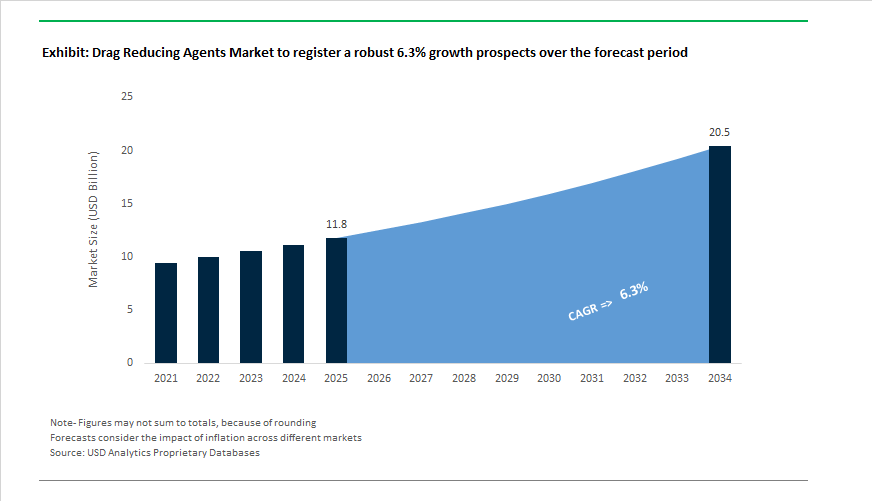

Drag Reducing Agents Market to Reach $20.4 Billion by 2034 at 6.3% CAGR Driven by Offshore Expansion and Digital Flow Optimization

The Drag Reducing Agents (DRA) Market is projected to grow from $11.8 billion in 2025 to $20.4 billion by 2034, registering a CAGR of 6.3%. Market momentum is closely tied to crude oil and refined product pipeline expansions, deepwater developments, and increasing demand for energy-efficient flow assurance technologies. In 2024, LiquidPower Specialty Products Inc. (LSPI), a Berkshire Hathaway company, finalized its equity investment in Safe Marine Transfer to deploy subsea drag reducing agents using patented all-electric dual-barrier delivery systems. This marked a structural shift in offshore DRA deployment, enabling safer injection in deepwater environments. The same year, Innospec introduced AquaBourne™, a water-based friction reducer designed to address environmental scrutiny surrounding oil-based formulations used in hydraulic fracturing and pipeline transport. The launch reflected growing regulatory and ESG pressures to lower aquatic toxicity and reduce hydrocarbon residues in produced water systems.

Capacity expansion and contract consolidation accelerated through 2025 as operators prioritized throughput optimization over new pipeline construction. In March 2025, Innospec announced a major expansion of its Pleasanton, Texas facility, with full operational capacity expected by Q4 2025 to meet rising domestic and export demand for specialty DRAs. In June 2025, bp awarded Baker Hughes a multi-year chemicals management contract for U.S. Gulf Coast pipelines, integrating advanced DRA formulations with digital monitoring systems. This was followed in July 2025 by Baker Hughes securing a multi-year supply agreement with Genesis Energy for the Cameron Highway and Poseidon offshore pipeline systems in the Gulf of Mexico. The agreement includes deployment of the Leucipa™ automated field production solution, designed to optimize DRA dosage rates and enhance pipeline throughput efficiency under fluctuating flow conditions. In parallel, Indian Oil Corporation commercialized its patented ultra-high molecular weight DRA polymer in 2025, strengthening India’s domestic additive capability and reducing reliance on imports for national crude pipeline infrastructure.

Innovation in formulation technology and regional capacity investments are reshaping competitive positioning heading into 2026. IRIS Tech launched HyMotion™ dry drag reducing agent in 2025, introducing a powdered injection solution that eliminates the need for liquid suspension transport in remote pipeline operations. BASF collaborated with offshore operators during 2025 to engineer customized DRA chemistries capable of maintaining solubility and flow stability in high-pressure, low-temperature subsea fields. In October 2025, Dow partnered with Schneider Electric to enhance circularity in thermoplastic carriers used in DRA systems, targeting Scope 3 emission reductions across pipeline chemical supply chains. Flowchem, a subsidiary of Kao Corporation, announced a manufacturing expansion in January 2026 to serve Middle East and North Africa infrastructure growth, while Qflo expanded its North Sea DRA support services in early 2026, deploying mobile injection skids and real-time advisory systems to optimize late-life asset performance. These developments highlight a structural evolution toward digitalized dosing, subsea-ready formulations, sustainable polymer carriers, and geographically diversified production hubs within the global drag reducing agents market.

