Zinc Oxide Market Overview 2025–2034: $10.1 Billion to $16.6 Billion at 5.7% CAGR Driven by Battery-Grade Expansion, Nano-Structured Innovation, and Circular Production

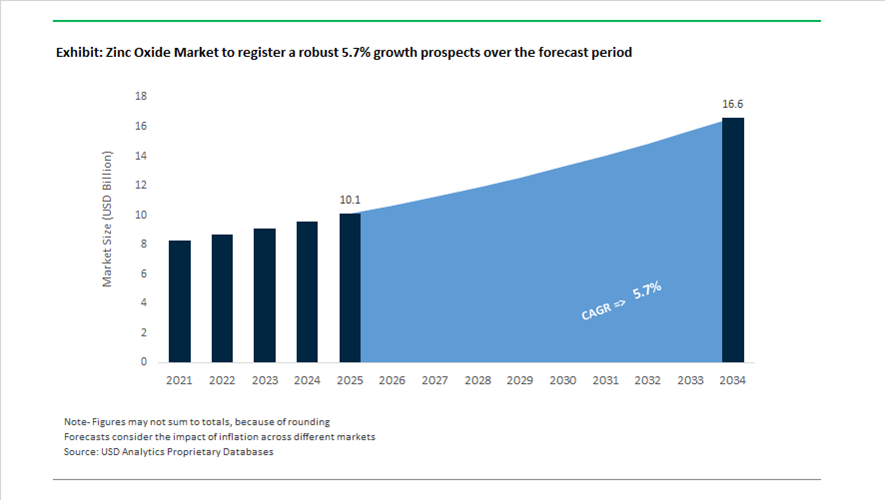

The Zinc Oxide market is valued at $10.1 billion in 2025 and is projected to reach $16.6 billion by 2034, expanding at a CAGR of 5.7%. Zinc oxide (ZnO), produced primarily via the French (indirect) and American (direct) processes, is indispensable in tire manufacturing, rubber vulcanization, ceramics, pharmaceuticals, cosmetics (UV filters), animal feed, electronics, and increasingly, rechargeable battery systems. Structural demand growth is linked to electrification trends, rising EV tire performance requirements, agricultural micronutrient fortification, and the expansion of grid-scale zinc-based storage technologies. Concurrently, sustainability pressures are reshaping feedstock sourcing, furnace efficiency, and dust-control technologies.

Industry consolidation and capital deployment accelerated between 2024 and 2025. The merger of U.S. Zinc and EverZinc was fully integrated, forming the world’s largest specialty zinc oxide producer with 14 production sites globally. In December 2025, EverZinc was acquired by affiliates of Cerberus Capital Management, injecting capital to accelerate expansion into energy storage and premium pharmaceutical-grade ZnO. Zochem expanded into South America during 2025–2026 through a strategic acquisition, targeting regional demand for emergency-backup batteries and agricultural micronutrients. In December 2025, Grillo Chemicals terminated force majeure at its Duisburg site following modernization of its zinc-based chemical lines under an “ECO ZINC” circular framework, restoring stability in European supply.

Technological differentiation intensified across high-value applications. In April 2024, Uviva Technologies launched Eclipse G1 zinc oxide granules engineered to reduce dust formation during mixing while retaining UV-protective and antimicrobial performance in cosmetics and rubber compounds. In 2025, researchers introduced “Black Zinc Oxide,” a nanostructured variant with enhanced light absorption characteristics, currently under pilot evaluation for solar cell efficiency enhancement and catalytic systems. An Indian zinc oxide producer announced a $28.7 million IPO in March 2024, allocating nearly $19 million toward an advanced R&D center focused on nano-grade and pharmaceutical ZnO grades, underscoring the premiumization trend.

Battery integration and low-carbon production are reshaping strategic priorities. In February 2026, EverZinc launched registration for the R-Zinc 4.0 Conference, highlighting commercial momentum behind rechargeable zinc battery technologies as safe alternatives to lithium-ion systems for stationary storage. Hindustan Zinc reported record revenues in early 2026 and retained top global ESG rankings, while commissioning a 160 ktpa Roaster at Debari and debottlenecking smelters at Chanderiya and Dariba to expand refined zinc supply for downstream chemical producers. Brüggemann’s biomass-powered plant in Heilbronn, operational through 2024–2025, uses 15,000 metric tons of biomass annually, materially lowering carbon intensity for zinc-based additives.

The zinc oxide market is advancing toward battery-grade and nano-structured ZnO, dust-free granulation formats, circular raw material sourcing, biomass-powered furnaces, and photovoltaic-grade black zinc oxide innovations. Demand from performance tires, sunscreen formulations, animal nutrition, electronics, and zinc-based energy storage will sustain mid-single-digit expansion through 2034.

