Specialty Oilfield Chemicals Market Valuation 2025–2034: $13.5 Billion to $21.5 Billion at 5.3% CAGR Driven by Digital Production Chemistry, EOR Demand, and Sustainable Formulations

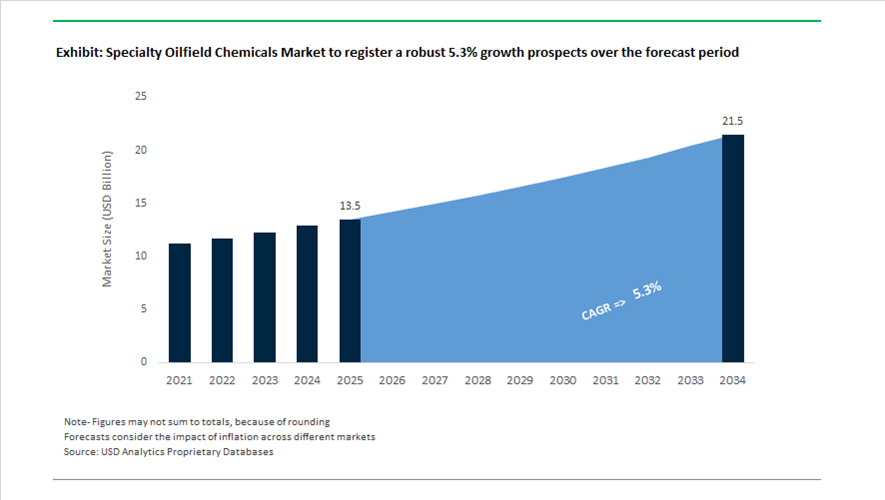

The global specialty oilfield chemicals market is valued at $13.5 billion in 2025 and is projected to reach $21.5 billion by 2034, expanding at a CAGR of 5.3%. Growth is supported by rising demand for production chemicals, corrosion inhibitors, scale inhibitors, demulsifiers, friction reducers, biocides, rheology modifiers, and enhanced oil recovery (EOR) formulations across mature reservoirs, deepwater assets, and unconventional shale plays. Operators are increasingly deploying digital oilfield technologies and AI-assisted chemical optimization platforms to enhance flow assurance, minimize downtime, and reduce chemical overdosing. Environmental discharge regulations in offshore regions and decarbonization mandates are accelerating the development of low-toxicity and bio-based specialty oilfield chemicals.

Market consolidation accelerated in 2024 and 2025. Throughout 2024, Dorf Ketal completed the operational integration of Clariant’s North American Land Oil business, strengthening its production chemical footprint across the Permian Basin and major U.S. shale plays. In October 2024, Baker Hughes announced the acquisition of EcoPetra Chemical Technologies, finalizing the deal in 2025 to enhance its corrosion and scale inhibitor portfolio for mature reservoir and EOR applications. In July 2025, SLB completed its landmark all-stock acquisition of ChampionX, integrating production chemicals with digital and subsea technologies and targeting $400 million in annual pre-tax synergies by 2026. In September 2025, Chevron Oronite acquired AccelChem Innovations to expand its friction reducer and bio-based surfactant portfolio for unconventional and deepwater drilling operations.

Technology-driven expansion intensified in late 2025 and early 2026. In December 2025, Baker Hughes expanded its Advanced Chemical Solutions Platform in Europe, embedding AI-assisted formulation systems to optimize specialty chemical deployment in high-pressure North Sea environments. In October 2025, Chevron Oronite unveiled an enhanced production chemical suite in Brazil targeting scale and corrosion challenges in offshore pre-salt reservoirs. In January 2026, SLB launched its Next-Generation Eco-Chemical Series, designed with improved biodegradability and reduced toxicity for offshore projects with strict discharge limits. In February 2026, Halliburton inaugurated a world-scale Chemical Reaction Plant in Saudi Arabia to localize manufacturing of high-performance specialty chemicals for Middle East upstream projects. The same month, Baker Hughes secured a multi-year downstream chemicals agreement with Marathon Petroleum covering 12 refineries, deploying XERIC™ demulsifiers and BIOQUEST™ renewable additives.