Trends and Opportunities in the Drag Reducing Agents (DRAs) Market

Strategic Shift Toward High-Performance, Application-Specific DRA Chemistries

- Pipeline operators are increasingly abandoning one-size-fits-all DRA formulations in favor of chemistries engineered for specific crude slates, viscosity profiles, and shear environments. This shift is particularly pronounced in heavy crude, asphaltenic streams, and aging pipelines where conventional DRAs suffer from mechanical degradation and inconsistent performance.

- In January 2025, Aether Industries formalized a strategic amendment with Baker Hughes to exclusively manufacture high-end specialty chemicals, including next-generation DRA components. Production is anchored at Aether’s newly operational Site 4 facility, designed to support controlled polymerization and formulation of shear-stable additives for high-pressure pipeline environments.

- A notable example of this technological shift is Baker Hughes’ FLO ULTIMA series, a latex-based DRA developed specifically for asphaltenic heavy oil systems. Unlike traditional DRAs that lose effectiveness in high-viscosity crudes, this formulation has demonstrated flow rate increases exceeding 25% and drag reduction performance of up to 50% in asphaltene-rich streams. For operators, this level of efficiency enables the shutdown of intermediate pump stations, directly reducing operating expenditure and maintenance exposure.

- These advanced DRAs are particularly valuable in North America, where a significant portion of pipeline infrastructure is operating under pressure constraints. Field deployments indicate that shear-stable formulations allow operators to maintain target throughput while reducing pump discharge pressures, translating into power consumption savings in the range of 10 to 15% without compromising line integrity.

Integration of Automated, On-Site Dosing and Real-Time Monitoring Systems

- The DRA market is rapidly adopting a chemical management as a service model, where performance is optimized through automation, analytics, and continuous monitoring rather than static dosing practices. Midstream companies are investing in on-site injection skids integrated with pipeline SCADA systems to dynamically adjust DRA dosage based on real-time operating conditions.

- In 2024, Innospec introduced an AI-enabled chemical injection monitoring platform capable of adjusting DRA feed rates in response to live data on temperature, viscosity, and flow regime. Early deployments have shown the potential to reduce chemical overuse by up to 20% while maintaining or improving drag reduction performance, directly improving cost efficiency per barrel transported.

- This digital shift is closely tied to the growing dominance of liquid DRA formulations, which accounted for approximately 75% of total market volume in 2024. Liquid products are inherently compatible with automated skids and standard metering pumps, enabling turnkey injection without manual handling or frequent truck-based servicing. For remote wellhead locations and long-distance pipelines, this ease of deployment is becoming a decisive procurement criterion.

Decarbonization and Emission Reduction Through Pipeline Energy Optimization

- DRAs are increasingly being reframed as decarbonization tools rather than purely throughput-enhancing additives. By lowering frictional resistance, DRAs allow pipelines to increase capacity or maintain throughput without installing additional compressors or pump stations, which are among the most carbon-intensive assets in midstream operations.

- Industry analysis indicates that optimized DRA programs can defer or eliminate the need for new compression infrastructure, avoiding significant methane and carbon dioxide emissions associated with gas-driven compressors. This positioning aligns directly with Scope 1 and Scope 2 emission reduction targets now embedded in midstream ESG strategies.

- Regulatory pressure is reinforcing this trend. The U.S. Environmental Protection Agency introduced stricter 2024 and 2025 rules targeting gas-driven pneumatic devices and internal combustion engines in oil and gas operations. These restrictions incentivize operators to maximize throughput through chemical optimization rather than mechanical expansion.

- In Canada, the Trans Mountain Expansion project has evaluated the use of DRAs to increase throughput by up to 300,000 barrels per day. This approach, often referred to as chemical expansion, offers a lower-emission bridge solution that meets near-term demand growth while deferring the environmental footprint of additional pipeline loops.