Technology-Driven Trends and High-Impact Opportunities in the Zinc Oxide Market

Trend 1: Strategic Pivot Toward High-Purity ZnO for Advanced Electronics

The expansion of 5G infrastructure, hyperscale data centers, and smart power grids is accelerating the adoption of high-energy zinc oxide varistors, where material purity and microstructural consistency directly determine surge suppression performance.

As of December 2025, industry assessments indicate that over 71% of U.S. power substations and 56% of data centers have integrated ZnO varistor-based surge protection systems. This penetration reflects the non-linear voltage-current characteristics of ZnO, which enable rapid clamping of transient overvoltages in high-density electronic environments. The industry-wide push toward micro-varistors below 2 mm diameter has materially increased technical complexity, with manufacturers reporting 27% higher R&D spending to maintain energy absorption capacity at reduced geometries.

Telecom and electric mobility are reinforcing this trend. The global deployment of 8.1 million communication nodes has driven a 41% year-on-year increase in surface-mount varistor installations during 2025, as compact formats improve board-level integration. Simultaneously, automotive OEMs are specifying high-energy ZnO discs for EV power electronics and control units, where voltage spikes are more frequent due to fast-switching inverters. Field data show that ZnO-based protection improves component durability by approximately 33% compared to legacy silicon-based suppression technologies.

Trend 2: Reformulation of Mineral Sunscreens Under Non-Nano Regulatory Pressure

In personal care, zinc oxide is benefiting from a structural shift toward mineral-based UV filters, driven by clean-label demand and tightening regulatory scrutiny over inhalation and environmental risks.

Under Regulation (EC) No 1223/2009 and its 2024–2025 updates, the European Union continues to authorize both nano and non-nano ZnO for cosmetic use up to 25% concentration. However, new risk assessments have imposed application-specific restrictions, particularly limiting sprayable products due to inhalation exposure. As a result, brands are reformulating into creams, sticks, and balms while prioritizing coated, non-nano zinc oxide to ensure compliance without sacrificing SPF performance.

Australia represents a parallel inflection point. With sunscreens regulated as medicines by the TGA, 2025 compliance strategies increasingly favor coated ZnO clusters with ≥96% purity, engineered in rod-like or star-like morphologies. These structures reduce whitening while maintaining dermal absorption well below the 2% safety threshold, even in high-SPF formulations. This regulatory-driven reformulation is structurally increasing demand for surface-treated, cosmetic-grade ZnO, shifting value creation toward specialty producers rather than bulk suppliers.

Opportunity 1: Nano-ZnO as a Performance Lever in Low-Rolling-Resistance Tires

Vehicle electrification is redefining tire design economics, creating a strong opportunity for nano-scale zinc oxide as an advanced vulcanization activator that enables lighter, more energy-efficient rubber compounds.

Industrial testing published in October 2025 demonstrates that substituting conventional rubber-grade ZnO with nano-ZnO in tire bead fillers delivers a 3% reduction in rolling resistance. This improvement is achieved by lowering hysteresis and heat build-up, supported by a 28% reduction in tan δ, a critical indicator of energy loss. For EV manufacturers, these gains translate directly into extended driving range without altering vehicle architecture.

Environmental performance is reinforcing adoption. A 2024–2025 Life Cycle Assessment showed that silica-anchored ZnO nanoparticles (ZnO@SiO₂) can reduce the environmental footprint of tire manufacturing by 9–12% through lower zinc loading and improved fuel efficiency over the product lifecycle. As tire labeling regulations tighten globally, nano-ZnO is emerging as a primary sustainability enabler for major tire OEMs.

Opportunity 2: Zinc Oxide as a High-Value API and Medical Coating Material

Zinc oxide’s biocompatibility, antimicrobial activity, and regulatory acceptance are opening premium opportunities in pharmaceuticals and medical devices, well beyond its historical use in topical ointments.

A February 2025 study in the Journal of Coatings Technology and Research reported that PEG-ZnO nanocomposite coatings applied to PPE achieved a 99.9968% reduction in viral load, with 0.75 wt% ZnO identified as the optimal balance between antimicrobial efficacy and material breathability. This positions ZnO as a scalable solution for infection control in healthcare textiles.

From a therapeutic standpoint, ZnO’s GRAS designation by the FDA is accelerating its use as an Active Pharmaceutical Ingredient and functional coating in smart wound dressings and implantable devices. Recent research confirms that ZnO-based coatings can deliver up to 96% photocatalytic activity, enabling continuous degradation of pathogens and organic contaminants. These properties elevate zinc oxide into a high-margin specialty chemical, aligned with rising global investment in advanced wound care and hospital-acquired infection prevention.