Sustainability and renewable chemistries are influencing product development pipelines. In early 2026, Nouryon introduced FinnFix® PB MAX, a 100% bio-based carboxymethylcellulose engineered for fluid loss control and rheology modification in drilling fluids. Increasing integration of digital monitoring, bio-based additives, localized production hubs, EOR-optimized chemistries, and offshore environmental compliance solutions is redefining competitive dynamics in the specialty oilfield chemicals market through 2034.

Strategic Trends and High-Impact Opportunities in the Specialty Oilfield Chemicals Market

Chemical Resilience Requirements Accelerate in HPHT and Sour Gas Developments

The global upstream industry is undergoing a structural shift away from mature, shallow-water reservoirs toward High-Pressure High-Temperature (HPHT) and sour gas fields that present extreme chemical and mechanical stress conditions. Reservoir environments exceeding 200°C and pressures approaching 20,000 psi fundamentally alter the performance envelope required of corrosion inhibitors, scale inhibitors, and production chemicals. In these settings, conventional formulations rapidly degrade, making specialty oilfield chemicals with engineered thermal stability and H₂S resistance a non-negotiable requirement rather than a performance upgrade.

This shift is clearly visible in long-duration contractual commitments by supermajors. In February 2025, Baker Hughes secured a multi-year specialty chemicals contract from ExxonMobil Guyana for the Uaru and Whiptail developments within the Stabroek Block. These projects are central to Guyana’s plan to reach 1.3 million barrels per day of production and require highly customized topside and subsea chemical packages compatible with advanced metallurgy and aggressive reservoir chemistry. The length and scope of such contracts underscore that chemical performance reliability is now embedded into field economics and project sanction decisions.

In parallel, suppliers are localizing complex chemical synthesis closer to end markets to reduce supply-chain risk and improve response times. Halliburton expanded its Chemical Reaction Plant at Saudi Arabia’s PlasChem Park to support Eastern Hemisphere sour gas developments. This facility is purpose-built to manufacture advanced corrosion and scale inhibitors on-site, reflecting a broader industry move toward regional chemical hubs that support long-life, high-complexity assets where failure costs are measured in millions of dollars per day.

Regulatory Enforcement Drives Mandatory Adoption of Environmentally Acceptable Lubricants

Environmental compliance in offshore and nearshore operations has transitioned from voluntary best practice to strict regulatory enforcement, fundamentally reshaping lubricant chemistry demand. Frameworks such as the U.S. EPA Vessel General Permit and the OSPAR Convention in the North Sea now mandate the use of Environmentally Acceptable Lubricants that meet biodegradability, low toxicity, and non-bioaccumulation thresholds defined under OECD 301B. These requirements have effectively eliminated mineral oil-based lubricants from critical oil-to-sea interfaces.

Under the U.S. EPA’s VGP rules, which faced intensified audits during 2024 and 2025, all commercial vessels over 79 feet operating within three miles of the U.S. coastline must deploy EALs in thrusters, stabilizers, and subsea hydraulic systems. This has created a structurally locked-in demand base for synthetic esters and advanced biodegradable fluids engineered to deliver long service life under high load and variable temperature conditions.

The strategic value of environmentally compliant specialty portfolios is also reshaping competitive dynamics. In April 2025, regulatory scrutiny by the UK Competition & Markets Authority surrounding SLB’s acquisition of ChampionX highlighted the importance of maintaining competitive access to eco-friendly production chemicals in the North Sea. This episode illustrates how environmental compliance is no longer peripheral but central to market access, asset valuation, and M&A strategy in offshore oil and gas.

Flow Assurance Chemicals Enable Ultra-Long Subsea Tieback Economics

Subsea tiebacks extending beyond 100 kilometers have emerged as a dominant strategy for maximizing returns on offshore capital by linking remote wells to existing infrastructure. However, these ultra-long flowlines significantly increase the risk of hydrate formation, wax deposition, and flow instability, creating a high-value opportunity for advanced flow assurance chemicals. Low-Dosage Hydrate Inhibitors have become the preferred solution due to their ability to prevent hydrate agglomeration at a fraction of the dosage required by traditional thermodynamic inhibitors.