Expansion into CCUS, Dense-Phase CO₂, and Non-Traditional Fluid Transport

- The rapid global scale-up of carbon capture, utilization, and storage infrastructure is creating a new frontier for specialized DRAs capable of operating in dense-phase carbon dioxide and complex multiphase systems. Transporting CO₂ under supercritical or near-supercritical conditions requires precise control of friction and flow regime to maintain phase stability over long distances.

- As of late 2025, the Global CCS Institute reported a sharp increase in CCUS project development worldwide, including the Porthos project in the Netherlands, which targets 2.5 million metric tons of CO₂ injection per year by 2027. These projects are accelerating demand for DRAs engineered for non-hydrocarbon environments, where conventional polymer additives are ineffective.

- In India, NITI Aayog and the Ministry of Petroleum and Natural Gas have outlined plans for 900 kilotons per annum of green hydrogen production alongside large-scale CCUS infrastructure by 2030. This policy direction creates a domestic requirement for DRAs that can function reliably in CO₂ pipelines, hydrogen-adjacent systems, and long-distance slurry transport.

- Ongoing research into nano-dispersed DRA formulations aims to address the unique rheology of supercritical fluids. If successfully commercialized, these additives could reduce the number of booster stations required for cross-country CCUS networks by an estimated 15 to 20 %, materially lowering the levelized cost of carbon transport and strengthening the economic case for large-scale decarbonization infrastructure.

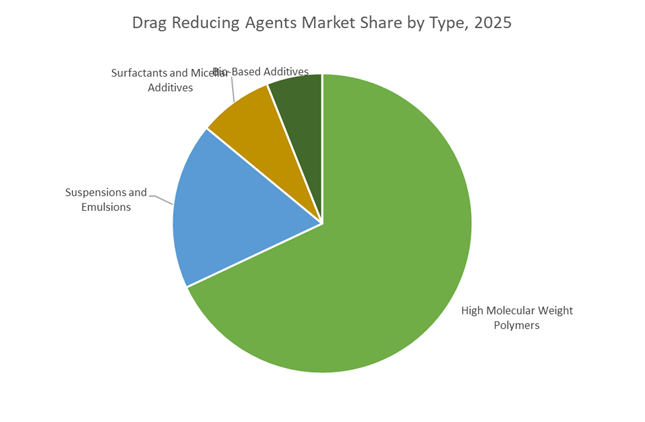

Drag Reducing Agents (DRA) Market Share and Segmentation Insights

High Molecular Weight Polymer DRAs Dominate Pipeline Flow Optimization

High molecular weight polymer drag reducing agents command 68% of total market share in 2025, underscoring their superior effectiveness in reducing turbulent flow friction in liquid hydrocarbon pipelines. Polyalphaolefin and polyisobutylene-based DRAs disrupt eddy formation near pipeline walls, enabling higher throughput or reduced pumping energy at very low dosage levels. Their proven performance makes them the preferred solution for long-distance crude oil and refined product pipelines. Suspension and emulsion-based DRAs represent a significant share due to easier handling, safer transportation, and precise automated injection in remote field operations. Surfactant and micellar drag reducers serve niche applications, particularly in water-based systems and district heating networks, where polymer shear degradation is a concern. Bio-based drag reducing agents are emerging gradually, supported by tightening environmental regulations and sustainability targets within pipeline operations.

Midstream Oil and Gas Pipelines Account for the Majority of DRA Consumption

The midstream oil and gas sector contributes 72% of global DRA demand, reflecting the strategic importance of drag reduction in maximizing existing pipeline capacity. Pipeline operators deploy DRAs to increase flow rates without infrastructure expansion, manage seasonal demand fluctuations, and maintain throughput during maintenance periods. Refinery and petrochemical processing facilities form a significant secondary segment, applying DRAs in transfer lines and inter-facility pipelines to reduce energy consumption and operational costs. Marine and terminal operations are a growing end-user group, leveraging DRAs to accelerate tanker loading and unloading, minimize vessel turnaround times, and improve terminal efficiency. Civil engineering and urban water management remain niche but stable segments, using drag reducing agents in flood control systems, stormwater management, and pressurized water distribution networks to enhance flow capacity and reduce pumping requirements.

