market is transitioning from import dependence toward strategic balance between trade liberalization and domestic resource utilization. In late 2024, the government revoked anti-dumping duties on Chinese titanium dioxide, significantly reducing input costs for ceramics, coatings, and plastics manufacturers. Demand momentum remains strong, led by the paints and coatings sector, which dominates domestic TiO2 consumption. Long-term growth expectations are anchored in sustained urbanization, infrastructure spending, and housing demand.

Strategic partnerships are reinforcing localization efforts. In late 2025, The Chemours Company entered into a collaboration with SRF Limited to support localized chemical manufacturing and application development. India’s natural resource base provides a structural advantage. Large ilmenite and rutile reserves across Tamil Nadu, Andhra Pradesh, and Kerala continue to support domestic pigment value chains. Beyond coatings, integration into aerospace-grade titanium supply is emerging, supported by collaborations between industrial gas specialists such as Messer and Indian titanium producers.

Saudi Arabia – Vision 2030 and Regional Supply Hub Ambitions

Saudi Arabia is positioning itself as a strategically advantaged opacifiers production and distribution hub for the Middle East. National Titanium Dioxide Company, operating under Tronox, completed major efficiency upgrades at its Yanbu facility to align with rising construction demand driven by Saudi Vision 2030 megaprojects. These upgrades enhance operational efficiency and cost competitiveness, particularly in energy-intensive TiO2 processing.

The country’s geographic location and access to competitively priced energy resources provide a structural cost advantage over European producers. Saudi Arabia is increasingly marketing itself as a regional distribution hub, serving construction, coatings, and plastics markets across the Gulf Cooperation Council and wider MENA region. This positioning supports supply chain resilience for downstream users while diversifying the global opacifiers trade away from traditional production centers.

Strategic Country Comparison – Opacifiers Industry

Opacifiers Market County Level Snapshot

|

Country / Region

|

Core Structural Driver

|

Strategic Focus Area

|

Competitive Position

|

|

China

|

Capacity scale and policy coordination

|

Chloride technology, consolidation

|

Global price and volume leader

|

|

EU (Germany & France)

|

Regulatory reset and energy costs

|

Sustainable opacifiers, polymers

|

High-value, compliance-driven market

|

|

United States

|

Supply security and innovation

|

Integrated feedstocks, new applications

|

Stable premium-grade producer

|

|

India

|

Demand growth and trade reform

|

Coatings-driven consumption

|

Fast-expanding downstream market

|

|

Saudi Arabia

|

Vision 2030 infrastructure push

|

Energy-efficient TiO2 production

|

Emerging regional supply hub

|

Opacifiers Market Report Scope

Opacifiers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$46 Billion

|

|

Market Size (2034)

|

$86.7 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Material Type (Titanium Dioxide, Zirconium Silicate, Opaque Polymers, Barium Sulfate, Calcium Carbonate, Silica, Talc and Kaolin), By Application (Paints and Coatings, Plastics, Ceramics, Paper and Inks, Personal Care, Aerospace and High-Temperature Applications), By Form (Powder, Dispersion or Slurry, Masterbatch)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Chemours, Tronox, LB Group, Kronos Worldwide, Venator Materials, Ishihara Sangyo Kaisha, DIC, Altana, Cristal, Shepherd Color, Omya, Cinkarna Celje, Tayca, Arkema, Precheza

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Opacifiers Market Segmentation

By Material Type

- Titanium Dioxide

- Zirconium Silicate

- Opaque Polymers

- Barium Sulfate

- Calcium Carbonate

- Silica

- Talc and Kaolin

By Application

- Paints and Coatings

- Plastics

- Ceramics

- Paper and Inks

- Personal Care

- Aerospace and High-Temperature Applications

By Form

- Powder

- Dispersion or Slurry

- Masterbatch

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Opacifiers Industry

- Chemours

- Tronox

- LB Group

- Kronos Worldwide

- Venator Materials

- Ishihara Sangyo Kaisha

- DIC

- Altana

- Cristal

- Shepherd Color

- Omya

- Cinkarna Celje

- Tayca

- Arkema

- Precheza

*- List not Exhaustive