Zinc Oxide Market Share and Segmentation Insights

Process Market Share: Indirect Process Leads with High-Purity Zinc Oxide for Critical Applications

The indirect process accounts for 52.80% of the zinc oxide market in 2025, driven by its ability to produce high-purity zinc oxide with consistent particle size and controlled morphology. This process is essential for demanding applications in rubber and tire manufacturing, pharmaceuticals, cosmetics, and electronics, where purity directly impacts product performance and regulatory compliance. Direct and wet chemical processes serve cost-sensitive or niche applications with different quality specifications. A key trend is the rising demand for high-purity zinc oxide, where manufacturers are investing in advanced purification technologies and process optimization to meet stringent requirements in pharmaceutical, cosmetic, and electronic-grade applications.

Application Market Share: Rubber and Tires Segment Leads with Global Vulcanization Demand

Rubber and tires hold a 48.60% share in the zinc oxide market in 2025, supported by its indispensable role as an activator in sulfur vulcanization processes used in tire production. The scale of global automotive manufacturing and tire replacement cycles drives sustained demand. Cosmetics and personal care, ceramics and glass, chemicals and catalysts, agriculture, pharmaceuticals, and electronics contribute to diversified consumption. A key market trend is the push toward sustainable tire manufacturing, where coated and nano-zinc oxide grades are being adopted to reduce zinc usage and environmental impact while maintaining vulcanization efficiency and performance standards required for modern tires.

Zinc Oxide Market Competitive Landscape

The Zinc Oxide market in 2026 is shaped by operational decarbonization and value-added specialization, with manufacturers advancing low-carbon ZnO production using renewable energy and muffle furnace technologies while scaling nano zinc oxide dispersions and surface-treated ZnO for cosmeceuticals, semiconductors, and high-performance coatings.

EverZinc Scales Ultra-Fine ZnO Portfolio Through Global Expansion and Battery-Grade Innovation

EverZinc continues to lead the specialty zinc oxide market through its diversified high-value portfolio and strong global manufacturing footprint. Following its December 2025 acquisition by Cerberus Capital Management, the company is accelerating investments in rechargeable zinc battery materials and specialty coatings. With 12 production sites across key regions, EverZinc ensures supply chain resilience for its Zano® ultra-fine zinc oxide used in high-SPF sunscreens and advanced industrial applications. The company’s leadership in organizing the R-Zinc 4.0 Conference reinforces its role in zinc-air and zinc-ion battery innovation. Its product range spans corrosion-resistant zinc powders to nano-dispersions tailored for transparency and UV-blocking efficiency. This multi-application strategy enables strong positioning in premium, non-commodity ZnO segments.

Hindustan Zinc Drives Low-Carbon ZnO Supply Chains with EcoZen and Downstream Integration

Hindustan Zinc Limited is redefining the zinc oxide value chain through scale, integration, and sustainability leadership. The company reported record refined metal production of 270 kt in Q3 FY2026, supported by smelter optimization projects. Its EcoZen low-carbon zinc brand, with emissions below 1 tonne CO2 per tonne, is increasingly adopted across downstream zinc oxide manufacturing. The March 2026 MoU with CMR Green Technologies to develop a facility at Zinc Park strengthens its presence in low-emission zinc alloy production. Partnerships with specialty players like Silox India highlight rising demand for low-carbon feedstocks in ZnO synthesis. This integration of upstream decarbonization and downstream expansion reinforces HZL’s influence in sustainable zinc oxide supply chains.

Zochem Enhances French Process ZnO Leadership with Automation and Capacity Expansion

Zochem is strengthening its position as North America’s largest French Process zinc oxide producer through sustainability-led operational scaling. The expansion of its Brampton and Dickson facilities enables continuous 24/7 production to meet rising demand from tire, pharmaceutical, and chemical sectors. Its strong safety record, exceeding 14 years without lost-time incidents, enhances credibility among Tier-1 clients. The company is deploying digital automation tools to improve production precision and reduce manual intervention. Industry validation from Smithers confirms that French Process ZnO delivers superior performance compared to American Process variants. This focus on high-purity, high-performance ZnO ensures Zochem’s leadership in premium application markets.