Industry data from 2025 indicates that LDHI deployment can reduce energy consumption by up to 20% compared with methanol-based systems. Because LDHIs are effective at concentrations of 1 to 3% versus 20 to 50% for conventional inhibitors, they dramatically lower storage, transport, and handling requirements on offshore facilities. This efficiency gain directly translates into improved project economics for deepwater operators.

Operational results reinforce this value proposition. Halliburton reported in mid-2025 that more than 500 subsea control modules deployed in the Gulf of Mexico, integrated with advanced flow assurance chemical programs, supported average field uptime of 98% even in assets with complex hydrate and wax profiles. This positions LDHIs as a core enabling technology for future deepwater developments rather than a discretionary chemical spend.

Produced Water Recycling Creates the Largest Volume Opportunity in Unconventional Plays

Water management has become the defining operational challenge in unconventional oil and gas, particularly in the Permian Basin where daily produced water volumes exceed 22 million barrels. The industry is rapidly shifting from disposal-centric models to circular reuse strategies, transforming produced water from a liability into a strategic resource. This transition represents the single largest volumetric growth opportunity for specialty water treatment chemicals.

According to a March 2025 assessment by Texas Living Waters, between 50 and 60% of produced water in the Permian is already being recycled for hydraulic fracturing, with projections indicating this figure could reach 80% by 2030. Achieving this scale requires robust chemical programs incorporating specialty biocides, oxidizers, and scale inhibitors capable of performing in high-salinity slickwater systems with complex microbial loads.

While treatment costs of $0.75 to $1.50 per barrel exceed deep-well injection disposal costs of roughly $0.60 to $0.70 per barrel, regulatory pressure to curb induced seismicity linked to injection wells is shifting operator preference decisively toward recycling. Major producers such as Chevron and ExxonMobil are increasingly viewing chemical-enabled water reuse as the most sustainable long-term strategy. This dynamic locks specialty oilfield chemicals into the core economics of shale development, supporting durable, multi-year demand growth.

Specialty Oilfield Chemicals Market Share and Segmentation Insights

Inhibitors and Scavengers Lead Specialty Oilfield Chemicals Demand for Asset Protection and Flow Assurance

Inhibitors and scavengers accounted for 32.80% of the specialty oilfield chemicals market in 2025, reflecting their essential role in protecting oil and gas production infrastructure. These chemicals include corrosion inhibitors, scale inhibitors, and hydrogen sulfide scavengers, which prevent equipment degradation, mineral scaling, and sour gas hazards during oilfield operations. Continuous treatment is required across pipelines, wellbores, and processing facilities to maintain safe and efficient production. A major 2025 industry driver is the growing complexity of unconventional shale and tight oil production, where increasing water cuts and scaling risks require more advanced chemical treatment programs. Enhanced inhibitor technologies help operators control corrosion, manage scaling tendencies, and maintain production efficiency in mature unconventional reservoirs.

Production Chemicals Segment Drives Continuous Demand for Oilfield Chemical Treatment

Production chemicals represent the largest application segment in the specialty oilfield chemicals market, accounting for 42.80% of global demand in 2025 due to the ongoing need for chemical treatment throughout the operational life of oil and gas wells. These chemicals are used to control flow assurance issues, corrosion, scale formation, microbial growth, and emulsions in produced fluids. The high volumes of produced water and complex fluid chemistry encountered in modern oilfields require continuous chemical dosing to maintain production efficiency. A key 2025 industry trend is the adoption of real-time chemical monitoring and automated dosing systems, where digital sensors track corrosion rates, scaling potential, and microbial activity, allowing operators to optimize chemical usage while improving operational safety and reducing treatment costs.