Competitive Landscape of the Drag Reducing Agents (DRA) Market

The global Drag Reducing Agents market in 2026 is shaped by pipeline throughput optimization, deepwater flow assurance, and smart polymer chemistry, with leading players competing on polymer performance, integrated injection systems, and real-time digital dosing across oil & gas, refinery, and midstream infrastructure.

LiquidPower Specialty Products dominates pipeline DRA with integrated subsea delivery systems

LiquidPower Specialty Products Inc. (LSPI) is the world’s largest DRA manufacturer, commanding 27.5% global market share in 2026. Its LiquidPower™ DRAs, including heavy-oil reducers and the Extreme™ line, are engineered for high-turbulence pipelines. In late 2025, LSPI expanded its partnership with Safe Marine Transfer to deploy subsea DRA delivery systems, enabling deepwater flow assurance without topside intervention. With roots dating back to the first commercial pipeline DRA in 1979, LSPI holds the industry’s deepest patent portfolio in polymer drag reduction. Its Integrated Systems Approach, combining proprietary injection hardware, on-site maintenance, and 24/7 technical support, makes LSPI the benchmark for guaranteed throughput and energy savings.

Baker Hughes integrates smart DRA chemistry with real-time refinery optimization

Baker Hughes Company embeds DRAs within its broader Downstream Chemical Solutions platform. Its FLO™ technology suite, including FLO™ XLWR for water systems and FLO™ ULTIMA for heavy crude, targets refinery and pipeline debottlenecking. In 2026, Baker Hughes launched FLO™ NOW, an instant drag reduction service using real-time analytics to automatically adjust dosage based on changing crude blends. The company is a leader in refinery throughput optimization, helping operators process opportunity crudes while lowering pumping energy. Major 2026 contracts across the US and Europe highlight Baker Hughes’ growing footprint, with clients reportedly saving thousands per day through adaptive DRA deployment and digital flow control.

Innospec accelerates midstream capacity with IoT-enabled friction reducers

Innospec Inc. focuses on complex flow chemistry challenges in pipelines and fuel logistics. Its AquaBourne™ water-based friction reducer is engineered for high-salinity environments common in 2026-generation hydraulic fracturing and wastewater transport. In late 2025, Innospec upgraded its injection skids with remote IoT monitoring, enabling ultra-low concentration dosing and tighter operational control. Known for versatile debottlenecking, Innospec helps operators increase pipeline capacity without adding pump stations or physical infrastructure. Strategically, the company is expanding across Asia-Pacific and the Middle East, where new long-distance pipelines in China and India are driving strong demand for high-efficiency drag reducing agents.

Flowchem challenges incumbents with shear-resistant smart polymer DRAs

Flowchem, a subsidiary of KAO Corporation, holds an estimated 22.2% global DRA market share in 2026, making it the primary challenger to LSPI. Flowchem specializes in high-viscosity “glue” DRAs designed for large-diameter gas and NGL pipelines, delivering superior shear resistance under extreme pressure. In early 2026, the company announced major investments in advanced polymerization techniques to develop temperature-stable smart polymers for harsher operating conditions. Backed by KAO’s global surfactant manufacturing network, Flowchem benefits from vertically integrated emulsifier supply, strengthening its position in suspension-grade DRAs for high-throughput energy corridors worldwide.

Nalco Champion leads deepwater flow assurance with predictive DRA analytics

Nalco Champion operates as a full-spectrum flow assurance partner, covering the fluid lifecycle from reservoir to refinery. Its SurFlo™ Plus certified chemistries, introduced in 2025, combine drag reduction with corrosion inhibition for ultra-deepwater umbilicals. Leveraging ECOLAB3D™ IIoT analytics, Nalco Champion delivers predictive dosing that minimizes chemical waste while improving pipeline efficiency. With over 950 industry patents and one of the largest global field service networks, the company dominates deepwater DRA applications, where products must perform under extreme pressures and temperatures from near-freezing to 120°C. Its strength lies in pairing advanced polymers with on-site expertise across every major oil-producing basin.

