Thermal-Responsive Materials and Heat-Management Technologies Driving Steady Growth

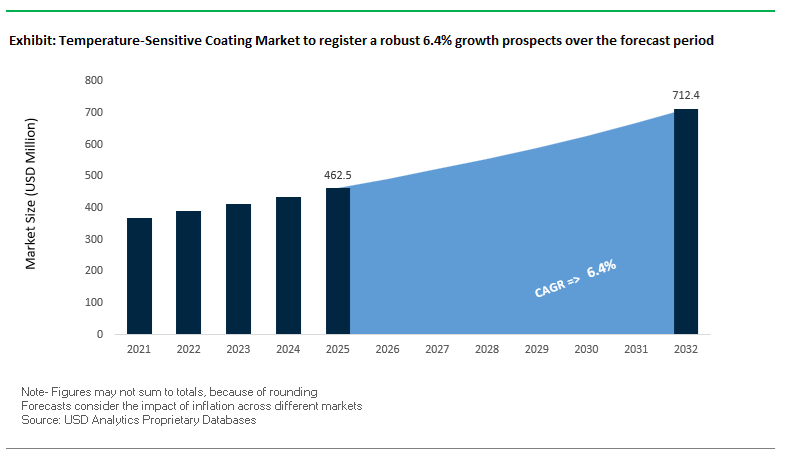

The global Temperature Sensitive Coating Market is gaining traction as industries increasingly demand thermal-responsive, heat-resistant, and energy-efficient coating systems across automotive, construction, energy, and industrial applications. The market was valued at $462.5 million in 2025 and is projected to reach $714 million by 2032, expanding at a CAGR of 6.4% during 2025–2032. This growth is driven by the rising need for coatings that can adapt to temperature variations, provide thermal protection, and maintain performance under extreme environmental conditions.

A key structural driver is the growing adoption of heat-management coatings, particularly in electric vehicles (EVs), industrial equipment, and infrastructure. These coatings are engineered to reflect, absorb, or dissipate heat, protecting sensitive components such as batteries, sensors, and pipelines. In EVs and autonomous systems, temperature-sensitive coatings play a critical role in ensuring sensor accuracy, battery efficiency, and system reliability, especially under fluctuating thermal conditions.

Another major growth factor is the increasing use of thermal-indicating and responsive coatings, which can change color, reflectivity, or physical properties in response to temperature shifts. These coatings are widely used in industrial safety, corrosion monitoring, and quality control processes, enabling real-time visualization of thermal exposure and potential failure points. Additionally, the rise of energy-efficient buildings and infrastructure is driving demand for coatings that contribute to thermal insulation, solar reflectance, and reduced energy consumption.

The market is also benefiting from advancements in polyaspartic, silicone, and hybrid coating technologies, which offer improved performance across a wide temperature range. These materials enable coatings to maintain adhesion, flexibility, and durability even under extreme heat or cold conditions. At the same time, sustainability trends are pushing the development of low-VOC, energy-efficient curing systems, aligning temperature-sensitive coatings with global environmental regulations.

Market Analysis: Thermal Monitoring Systems, All-Weather Polyaspartics, and Energy-Sector Applications Driving Competitive Innovation

The temperature-sensitive coatings market is evolving through innovation in thermal monitoring, advanced material systems, and strategic industry initiatives, reflecting the increasing importance of heat-responsive technologies in modern applications. In March 2026, AkzoNobel introduced its IONOMY™ ecosystem, which integrates temperature-sensitive formulations capable of monitoring real-time thermal profiles during coil coating processes. This innovation enhances energy efficiency and process control, particularly in high-speed industrial coating lines.

Material innovation is also advancing in automotive and industrial coatings. Sun Chemical’s February 2026 showcase at ABRAFATI highlighted temperature-stable pigments and resins designed to maintain consistent color performance across wide thermal variations, addressing the growing need for aesthetic stability in automotive basecoats.

In the energy and infrastructure sectors, thermal-barrier coatings are becoming increasingly critical. Hempel’s “Accelerate to Win” strategy (January 2026) emphasizes the expansion of heat-reflective and thermal-insulative coatings aimed at extending asset lifetimes and reducing energy consumption.