Specialty Oilfield Chemicals Market Competitive Landscape

The global specialty oilfield chemicals market in 2026 is shaped by consolidation, digital-chemical integration, and carbon-neutral production chemistry. Tier-1 players are advancing real-time chemical dosing, enhanced oil recovery (EOR) formulations, and automated well optimization platforms to improve asset productivity and reduce lifecycle emissions.

SLB Integrates ChampionX to Build $400 Million Synergy Production Chemistry Ecosystem with Real-Time Digital Injection Systems

SLB has established market dominance following its 2025 acquisition of ChampionX, unlocking $400 million in annual pre-tax synergies by 2028. The combined portfolio integrates corrosion inhibitors, scale inhibitors, and artificial lift technologies into a unified production optimization system. Its ESP Digital Ecosystem enables real-time monitoring of chemical performance and equipment diagnostics to prevent failures and optimize dosing. Strategic divestments and licensing agreements have streamlined regulatory approvals while preserving technology access. The company’s pore-to-pipeline model combines digital analytics with specialty chemicals to enhance oil recovery efficiency. This integration strengthens SLB’s leadership in production-focused oilfield chemistry.

Halliburton Advances Digital Well Construction and Stimulation Chemistry with Automated Reservoir Targeting and Asia Expansion

Halliburton is strengthening its specialty oilfield chemicals portfolio through digital well construction and advanced stimulation technologies. Its collaboration with ExxonMobil achieved the first fully automated closed-loop geological well placement, integrating drilling fluids with digital systems for precision targeting. Expansion into Indonesia through a partnership with Pertamina supports deployment of unconventional fracturing chemistries. The NEX Lab℠ in Singapore accelerates R&D for next-generation completion fluids and specialty additives. The company reported a 13% operating margin on $5.7 billion revenue in 2025, reflecting strong financial performance. Its focus on digital automation and chemical innovation enhances efficiency in complex reservoirs.

Baker Hughes Expands CCUS and Hydrogen-Focused Chemical Solutions with Industrial Technology Growth and 20% Margin Target

Baker Hughes is repositioning its specialty chemical portfolio toward industrial and energy transition applications, particularly CCUS and hydrogen infrastructure. Its Industrial & Energy Technology segment delivered record EBITDA in 2025, with non-LNG orders accounting for 85% of total demand. Climate Technology Solutions saw a 23% increase in orders, driven by emissions reduction and hydrogen transport applications. The company’s supply of BRUSH™ generators supports grid resilience, requiring advanced corrosion inhibitors and industrial fluids. Baker Hughes is targeting a 20% EBITDA margin by 2026 through a solution-based service model. Its diversification into low-carbon technologies strengthens its long-term competitiveness.

Clariant Enhances Digital Oilfield Chemistry with CLARITY™ Platform and High-Margin Performance in Brazil Operations

Clariant Oil Services is advancing its specialty oilfield chemicals business through digital monitoring and sustainability-focused solutions. Its CLARITY™ platform has expanded to over 800 users across 38 countries, enabling real-time optimization of chemical performance and pipeline integrity. Recognition from Petrobras as a top supplier highlights its operational excellence in key markets. The company achieved a 17.8% EBITDA margin in 2025, supported by cost-saving initiatives and performance improvement programs. Strategic focus on high-value specialty additives enhances profitability despite flat sales expectations. Clariant’s integration of digital tools with chemical solutions strengthens its position in production optimization.

Solenis Expands Global Water and Oilfield Chemical Platform Through NCH Acquisition and 360-Degree Service Integration

Solenis is scaling its presence in specialty oilfield chemicals through the acquisition of NCH Corporation, adding 24 manufacturing plants and 76 distribution centers. The integration creates a comprehensive platform combining industrial water treatment and specialty chemical services across 48 countries. Its strategy focuses on digital water management and sustainable chemical solutions for oilfield and industrial applications. The company is targeting cross-selling opportunities in North America’s middle-market segment. Backed by Platinum Equity, Solenis continues aggressive M&A to consolidate fragmented markets. Its on-site service model enhances customer engagement and operational efficiency in chemical applications.