United States: AI-Enabled Injection and Capacity-Led Throughput Gains

The United States drag reducing agents market is undergoing a decisive transition toward digitally optimized, high-capacity pipeline operations. In March 2025, Innospec announced a major production expansion at its Pleasanton, Texas facility, with new capacity scheduled to come on-stream in Q4 2025. This expansion is strategically designed to support rising domestic and export demand for proprietary DRA formulations used in long-haul crude oil and refined product pipelines. Capacity additions are increasingly aligned with higher molecular-weight polymer chemistries that deliver throughput gains without requiring pipeline uprating or additional pumping infrastructure.

Application-side innovation is equally significant. In July 2025, Baker Hughes secured a multi-year offshore contract from Genesis Energy, integrating DRAs with the Leucipa™ automated field production system across the Cameron Highway and Poseidon pipelines. This deployment uses real-time AI to optimize injection rates, minimizing chemical overuse while stabilizing flow. Heavy crude transportation has emerged as another focal area, with midstream operators rapidly adopting FLO™ ULTIMA to handle higher-viscosity Canadian imports. Field data indicates frictional pressure reductions of 30% to 50% without major capital expenditure. Regulatory alignment is reinforcing these trends. Under the EPA’s 2025 Strategic Plan, operators are shifting toward water-based AquaBourne technologies that eliminate surfactants and oils, reducing environmental exposure risks during spills. The operational impact is visible in projects such as Kinder Morgan’s SFPP East Line Expansion, which went live in July 2025 with high-efficiency DRA skids enabling incremental throughput at the Deming pump station.

China: National Pipeline Integration and Polymer Chemistry Localization

China’s drag reducing agents market is increasingly shaped by national energy efficiency mandates and domestic polymer innovation. In 2025, China Oil & Gas Pipeline Network Corp deployed advanced DRA monitoring systems across the West–East Gas Pipeline network. This integration combines real-time flow analytics with optimized chemical dosing and is projected to reduce pump station energy consumption by 12% by the end of 2026. The initiative underscores China’s focus on operational efficiency at scale, particularly across ultra-long-distance transmission corridors.

On the supply side, domestic chemical producers in Zhejiang achieved a late-2025 breakthrough in synthesizing ultra-high-molecular-weight poly-alpha-olefins. These polymers enable effective drag reduction at significantly lower ppm dosages, improving cost efficiency and reducing chemical load per barrel transported. Policy support is reinforcing localization. Under the Ministry of Industry and Information Technology 2025–2027 Work Plan, the government has set a target of 75% domestic content for specialty oilfield chemicals, including DRAs. This is accelerating the shift away from imported formulations and positioning Chinese suppliers as competitive exporters to Central Asia and Southeast Asia.

India: Policy-Driven Adoption and Offshore Readiness

India’s drag reducing agents market is being propelled by energy-efficiency mandates and domestic manufacturing partnerships. A central development is the optimization of the Dahej, Gujarat DRA facility operated under the partnership between Indian Oil Corporation and Dorf Ketal. By 2025, this site had become a primary supply hub for high-performance DRAs used across India’s cross-country crude pipelines, supporting reliability and localized sourcing.

Regulatory pressure is amplifying demand. In 2025, the Ministry of Petroleum and Natural Gas issued directives requiring state-owned refiners to reduce midstream carbon intensity, explicitly encouraging the adoption of chemical flow improvers over energy-intensive mechanical pumping. This policy shift has driven mandatory DRA deployment along key routes such as the Kandla–Bhatinda pipeline. Forward-looking demand is also emerging offshore. With intensified exploration in the Krishna–Godavari Basin, 2026 procurement tenders are prioritizing DRAs capable of maintaining performance under high-pressure, low-temperature subsea conditions, signaling a move toward more technically advanced formulations.

Kuwait: Reservoir-Specific R&D and Integrated Lift Systems

Kuwait’s DRA market is closely linked to production optimization in high-salinity, high-temperature reservoirs. In December 2025, Baker Hughes secured a multi-year award from Kuwait Oil Company. While the contract centers on artificial lift, it also integrates DRA skids at gathering centers to ensure that incremental production from Leucipa™-optimized wells does not create downstream bottlenecks.