The automotive sector continues to drive innovation in heat-management technologies. Axalta’s 2026 “A Plan” execution prioritizes coatings with infrared-reflective and thermal regulation capabilities, essential for protecting EV battery systems and advanced sensors.

High-performance industrial coatings are also evolving to address extreme conditions. Sherwin-Williams’ Heat-Flex® AEB, recognized with multiple industry awards in November 2025, provides a thermal barrier and corrosion protection solution capable of withstanding the extreme cycles of industrial autoclaves. Complementing this, its Acrolon 680 (August 2025) delivers all-weather application performance, maintaining curing stability in high-temperature and high-humidity environments.

Sustainability-focused innovation is further shaping the market. Sun Chemical’s September 2025 launch of VOC-free polyaspartic systems enables fast curing even at low temperatures, supporting green building initiatives and reducing energy consumption during application.

Marine and industrial applications are also benefiting from temperature-stable coatings. The launch of Hempaguard NB (January 2025) demonstrates the use of silicone-based technologies that maintain consistent performance across varying sea temperatures, ensuring durability and efficiency in marine environments.

Additionally, advancements in functional aesthetics are bridging decorative and performance applications. AkzoNobel’s “Colors of the Year 2026” initiative introduces pigments that change tone based on thermal and UV exposure, reflecting a growing trend toward coatings that combine visual impact with functional responsiveness.

Market Trend: FAA and EASA Certification Requirements Elevate Temperature-Sensitive Coatings to Critical Validation Tools in Turbine Testing

Temperature-sensitive coatings are transitioning from auxiliary diagnostics to mission-critical validation tools as aviation regulators tighten certification protocols for next-generation engines. Under 14 CFR Part 33 and aligned European requirements, thermal paints are now integral to verifying life-prediction models of turbine hot-section components. In 2026 certification workflows, coatings must deliver measurement precision within ±5°C at temperatures exceeding 900°C, ensuring accurate mapping of thermal gradients across turbine blades and vanes. This level of accuracy is essential to mitigate risks such as creep deformation and premature material fatigue in high-stress environments. Additionally, irreversible thermochromic coatings are gaining preference over traditional infrared-based measurement systems for Full Authority Digital Engine Control validation. These coatings provide continuous, surface-wide thermal mapping that is not affected by optical distortions caused by high-velocity exhaust flows, a limitation commonly observed in IR sensing due to refractive “shimmering” effects. As aerospace propulsion systems evolve toward higher efficiency and temperature thresholds, temperature-sensitive coatings are becoming indispensable in certification-grade testing and validation processes.

Market Trend: ISO 23478-2024 Standard Drives Quantitative Adoption of Thermochromic Coatings in Industrial Applications

The implementation of ISO 23478-2024 is establishing a unified global framework for the evaluation and deployment of thermochromic coatings across industrial sectors. This standard marks a shift from qualitative color-change observation toward quantitative, data-driven thermal monitoring systems. Under the new guidelines, coatings must demonstrate consistent color-change accuracy after exposure to at least 5,000 thermal cycles or 2,000 hours of ultraviolet radiation, setting a high durability threshold for outdoor and high-temperature applications. This requirement is accelerating the replacement of traditional organic leuco dye systems, which are prone to degradation, with more stable inorganic pigment technologies capable of maintaining performance under prolonged environmental stress. Furthermore, ISO 23478-2024 formalizes the use of AI-assisted colorimetry, specifically Delta E measurement systems, to interpret color transitions with high precision. This approach reduces human interpretation errors by approximately 30% compared to manual inspection methods, enabling more reliable and repeatable thermal diagnostics. As industries increasingly adopt digital inspection frameworks and predictive maintenance strategies, standardized thermochromic coatings are emerging as a key enabler of accurate and scalable thermal monitoring.