Grillo-Werke Strengthens GMP-Grade ZnO Production with Circular Economy Integration

Grillo-Werke is advancing its role in the European zinc oxide market through pharmaceutical-grade production and circular material strategies. Its Goslar facility produces ZnO compliant with EU GMP and US FDA standards, supporting pharmaceutical and cosmeceutical applications. The ECO ZINC initiative leverages secondary raw materials to significantly reduce product carbon footprint, aligning with sustainability-driven procurement trends. The company is expanding ZnO applications into zinc-air battery technologies, targeting grid-scale energy storage markets. With over a century of expertise, Grillo offers customized ZnO formulations tailored to specific industrial requirements. Its certified, traceable European supply chain strengthens its position in regulated, high-purity ZnO segments.

Zinc Oxide LLC Expands Specialty ZnO Capabilities Through Recycling and Nano-Coating Innovation

Zinc Oxide LLC, formed through the integration of U.S. Zinc and EverZinc assets, operates as a major global supplier of specialty zinc oxide solutions. The company focuses on high-grade and special high-grade recycled zinc inputs, enabling sustainable ZnO production for industrial and agricultural applications. Its centralized logistics network across North America provides a single-source solution for high-volume customers. The group is expanding its Zano® portfolio with coated nano zinc oxide variants designed for advanced electronics, including thin-film transistors and flexible devices. Subsidiaries such as Midwest Zinc and Gulf Reduction enhance feedstock security and processing efficiency. This recycling-driven and innovation-focused model strengthens its competitiveness in next-generation ZnO markets.

India Zinc Oxide Market Driven by Smelter Expansion and Agriculture-Led Demand

India’s zinc oxide market is entering a structurally transformative phase, anchored by upstream capacity expansion and downstream consumption pull from infrastructure and agriculture. In June 2025, Hindustan Zinc Limited announced a board-approved investment of ₹12,000 crore to initiate the first phase of doubling its integrated metal capacity. Central to this plan is a new 250 KTPA smelter at Debari, explicitly designed to support domestic demand for high-grade zinc chemical feedstocks, including pharmaceutical and specialty zinc oxide. This expansion forms part of a broader capital expenditure roadmap of ₹30,000–35,000 crore over the next three to five years, targeting a total metal production capacity of 2,000 KTPA. From a supply-chain perspective, this materially strengthens India’s self-reliance in zinc oxide inputs and reduces exposure to imported high-purity grades.

On the demand side, India’s ₹11.11 lakh crore infrastructure allocation for 2025–2026 is driving sustained consumption of zinc oxide in galvanization-grade coatings, industrial primers, and corrosion-resistant steel systems. In parallel, agricultural policy is becoming an increasingly important growth vector. Under the 2026 targets of the Pradhan Mantri Krishi Sinchayee Yojana, subsidies for zinc oxide-fortified fertilizers have been expanded to address chronic zinc deficiency across the Indo-Gangetic plain. This combination of industrial and micronutrient demand is positioning India as one of the fastest-evolving zinc oxide markets, spanning bulk, fertilizer-grade, and emerging battery-related applications.

United States Zinc Oxide Market Shaped by Energy Storage and Reshoring

The United States zinc oxide market is being reshaped by federal critical minerals policy, energy storage commercialization, and trade-driven reshoring. In November 2025, the U.S. Department of Energy announced $355 million in new funding to strengthen domestic critical material production, including the recovery of high-value zinc units from industrial byproducts. This initiative directly supports recycled feedstock availability for the Direct Process of zinc oxide manufacturing, aligning cost efficiency with sustainability goals. Simultaneously, CHIPS Act-driven semiconductor investments have accelerated R&D into electronic-grade zinc oxide, used as a wide-bandgap semiconductor in high-power varistors and gas sensors for advanced electronics.

Battery applications represent a second structural pillar. In late 2025, Eos Energy Enterprises expanded production of its Z3 zinc-battery platform, relying on specialized zinc oxide grades as cathode stabilizers for long-duration energy storage systems. Trade policy is reinforcing domestic supply chains. The implementation of reciprocal tariffs in early 2026 has triggered active reshoring of zinc oxide production, with producers such as Zochem and U.S. Zinc expanding domestic lines to replace higher-cost Asian imports. Collectively, these dynamics are repositioning the U.S. as a high-value zinc oxide market focused on energy, electronics, and secure sourcing.

China Zinc Oxide Market Transitioning Toward Green French Process Models

China remains the world’s largest zinc oxide consumer, with policy now accelerating a transition toward cleaner and more advanced production models. In August 2025, the Ministry of Ecology and Environment and MIIT released a joint Action Plan for Industrial Emission Control, mandating that zinc oxide producers install advanced catalytic abatement systems by 2026 to neutralize N₂O and SOx byproducts. This requirement is particularly impactful for French Process operators, pushing rapid modernization across major clusters. Under the Made in China 2025 framework, more than 40% of the Shandong zinc cluster has already transitioned to Green Innovation models, including biomass-fired heating systems that enable carbon-neutral zinc oxide certification.