To localize innovation, a 2025 memorandum of understanding established a dedicated R&D center in Ahmadi Innovation Valley. This facility focuses on tailoring DRA chemistries for Kuwait’s unique crude profiles, emphasizing thermal stability and salt tolerance. The strategic objective is to reduce reliance on generic formulations and improve pipeline reliability under extreme operating conditions.

Saudi Arabia: Shear-Resistant Polymers and Non-Metallic Strategy

Saudi Arabia is embedding drag reducing agents into a broader midstream modernization and non-metallic materials strategy. In November 2025, Saudi Aramco signed 17 memoranda of understanding with U.S. energy technology firms to modernize its supply chain. A core element involves deploying next-generation, shear-resistant DRAs across the East–West Crude Oil Pipeline to maintain flow rates under high turbulence and variable throughput.

These initiatives align with the Kingdom’s Non-Metallic materials program, which emphasizes polymer-based solutions to mitigate corrosion and extend pipeline life. By reducing turbulence-induced wall shear, advanced DRAs are being positioned not only as throughput enhancers but also as contributors to asset integrity and long-term maintenance cost reduction.

Drag Reducing Agents Market: Country-Level Strategic Snapshot

Drag Reducing Agents Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Application Focus

|

Structural Direction

|

|

United States

|

AI-enabled injection and capacity expansion

|

Offshore pipelines, heavy crude, terminals

|

Water-based, shear-stable DRAs

|

|

China

|

National pipeline efficiency and localization

|

Long-distance gas and crude pipelines

|

Ultra-high MW polymers, low ppm dosing

|

|

India

|

Energy-efficiency mandates and localization

|

Cross-country pipelines, offshore prep

|

Policy-driven adoption, HPHT-ready DRAs

|

|

Kuwait

|

Reservoir-specific optimization

|

Gathering centers, artificial lift integration

|

High-salinity, high-temperature formulations

|

|

Saudi Arabia

|

Midstream modernization and asset integrity

|

East–West crude pipeline

|

Shear-resistant, non-metallic-aligned DRAs

|

Drag Reducing Agents Market Report Scope

Drag Reducing Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.8 Billion

|

|

Market Size (2034)

|

$20.4 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Type (High Molecular Weight Polymers, Surfactants and Micellar Additives, Suspensions and Emulsions, Bio-Based Additives), By Form (Liquid and Slurry, Powdered and Granular), By Application (Crude Oil Transportation, Refined Product Pipelines, Multi-Product Pipelines, Heavy Crude Oil Flow Improvement, Water Injection and Irrigation Systems, Firefighting), By End-User Industry (Midstream Oil and Gas, Refinery and Petrochemical Processing, Marine and Terminals, Civil Engineering and Urban Water Management)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

LiquidPower Specialty Products Inc., Innospec Inc., Baker Hughes Company, Flowchem, Dorf Ketal Chemicals India Pvt. Ltd., ChampionX Corporation, Suez Water Technologies & Solutions, Infinum, NuGenTec, Evonik Industries AG, Q Petro, The Lubrizol Corporation, Clariant AG, Zirax Ltd., China National Petroleum Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Drag Reducing Agents Market Segmentation

By Type

- High Molecular Weight Polymers

- Surfactants and Micellar Additives

- Suspensions and Emulsions

- Bio-Based Additives

By Form

- Liquid and Slurry

- Powdered and Granular

By Application

- Crude Oil Transportation

- Refined Product Pipelines

- Multi-Product Pipelines

- Heavy Crude Oil Flow Improvement

- Water Injection and Irrigation Systems

- Firefighting

By End-User Industry

- Midstream Oil and Gas

- Refinery and Petrochemical Processing

- Marine and Terminals

- Civil Engineering and Urban Water Management

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Drag Reducing Agents Industry

- LiquidPower Specialty Products Inc.

- Innospec Inc.

- Baker Hughes Company

- Flowchem

- Dorf Ketal Chemicals India Pvt. Ltd.

- ChampionX Corporation

- Suez Water Technologies & Solutions

- Infinum

- NuGenTec

- Evonik Industries AG

- Q Petro

- The Lubrizol Corporation

- Clariant AG

- Zirax Ltd.

- China National Petroleum Corporation

*- List not Exhaustive