Market Opportunity: Reversible Thermochromic Coatings Enable Real-Time Thermal Monitoring in Advanced EV Battery Systems

The rapid evolution of electric vehicle battery technologies, particularly high-nickel and solid-state chemistries, is creating a strong demand for advanced thermal monitoring solutions at the cell level. Reversible thermochromic coatings are emerging as a viable solution by providing continuous, surface-level temperature visualization integrated with onboard imaging systems. These coatings can trigger visible color changes at critical thresholds between 60°C and 70°C, offering early warning signals for potential thermal runaway events. Compared to conventional thermistors, which provide point-based measurements and may lag during rapid temperature spikes, coating-based systems deliver a lead time advantage of 10 to 15 seconds. This early detection capability is crucial for battery management systems aiming to prevent catastrophic failures. Additionally, the full-surface coverage provided by thermochromic coatings enables high spatial resolution, allowing detection of localized hot spots as small as 2 millimeters that may indicate internal defects such as short circuits or electrolyte leakage. As electric mobility scales globally and safety standards become more stringent, reversible thermochromic coatings are positioned as a critical innovation in next-generation battery monitoring systems.

Market Opportunity: High-Temperature Irreversible Coatings Expand Applications in Gas Turbine Diagnostics and Forensic Engineering

Irreversible temperature-sensitive coatings designed for extreme environments are unlocking new opportunities in gas turbine diagnostics and aerospace engineering. These coatings are engineered to permanently record peak temperatures experienced during operation, providing valuable post-test data for performance validation and failure analysis. Advanced formulations introduced in 2026 utilize rare-earth doped phosphor systems capable of accurately mapping temperatures up to 1,400°C, enabling detailed assessment of thermal distribution in high-pressure turbine components. This capability is particularly important for evaluating the effectiveness of cooling technologies such as film cooling holes, which are critical for maintaining structural integrity under extreme thermal loads. Modern coatings are also designed with multiple color transition stages, allowing a single application to capture a comprehensive thermal profile across a wide temperature range, typically in increments of 200°C. This multistage mapping enhances diagnostic resolution and reduces the need for multiple test cycles. Additionally, these coatings exhibit strong adhesion under extreme mechanical stress, withstanding centrifugal forces of up to 20,000 Gs during high-speed engine operation. As the demand for high-efficiency turbines and advanced propulsion systems grows, irreversible temperature-sensitive coatings are becoming an essential tool for both real-time validation and post-operational forensic analysis.

Temperature-Sensitive Coatings Market Share and Segmentation Insights: Thermochromic Technologies and Smart Packaging Driving Industry Leadership

By Product Type: Thermochromic Coatings Command 45.7% Share with Strong Adoption in Smart Packaging and Cold Chain Monitoring

Thermochromic coatings led the temperature-sensitive coatings market in 2025 with a 45.7% share, driven by their reversible color-change functionality and low activation temperature range of 15°C to 40°C. These coatings are widely adopted in smart packaging applications across food, beverage, and pharmaceutical sectors, where visual temperature indicators are critical for product safety and quality assurance. The integration of thermochromic coatings with IoT-enabled printed sensors and QR codes is further accelerating adoption, enabling real-time temperature tracking in cold chain logistics. This is particularly vital for vaccines and perishable goods, positioning thermochromic coatings as a key technology in intelligent packaging and advanced temperature monitoring systems.

By End-User Industry: Packaging Sector Leads with 31.3% Share Supported by Smart Labeling and Regulatory-Driven Cold Chain Compliance

The packaging industry accounted for 31.3% of the temperature-sensitive coatings market share in 2025, emerging as the dominant end-use segment due to rising demand for smart and functional packaging solutions. Over 50% of this segment’s demand is driven by temperature-indicating coatings used in food safety and pharmaceutical packaging, where color-change mechanisms provide immediate visual alerts for temperature excursions. Additionally, stringent regulatory frameworks enforced by agencies such as U.S. Food and Drug Administration and EU Good Distribution Practice (GDP) guidelines are mandating temperature monitoring for biologics, insulin, and other sensitive drugs. This regulatory push is accelerating the adoption of thermochromic and irreversible coatings, reinforcing packaging as a high-growth segment in the global temperature-sensitive coatings market.

Competitive Landscape Analysis of the Temperature Sensitive Coating Market

AkzoNobel Driving Sustainable Low-Cure Powder Coatings Innovation

AkzoNobel N.V. continues to lead the temperature sensitive coating market through strategic innovation and sustainability initiatives. In 2026, the company partnered with IPG Photonics to introduce laser-based curing technology, significantly reducing energy consumption for thermal-responsive coatings. Its €50 million investment in the Waukegan aerospace coatings facility enhances production capacity for high-spec heat-sensitive coatings. AkzoNobel’s flagship Interpon D low-cure powder coatings now incorporate bio-attributed raw materials, reducing carbon footprint in architectural applications. With a strong global presence in powder coatings and its proprietary Calosol heat-absorbing technology, the company is transforming building façades into energy-generating assets, reinforcing its leadership in energy-efficient coating solutions.