United States Specialty Oilfield Chemicals Market Reshaped by Consolidation and Horizontal Complexity

The United States specialty oilfield chemicals market is undergoing a structural transformation driven by consolidation, automation, and increasingly complex reservoir architectures. In July 2025, SLB received final regulatory clearance for its $8 billion acquisition of ChampionX, creating one of the most vertically integrated production-chemicals platforms globally. The combined entity is focused on embedding chemical automation, digital monitoring, and predictive analytics directly into production workflows, particularly across aging assets in the Permian Basin. This integration is redefining the value proposition of oilfield chemicals, shifting from standalone formulations to outcome-based chemical systems that optimize flow assurance, corrosion control, and water management.

Operational intensity continues to rise. With U.S. crude production reaching 13.2 million barrels per day in late 2024, operators are drilling longer horizontal laterals, increasing the need for advanced friction reducers, proppant transport aids, and rheology modifiers that remain stable under extreme shear and salinity. Infrastructure investment is following this trend. In August 2025, Cathedral Holdings commissioned a dedicated technical laboratory in The Woodlands, Texas, focused on basin-specific chemical design for the Midland and Delaware sub-basins. Regulatory pressure is also reshaping formulations. The EPA’s 2025 offshore drilling fluid criteria have accelerated the replacement of legacy biocides with biodegradable antimicrobial systems, while the expansion of the 45Q tax credit is stimulating demand for CO2-EOR chemicals and carbon capture compatible corrosion inhibitors.

Saudi Arabia Specialty Oilfield Chemicals Market Anchored in Localization and HTHP Reservoirs

Saudi Arabia’s specialty oilfield chemicals industry is strategically aligned with localization, gas expansion, and extreme reservoir conditions. Halliburton continues to scale its Chemical Reaction Plant at PlasChem Park in Jubail, positioning the facility as a cornerstone of in-kingdom production for drilling, completion, and water-treatment chemicals. This site supports Saudi Arabia’s objective to localize the full oilfield chemicals value chain, reducing import reliance while improving supply security for large-scale upstream projects.

The In-Kingdom Total Value Add program is a decisive market shaper. Under IKTVA requirements, international suppliers must increase local manufacturing content, prompting several European and U.S. specialty chemical firms to announce new blending and reaction facilities in late 2025 to support developments such as the Jafurah unconventional gas field. From a technical perspective, Saudi reservoirs are driving innovation in high-temperature, high-pressure chemistries. New surfactant and scale-inhibitor systems capable of maintaining performance beyond 150°C were highlighted by industry experts ahead of 2026 regional technical forums, underscoring the kingdom’s role as a proving ground for next-generation oilfield chemical formulations.

India Specialty Oilfield Chemicals Market Driven by Refining Expansion and Mature Fields

India’s specialty oilfield chemicals market is expanding in parallel with national energy infrastructure investments and enhanced recovery requirements. Under the National Infrastructure Pipeline, over $60 billion has been earmarked for oil refining and petrochemical capacity additions through 2025–2026, directly increasing demand for specialty catalysts, process chemicals, and crude treatment additives. This downstream expansion is reinforcing upstream chemical demand, particularly for demulsifiers, corrosion inhibitors, and fouling control agents.

Upstream, India’s push to raise domestic crude production is accelerating the deployment of Improved Oil Recovery techniques across mature assets operated by ONGC. This shift has driven a measurable increase in demand for asphaltene inhibitors, water clarifiers, and polymer-based mobility control agents. Policy support is reinforcing localization. The PCPIR framework and PLI-linked bio-foundry initiatives are encouraging the development of greener oilfield chemistries, while refiners such as Reliance Industries and Indian Oil Corporation are scaling eco-friendly specialty chemical production to comply with tightening domestic environmental mandates.

China Specialty Oilfield Chemicals Market Defined by Gas Growth and Digital Injection

China’s specialty oilfield chemicals industry is increasingly shaped by natural gas expansion and digital oilfield integration. Under the 14th Five-Year Plan, natural gas demand reached approximately 430 billion cubic meters by 2025, intensifying drilling and completion activity in complex shale and tight gas formations. This growth has increased reliance on high-performance drilling fluids, shale inhibitors, and thermal-stable friction reducers tailored for deep and geologically challenging reservoirs.