End-use demand remains robust, especially in rubber and mobility applications. In 2025, China’s domestic tire output rose by 12%, driven largely by EV exports that require high-surface-area zinc oxide for enhanced heat dissipation and durability. At the technology frontier, the National Natural Science Foundation of China funded multiple 2025 research programs on hierarchical nano-zinc oxide structures, targeting self-cleaning architectural glass and high-efficiency wastewater photocatalysis. These developments signal a dual-track market evolution in China, balancing scale-driven rubber demand with innovation-led nano and environmental applications.

Belgium and Germany Zinc Oxide Market Anchored by Pharma-Grade Leadership

Belgium and Germany occupy a premium position in the global zinc oxide landscape, defined by pharmaceutical-grade purity, nano-scale innovation, and low-carbon processing. In December 2025, EverZinc finalized strategic steps to accelerate commercialization of Zano®, a high-transparency nano-zinc oxide developed for the premium suncare and dermatology market. EverZinc remains the only global producer with GMP-certified zinc oxide holding an official CEP, positioning European supply chains as the default choice for pharmaceutical and clinical skincare manufacturers preparing for tighter purity standards in 2026.

Sustainability-led processing is reinforcing this competitive edge. German producer Brüggemann successfully scaled biomass-powered refining at its Heilbronn site in 2025, processing 15,000 metric tons of biomass annually to produce low-carbon-footprint zinc oxide for polymers and specialty chemicals. Complementing this, German-led innovations such as Uviva Technologies’ Eclipse G1 introduced free-flowing zinc oxide granules that eliminate dust during mixing, significantly improving occupational safety and handling efficiency in large-scale cosmetic production. These factors collectively position Belgium and Germany as technology and compliance benchmarks for the global zinc oxide market.

Zinc Oxide Market Country Snapshot

Zinc Oxide Market County Level Snapshot

|

Region

|

Strategic Focus

|

Key Zinc Oxide Applications

|

Market Positioning

|

|

India

|

Smelter expansion and fertilizer demand

|

Galvanization, micronutrient fertilizers

|

High-growth, capacity-led

|

|

United States

|

Energy storage and reshoring

|

Zinc batteries, electronics

|

High-value, policy-driven

|

|

China

|

Green French Process and EV tires

|

Rubber, nano-ZnO

|

Scale with rapid modernization

|

|

Belgium & Germany

|

GMP purity and nano innovation

|

Pharma, suncare, polymers

|

Premium and compliance-led

|

Zinc Oxide Market Report Scope

Zinc Oxide Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.1 Billion

|

|

Market Size (2034)

|

$16.6 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Process (Indirect Process, Direct Process, Wet Chemical Process), By Grade (Standard Grade, Pharmaceutical Grade, Food and Feed Grade, Specialty Grade), By Application (Rubber and Tires, Ceramics and Glass, Cosmetics and Personal Care, Pharmaceuticals, Agriculture, Chemicals and Catalysts, Electronics and Energy)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

EverZinc, Hindustan Zinc Limited, Zochem Inc., U.S. Zinc, Brüggemann Group, Sakai Chemical Industry Co., Ltd., Rubamin, Uviva Technologies GmbH, Pan-Continental Chemical Co., Ltd., Sinopec Corporation, Grillo-Werke AG, Silox S.A., Seyang Zinc Technology Co., Ltd., Global Chemical Co., Ltd., Akrochem Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Zinc Oxide Market Segmentation

By Process

- Indirect Process

- Direct Process

- Wet Chemical Process

By Grade

- Standard Grade

- Pharmaceutical Grade

- Food and Feed Grade

- Specialty Grade

By Application

- Rubber and Tires

- Ceramics and Glass

- Cosmetics and Personal Care

- Pharmaceuticals

- Agriculture

- Chemicals and Catalysts

- Electronics and Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Zinc Oxide Market

- EverZinc

- Hindustan Zinc Limited

- Zochem Inc.

- U.S. Zinc

- Brüggemann Group

- Sakai Chemical Industry Co., Ltd.

- Rubamin

- Uviva Technologies GmbH

- Pan-Continental Chemical Co., Ltd.

- Sinopec Corporation

- Grillo-Werke AG

- Silox S.A.

- Seyang Zinc Technology Co., Ltd.

- Global Chemical Co., Ltd.

- Akrochem Corporation

*- List not Exhaustive