PPG Industries Advancing Low-Bake and Corrosion-Resistant Coating Technologies

PPG Industries, Inc. is strengthening its position in the temperature sensitive coatings market through continuous innovation in low-temperature curing coatings and corrosion resistance technologies. In 2026, the company introduced advanced low-bake powder coatings for wood and heat-sensitive substrates, ensuring durability without high-temperature curing. It also set a new benchmark in metal edge corrosion resistance, targeting vulnerabilities in industrial equipment like heat exchangers and storage tanks. PPG’s investment in zinc-rich primers addresses thermal shock challenges in oil & gas infrastructure. Additionally, its AI-driven digital color-matching systems enhance thermochromic monitoring, positioning PPG as a leader in smart industrial coatings and predictive performance solutions.

Sherwin-Williams Leading High-Temperature and Smart Coatings Segment

Sherwin-Williams Company dominates the high-temperature powder coatings segment, particularly for applications exceeding 500°C, including aerospace engines and industrial incinerators. Its expanding smart coatings portfolio leverages nanotechnology to provide anti-corrosion protection and visual thermal indicators, addressing critical industrial safety needs. With a strong distribution network, the company maintains leadership in North America’s MRO coatings market, ensuring rapid supply and service efficiency. Sherwin-Williams also targets automotive and fireplace applications, where coatings must retain color integrity under continuous exposure to 400°C+. This strategic focus on high-performance heat-resistant coatings strengthens its competitive edge in demanding industrial environments.

Axalta Accelerating EV-Focused Thermal Management Coatings

Axalta Coating Systems is rapidly evolving within the temperature sensitive coating market by aligning with the global shift toward electric mobility. In 2026, the company leveraged SAP S/4HANA to optimize logistics for temperature-sensitive coating products, enhancing supply chain efficiency. Its innovation in electric motor coatings focuses on thermal conductivity and heat dissipation, supporting high-performance EV components. Financial results from Q1 2026 highlight strong growth in industrial and refinish coatings, driven by sustainable, low-VOC formulations. With over 150 years of expertise in corrosion prevention, Axalta is transitioning toward intelligent coating solutions that integrate structural health monitoring with advanced thermal management capabilities.

Jotun Innovating Smart Fireproof and Heat-Responsive Coating Systems

Jotun A/S is advancing the temperature sensitive coatings market through next-generation smart coatings and fireproofing technologies. In 2026, the company launched intelligent coatings capable of signaling surface degradation through precise thermochromic color changes, enhancing maintenance efficiency. Its expertise in intumescent fireproof coatings has improved safety margins by enabling faster expansion with thinner application layers. Jotun is expanding its presence in the Middle East and Asia-Pacific, particularly through its Dubai hub, to meet demand for extreme heat-resistant coatings in petrochemical and desalination sectors. Its flagship Jotatherm systems, now integrated with micro-sensor technologies, provide real-time asset protection, reinforcing its position in advanced thermal insulation coatings.

Germany’s Leadership in Smart Thermotropic Coatings and Industrial Precision Applications

Germany continues to dominate the temperature sensitive coating market in Europe through its strong foundation in precision engineering and advanced material science. The country is actively advancing thermotropic and thermoresistive sol-gel technologies, particularly for high-durability industrial coatings and automotive applications. A significant breakthrough emerged in early 2026 when the Fraunhofer Institute commercialized a low-temperature curing thermoresistive coating, enabling real-time thermal monitoring for lightweight composite aircraft components—an innovation that strengthens Germany’s aerospace manufacturing ecosystem.

Product innovation is accelerating with the introduction of nanostructured reversible thermochromic coatings for optical lenses, enhancing sensor protection through dynamic opacity control. Infrastructure modernization is also a major growth driver, as Deutsche Bahn mandates temperature-sensitive safety coatings for high-speed rail axle bearings to provide visual overheating alerts. Germany’s regulatory landscape is shifting toward REACH-compliant, water-based thermochromic coatings, reinforcing sustainability goals. Additionally, the adoption of thermochromic smart glass in commercial buildings is improving energy efficiency by optimizing Solar Heat Gain Coefficient (SHGC). Strategic investments, including a €45 million federal grant led by BASF, are further boosting the development of smart sol-gel coatings with embedded thermal indicators.