At the policy level, the Ministry of Industry and Information Technology issued directives in early 2025 to curb oversupply in basic chemicals, pushing state-owned players such as Sinopec toward higher-margin specialty polymers and oilfield chemicals, including deepwater corrosion inhibitors and specialty cement additives. China is also advancing digital chemical management. In late 2025, major fields in Bohai Bay implemented IoT-enabled dosing systems integrated with AI models to predict scaling and corrosion in real time, enabling precision chemical injection and reducing overall chemical consumption while improving asset integrity.

Guyana Specialty Oilfield Chemicals Market Emerging Through Offshore Scale

Guyana has rapidly emerged as a high-growth offshore market for specialty oilfield chemicals, driven by deepwater project execution. In February 2025, Baker Hughes secured a multi-year contract from ExxonMobil Guyana to supply a full suite of specialty production chemicals for the Uaru and Whiptail developments. These projects are central to Guyana’s ambition to reach 1.3 million barrels per day of production by late 2026.

The scope of supply extends beyond production chemicals to include subsea, water injection, and utility chemistries for multiple FPSO units. This integrated logistics and chemical management model highlights the growing importance of offshore-specific formulations such as hydrate inhibitors, oxygen scavengers, and biocides engineered for long subsea tiebacks. Guyana’s offshore growth trajectory is positioning it as a reference market for scalable, FPSO-centric oilfield chemical programs.

Comparative Snapshot: Specialty Oilfield Chemicals Industry by Country

Specialty Oilfield Chemicals Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Demand Drivers

|

Market Positioning

|

|

United States

|

Production optimization and automation

|

Horizontal drilling, 45Q incentives

|

Technology-led global benchmark

|

|

Saudi Arabia

|

Localization and HTHP performance

|

IKTVA, gas field development

|

High-volume, in-kingdom hub

|

|

India

|

Refining growth and IOR

|

NIP investments, mature fields

|

Rapidly localizing market

|

|

China

|

Gas expansion and digital dosing

|

Shale gas, AI-enabled injection

|

Efficiency-driven scale player

|

|

Guyana

|

Offshore FPSO development

|

Deepwater production growth

|

High-growth emerging market

|

Specialty Oilfield Chemicals Market Report Scope

Specialty Oilfield Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.5 Billion

|

|

Market Size (2034)

|

$21.5 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Product Type (Inhibitors and Scavengers, Rheology Modifiers, Demulsifiers and Surfactants, Friction Reducers, Specialty Biocides, Pour Point Depressants, Foamers and Defoamers, Fluid Loss Control Agents), By Application (Drilling Fluids, Production Chemicals, Well Stimulation, Enhanced Oil Recovery, Cementing and Workover), By Location (Onshore, Offshore)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SLB, Baker Hughes Company, Halliburton Company, ChampionX Corporation, BASF SE, Clariant AG, Dow Inc., Nalco Champion, Nouryon, Solvay S.A., Kemira Oyj, Innospec Inc., Lubrizol Corporation, Huntsman Corporation, Fineotex Chemical Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Oilfield Chemicals Market Segmentation

By Product Type

- Inhibitors and Scavengers

- Rheology Modifiers

- Demulsifiers and Surfactants

- Friction Reducers

- Specialty Biocides

- Pour Point Depressants

- Foamers and Defoamers

- Fluid Loss Control Agents

By Application

- Drilling Fluids

- Production Chemicals

- Well Stimulation

- Enhanced Oil Recovery

- Cementing and Workover

By Location

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Oilfield Chemicals Industry

- SLB

- Baker Hughes Company

- Halliburton Company

- ChampionX Corporation

- BASF SE

- Clariant AG

- Dow Inc.

- Nalco Champion

- Nouryon

- Solvay S.A.

- Kemira Oyj

- Innospec Inc.

- Lubrizol Corporation

- Huntsman Corporation

- Fineotex Chemical Limited

*- List not Exhaustive