China’s Mass Production Ecosystem for Smart City and Energy Applications

China is rapidly transforming into a global powerhouse in the temperature sensitive coatings market, shifting from decorative pigments to functional thin-film coatings for semiconductors, energy, and infrastructure. Under the “New Material Industry Development Plan (2025–2026),” thermochromic coatings are classified as critical technologies, unlocking tax incentives and accelerating domestic production capabilities.

The country is witnessing large-scale deployment of titania-based photocatalytic thermotropic coatings on high-rise buildings in Shanghai, combining thermal regulation with air purification. Industrial expansion is evident with a $400 million manufacturing facility established in 2026 to meet rising demand for temperature-sensitive pharmaceutical labels, strengthening China’s cold-chain logistics sector. Technological advancements include the integration of graphene oxide in thermoresistive coatings, enabling ultra-sensitive thermal mapping for flexible electronics.

China’s energy infrastructure is also leveraging irreversible temperature-sensitive paints for transformer monitoring, ensuring grid reliability. The nation has achieved a production peak in high-purity thermochromic pigments, positioning itself as the leading global supplier for textile and packaging industries.

United States Driving Aerospace Innovation and Sustainable Coating Technologies

The United States temperature sensitive coating market is evolving through a combination of aerospace innovation, defense applications, and environmental regulation. The 2026 EPA phase-out of PFAS chemicals has accelerated the adoption of fluorine-free thermochromic coatings, particularly in consumer cookware and industrial applications.

A key innovation includes the commercialization of self-healing thermoresistive coatings that use micro-encapsulation technology to repair aircraft fuselage cracks triggered by friction-induced heat. Infrastructure initiatives led by the Department of Energy have also expanded the use of thermochromic “cool roof” coatings across government buildings, significantly reducing HVAC energy consumption.

Major investments from PPG and Sherwin-Williams into dry-sol coating technologies are reducing environmental impact while improving performance efficiency. The U.S. also leads in temperature-sensitive labeling for military logistics, ensuring thermal stability of sensitive materials during transport. Additionally, innovations such as radiation-resistant thermochromic coatings for small modular reactors (SMRs) highlight the country’s leadership in next-generation energy systems.

Japan’s Nano-Precision and Medical-Grade Temperature Sensitive Coatings

Japan remains at the forefront of nano-scale temperature sensitive coating technologies, particularly for electronics and medical applications. Companies like Shin-Etsu have pioneered ultra-thin thermoresistive dielectric layers (10nm) for high-density MLCCs, enhancing performance in compact electronic devices.

The automotive sector is adopting thermochromic glass-ceramic coatings for EV battery enclosures, offering both fire resistance and real-time visual diagnostics of battery health. Government support through the “Nanotech 2026 Strategy” is driving innovation in biocompatible thermochromic coatings for orthopedic implants, enabling monitoring of localized inflammation.

Japan is also advancing anti-fogging thermotropic films for medical endoscopy, improving procedural clarity. Industrial expansion includes Nippon Paint’s clean-room facility dedicated to semiconductor coatings that indicate wafer temperature. In the consumer segment, thermochromic smart appliance coatings are gaining traction, enhancing safety through “safe-to-touch” indicators.

India’s Rapid Growth Driven by Infrastructure and Cold Chain Expansion

India is emerging as a high-growth market in the temperature sensitive coating industry, fueled by urbanization, infrastructure modernization, and pharmaceutical exports. The National Highways Authority of India (NHAI) is piloting thermochromic road markings in mountainous regions to alert drivers of hazardous conditions such as black ice.

Industrial expansion is supported by Tata Chemicals’ increase in precursor production capacity, enabling domestic manufacturing of temperature-sensitive pharmaceutical labels. Under the “Viksit Bharat 2026” initiative, smart specialty coatings have been prioritized, attracting significant private investments into thermochromic R&D.

Innovations include low-cost thermochromic water purification systems that indicate pasteurization through color change, addressing rural water safety challenges. Indian Railways is deploying temperature-indicating primers in station redevelopment projects to monitor structural stress. Additionally, advancements in spray-pyrolysis manufacturing are boosting the production of thermochromic architectural glass, improving energy-efficient building solutions.

South Korea’s Dominance in Optoelectronic and Display Coating Technologies

South Korea is a global leader in optically active temperature sensitive coatings, particularly for OLED, micro-LED, and semiconductor applications. Samsung Display has introduced thermochromic moisture barrier coatings that visually indicate encapsulation failure in OLED panels, improving device reliability.

Technological breakthroughs include high-refractive index thermochromic materials that enhance light extraction efficiency in advanced display technologies. Strategic collaborations led by Hyundai Motor Group are driving the development of self-cleaning thermotropic coatings for autonomous vehicle sensors, ensuring performance in extreme weather conditions.

Regulatory updates under K-REACH are accelerating the transition to eco-friendly water-based thermochromic coatings, aligning with sustainability goals. LG Chem’s expansion in electronic-grade silane production is strengthening vertical integration within the coating supply chain. South Korea also dominates the anti-static thermoresistive coatings market for semiconductor clean-room environments, ensuring precision and thermal stability in fabrication processes.

Temperature-Sensitive Coating Market Report Scope

Temperature-Sensitive Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$462.5 Million

|

|

Market Size (2032)

|

$714 Million

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Product Type (Reversible Coatings, Irreversible Coatings, Thermochromic Coatings, Thermotropic Coatings, Thermoluminescent Coatings, Thermoresistive), By Material Chemistry (Liquid Crystals, Leuco Dyes, Inorganic Pigments, Polymer Matrices, Specialized Materials), By Technology (Water-based Systems, Solvent-based Systems, Powder-based Systems, Microencapsulation, Sol-Gel Technology, Printable Inks), By Substrate (Metals, Plastics, Paper and Cardboard, Glass and Ceramics, Textiles), By End-User Industry (Packaging, Industrial and Manufacturing, Aerospace and Defense, Automotive, Consumer Goods and Household, Healthcare and Medical Devices, Energy and Power), By Sales Channel (Direct Sales, Specialized Industrial Distributors, Research and Development Procurement, E-commerce)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries, Inc., Akzo Nobel N.V., The Sherwin-Williams Company, BASF SE, Chromatic Technologies Inc., LCR Hallcrest, Inc., OliKrom, SpotSee, Matsui Shikiso Chemical Co., Ltd., 3M Company, Axalta Coating Systems Ltd., Indestructible Paint Limited, Innovative Scientific Solutions, Inc., Kansai Paint Co., Ltd., Rolls-Royce plc

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Temperature Sensitive Coating Market Segmentation

By Product Type

- Reversible Coatings

- Irreversible Coatings

- Thermochromic Coatings

- Thermotropic Coatings

- Thermoluminescent Coatings

- Thermoresistive

By Material Chemistry

- Liquid Crystals

- Leuco Dyes

- Inorganic Pigments

- Polymer Matrices

- Specialized Materials

By Technology

- Water-based Systems

- Solvent-based Systems

- Powder-based Systems

- Microencapsulation

- Sol-Gel Technology

- Printable Inks

By Substrate

- Metals

- Plastics

- Paper and Cardboard

- Glass and Ceramics

- Textiles

By End-User Industry

- Packaging

- Industrial and Manufacturing

- Aerospace and Defense

- Automotive

- Consumer Goods and Household

- Healthcare and Medical Devices

- Energy and Power

By Sales Channel

- Direct Sales

- Specialized Industrial Distributors

- Research and Development Procurement

- E-commerce

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Temperature Sensitive Coating Industry

- PPG Industries, Inc.

- Akzo Nobel N.V.

- The Sherwin-Williams Company

- BASF SE

- Chromatic Technologies Inc.

- LCR Hallcrest, Inc.

- OliKrom

- SpotSee

- Matsui Shikiso Chemical Co., Ltd.

- 3M Company

- Axalta Coating Systems Ltd.

- Indestructible Paint Limited

- Innovative Scientific Solutions, Inc.

- Kansai Paint Co., Ltd.

- Rolls-Royce plc

*- List not Exhaustive